I actually do think the FED needs to be careful because, with enough and consistent momentum to the downside, the economy could fall into deflation pretty fast.

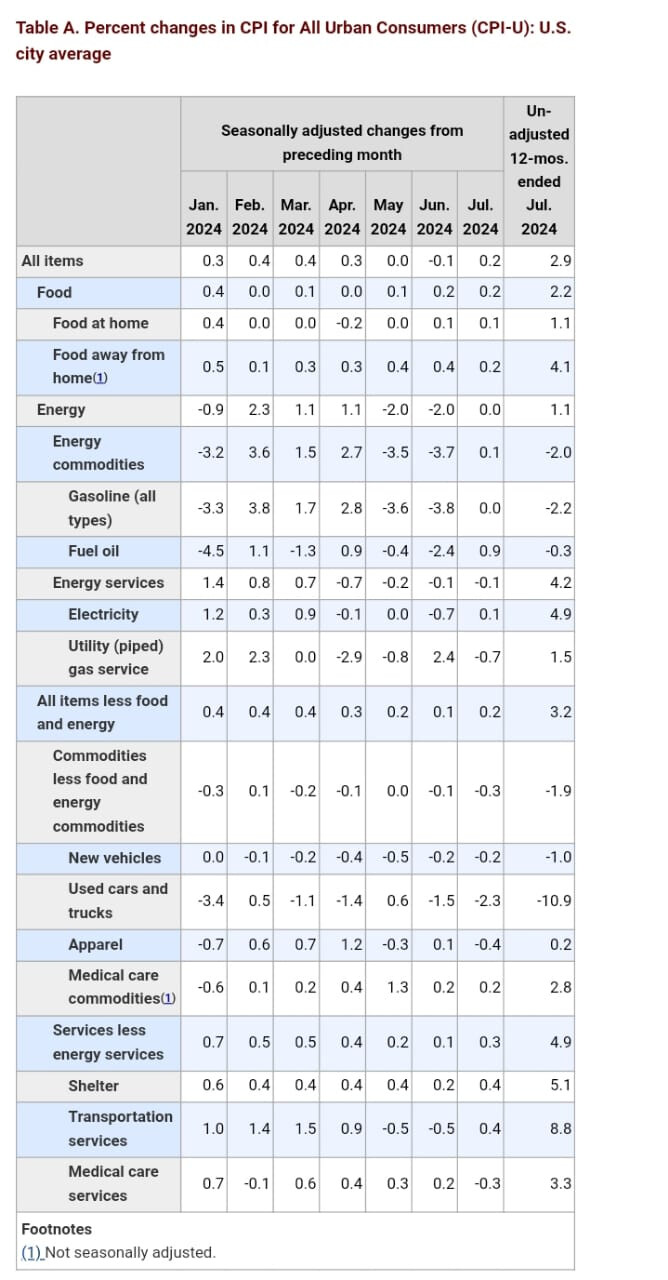

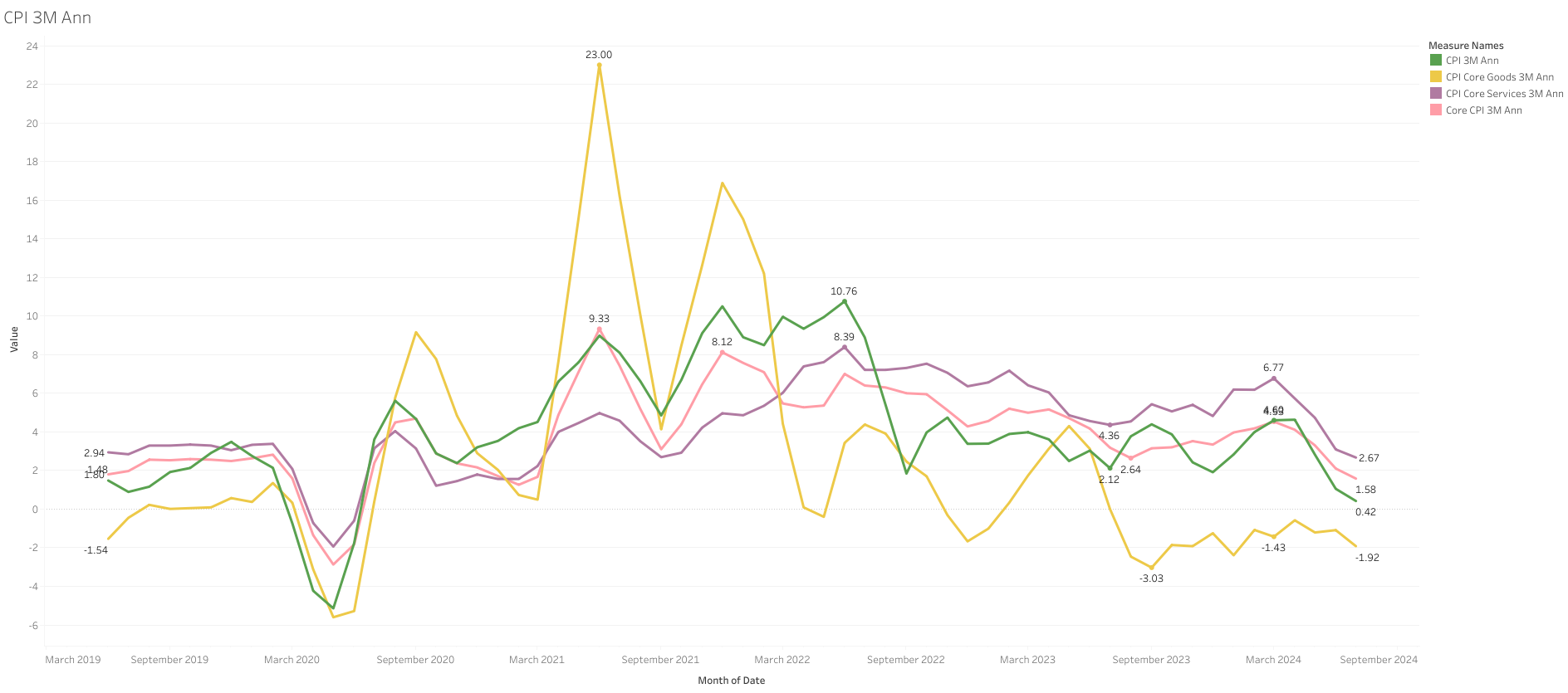

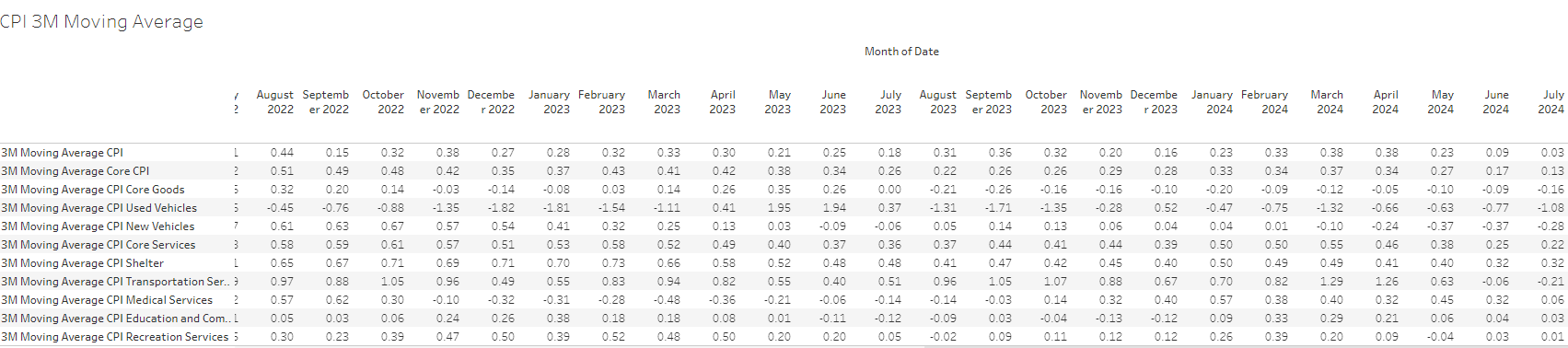

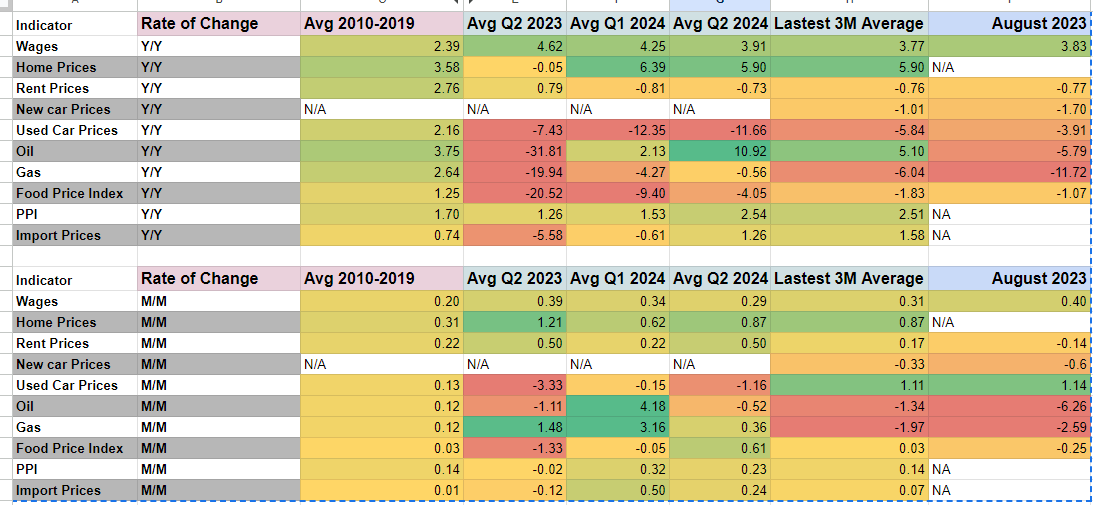

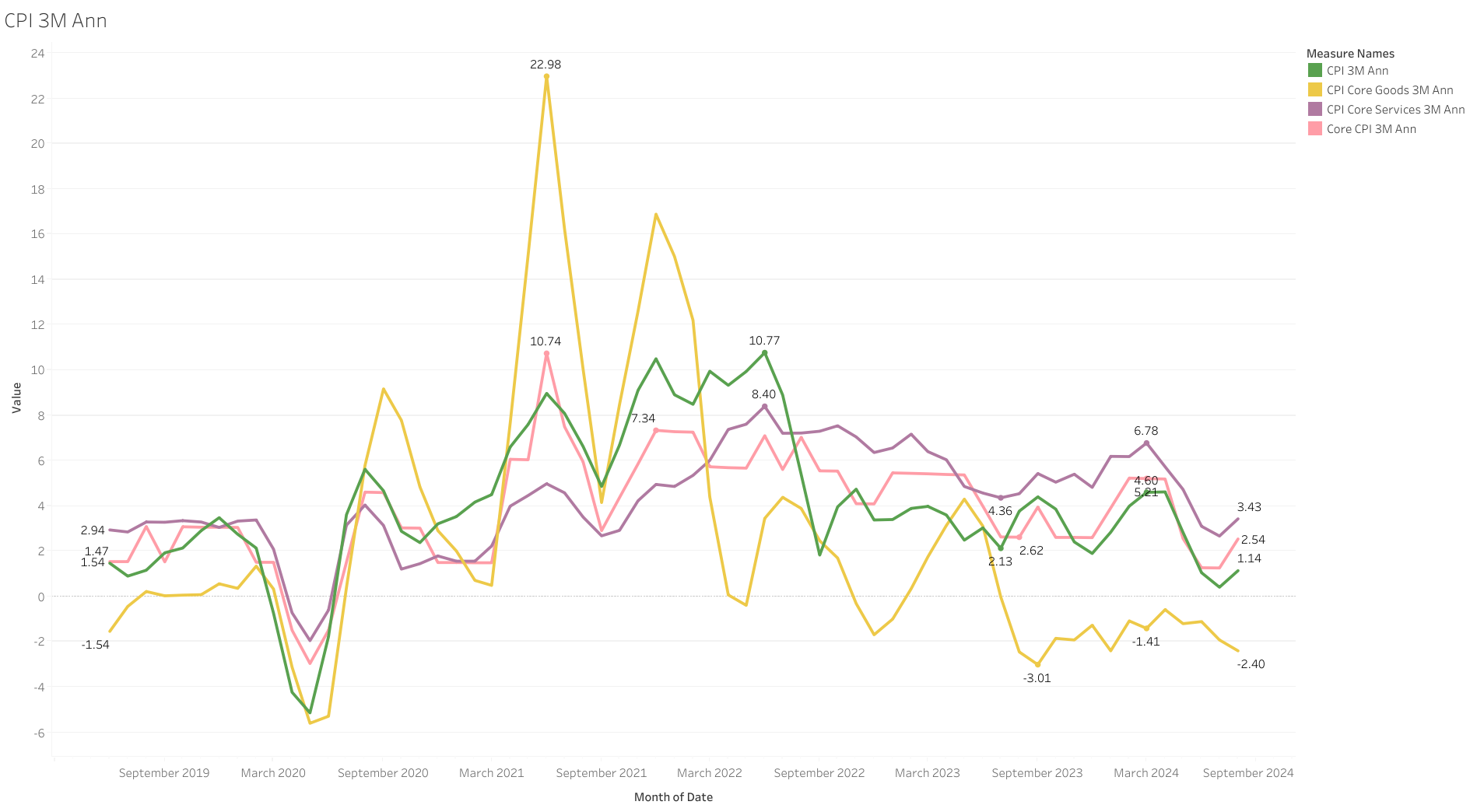

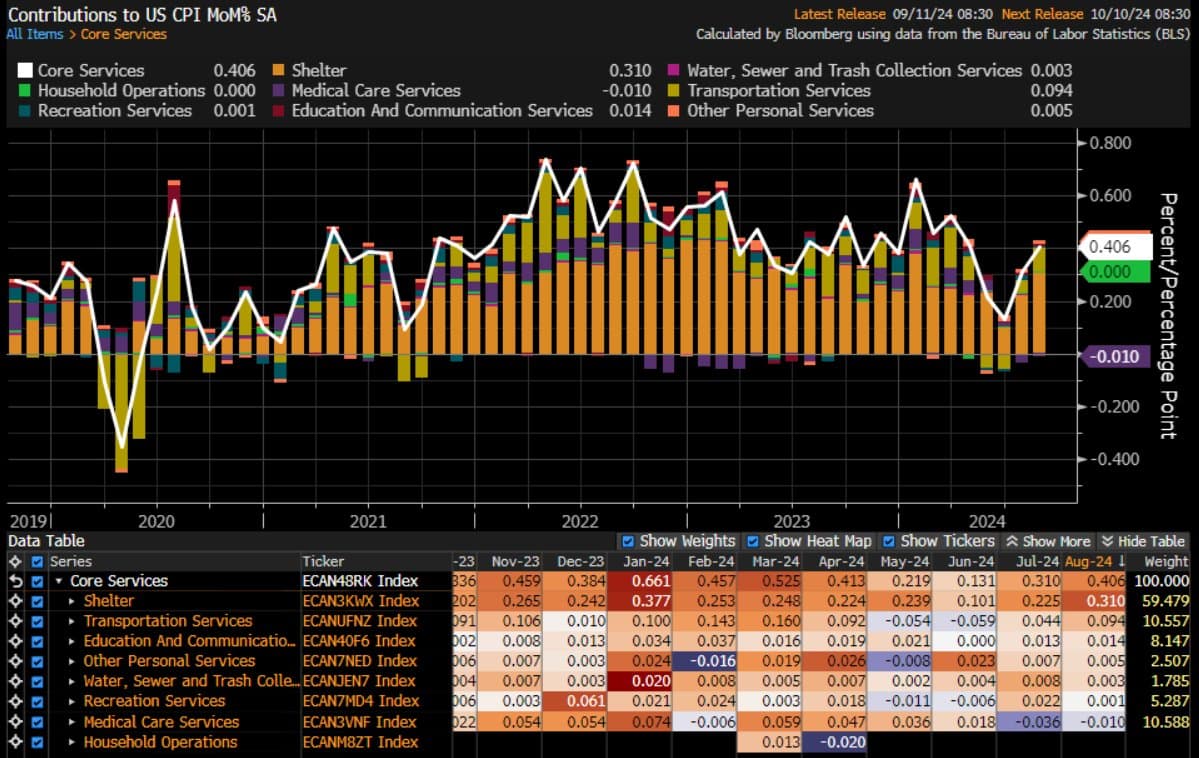

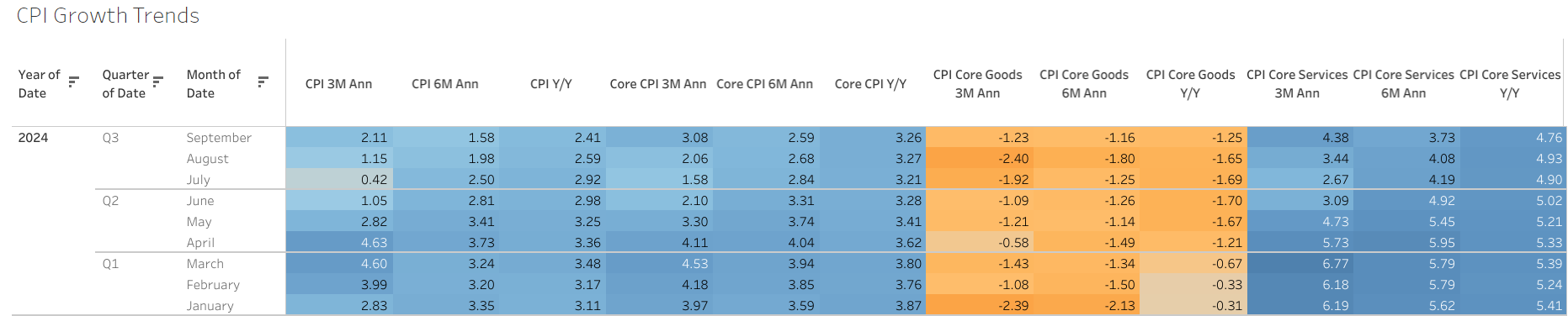

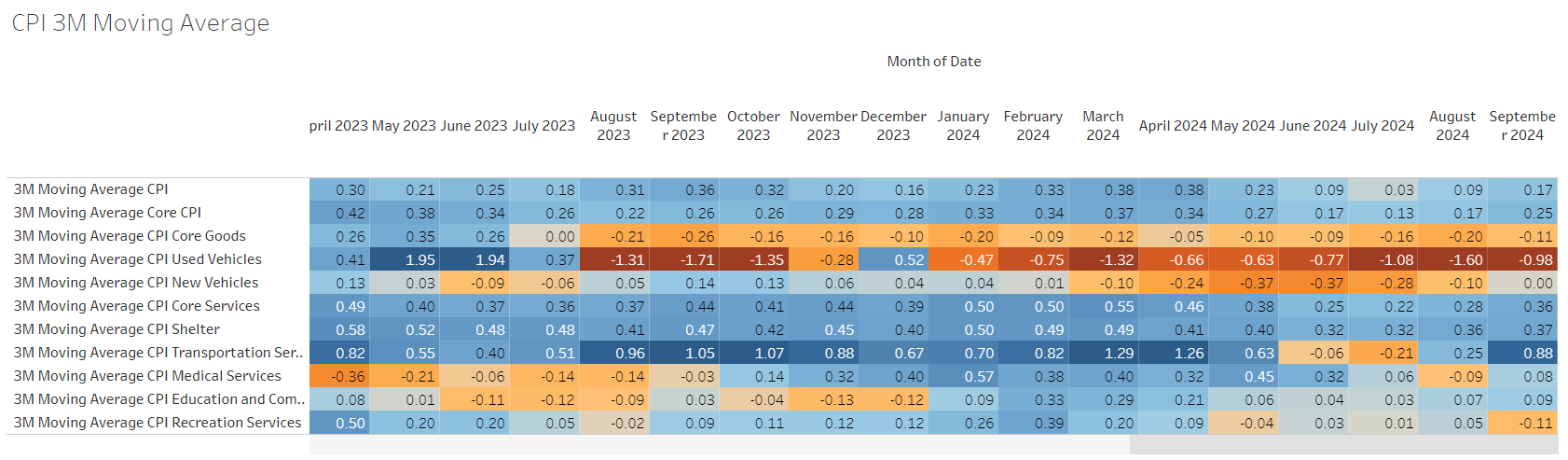

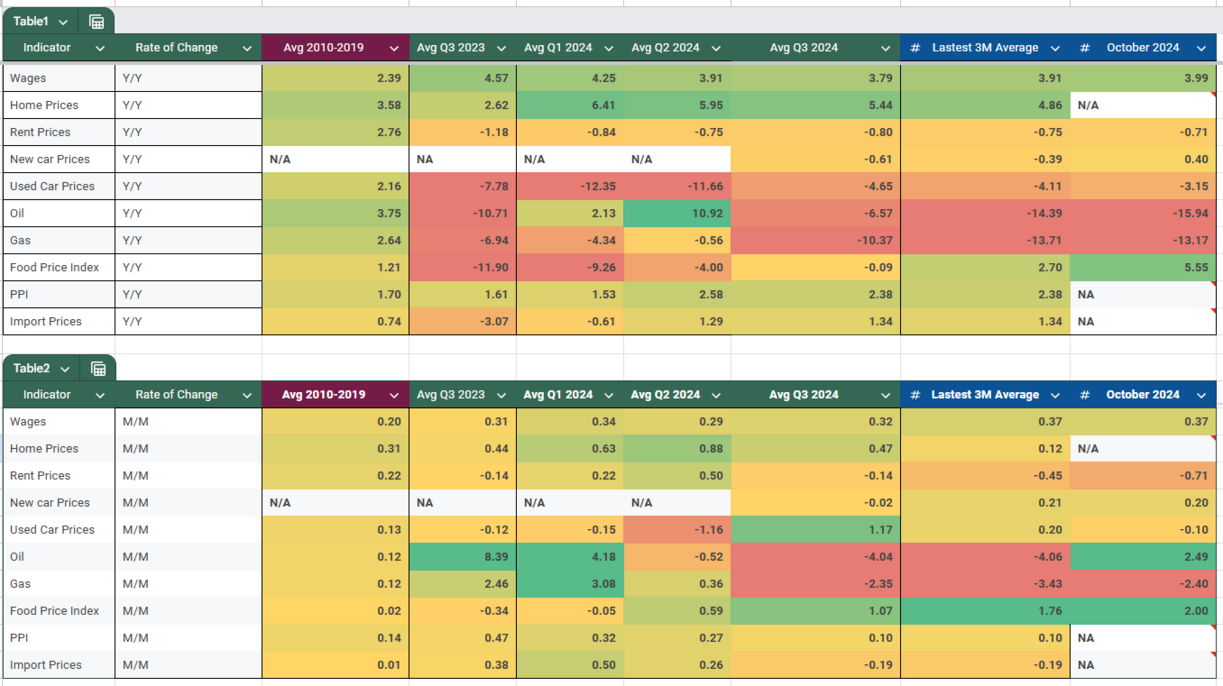

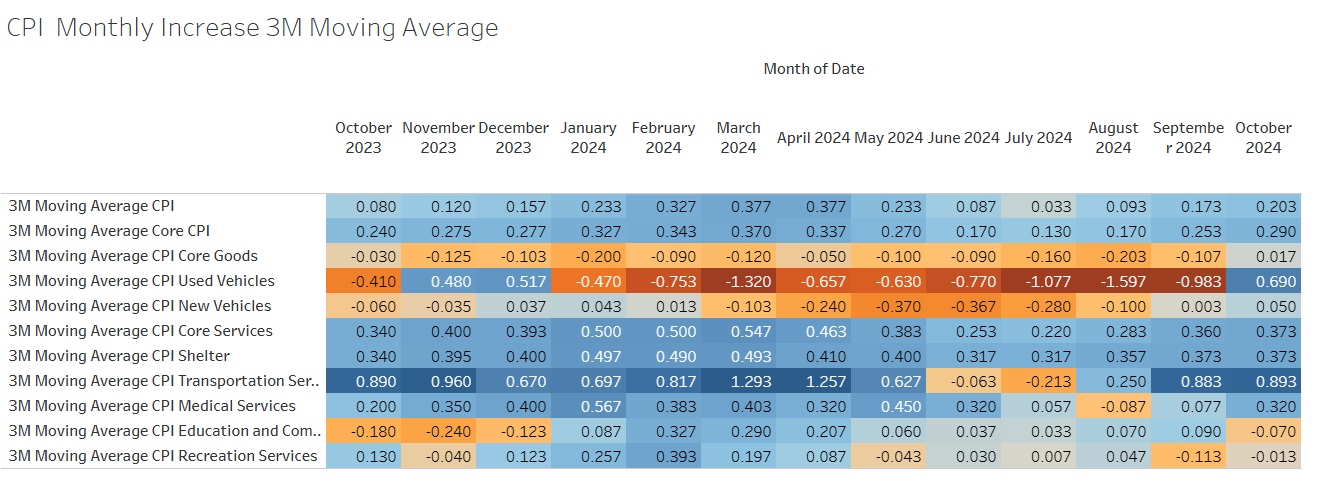

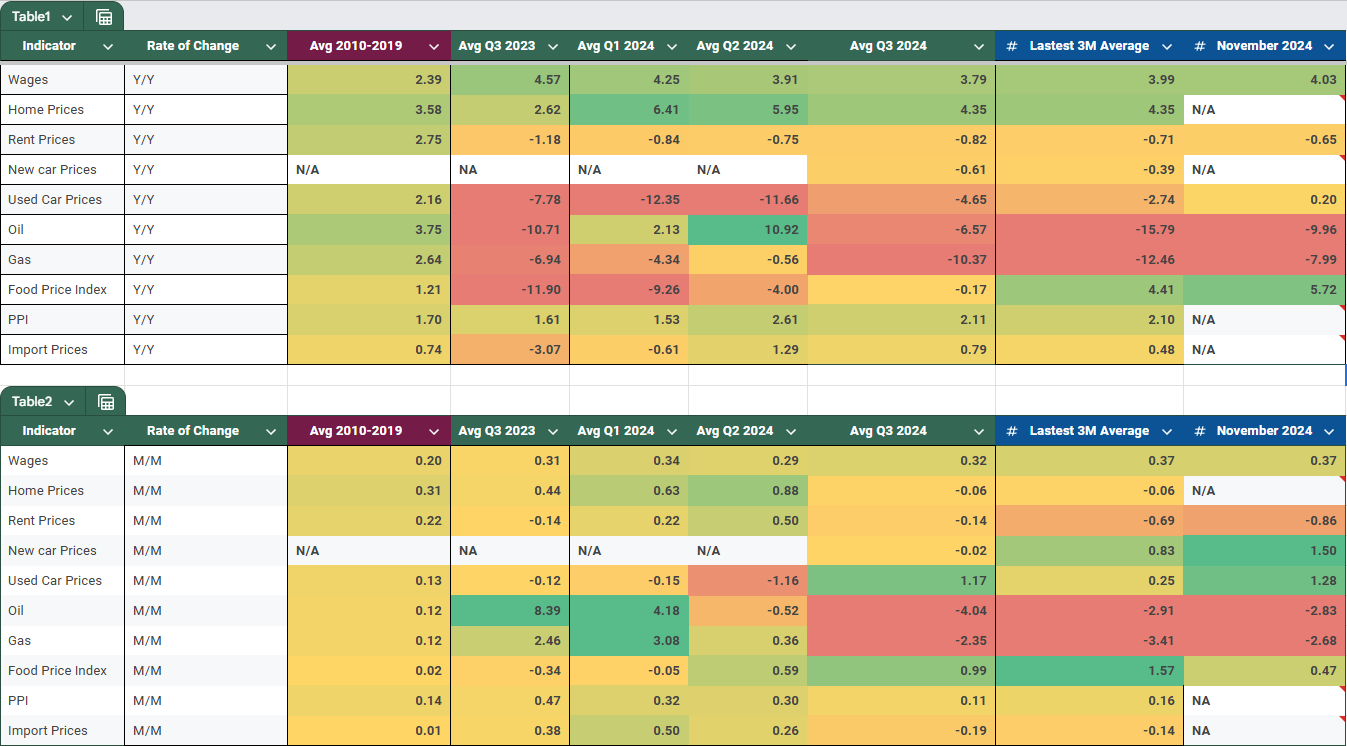

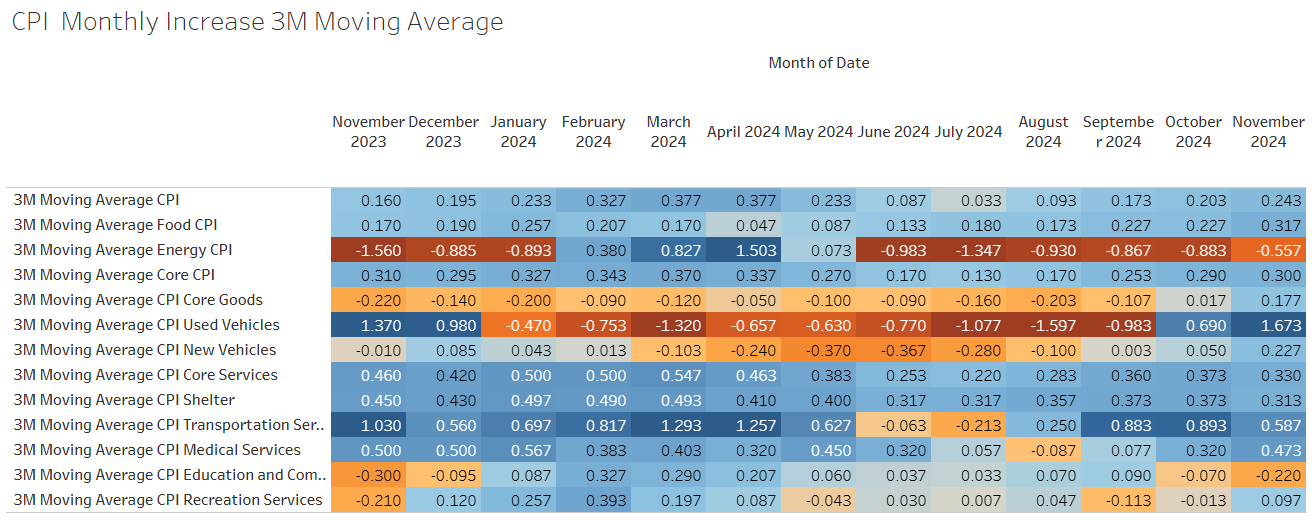

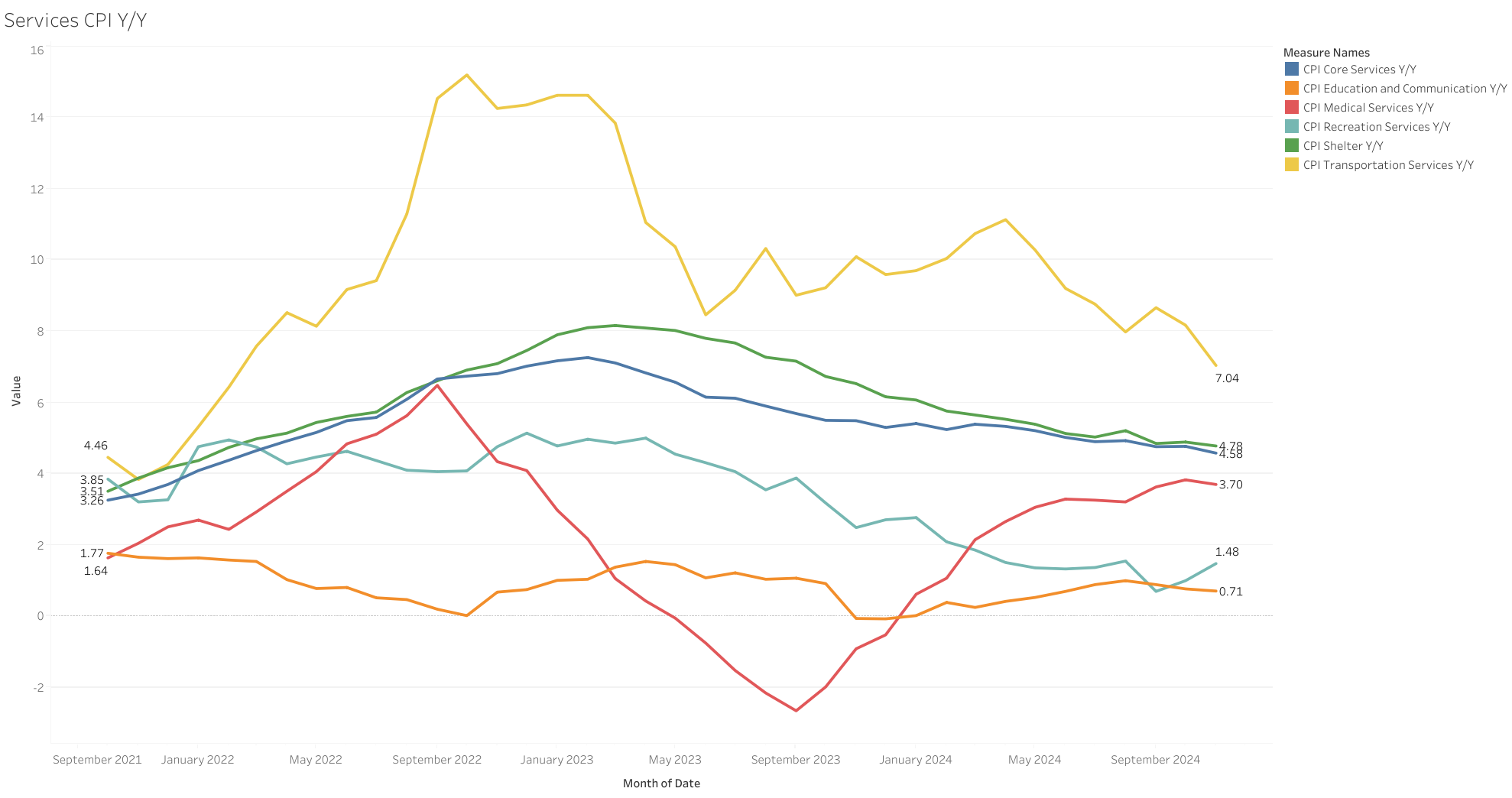

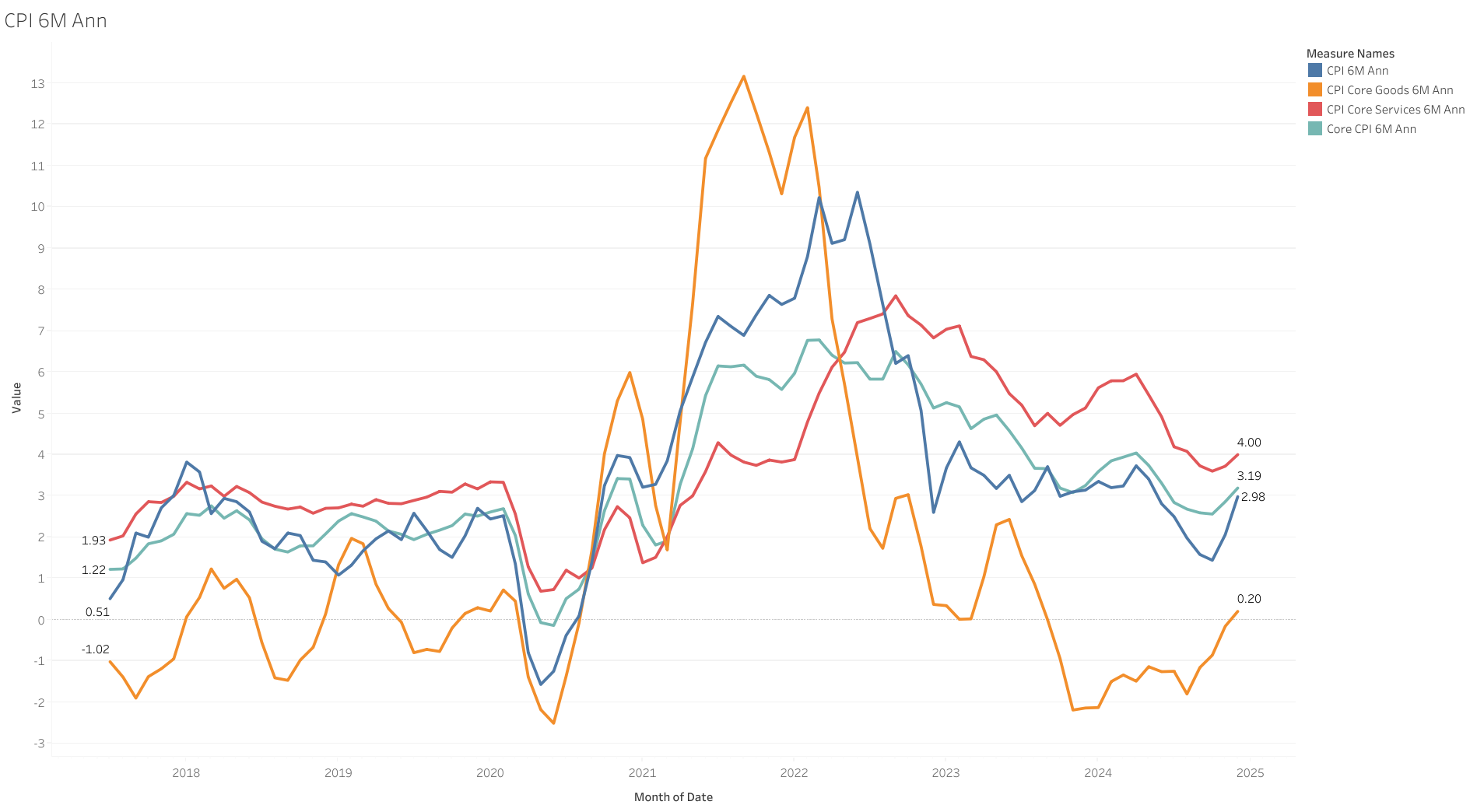

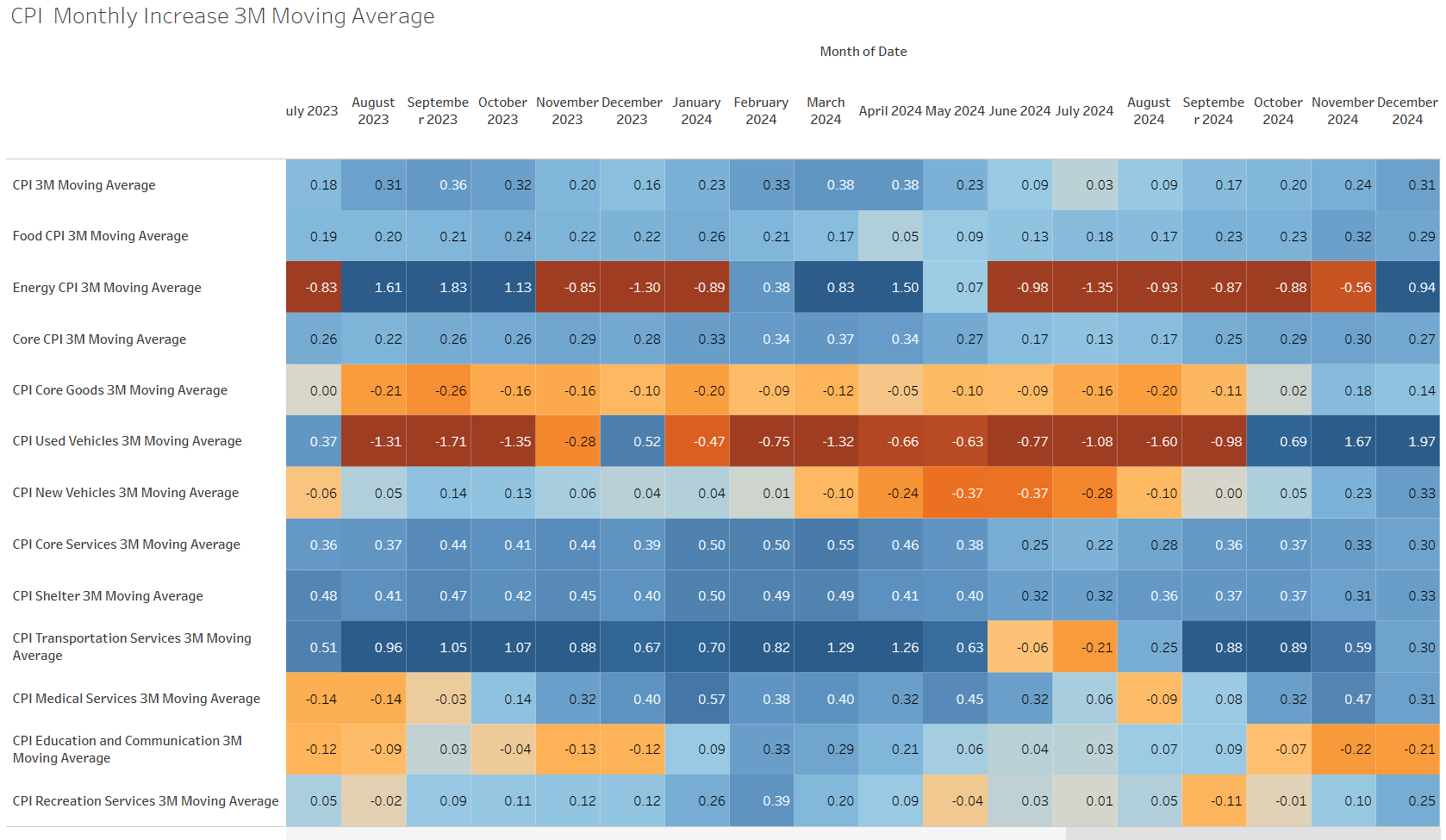

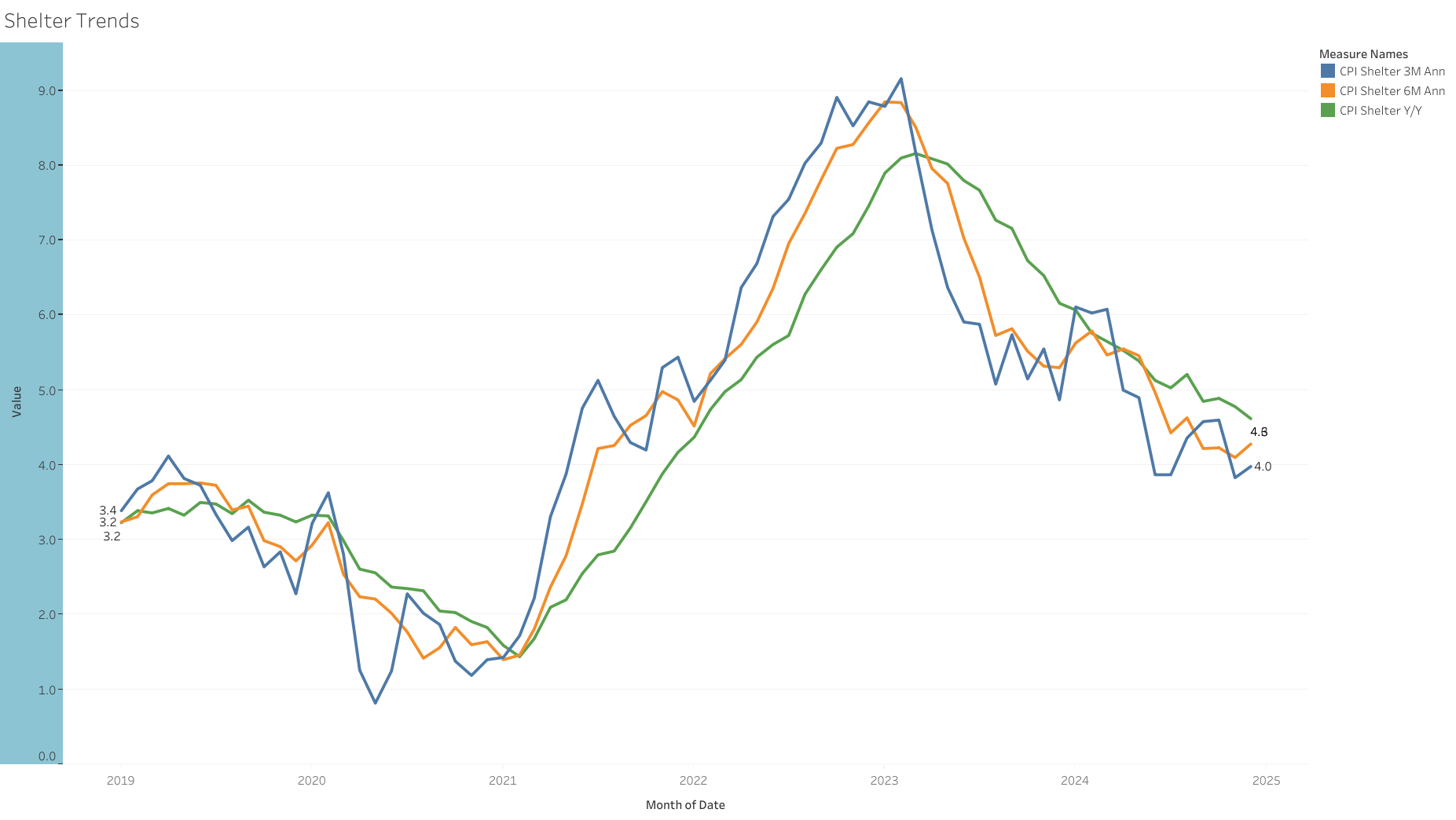

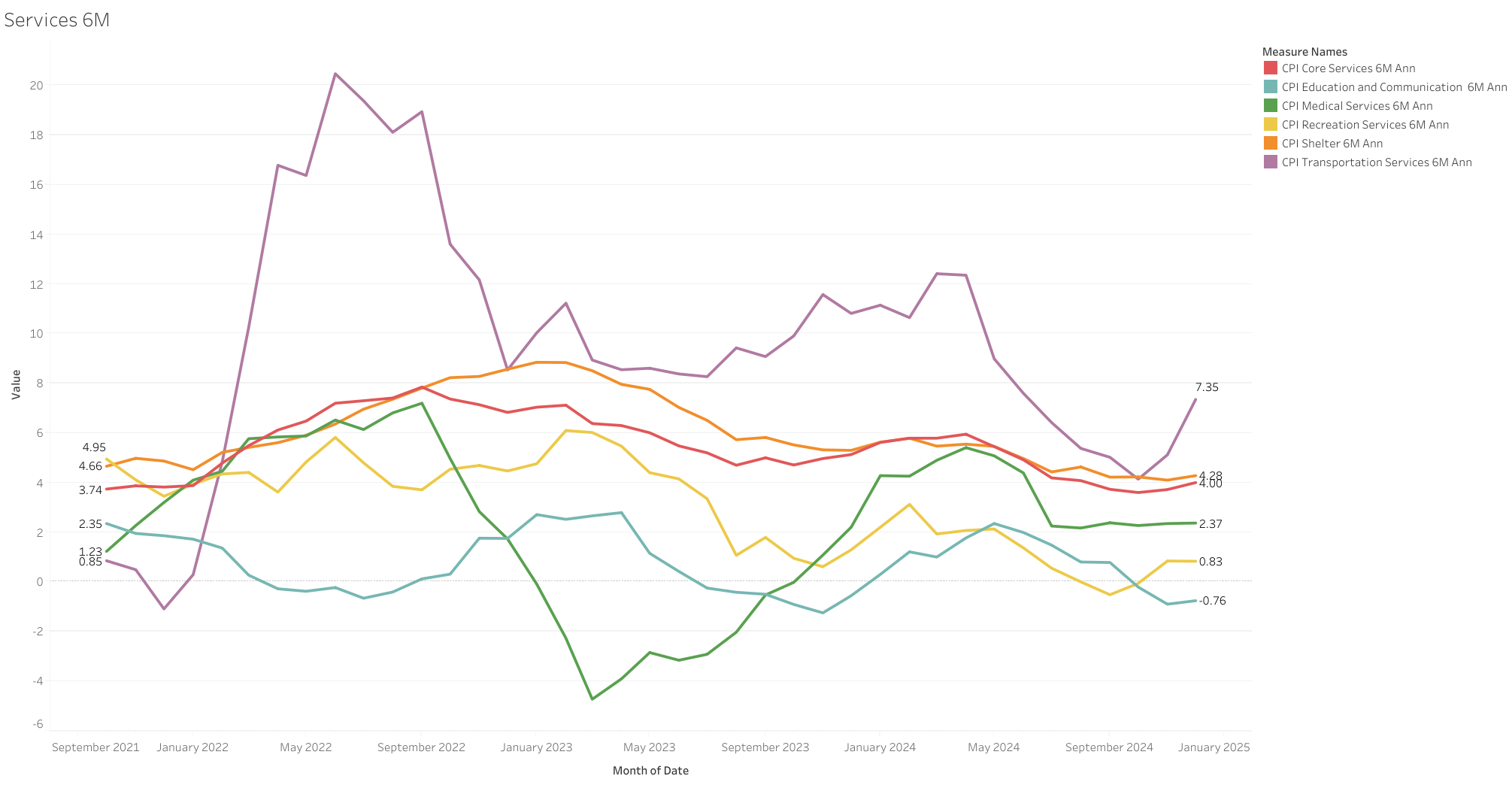

The 3 month average increase of most important components are close to zero or negative, the only significantly higher is shelter.

However this report coming in line with estimates makes think 25bps is more likely in September than 50 bps, and I think the current 100 bps of cuts for 2024 are too aggressive unless the labor market continues to slow.

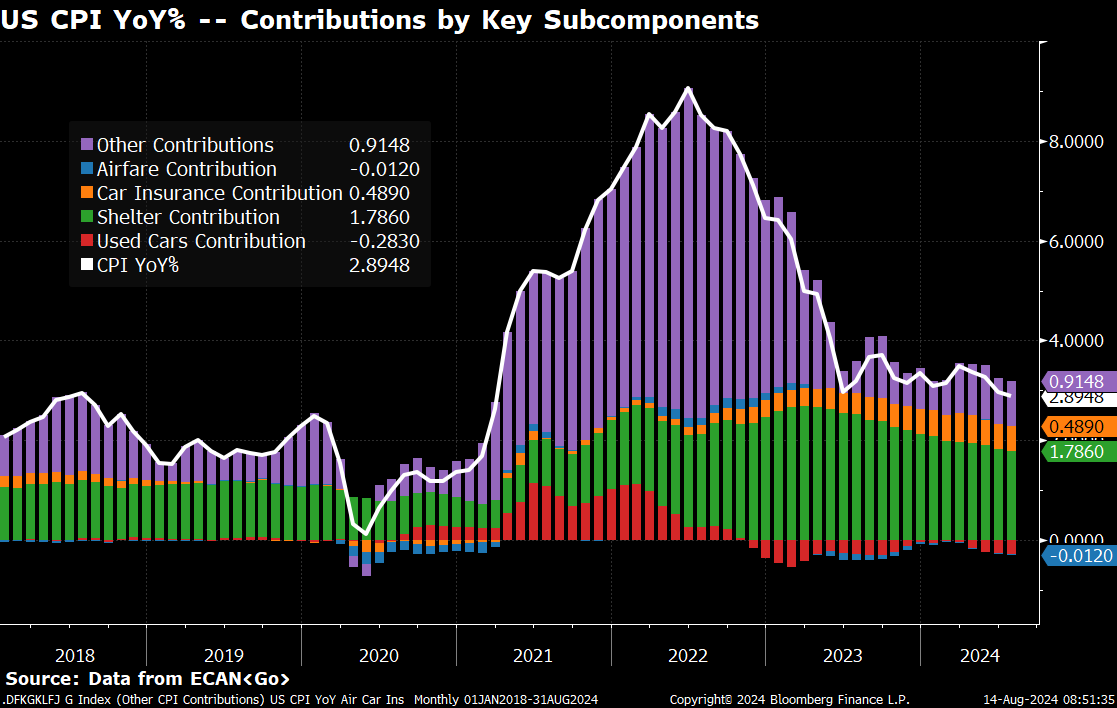

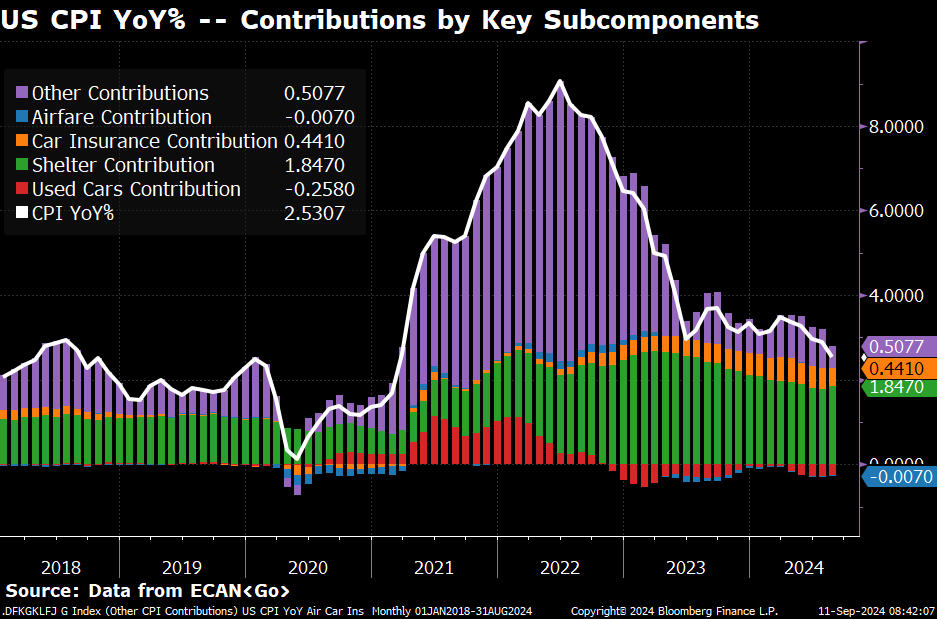

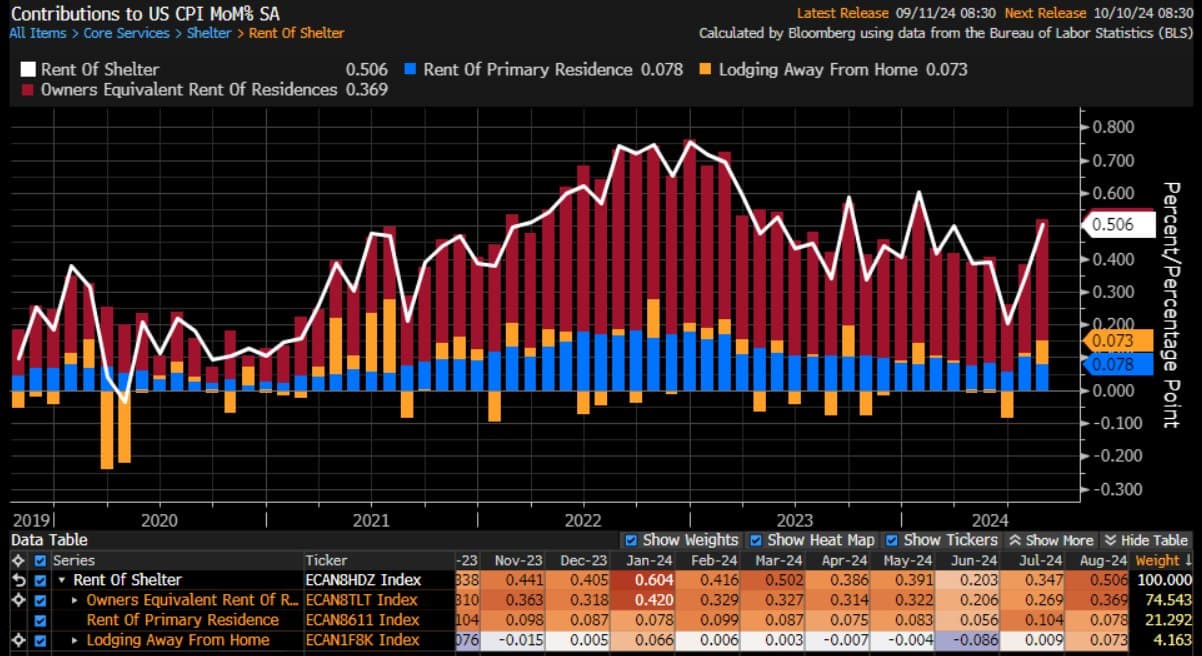

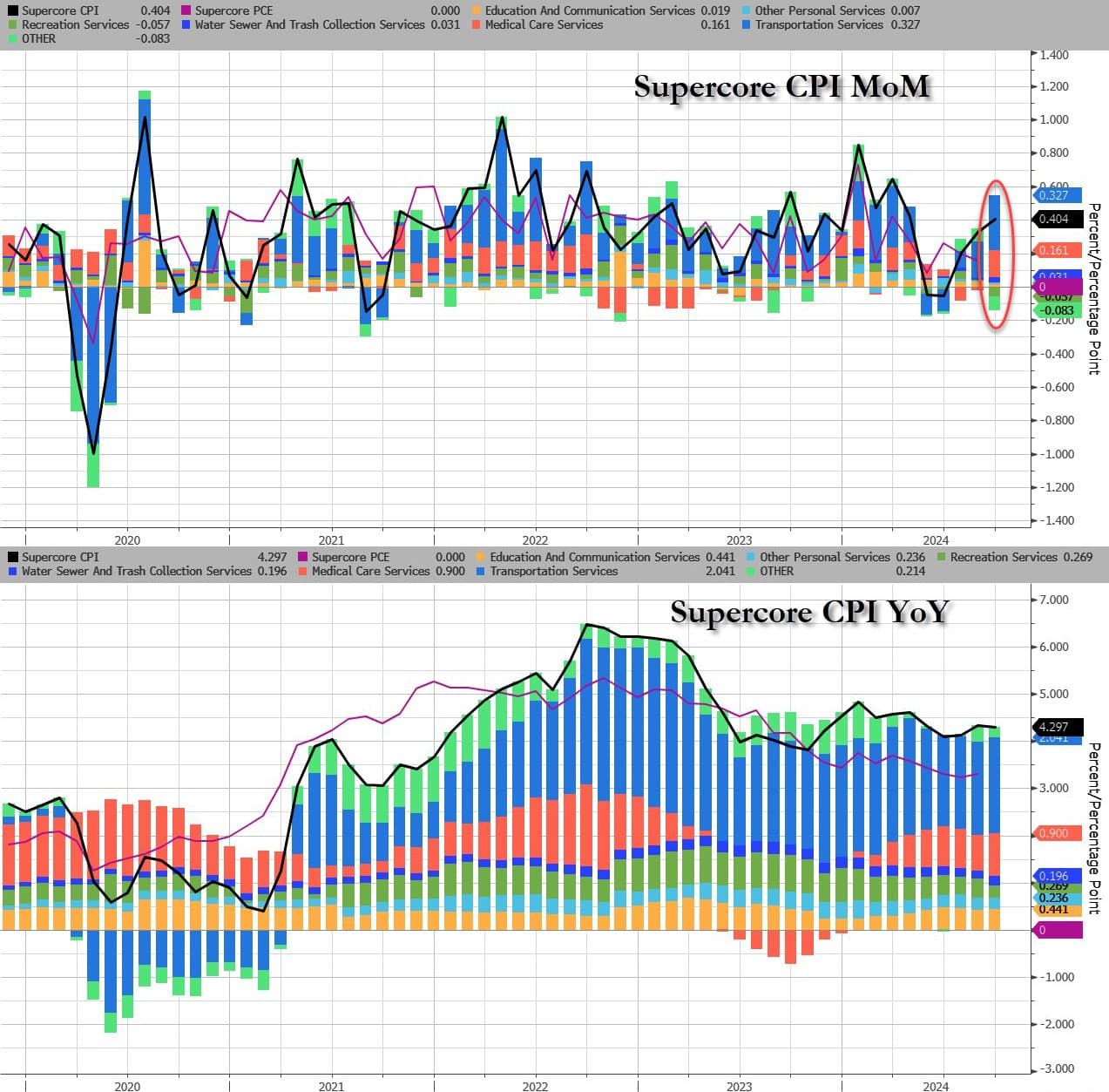

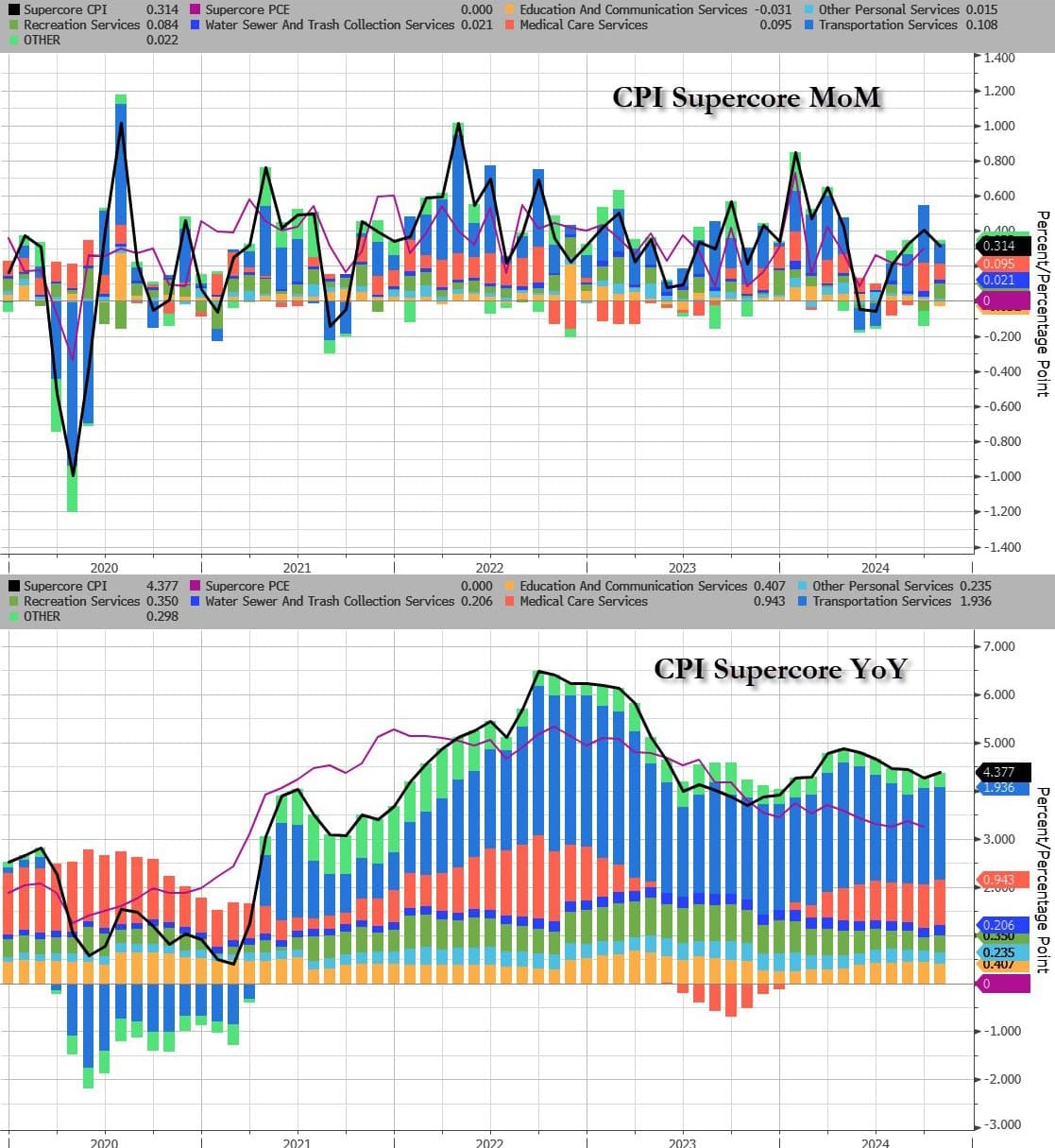

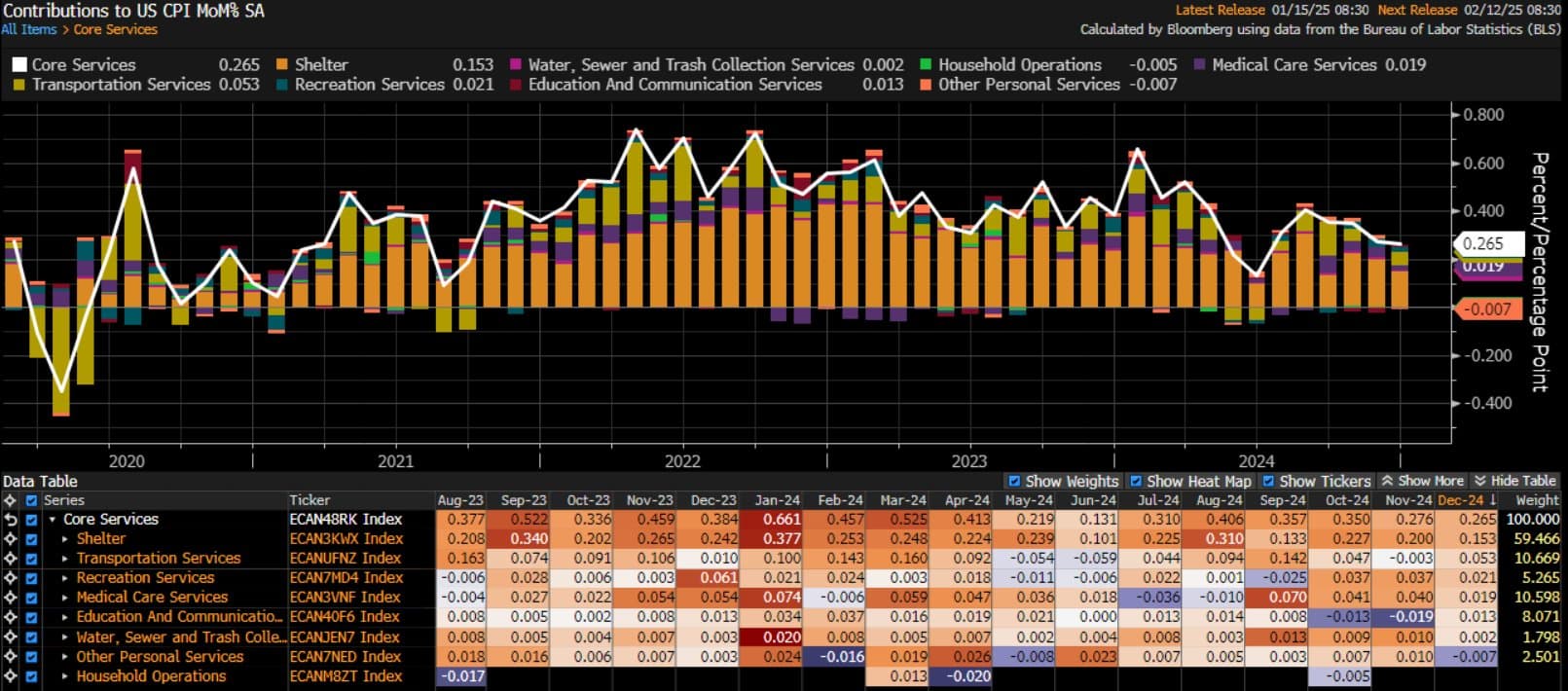

In terms of contribution shelter continues to be the driver of current inflation.

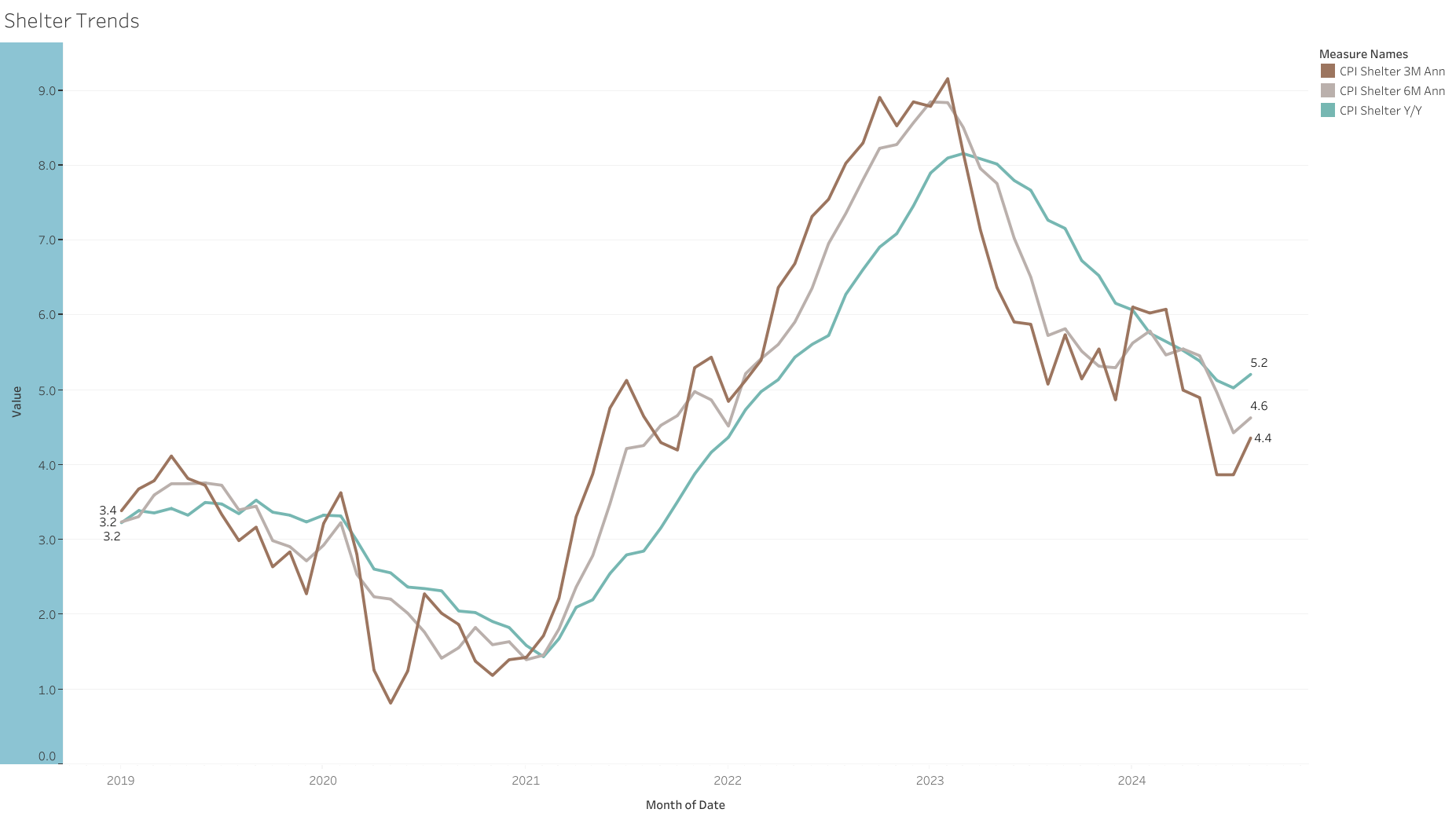

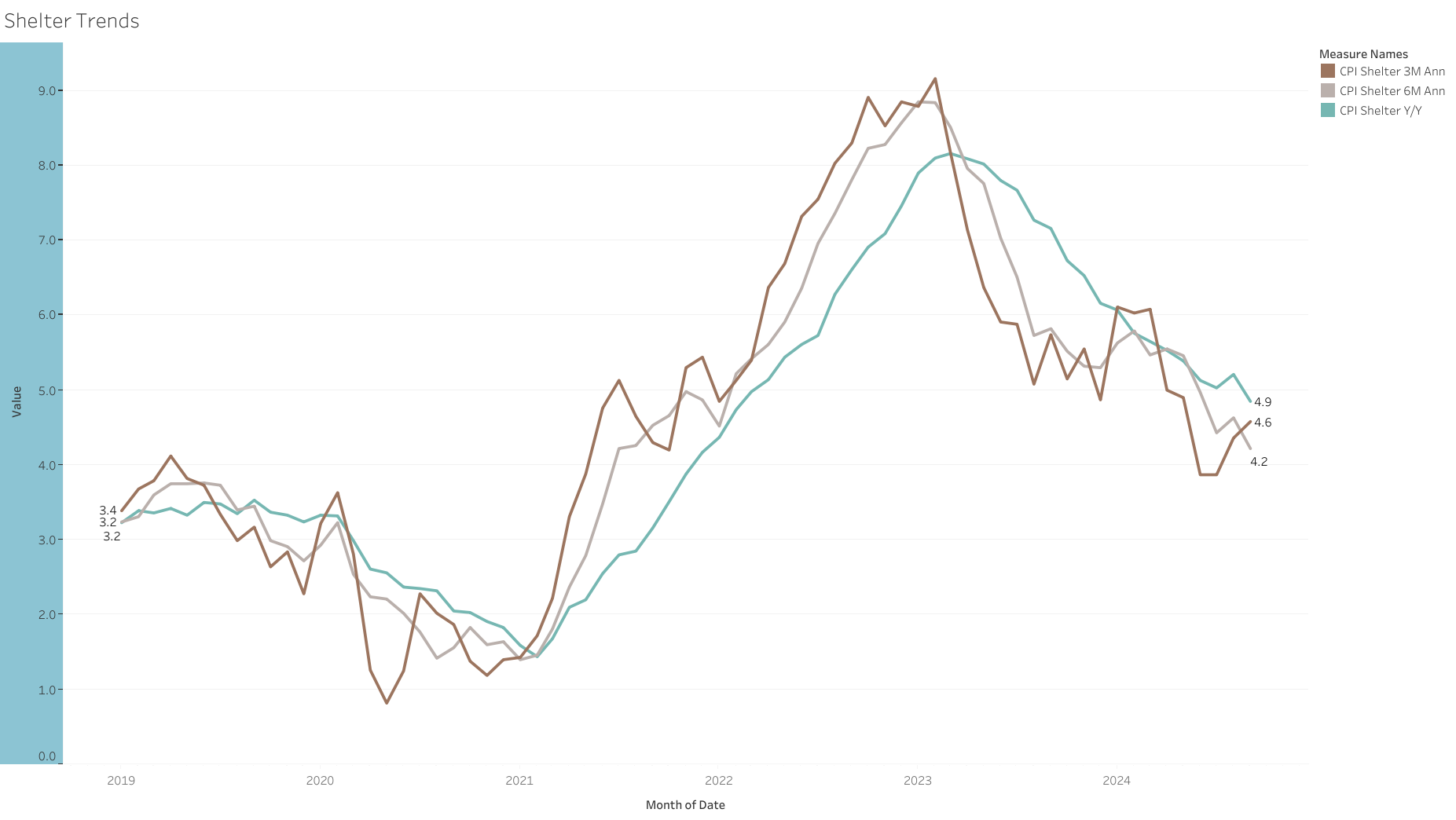

While shelter is slowly coming back down, I think is being extremely slower than expected, and will most likely continue to contribute to stickier services inflation.

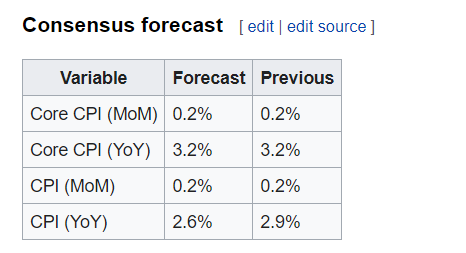

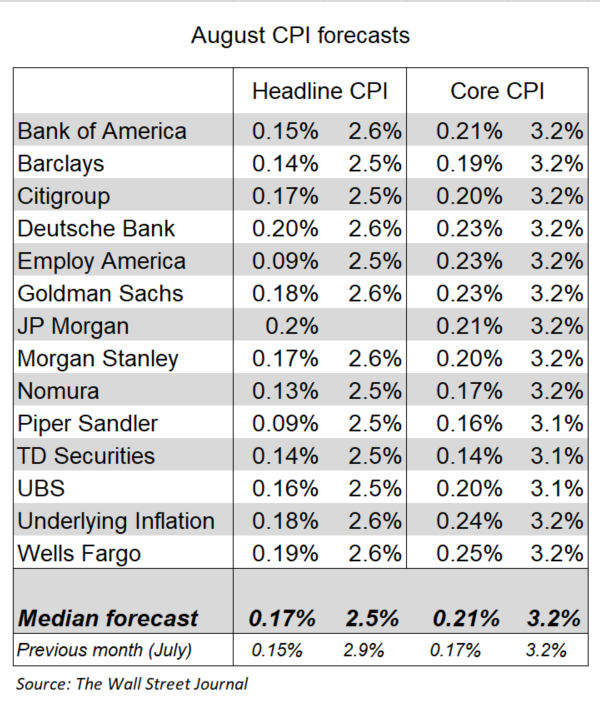

The latest Consumer Price Index (CPI) report is expected to show softer results. Headline inflation is anticipated to decline, primarily driven by a fall in energy prices during the month. However, core CPI, is expected to remain unchanged.

Some developments during the month: I am experimenting with a table format to show developments, please let me know if it looks bad, or is difficult to read, or how it can be improved

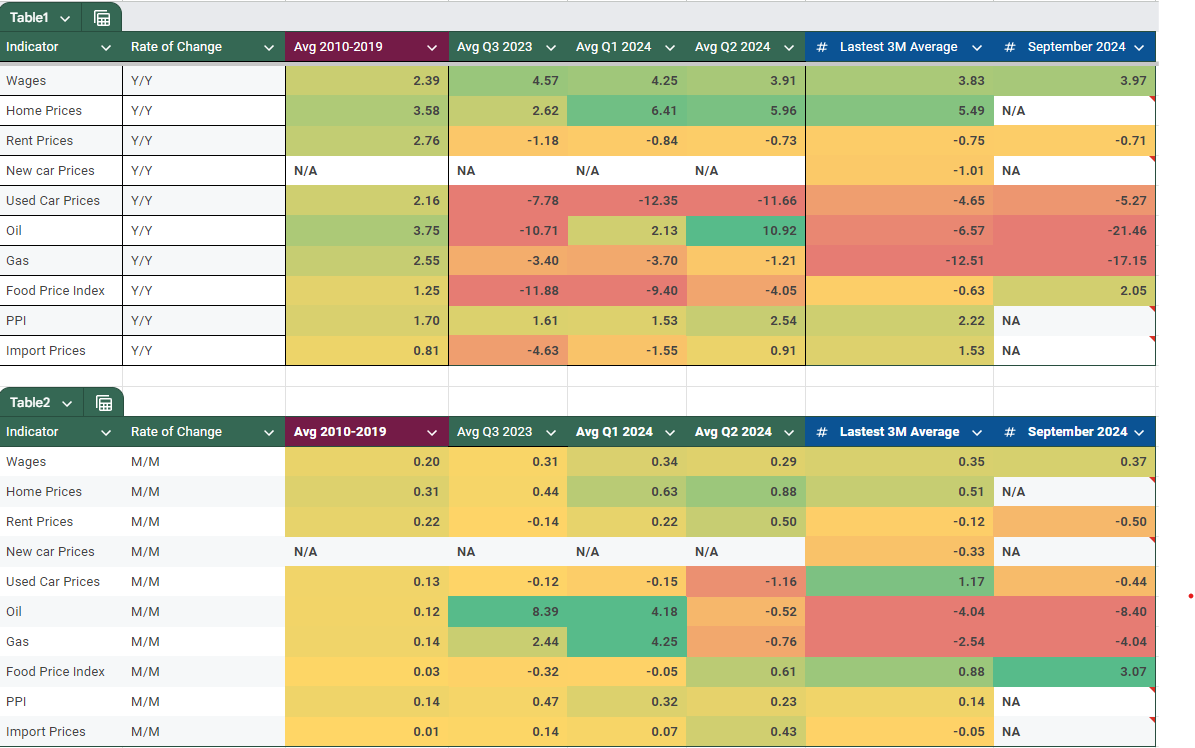

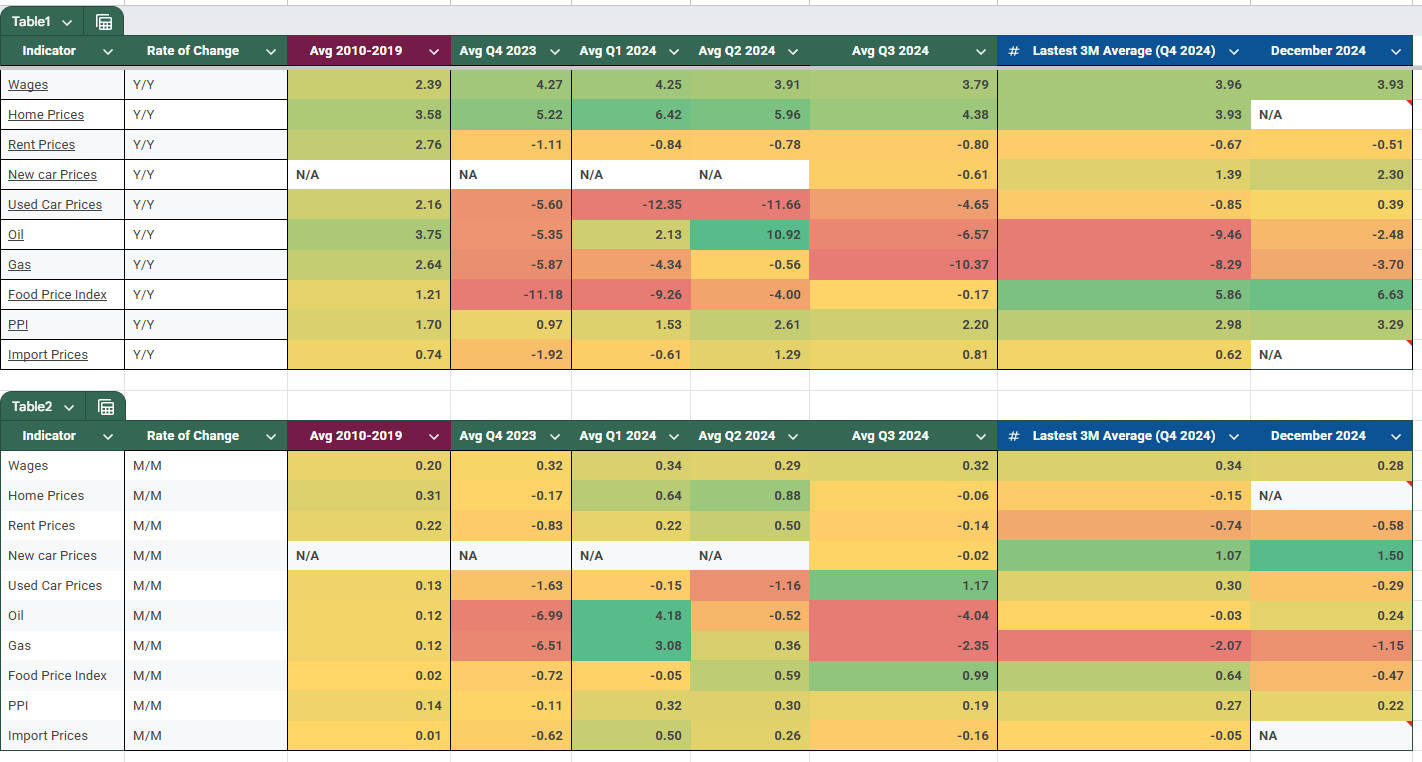

Persistent wage growth, though at a slower pace than the 2023 growth rate.

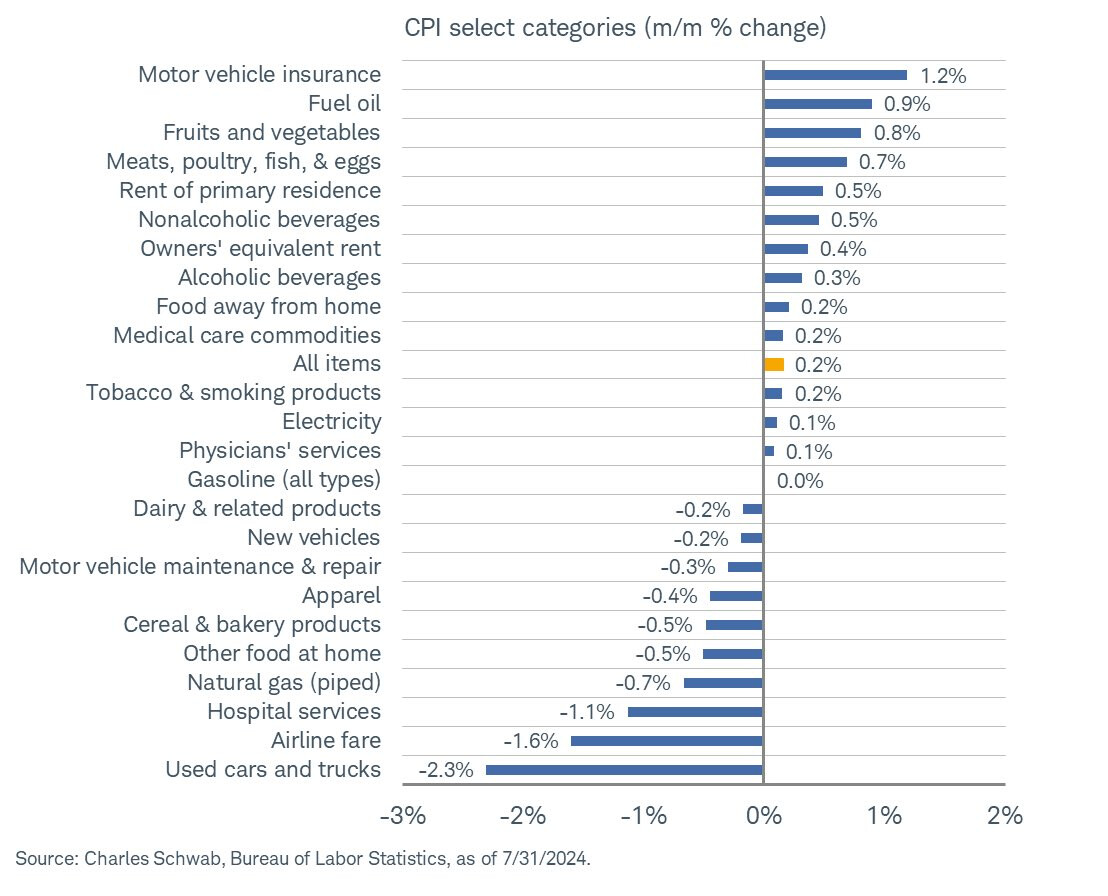

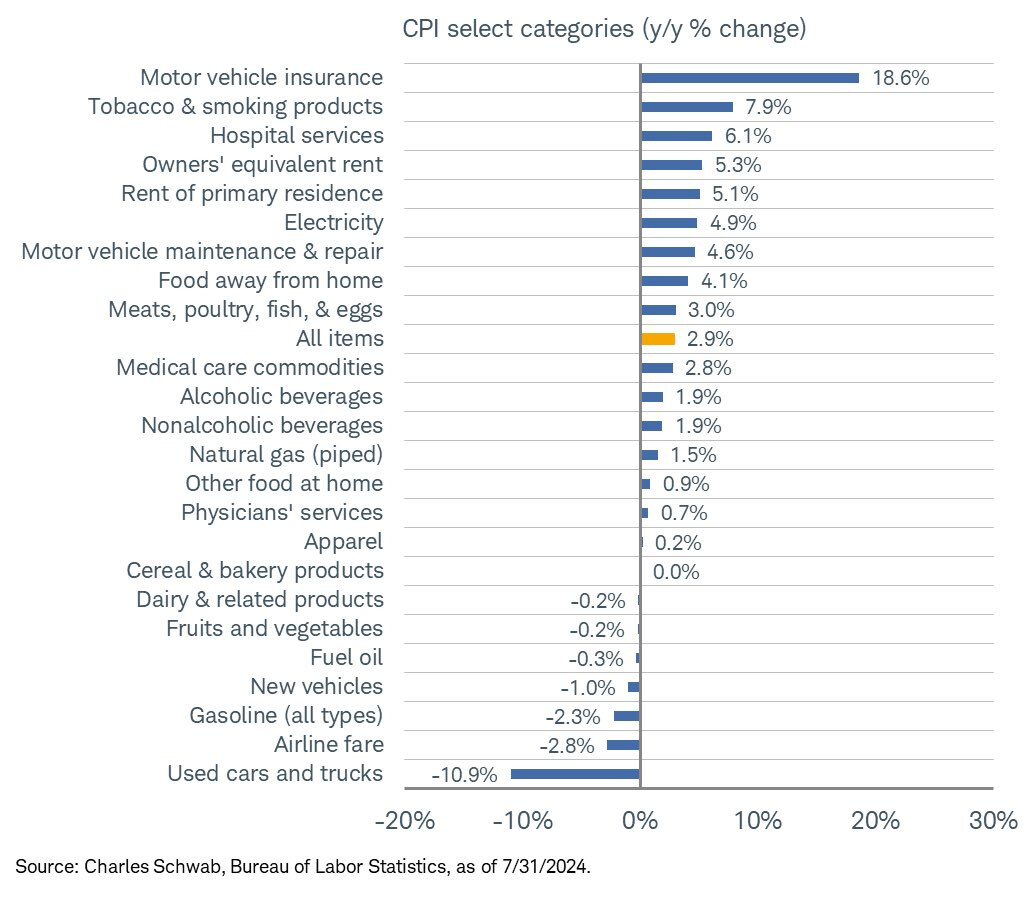

Rent prices remained on a negative Y/Y price trend, however, home prices continue with strong appreciation.

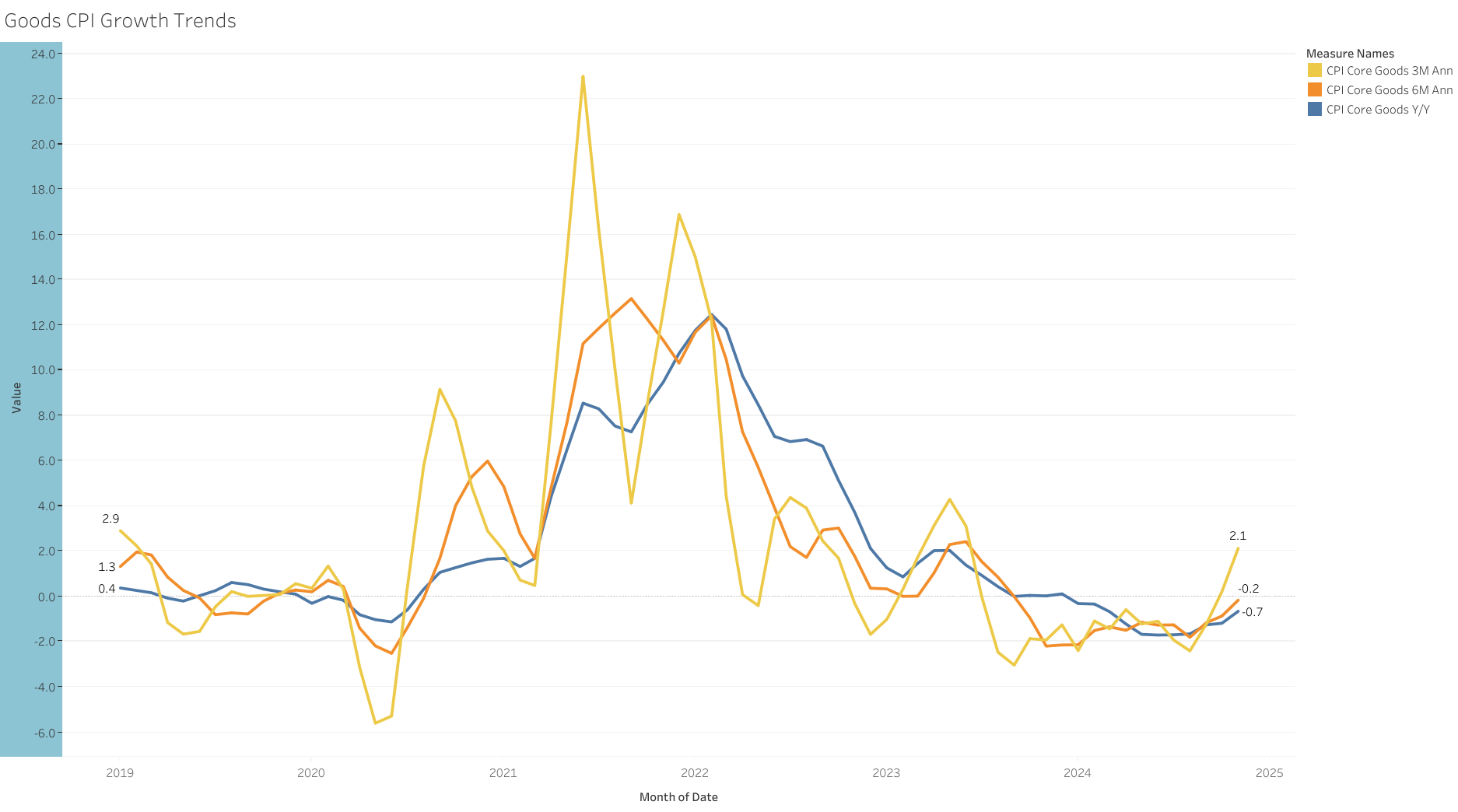

Car prices continue to deflate, however used car prices have shown some signs of appreciation in recent months.

Energy prices are currently on a significant decline, and it has gotten significantly worse during September.

Food, PPI and import prices are all currently stable and more in line with pre-pandemic increases.

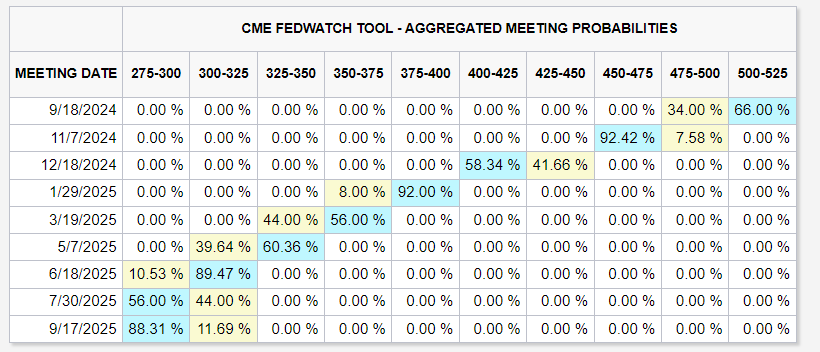

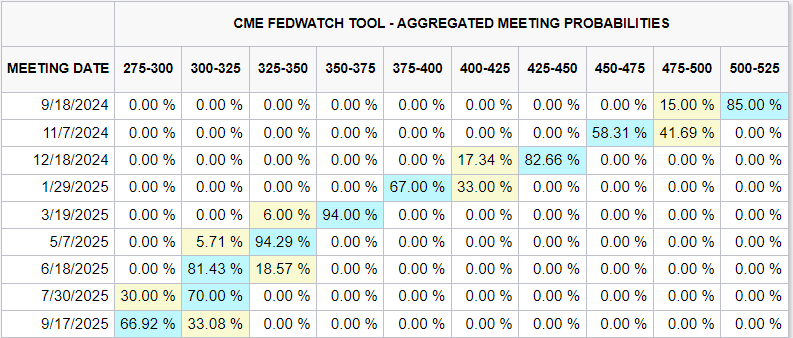

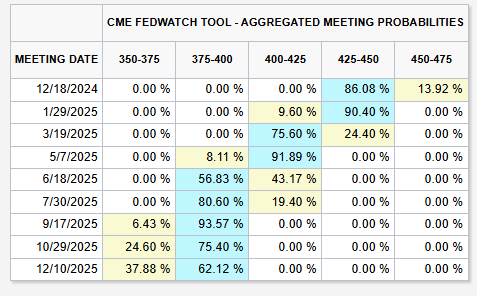

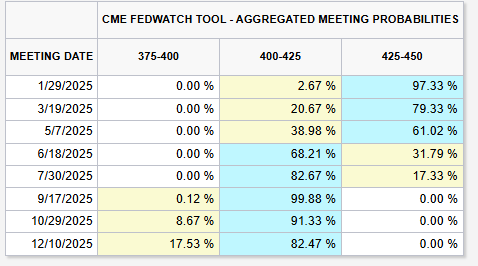

The market is currently pricing 25bps rate cuts in September 2024, with 125bps rate cuts for all 2024, and 250bps rate cuts as of September 2025.

For me, this is aggressive for a market that all thinks that a recession is not the most likely outcome.

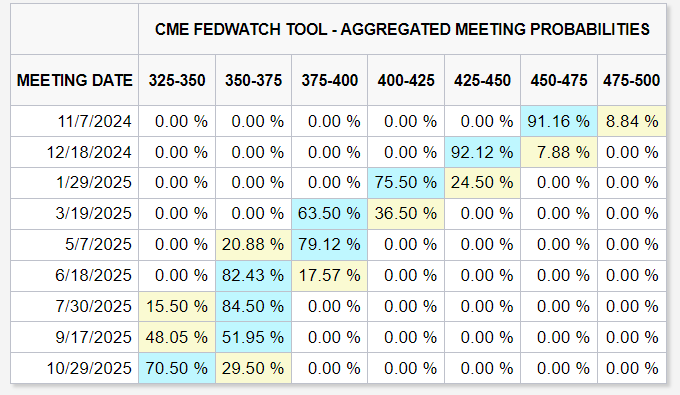

The higher-than-expected core monthly gain in this report likely ruled out most chances of a 50bps rate cut in September. It appears the market thinks similarly, as the probability of a 50bps cut has dropped sharply to just 15%, down from 35% yesterday

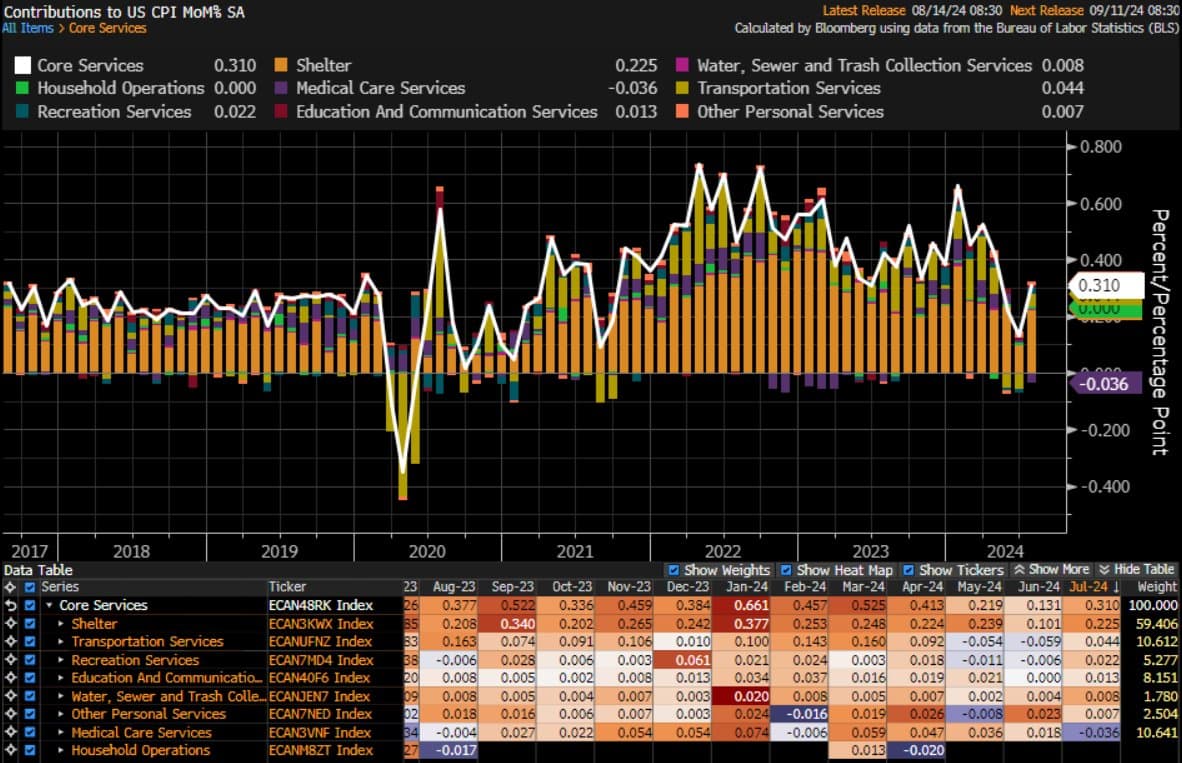

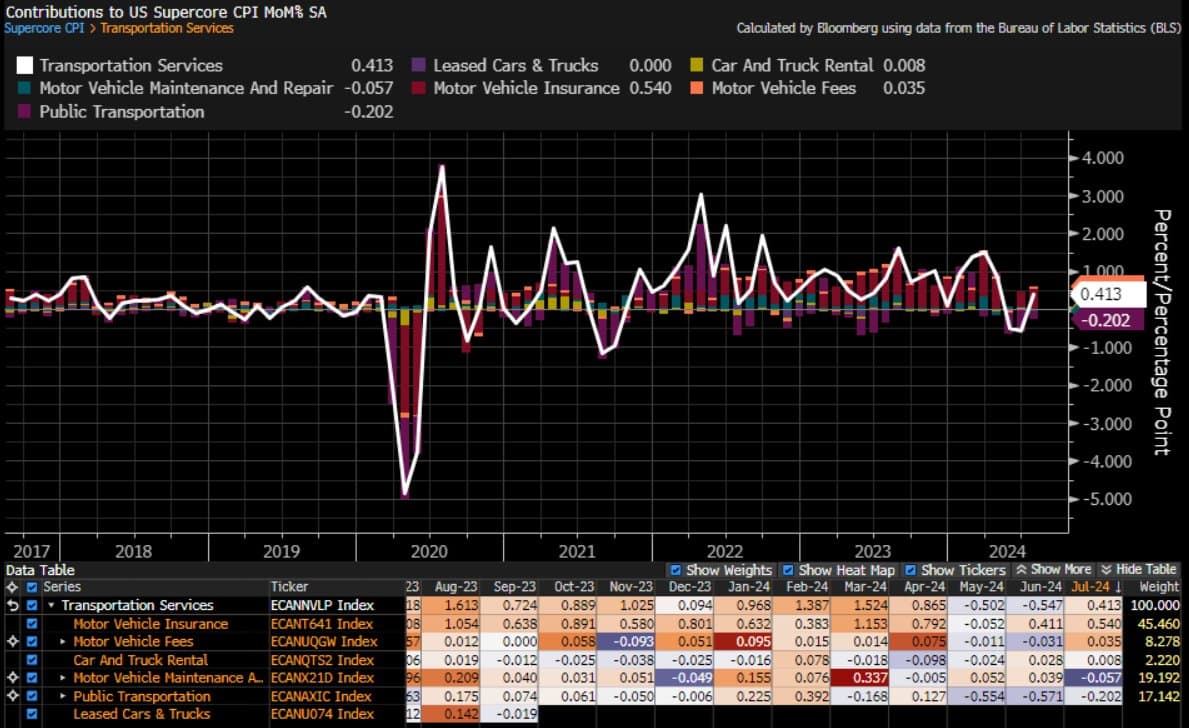

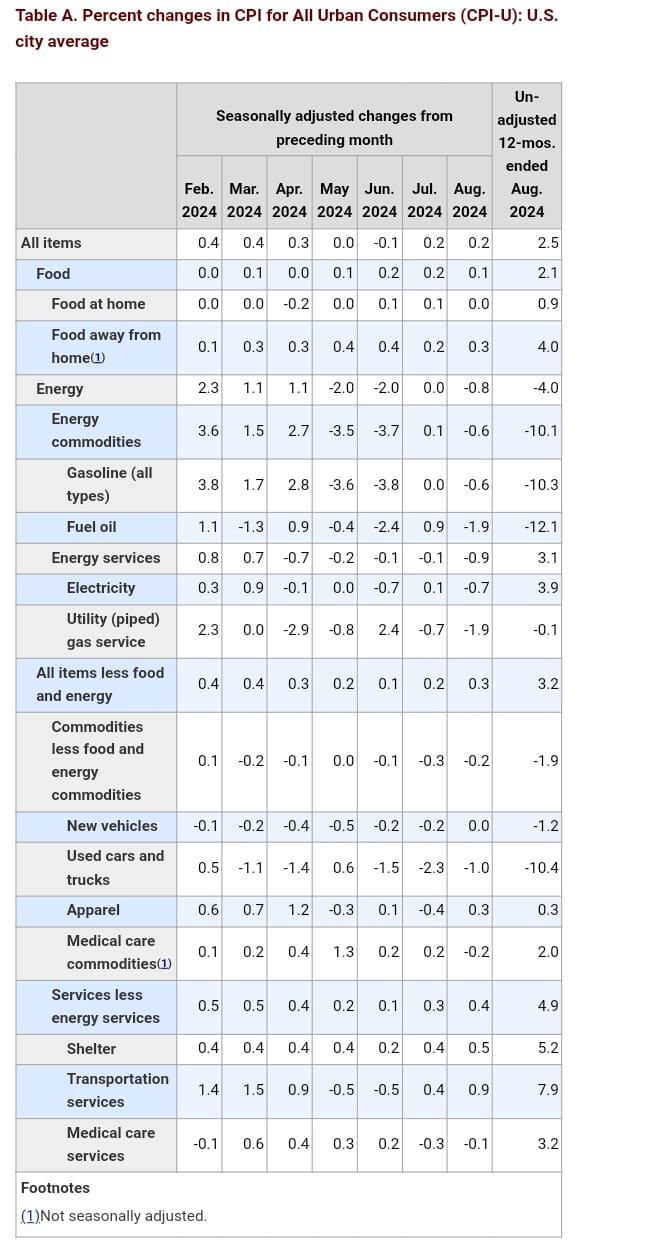

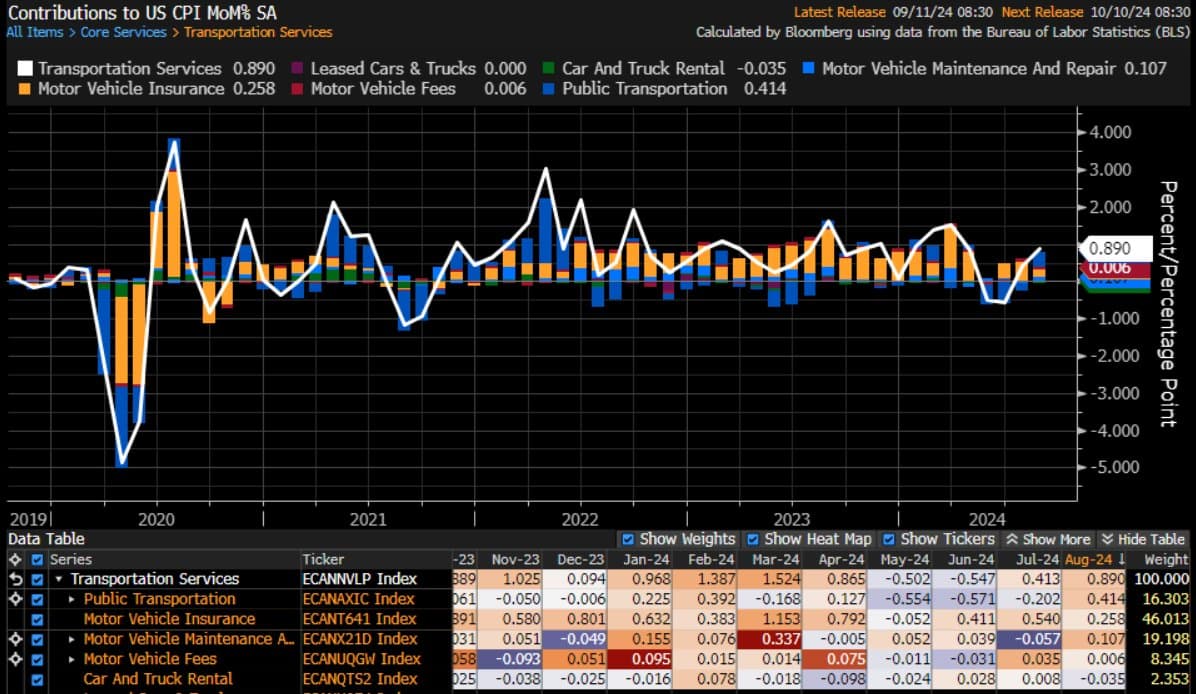

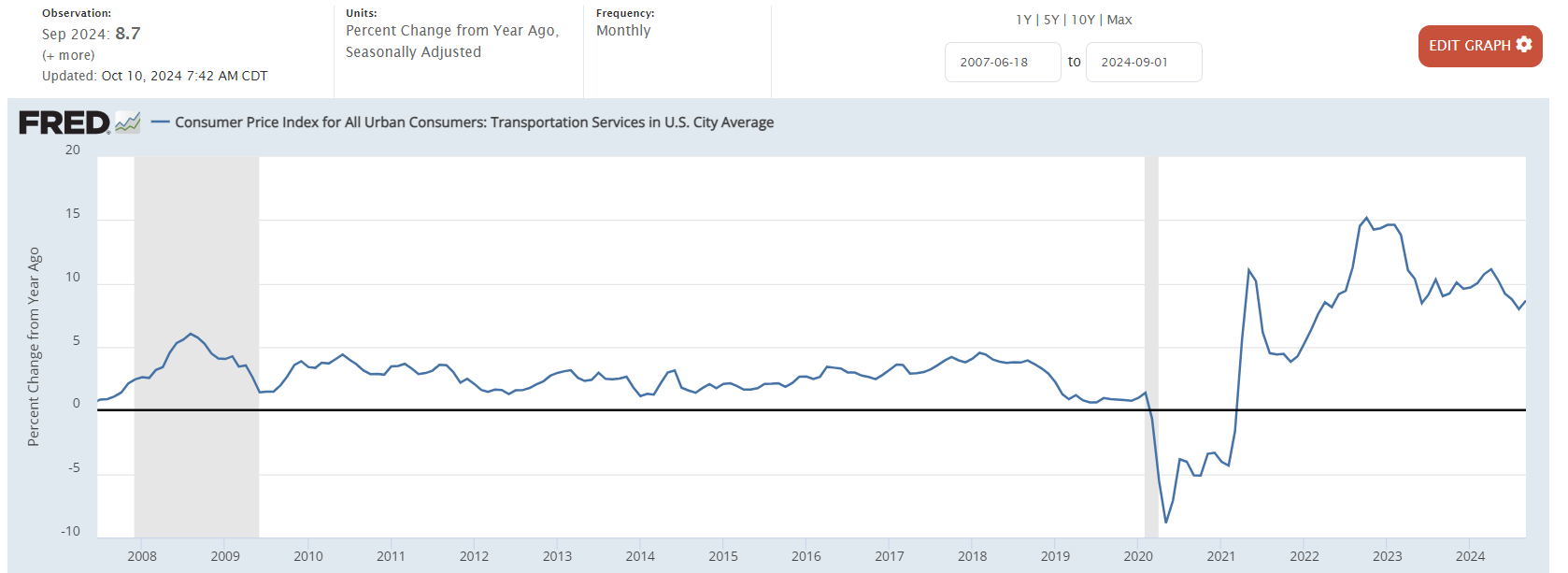

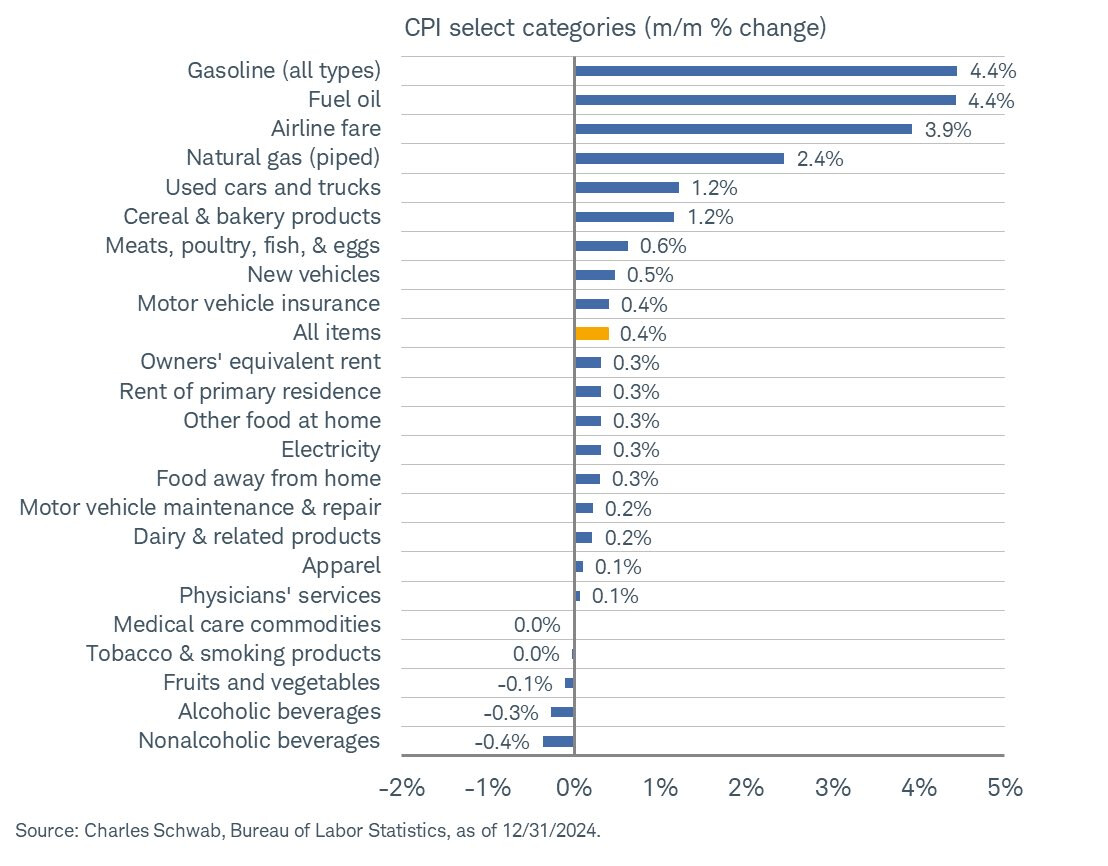

Transportation increased by 0.89% m/m, mostly about airfares, which rebounded 3.9% m/m after 5 months of declines.

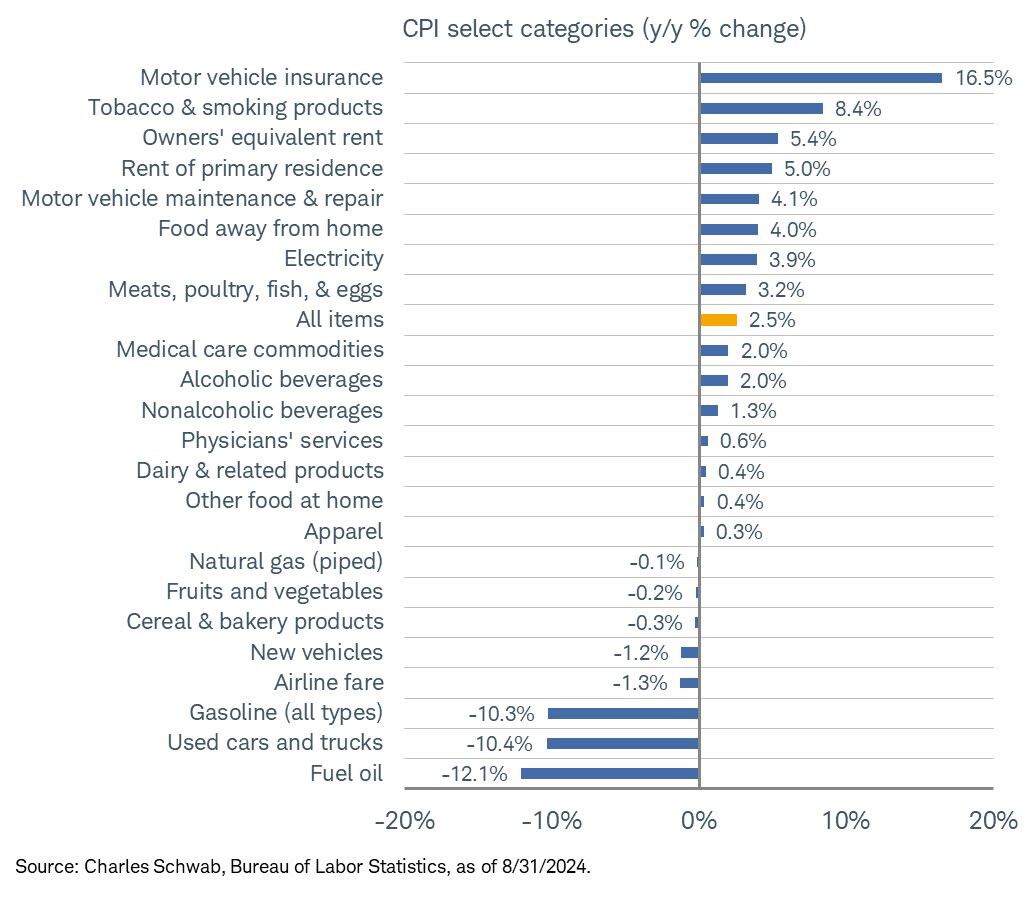

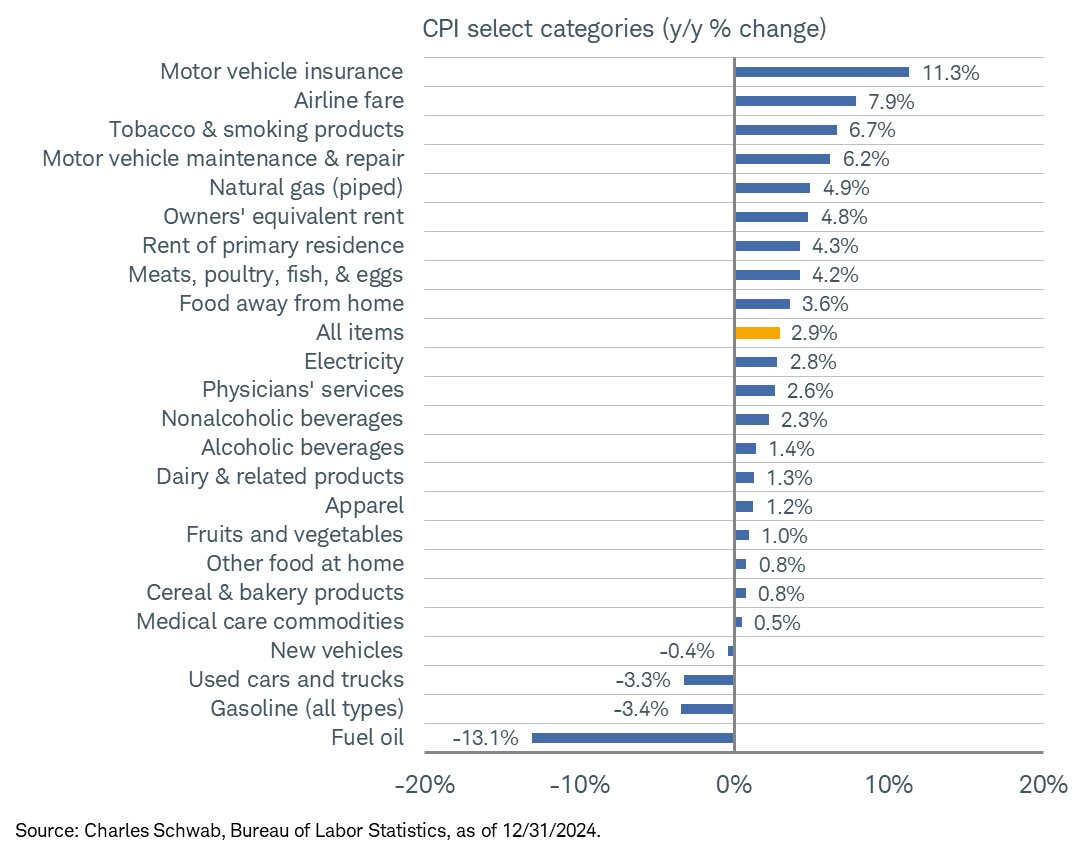

Vehicle insurance is moderating, but still very high on a annual basis (16.5% Y/Y)

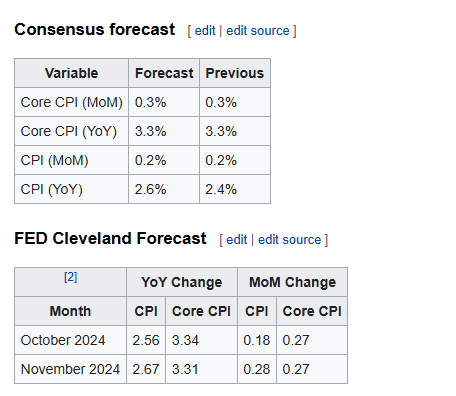

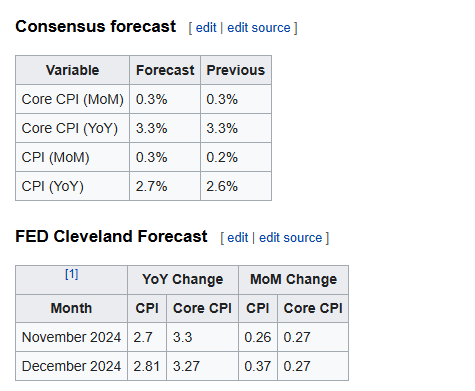

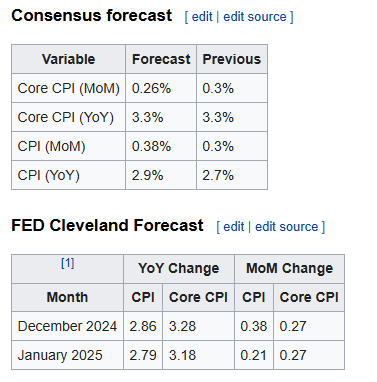

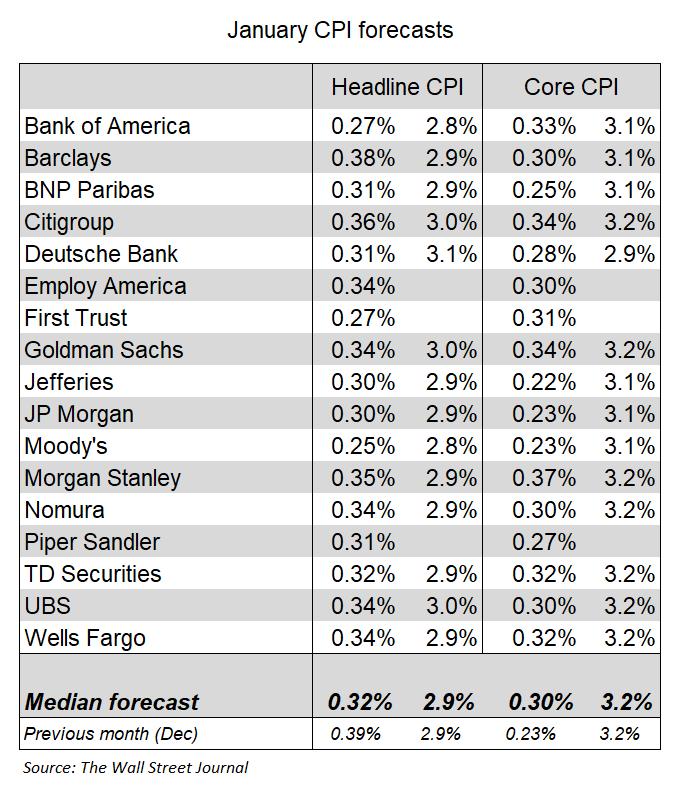

Tomorrow expectations are for again a mild month-over-month increase in both headline and core CPI. However core prices are expected to remain stuck at 3.2% Y/Y.

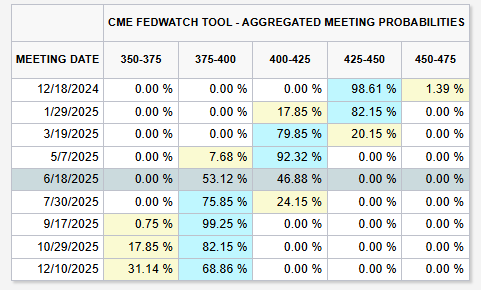

These are the current rate cut expectations ahead of the CPI release. I don’t anticipate the CPI will significantly alter these expectations unless there’s a notable upside surprise. Otherwise, labor market data seems to be the more important factor at the moment

Despite the CPI report coming in higher than anticipated, expectations for rate cuts remained largely unchanged. While it did reduce the likelihood of a 50 basis point cut in November, the majority of market still anticipate a 25 basis point reduction

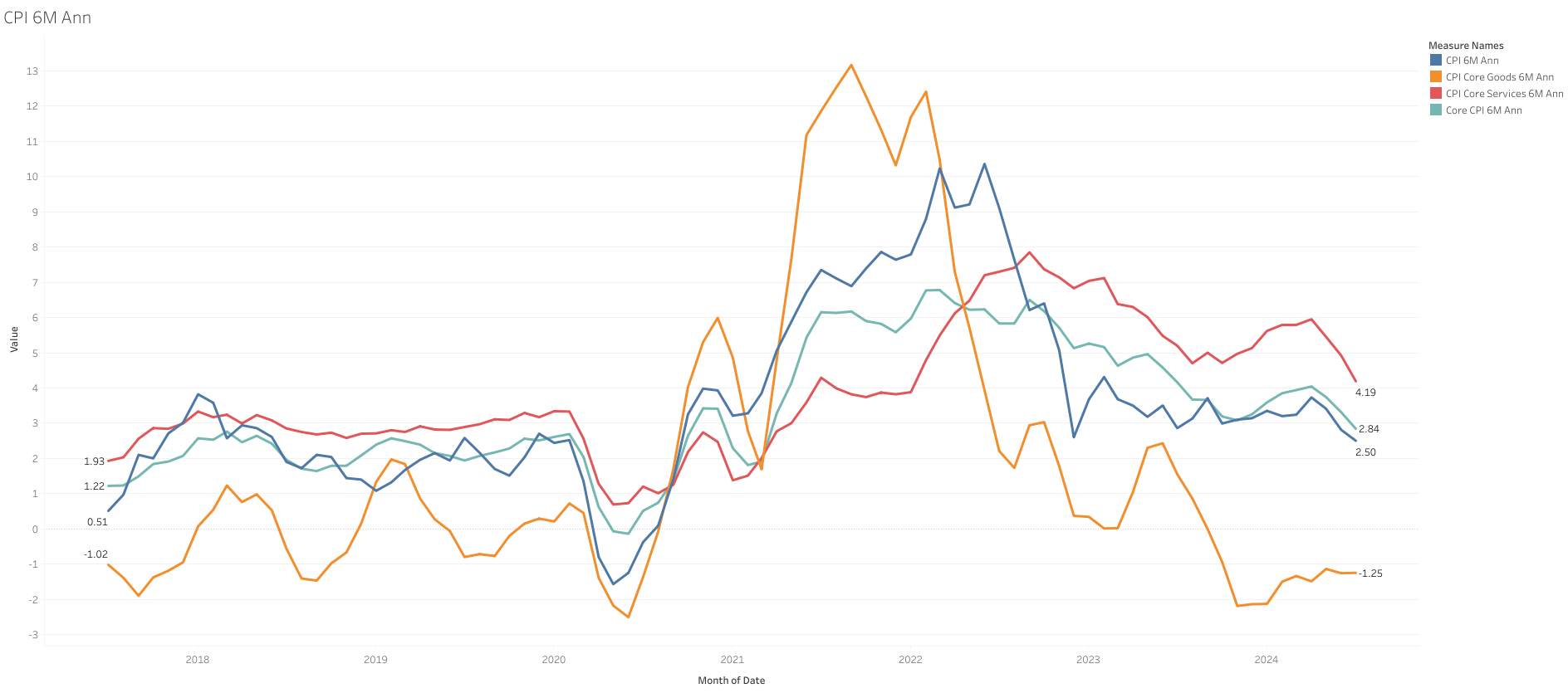

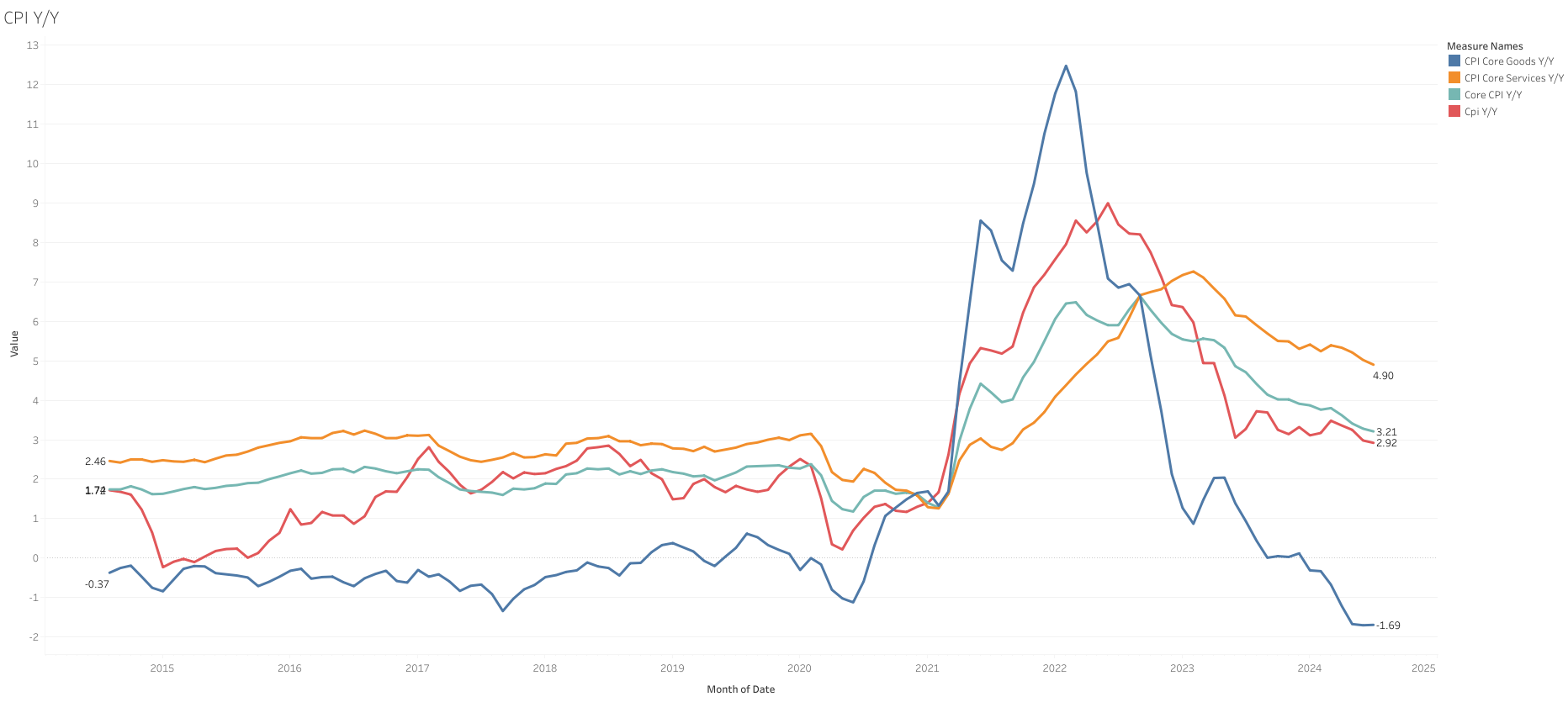

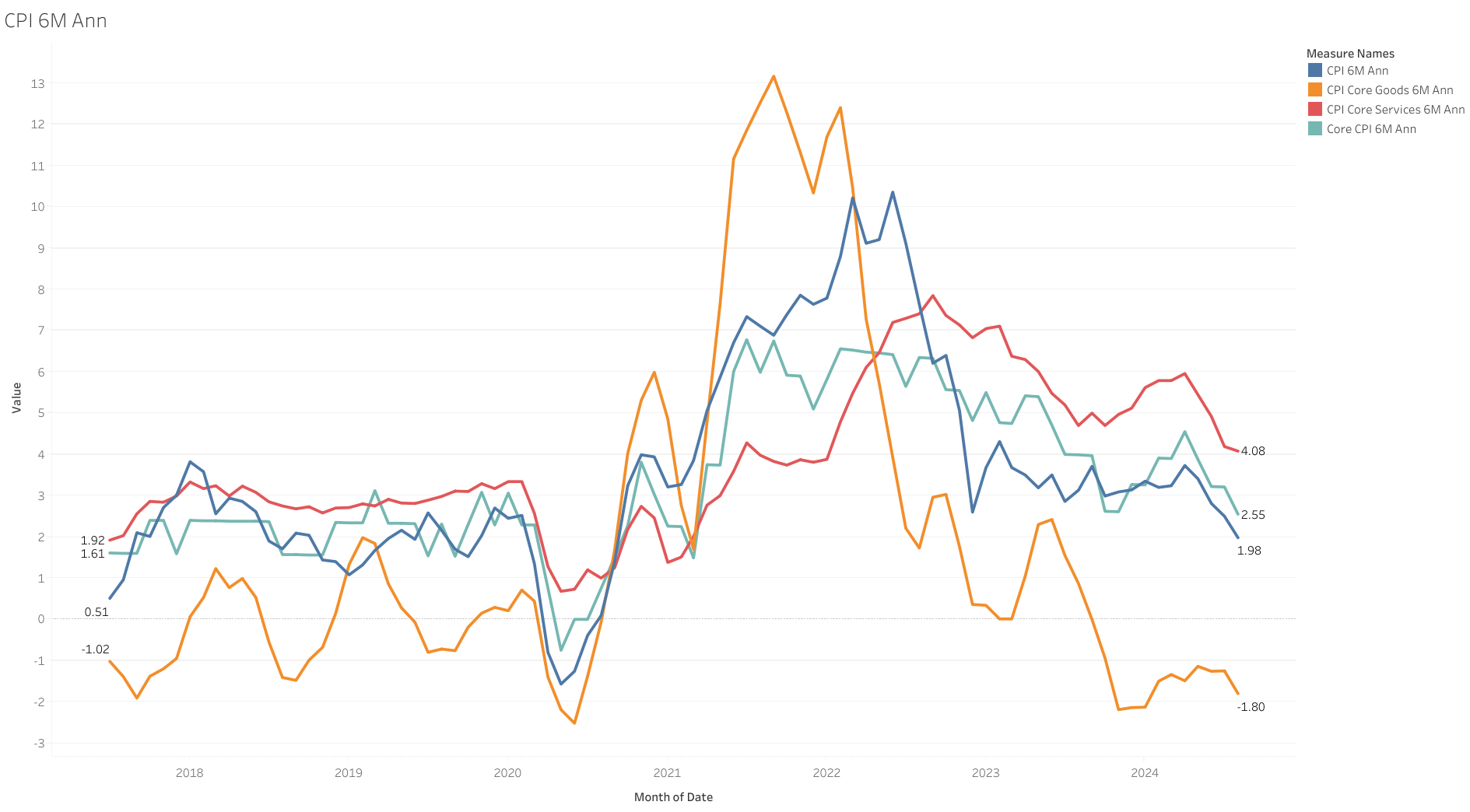

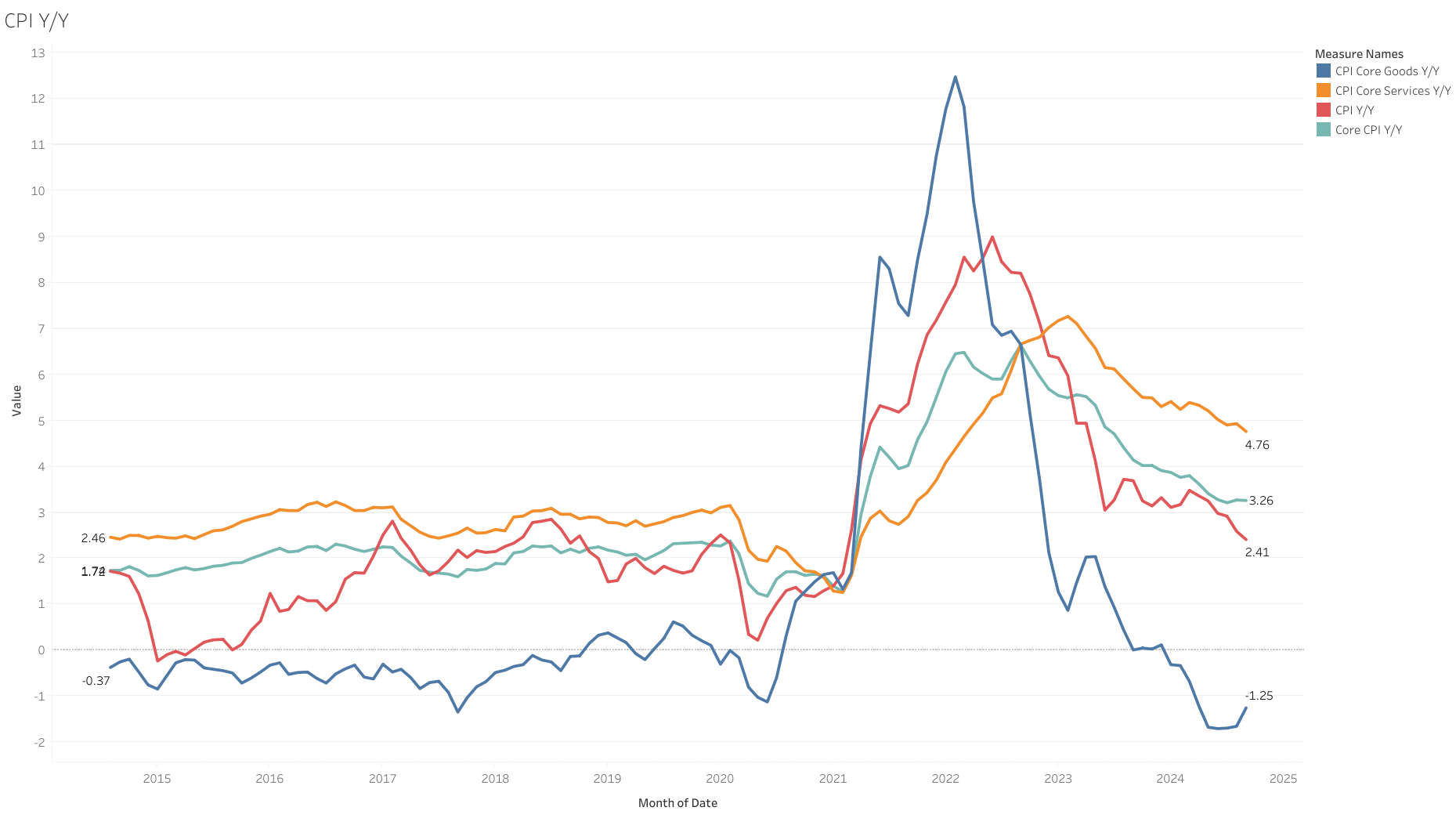

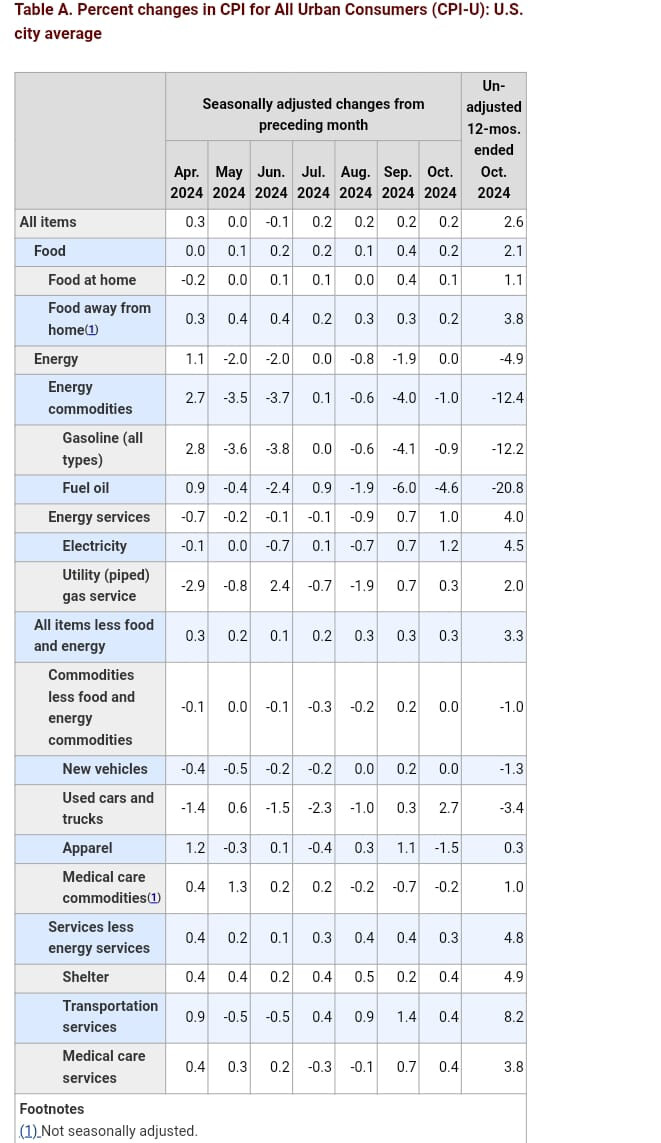

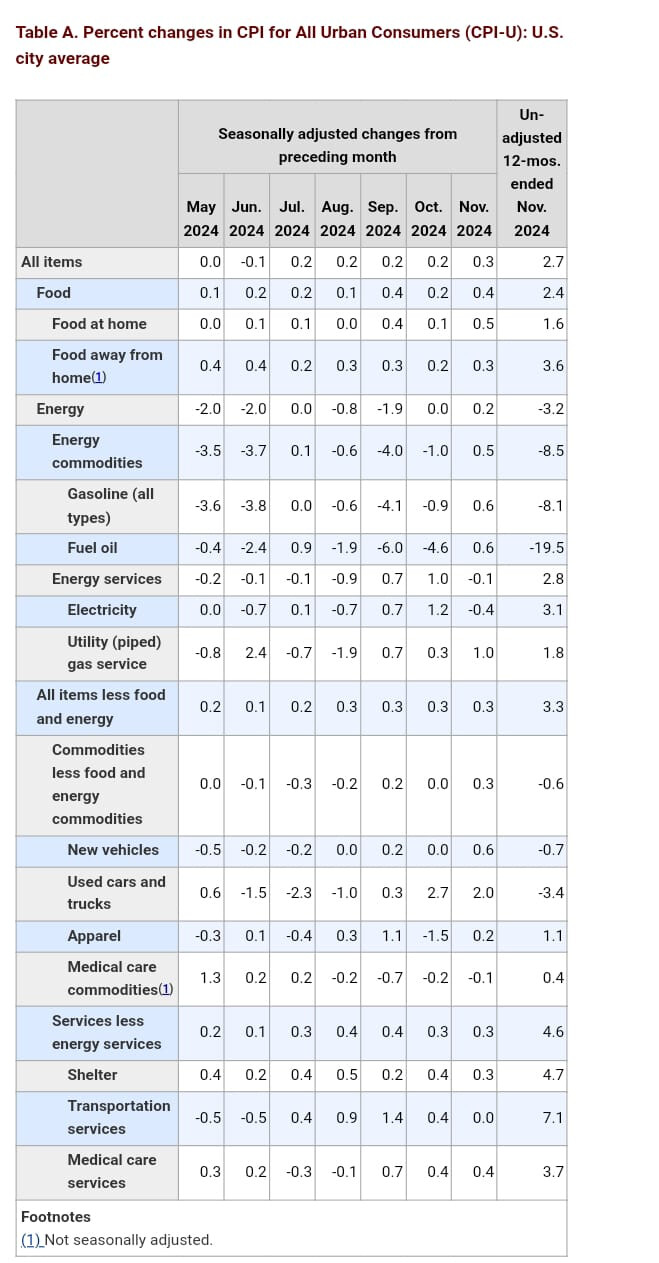

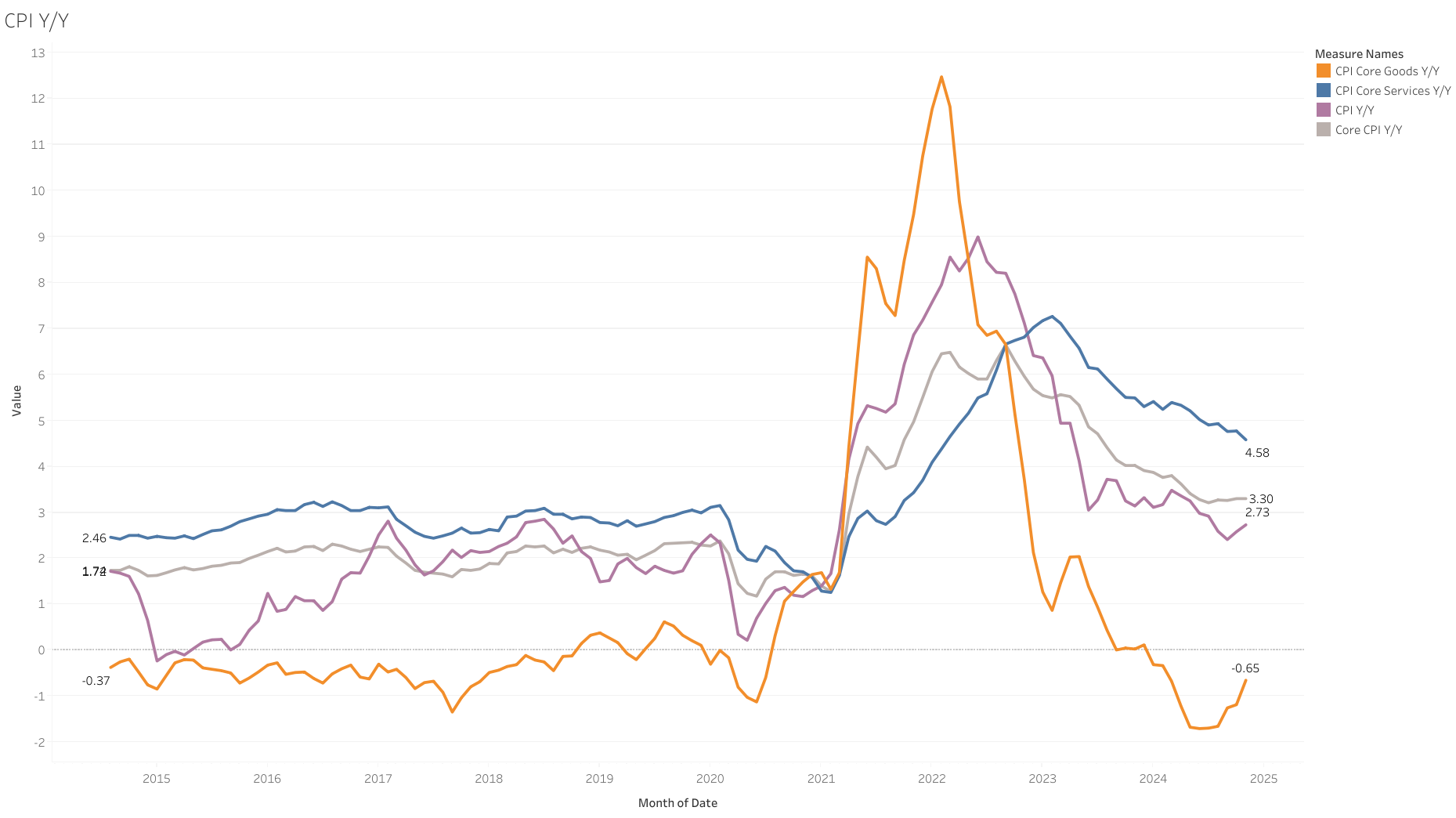

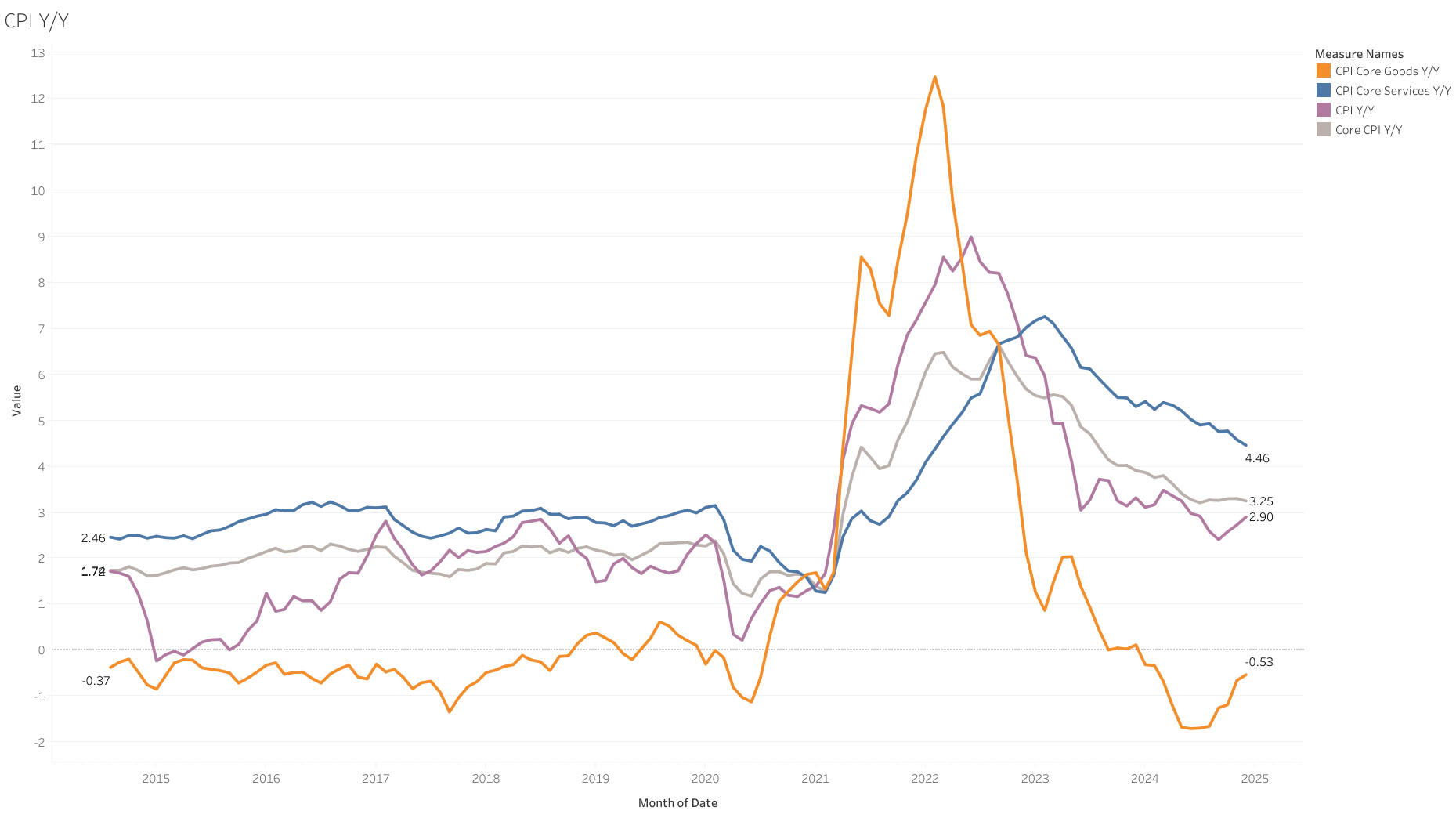

The headline CPI has dropped significantly, driven by a recent decline in energy prices. However, core CPI has shown less improvement, remaining stubbornly sticky at 3.3%

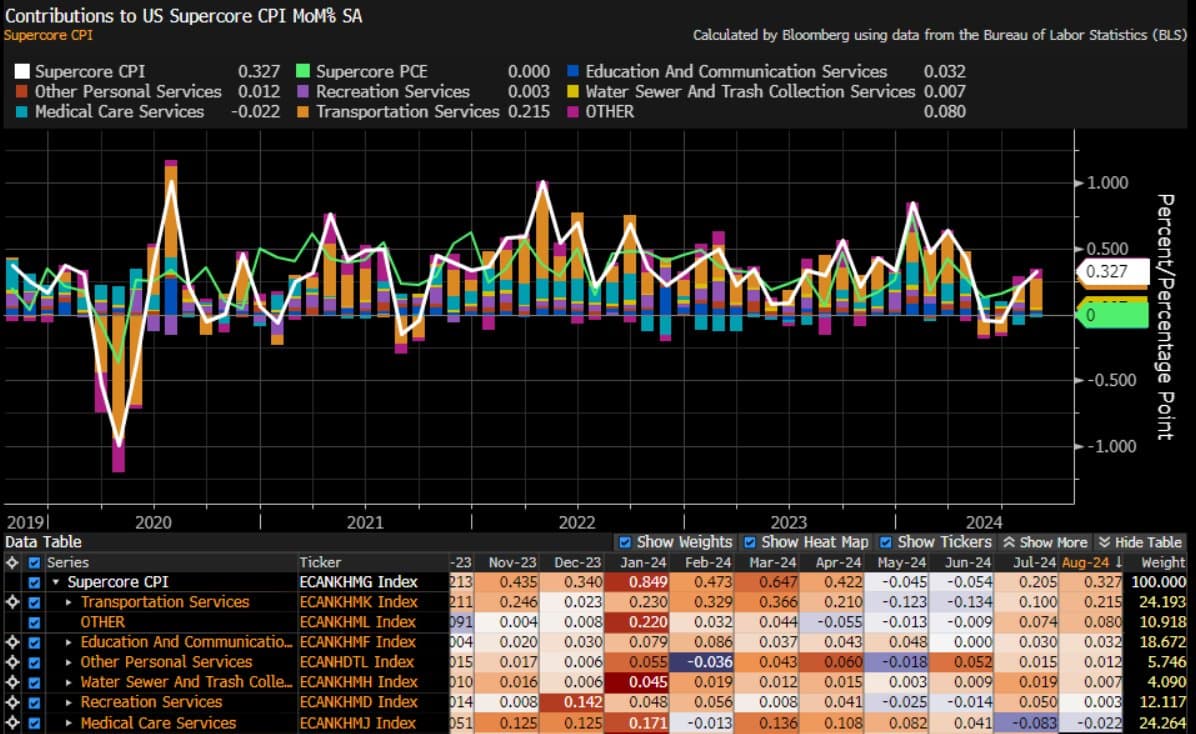

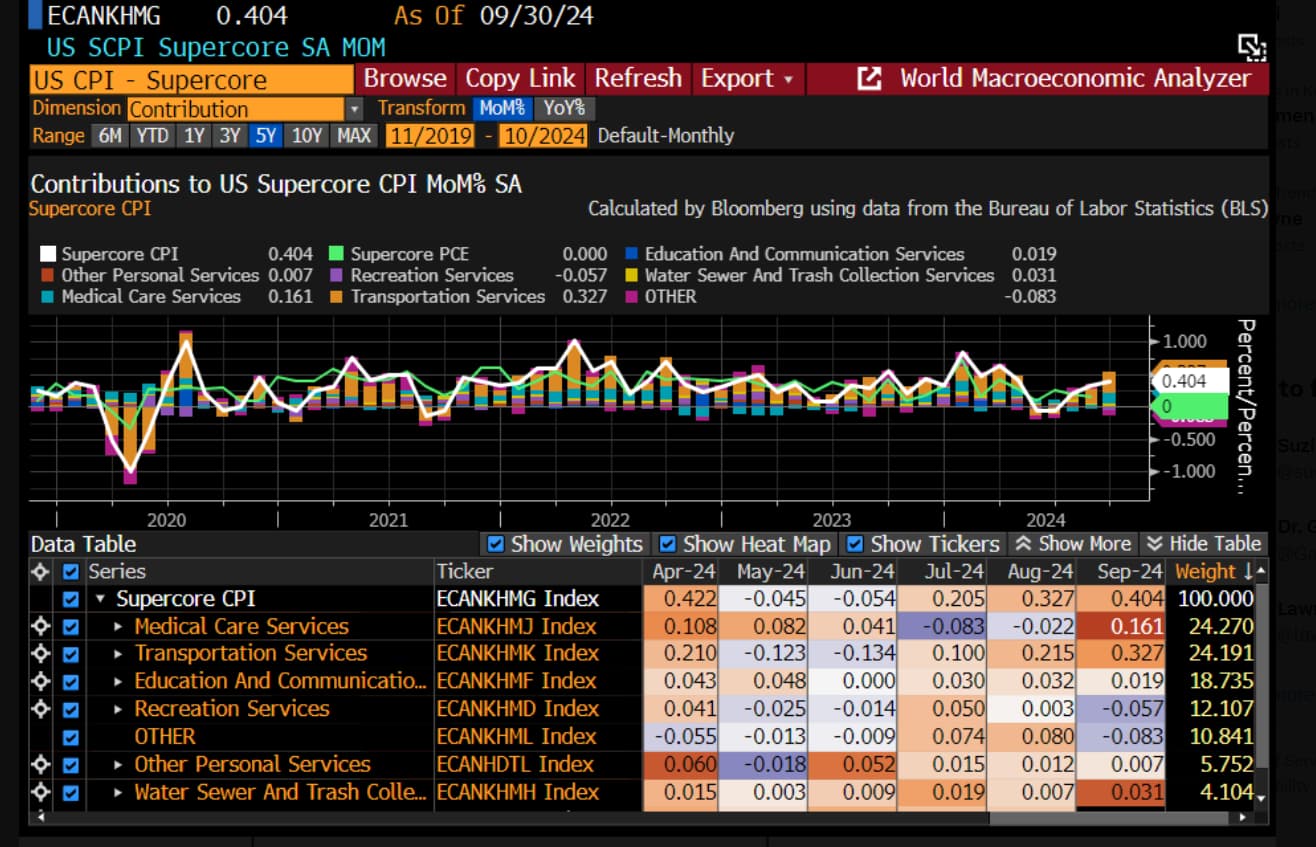

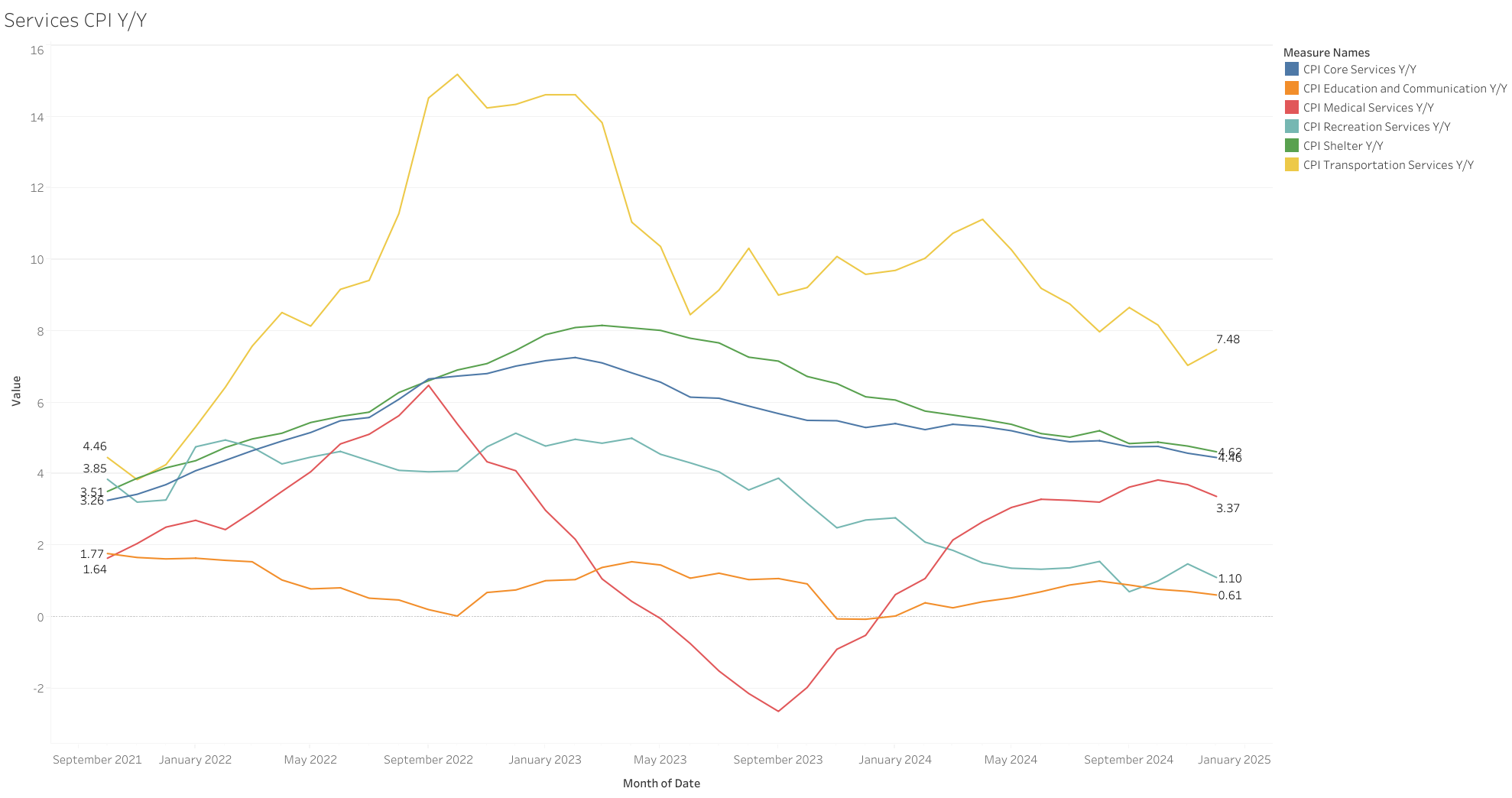

Shelter and transportation remain the primary drivers of core CPI, standing out as the only components with strong gains, as reflected in the 3-month average of monthly increases.

Shelter saw a modest increase of 0.2% month-over-month in September 2024, but consistent improvements like this will be necessary. For now, shelter costs remain significantly elevated on a annual basis.

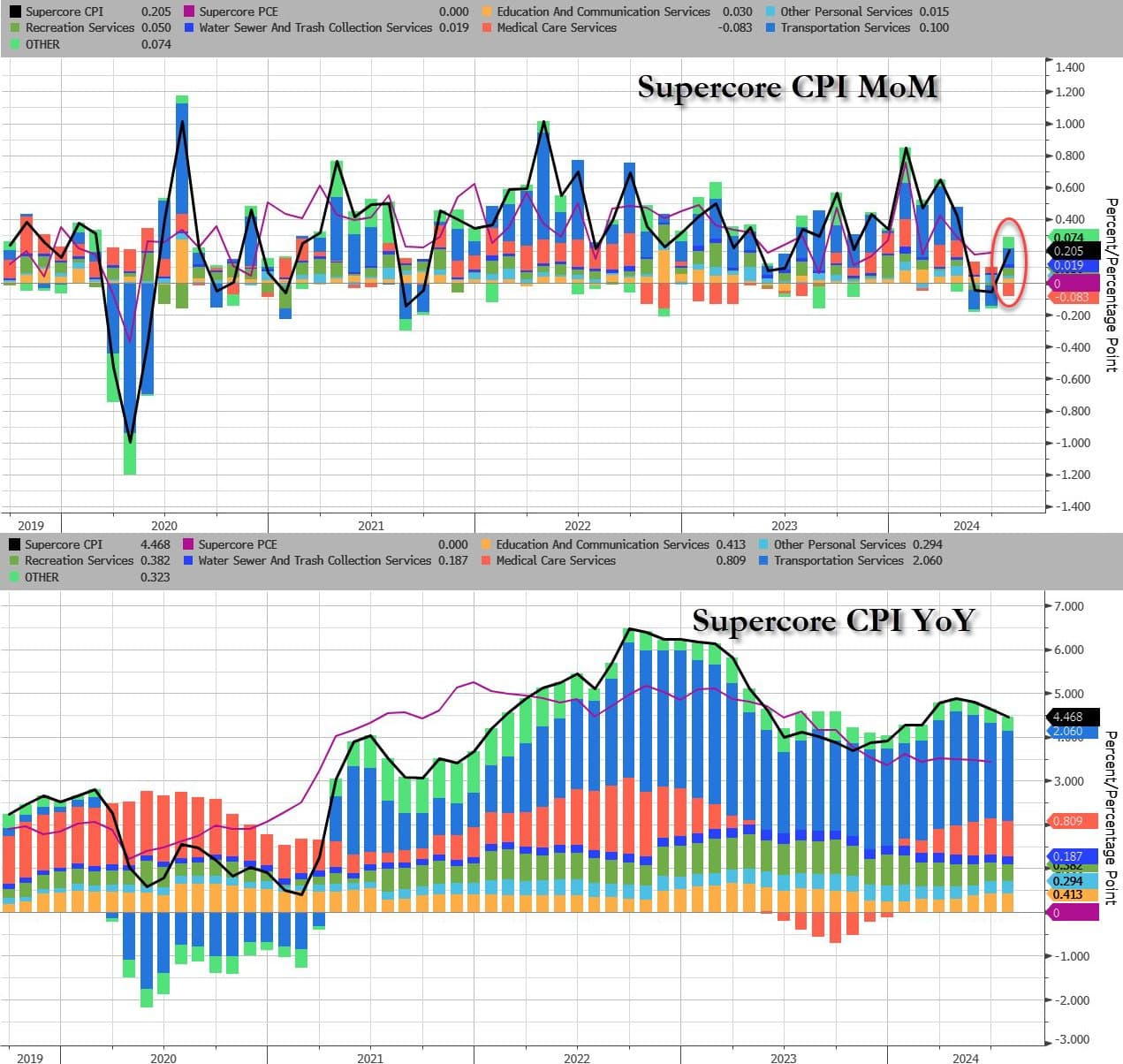

Transportation was the major responsible again, it recorded a very strong increase of 1.4% m/m. All major components of transportation saw increases in September, with vehicle insurance 1.2% m/m and 16.3% y/y/.

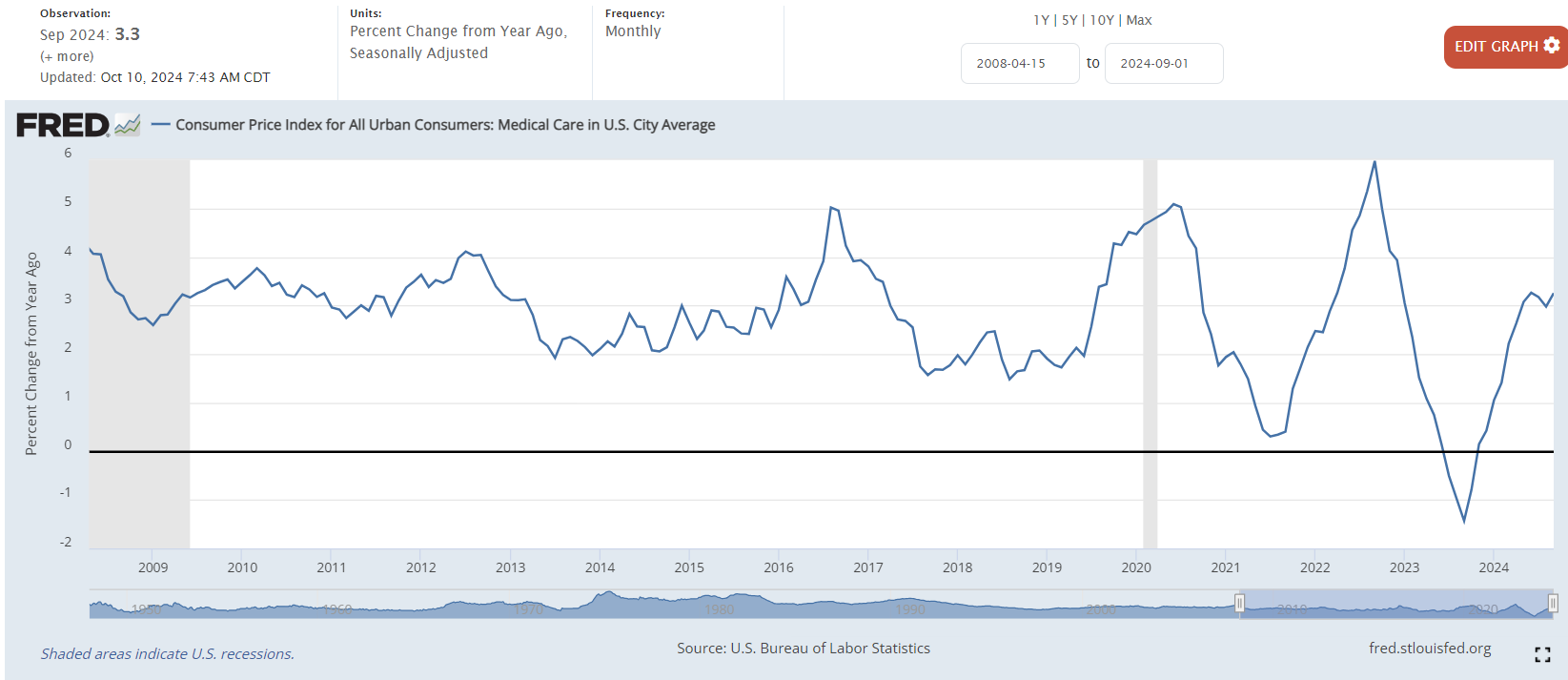

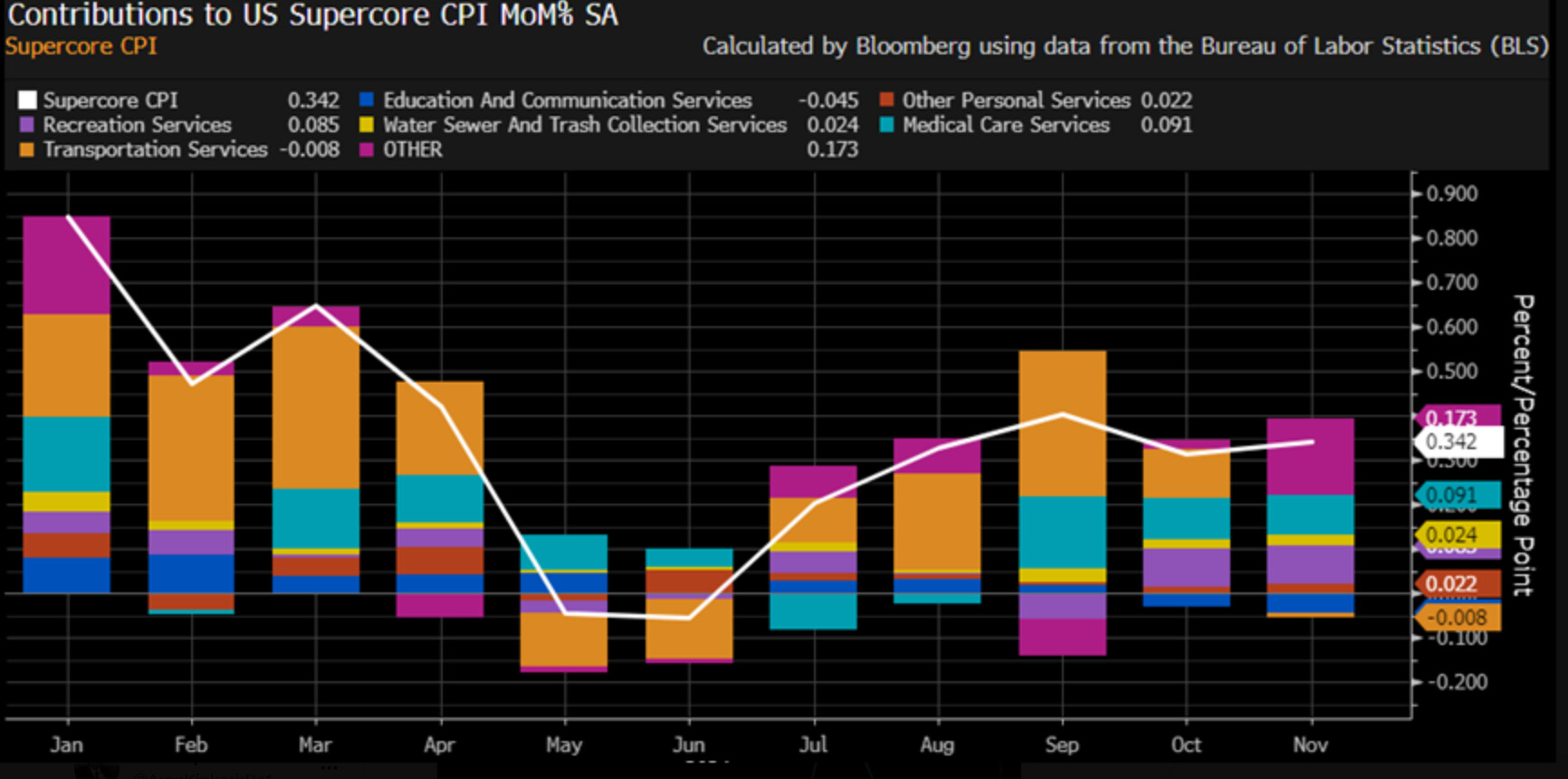

Medical services also contributed to super core increases with a 0.7% m/m gain, showing a rebound in y/y numbers since October 2023, sitting at 3.3% y/y

In my view, the potential for significant upside risk in this report remains limited. Wage growth remains persistently sticky, and rising food prices are the only notable factors posing an immediate risk.

Wages remain persistently sticky at around 4%, despite noticeable current weakness in job openings and hiring activity.

Food prices have risen sharply over the past two months, now standing at over 5% year-over-year.

Home prices have shown a more moderate increase recently, while rent prices remain negative year-over-year. This trend suggests we may continue to see further moderation in the shelter CPI going forward.

New and used car prices have stabilized in recent months, though they continue to exhibit a downward trend.

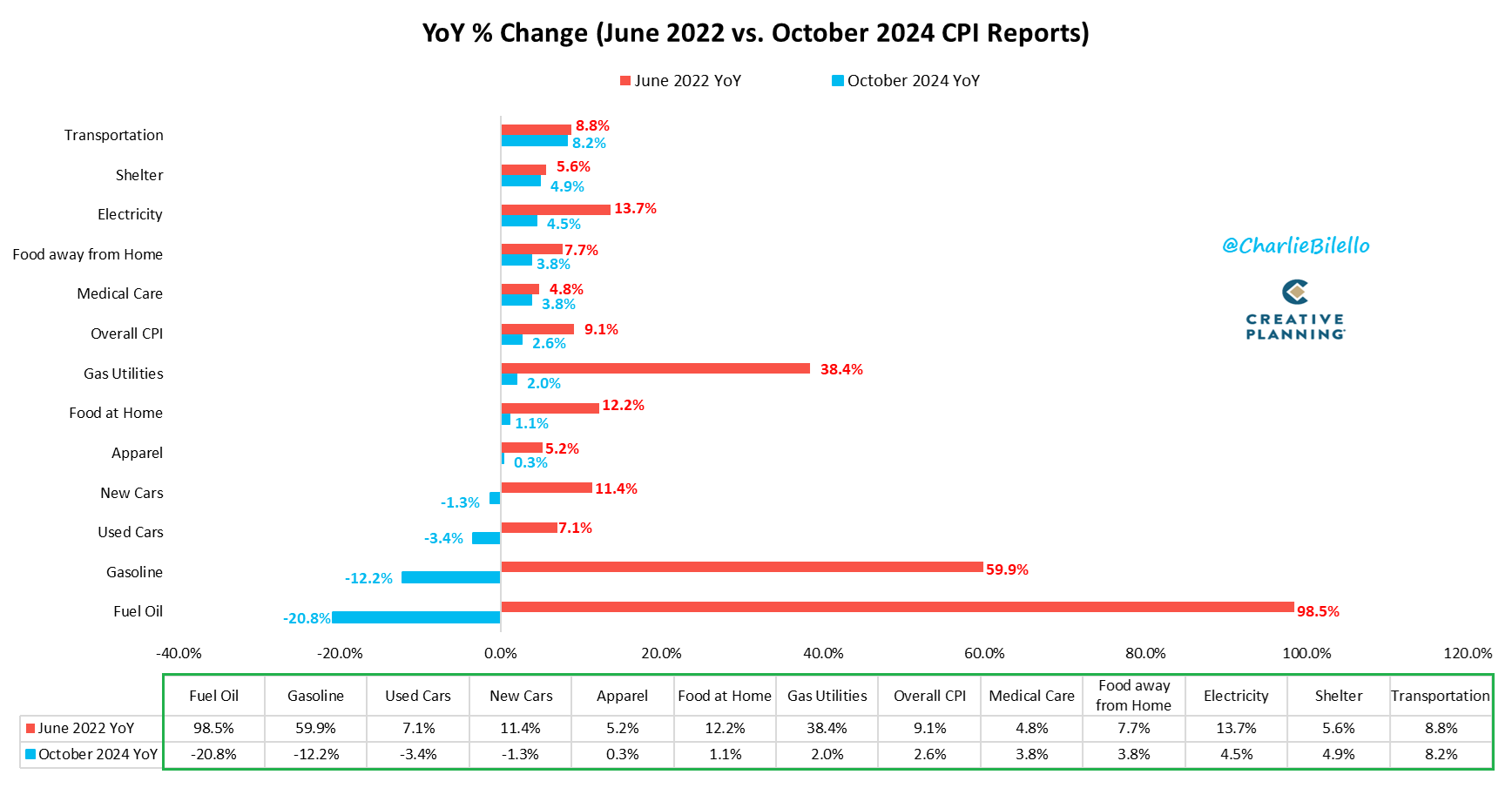

Although oil prices saw a slight increase in October, it remains significantly negative year-over-year, same as gasoline prices

PPI, import prices, and supply chains remain stable, which could support continued low inflation in goods CPI. However, it’s worth noting that potential policy changes under Trump could shift this dynamic in the near future.

Method

How could one think about the connection between wages and cpi? How strongly are they influencing the prices of goods and services of CPI?

Do we have this connection researched and documented somewhere in the Wiki?

I noticed that we don’t have the cpi release date and time in the calendar. This is important for everyone to have a clear orientation of what is upcoming.

I would also mention the day of the CPI release in our forum expectation post or even link to the calendar event so people know instantly when numbers will be released.

Labor costs, especially for the services sector, are usually a large part of the total costs. In the sectors that are more labor intensive, wage increases are more likely to lead directly to higher consumer prices, as companies pass their cost to consumers.

The extent of this relationship will vary significantly IMO by th industries being affected, the overall strength of the economy, and consequently, the pricing power companies can ultimately have. Additionally, it depends on whether productivity gains are offsetting a portion, all, or none of the wage growth.

The effect could also happen through income, higher wages mean more disposable income for households, boosting or sustaining strong demand for goods and services.

We haven’t yet done in-depth research or developed our own historical calculations on the correlation between wages and inflation. I’ve started monitoring this closely, as both the Federal Reserve and the ECB have emphasized wages as a key factor for sustainably bringing inflation back to the 2% target.

These are some research articles I found for the US:

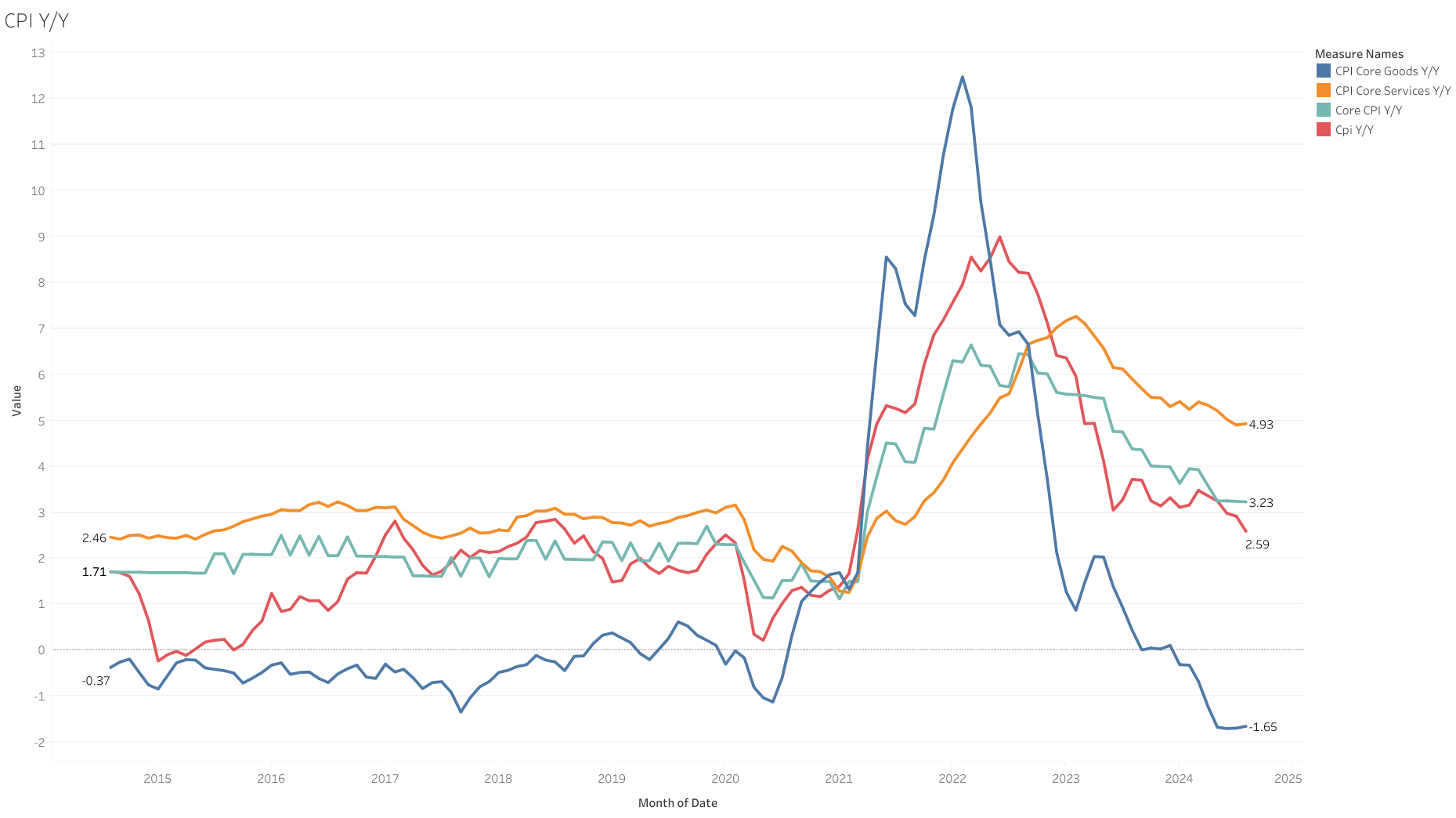

The Richmond Fed, using a Granger causality test, identified a significant positive correlation between wage growth and services CPI but not goods CPI over the 2000-2022 period. This relationship became particularly pronounced post-pandemic. They didn’t quantify the exact relationship though (IMO this is not fixed, is most likely dynamic as is dependent on a lot of other factors as I described above)

The Boston Fed also observed a strong positive correlation between core PCE inflation and growth in the Employment Cost Index (ECI) over the past four decades,and particularly in 2021 and 2022, when both increased sharply. However, given the influence of other significant shocks in both metrics, wage growth accounted for less than 15% of inflation at the peak of the recent inflationary episode, a lower contribution than during the 1970s, where wages was the primary driver of inflation, creating a wage-price spiral. (This is contributing to my thinking that the relationship will vary a lot depending on the conditions in the economy)

I don’t necessarily currently view wages as a significant risk for triggering another wave of inflation (though further acceleration above current levels should be monitored). While wage growth is high relative to recent historical trends, it has stabilized, reducing the likelihood imo of a near-term wage-price spiral. Instead, the primary risk for me is that it could be creating some stickiness in CPI growth, particularly within the services sector.

In its recent conference, the Fed noted that wage growth is currently in line with 2% inflation only if productivity gains continue to be strong. However, productivity gains have been easing a bit, raising questions about the durability of the gains in the near term for me.

Powell also said he is still uncertain productivity gains will remain strong, since it is common to see it rise after a shock and then return to the mean.

This report doesn’t change much the picture of the recent months. However, I’m becoming currently somewhat concerned by the lack of further improvement in core inflation since June, particularly as the Federal Reserve continues to cut rates. With GDP growth and consumer spending still robust, alongside the stock market at ATH and historically tight credit spreads, I question whether this level of monetary stimulus was necessary at this point, and if they could be stimulating the economy too soon. It also risks wasting room to maneuver and react when a deceleration of the economy comes later on at any point that requires more intervention.

While I don’t consider this the most probable scenario yet, the recent election of Trump introduces a new set of potential inflationary pressures that increase the probability. His proposed policies could present challenges to the Fed’s 2% inflation target, and even though is still very early, I think the FED need to consider the impact at some point in their policy:

Tax cuts that may increase profits, and disposable income and drive additional demand

Import tariffs that could raise the cost of goods, affecting inflation directly, and also lowering productivity

Mass Deportation of immigrants that may disrupt labor supply, pushing wages and potentially prices upward

Increased fiscal deficits and debt that could add upward pressure on inflation if the government continues to increase spending.

I haven’t conducted an in-depth assessment of the economic implications of each proposed policy. However, this research is in my medium-term priorities, as it’s essential imo to anticipate and understand the potential impact when or if they get implemented.

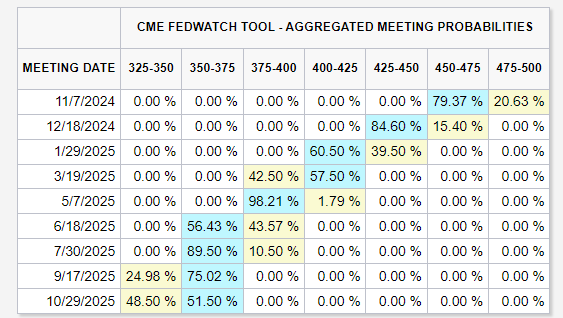

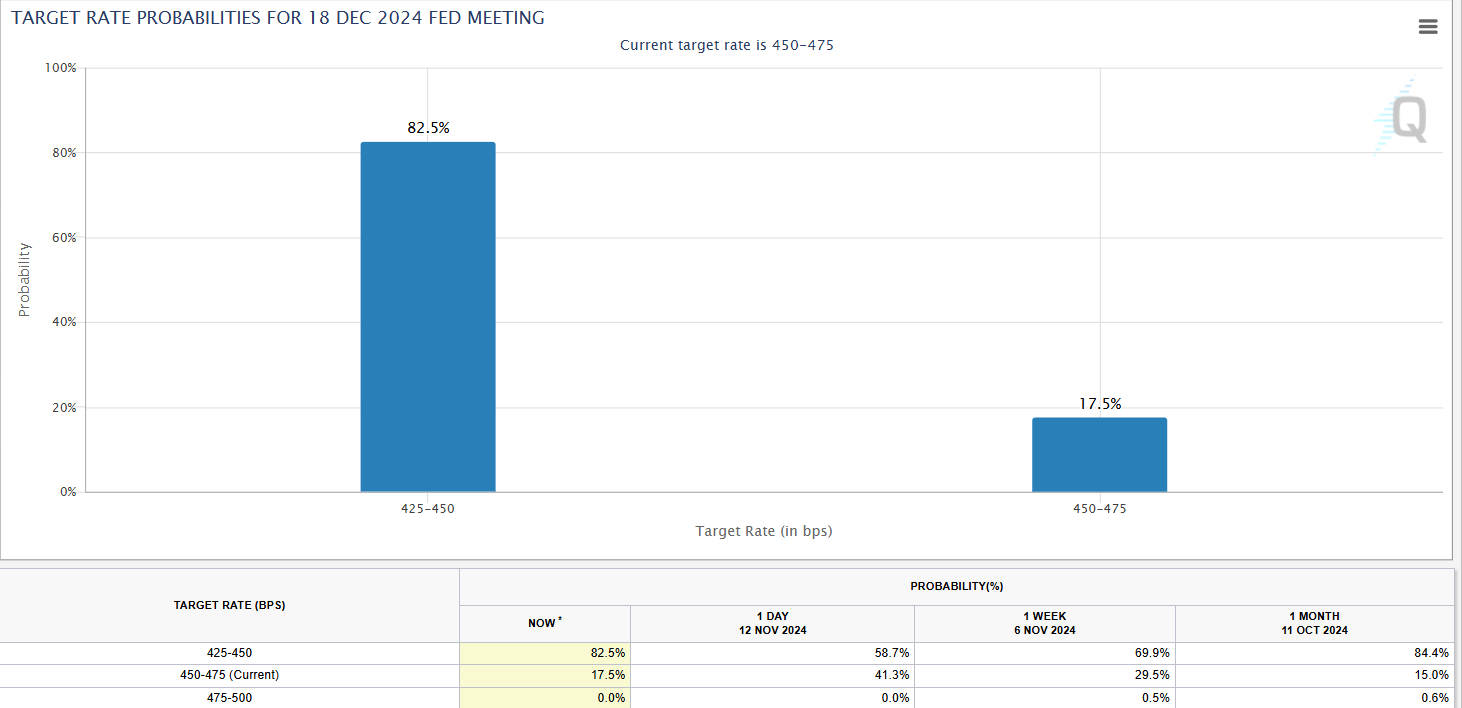

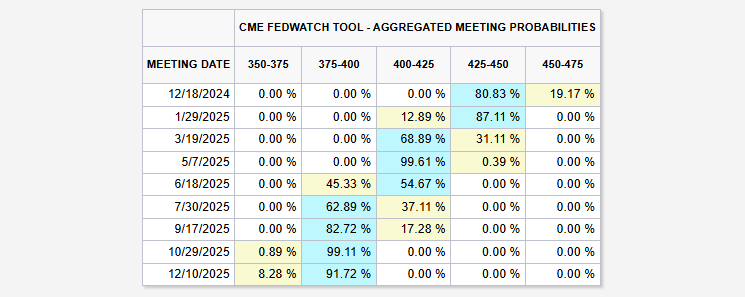

The market got greater confidence for a rate cut in December after today’s reports but is now pricing only 2 rate cuts in 2025. A significant shift from what they were expecting in August.

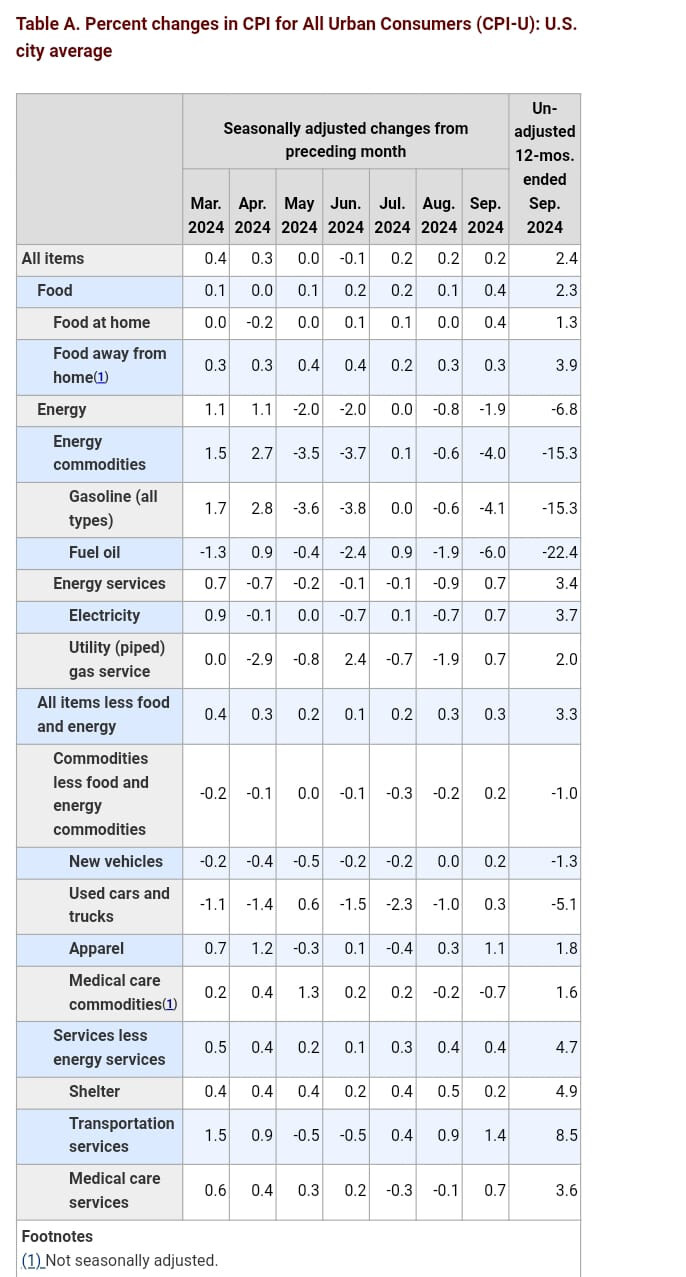

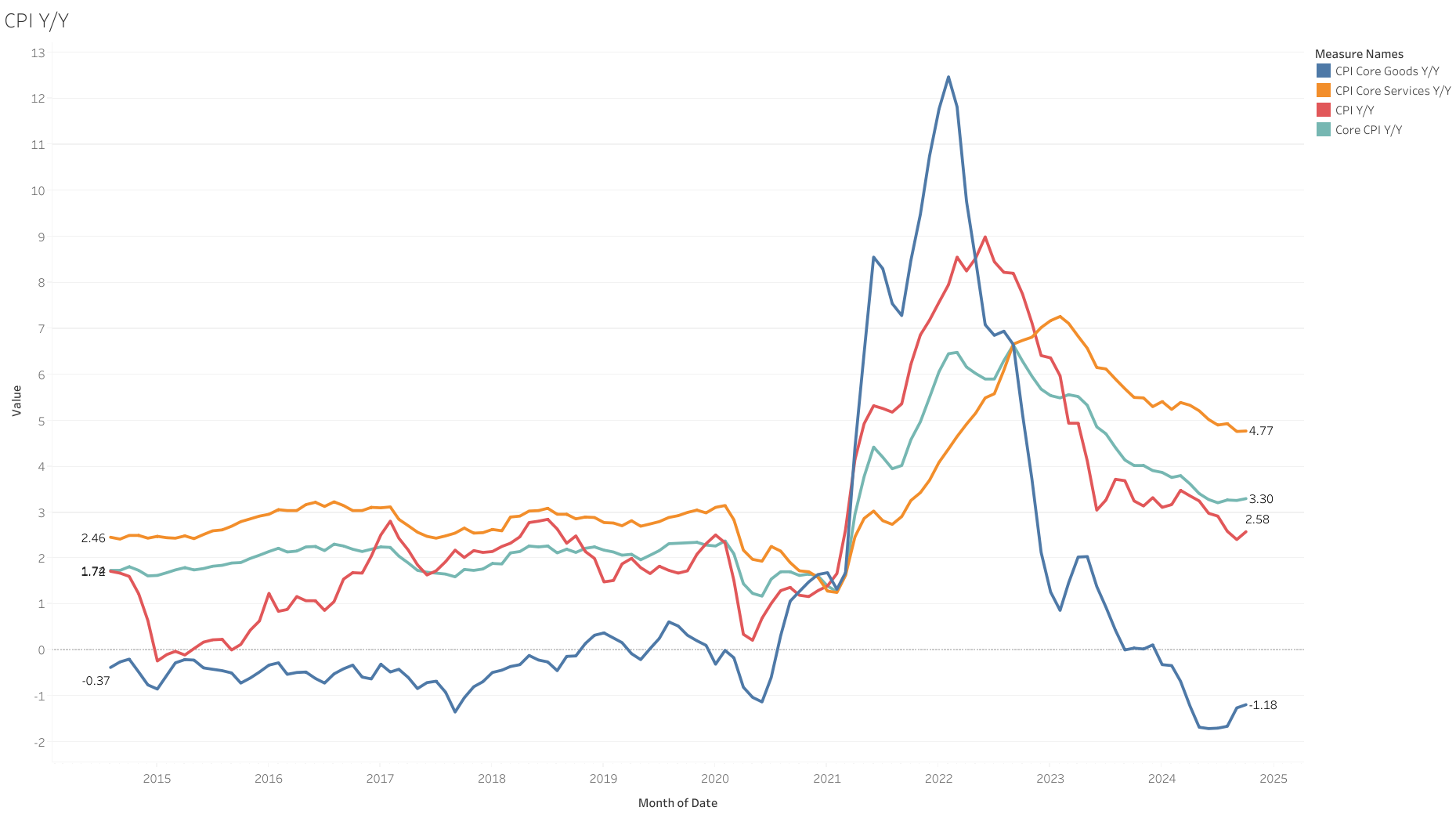

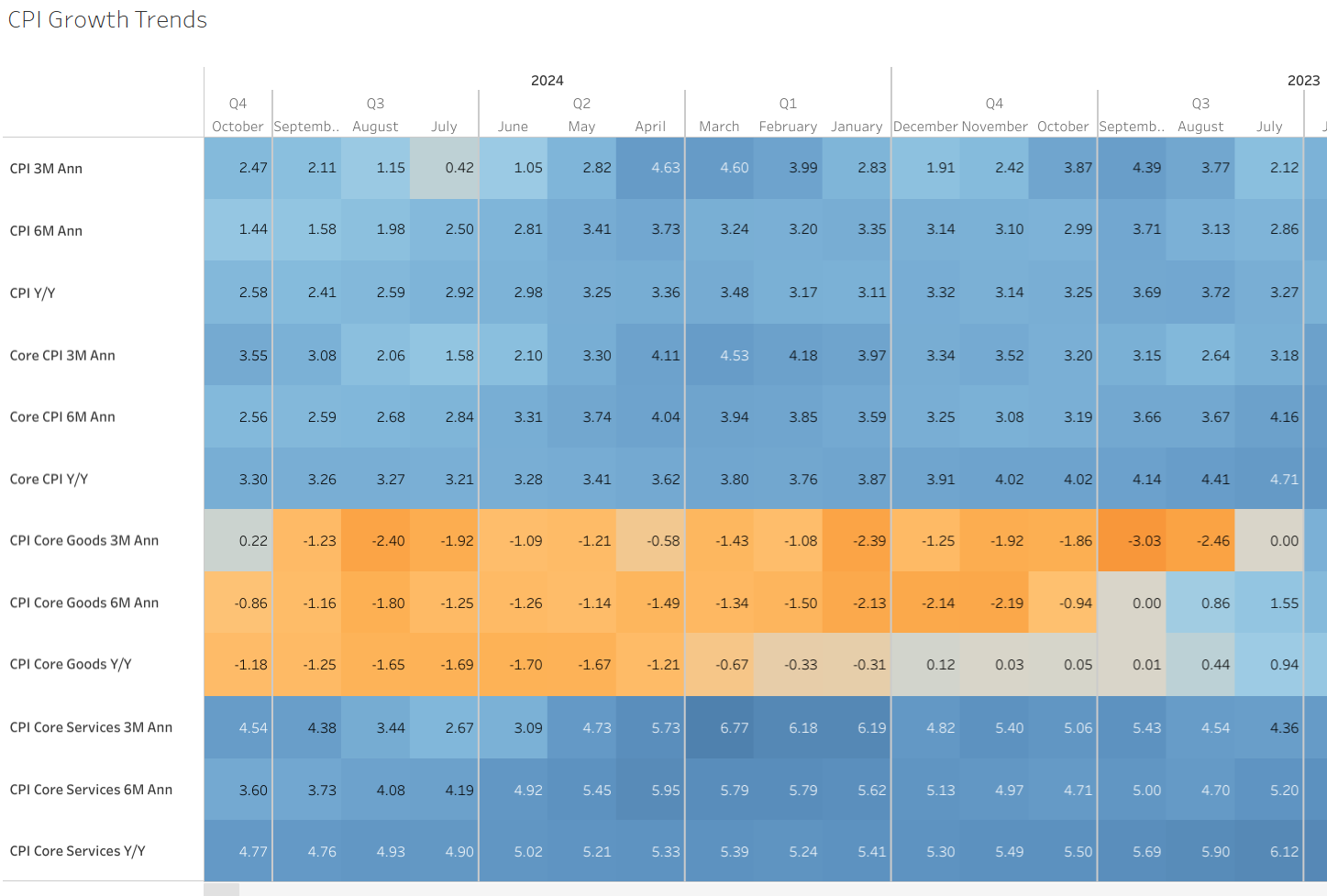

US Core CPI moved up to 3.30% in October, the highest reading since May, increasing slightly in recent months, but mostly stuck around current levels since June.

The headline CPI is volatile due to recent energy movements.

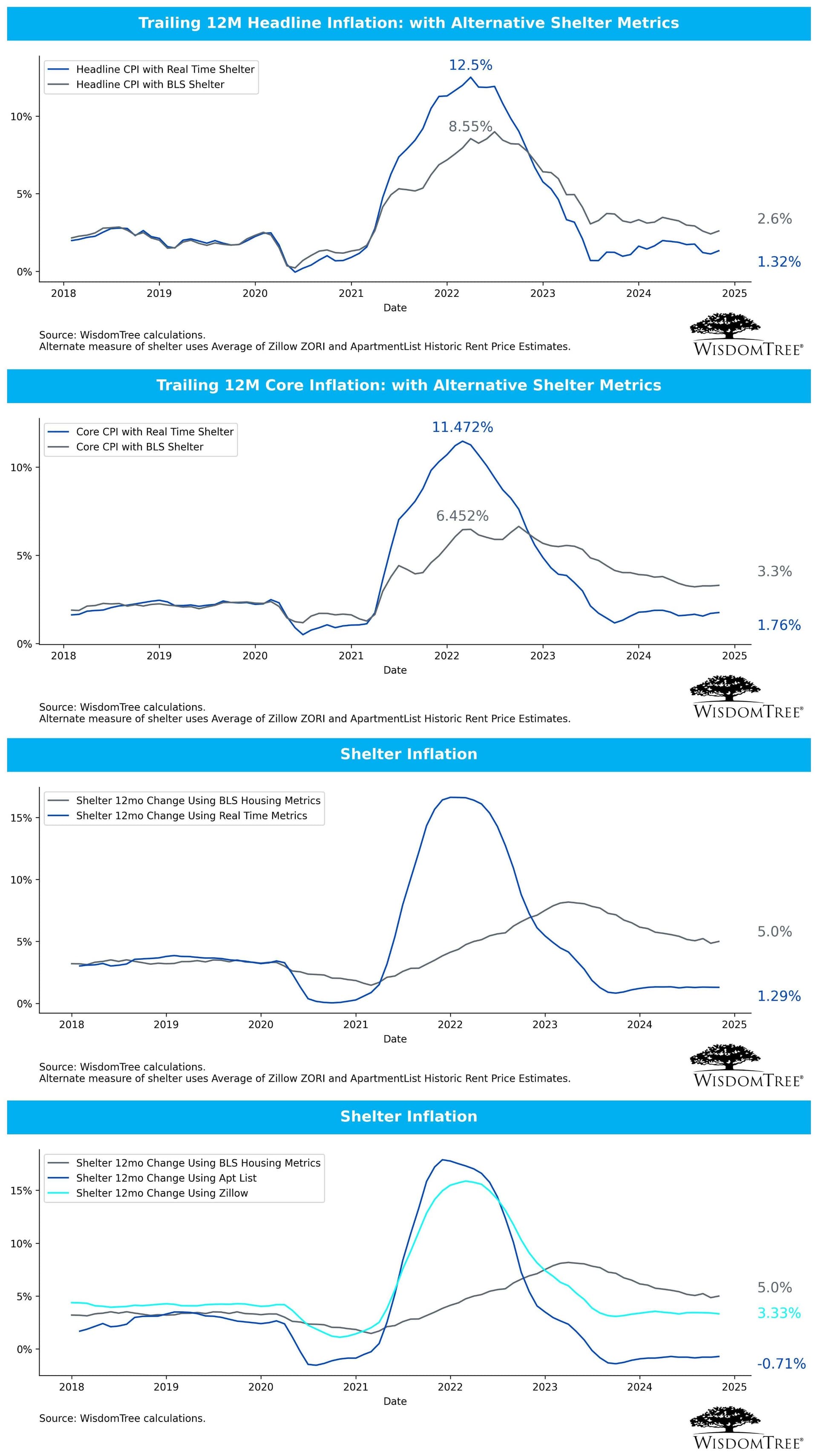

Shelter is still responsible for more than half of the CPI increases. While there’s hope that shelter inflationary pressures will eventually ease, the decline has been very gradual and not linear.

Alternative measures of CPI with real-time rent data show inflation may actually be running below the Fed’s target. Unfortunately, BLS shelter methodology is extremely bad currently, lagging and smoothing a lot of the real changes, so I am concerned also that it get stuck at current levels for a long time.

The recent acceleration in wages (answer here before an overview of the importance of wages, however more in-depth research is needed), rising food prices, and renewed increases in auto prices continue to pose upside risks to inflation.

However, other key components, including home prices (CPI will continue to lag these developments) have remained stable or even declined this month.

Despite recent stagnation in inflation progress, the market has grown more confident in the likelihood of a December rate cut after today’s report, while expectations for 2025 cuts remain unchanged.

Following Trump’s election, potential inflation risks could emerge. In such a scenario, I do agree it would be prudent for the Federal Reserve to adopt a more cautious approach until there is greater clarity on the trajectory of CPI, labor dynamics, and the specifics of forthcoming policy changes.

Used and New Car prices as mentioned above put upward pressure on goods CPI this month

Goods prices have played a key role in driving disinflation thus far, making it important to monitor any pressures in this area closely. While I do not anticipate a resurgence of inflation in car prices given the current industry dynamics, potential policy shifts related to tariffs under a Trump administration could temporarily alter this trajectory.

Core Good increased 0.31% m/m, the highest since May 2023. The 3M annualized trend back into positive territory.

Tomorrow’s CPI is expected to come in on the hotter side, with a projected increase of approximately 0.4% for the headline figure and 0.3% for core CPI.

There is much improvement expected on both metrics on demcember, but January CPI expected to improve a bit.

The risks to the upside remain similar to those outlined in the November 2024 report and continue to outweigh downside risks:

New car prices surged significantly in the latter part of 2024 and are now approaching their previous peak once again. Used car prices have also shown upward pressure. Both sectors played a key role in goods disinflation until now.

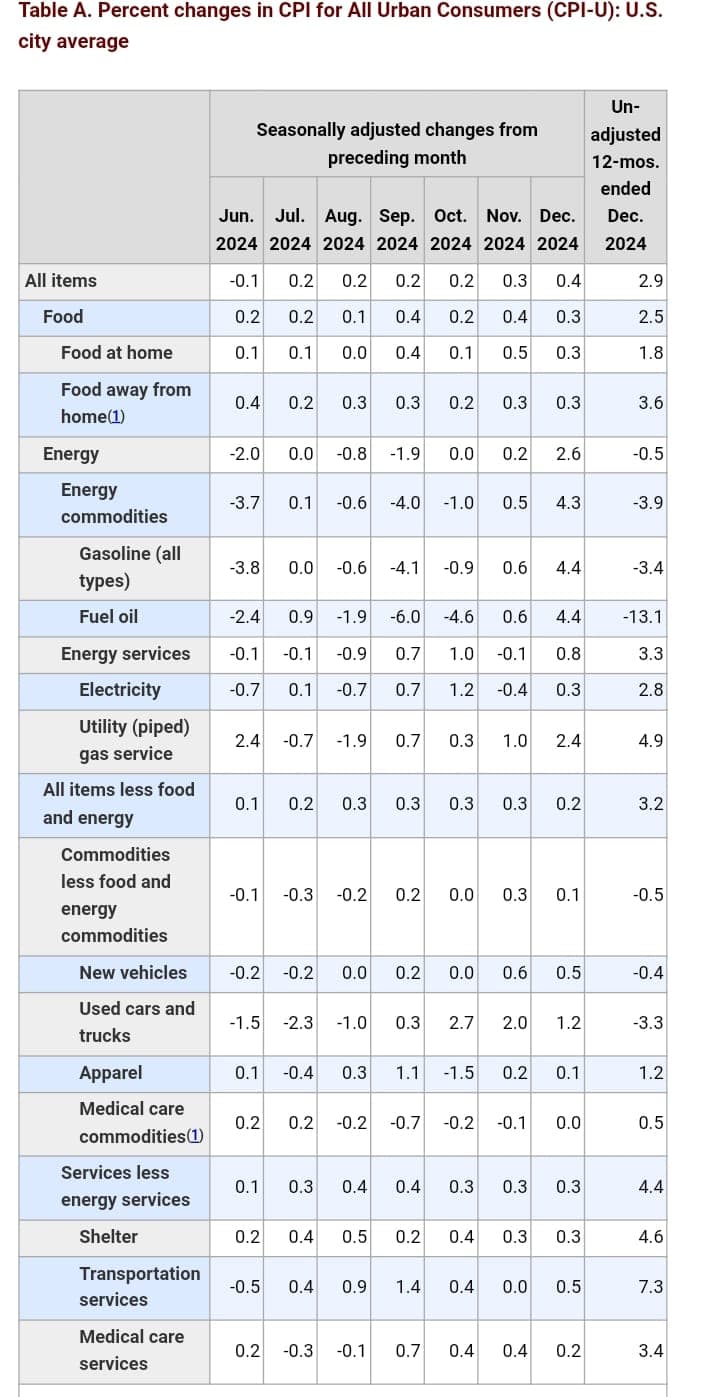

Food prices, despite a decline in December, have risen sharply year-over-year

Oil prices, particularly in January, have resumed an increase in prices

Wage growth remains persistently around the 4% level. Policies on immigration could make this a bigger problem.

Potential rising tariffs could impact producer price inflation (PPI) and import costs, both of which have already been trending higher recently.

Similar to labor market report, this CPI release doesn’t necessarily changes the broader trends on inflation, it seems that it remains sticky, with upside risks still present

Core CPI declined only slightly by 0.05% to 3.25% year-over-year (0.23% m/m vs. 0.26% expected). It continues to be elevated and above the Federal Reserve’s target, without much improvement in all 2024 (Dec 2023 Core CPI: 3.91%).

Headline CPI reached its highest level since July, driven by a resurgence in energy and food prices.

Notably, many key components are currently above the 0.3% monthly increase on a 3-month moving average basis.

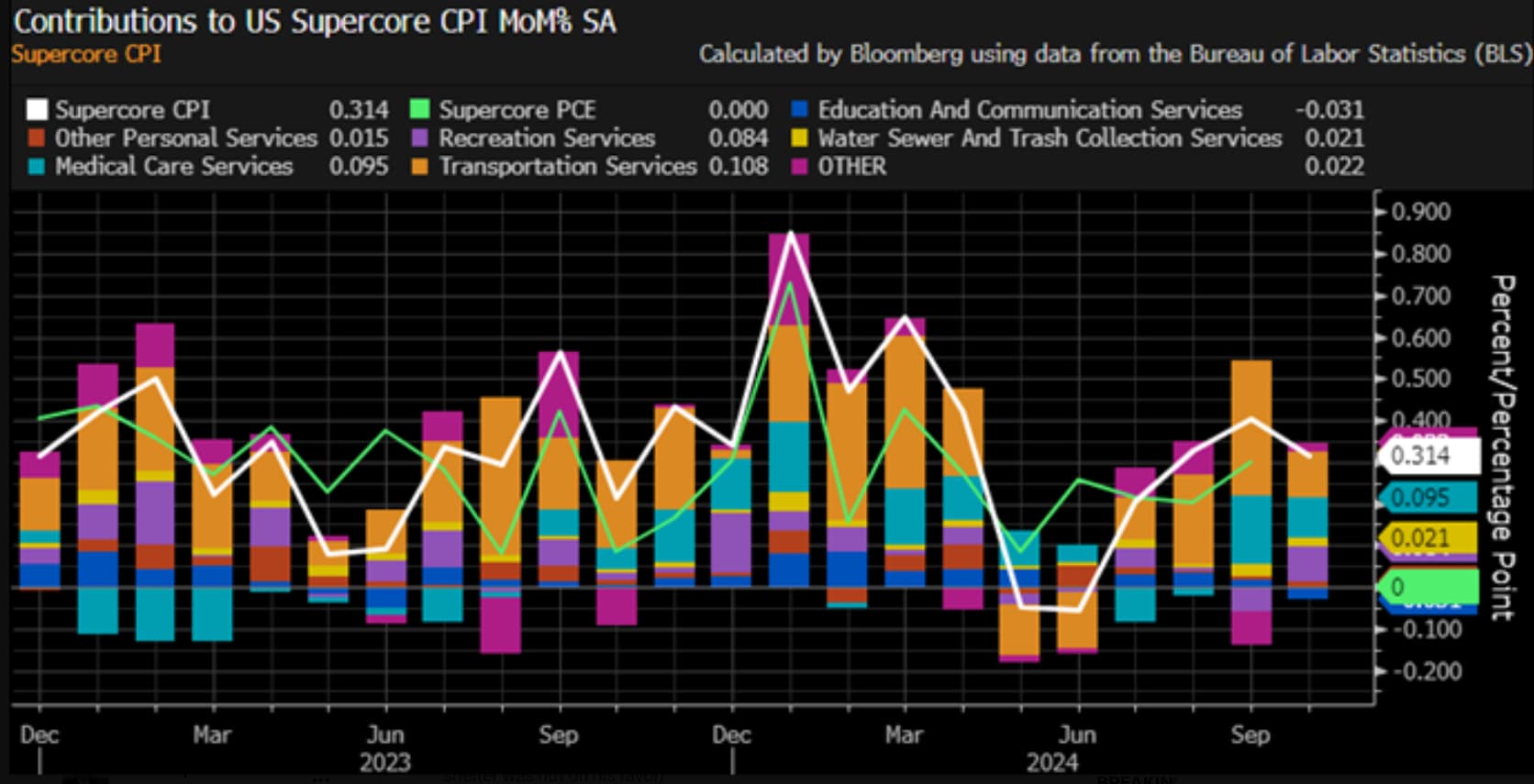

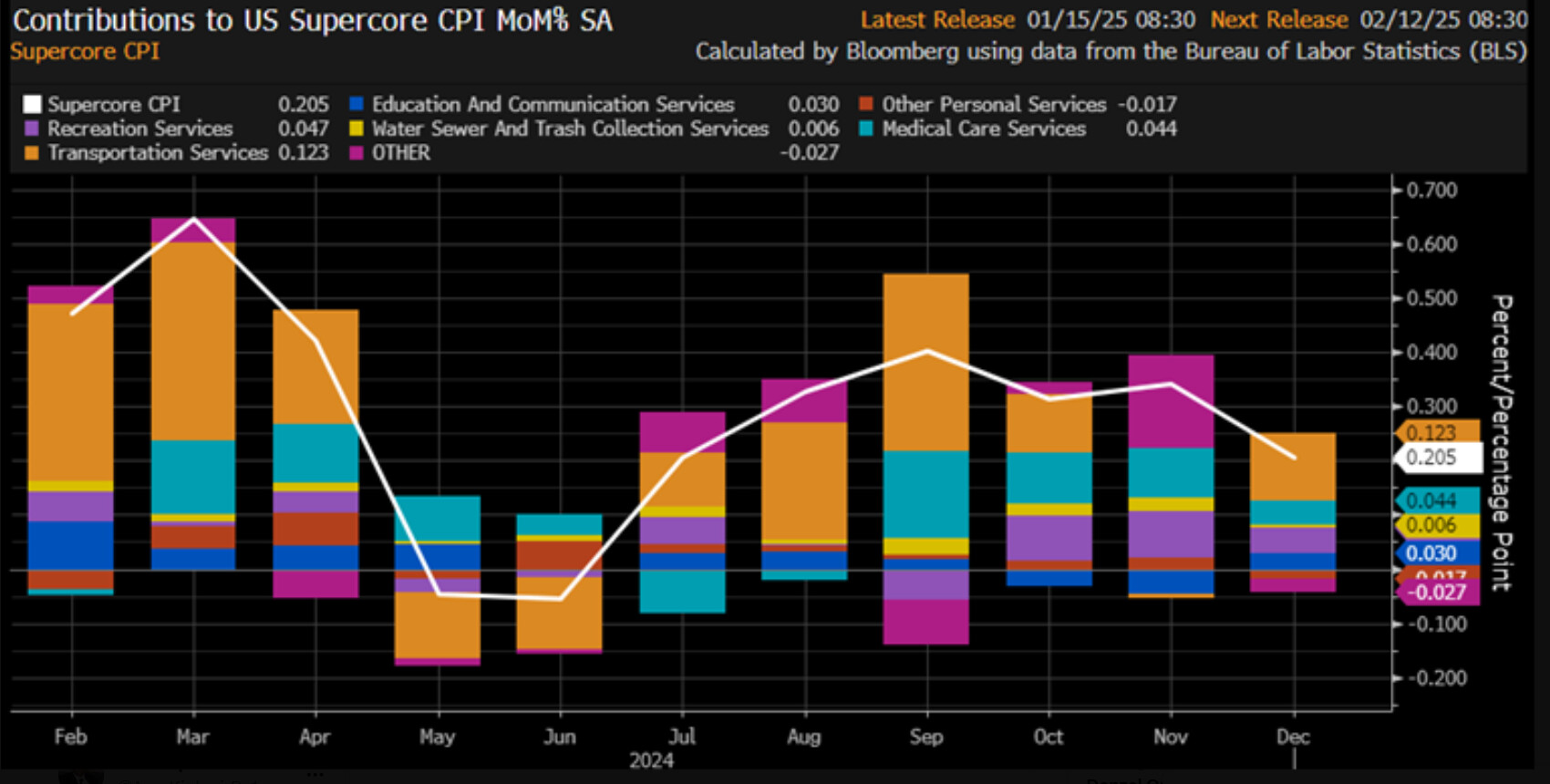

A positive takeaway is that the shelter component remains on a gradual downtrend, however at a very slow pace. Additionally, super-core inflation registered its softest reading since July.

I think this report is just a relief to the markets, which could have expected even worse-than-forecasts numbers

In my view, this is an encouraging development, but it’s not enough for me to dismiss inflation concerns entirely. Consistent progress across multiple reports is needed to confidently conclude that inflation risks are very low, especially with potential headwinds with the coming administration.

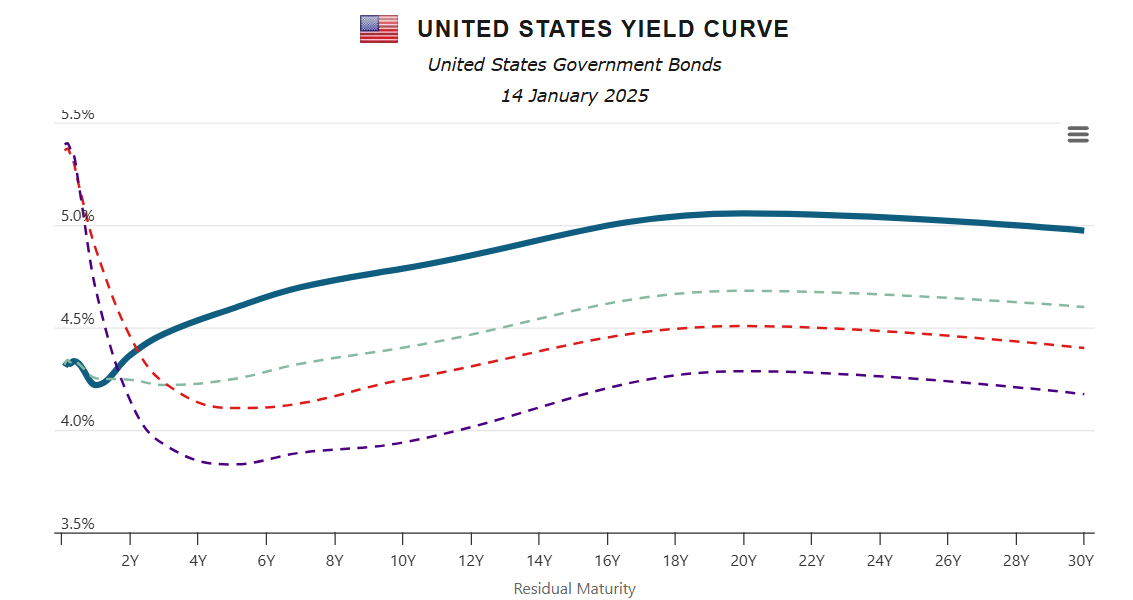

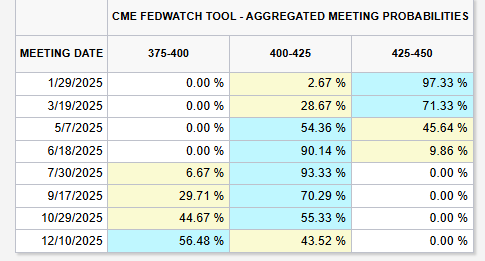

After the CPI reports market are currently slightly pricing two rate cuts for 2025 again, with the first one in May. And 10-year yields declined to 4.66%

Expectations for January CPI show no additional progress on inflation for another month. However, Cleveland Fed projections suggest February could mark the start of another improvement.