This is actually not a very positive report, even if headline inflation is still coming down y/y.

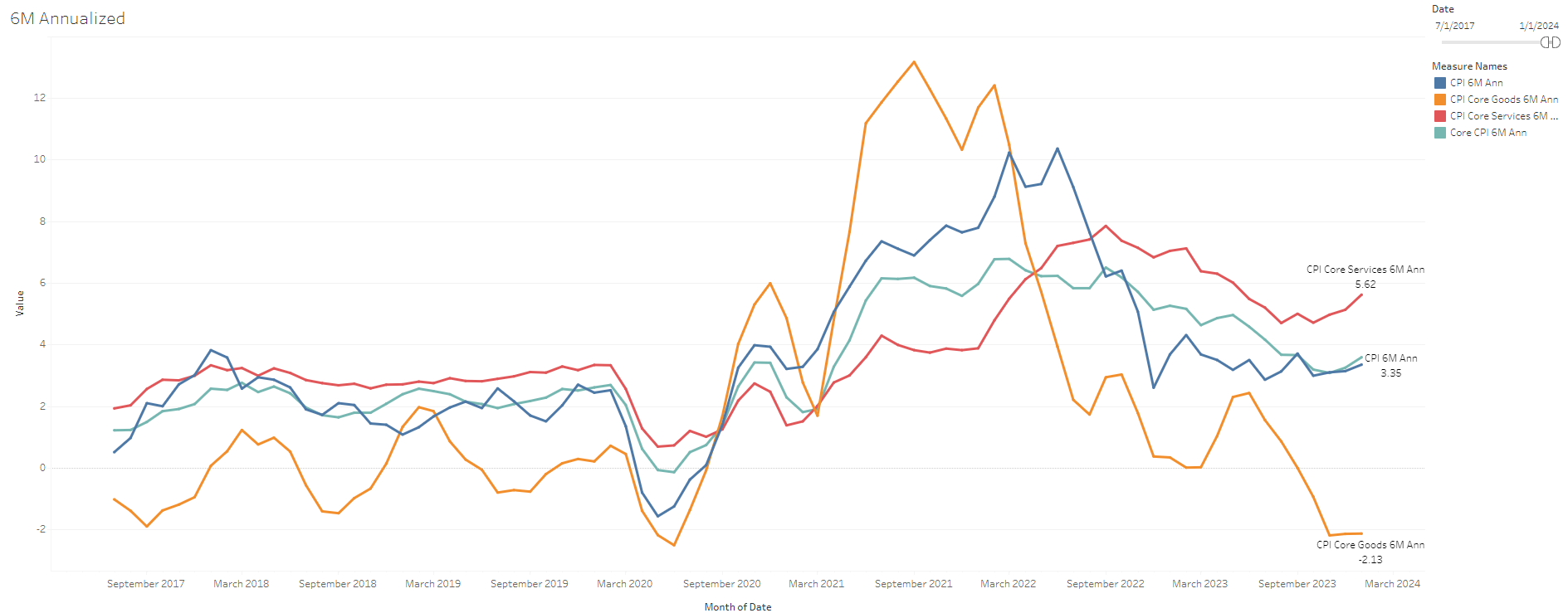

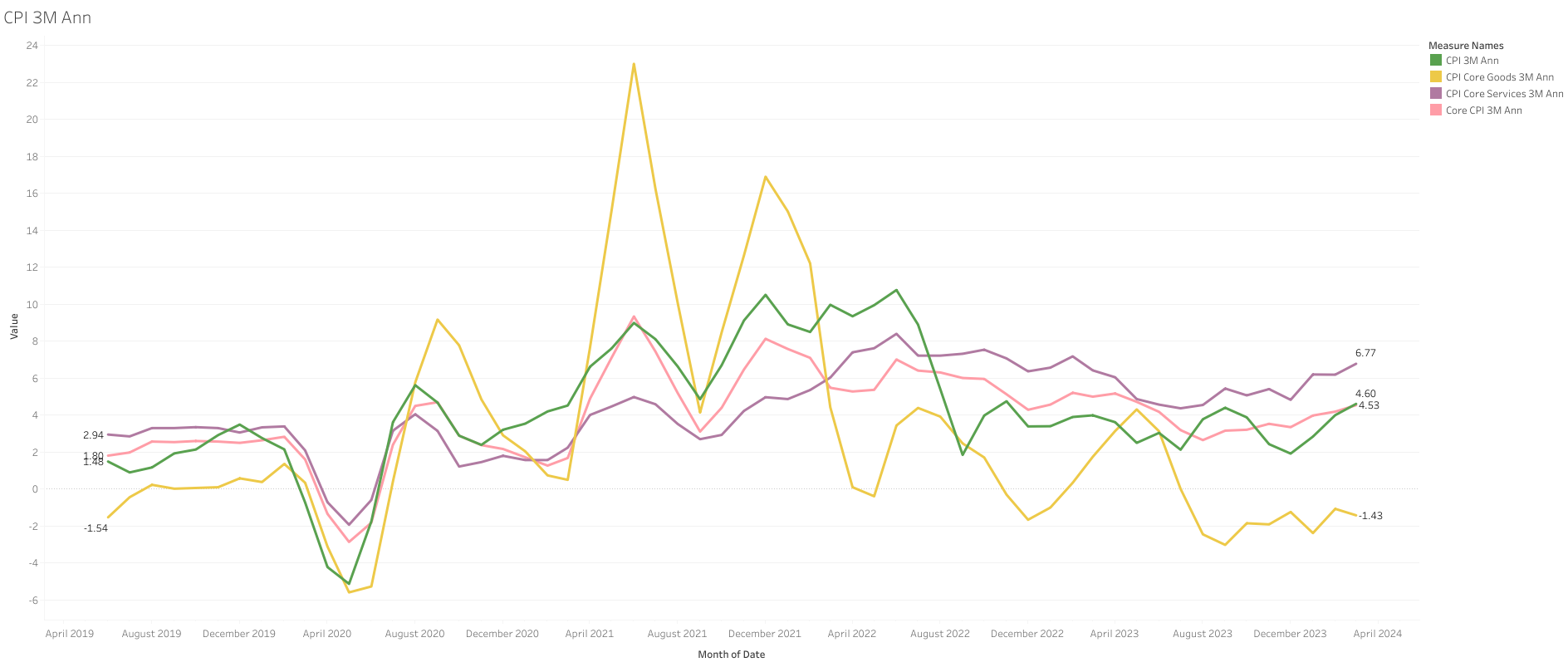

Is just 1 month and seems that seasonal adjustments have been screwed up after covid (have not looked at this myself). But at the same time, the 3/6 months trends are especially concerning.

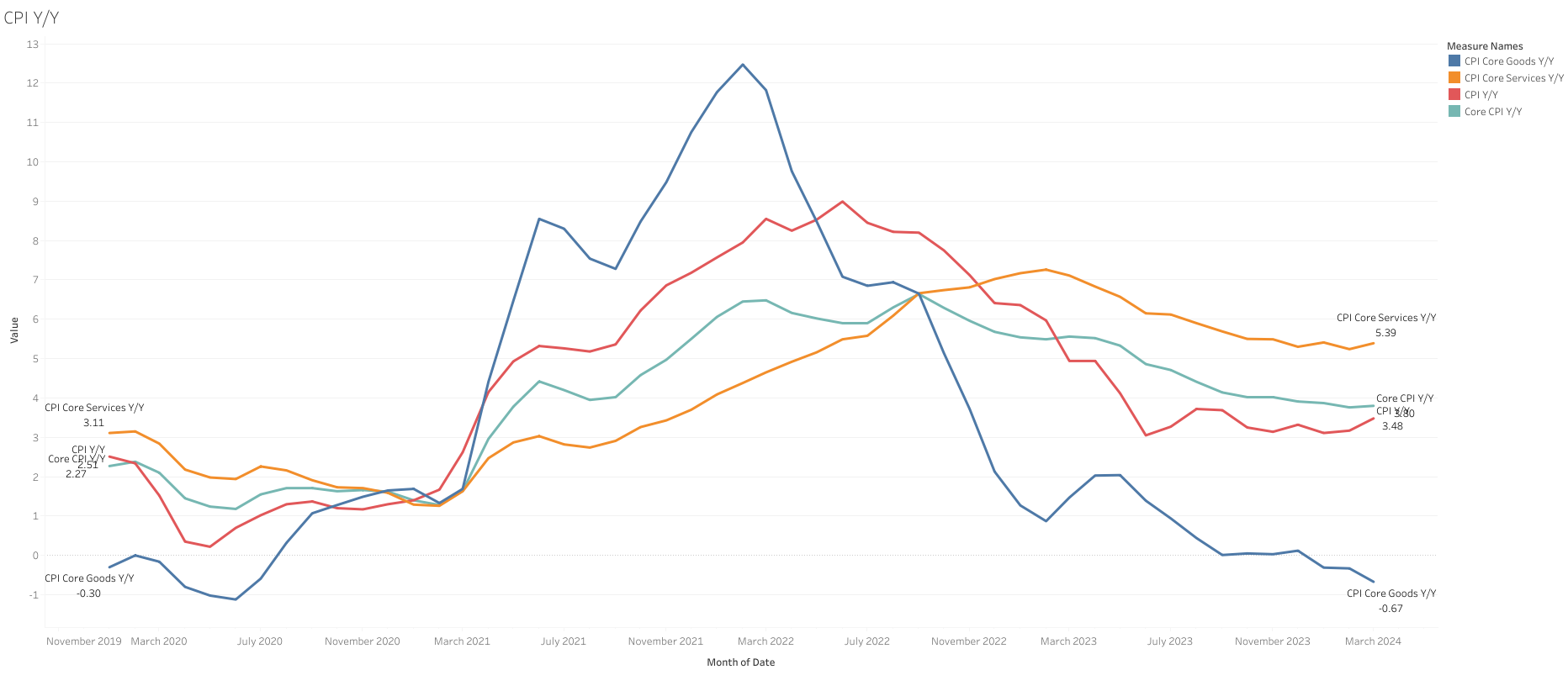

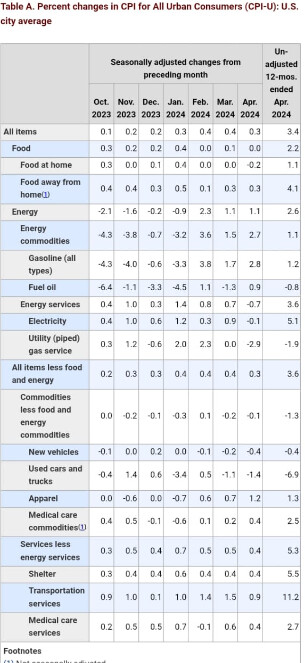

Important goods disinflation, especially coming from used cars, but was not enough to offset services.

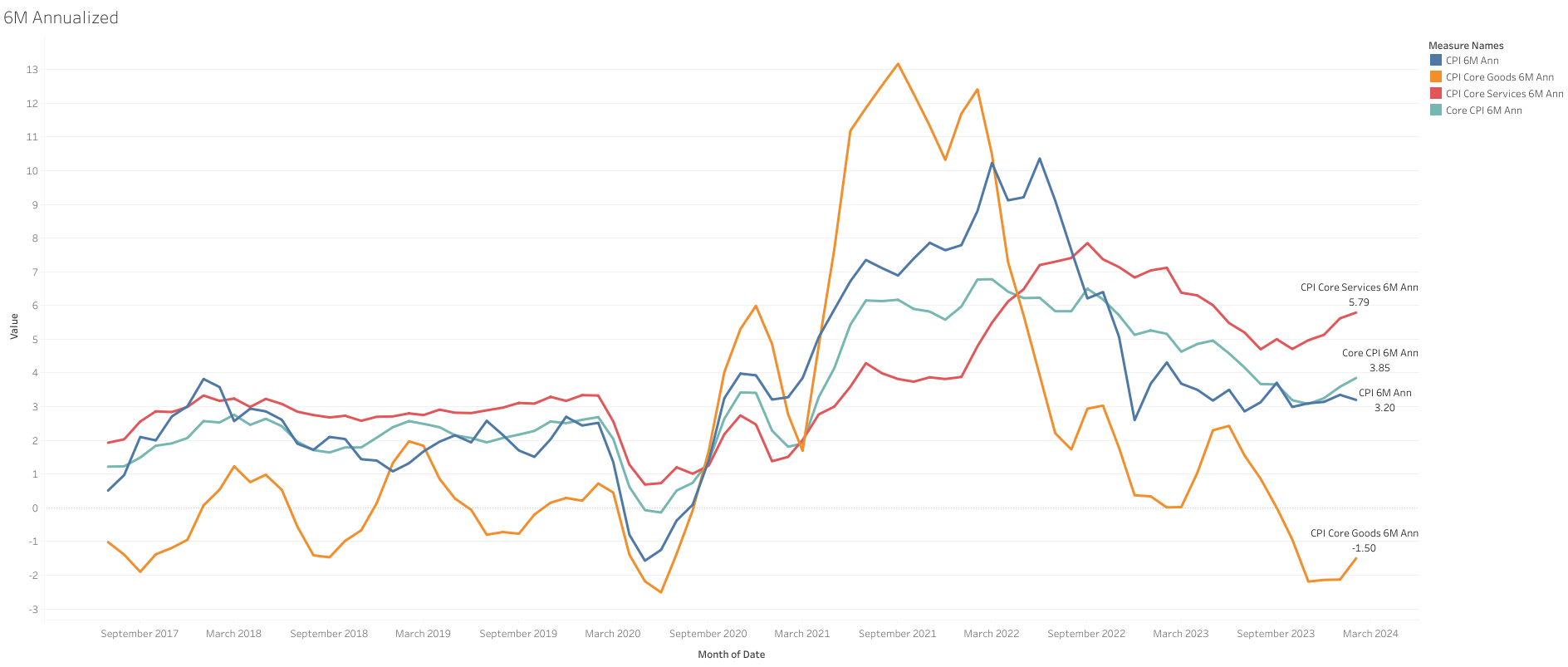

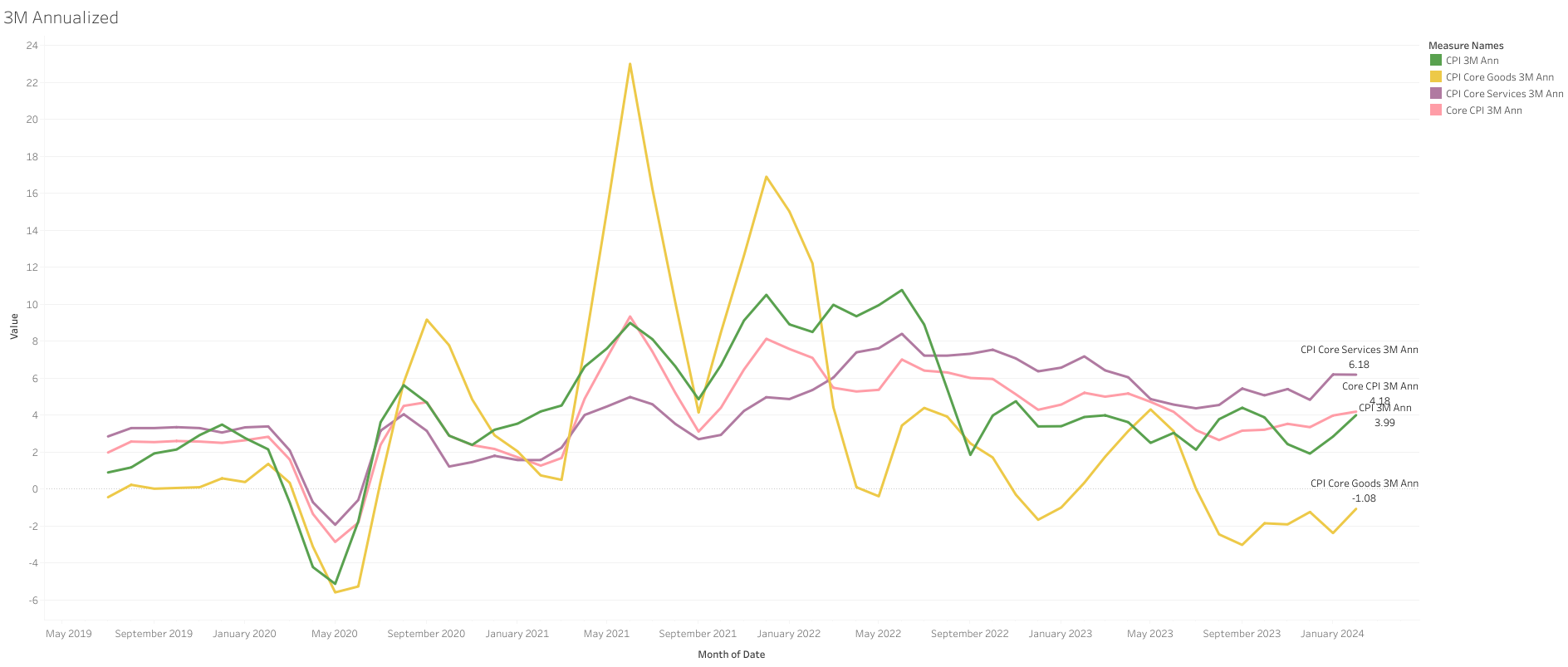

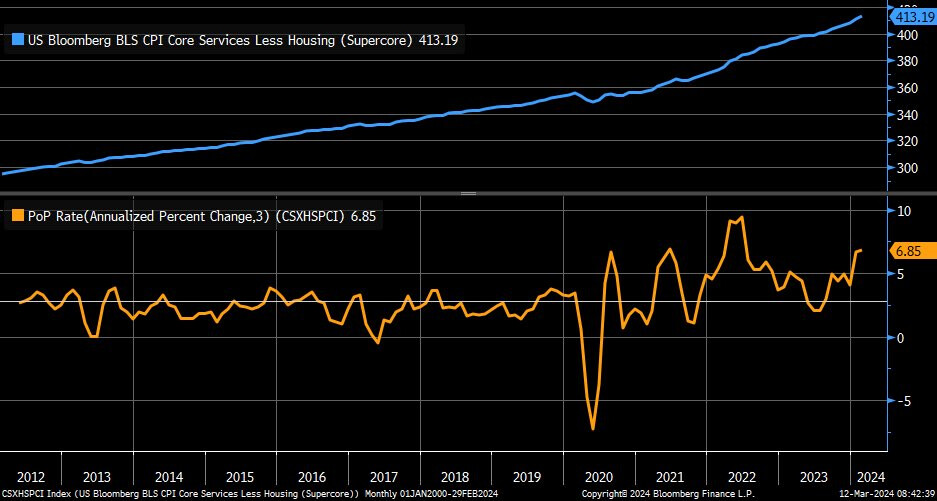

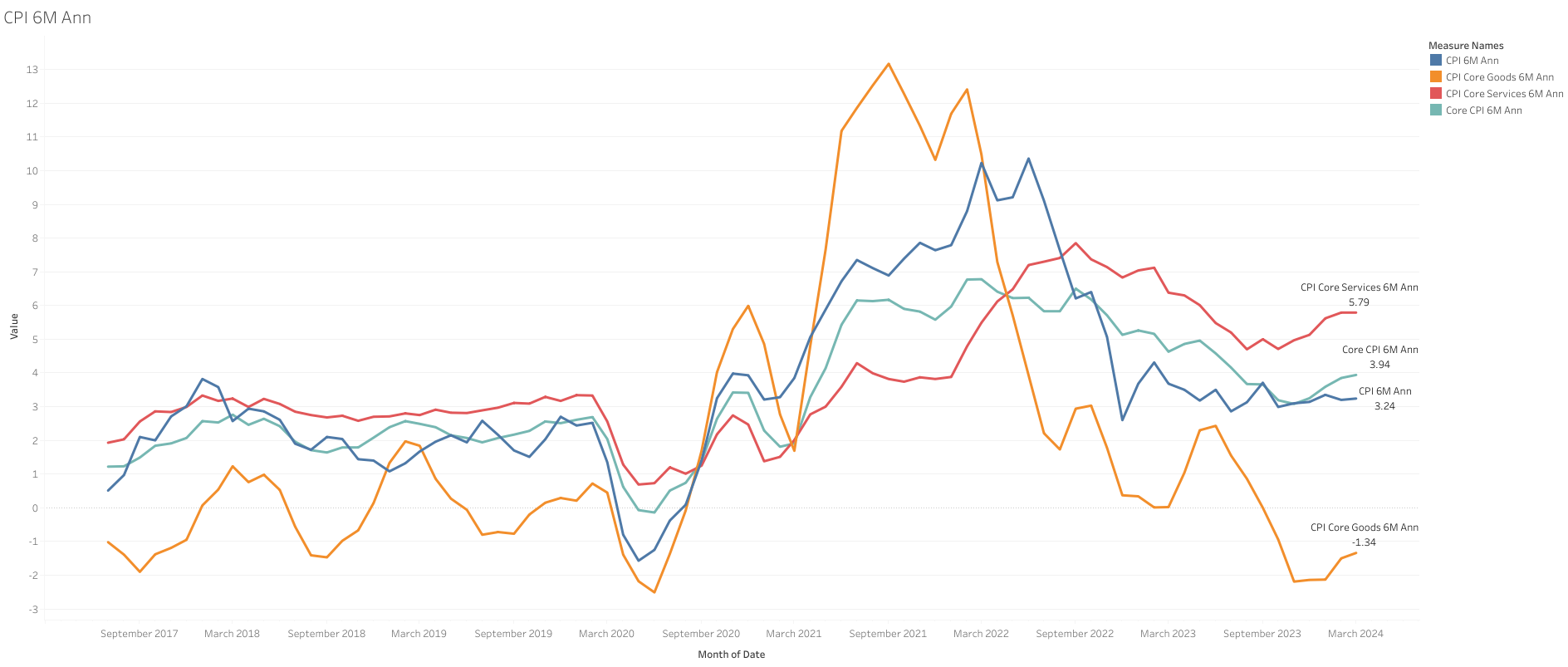

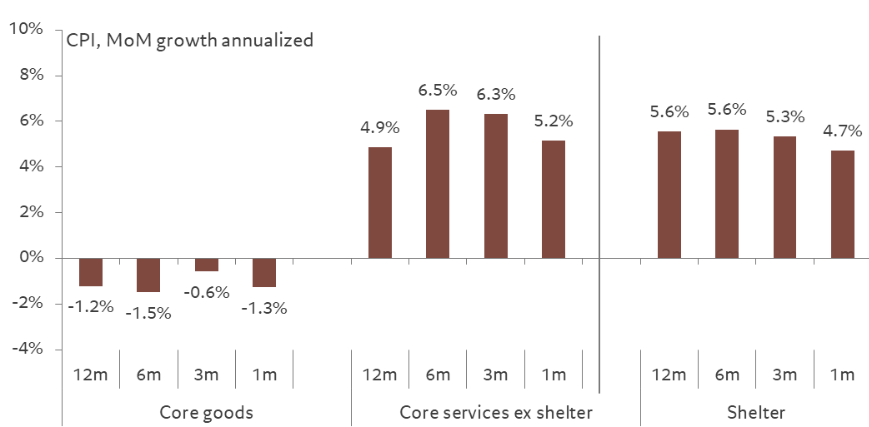

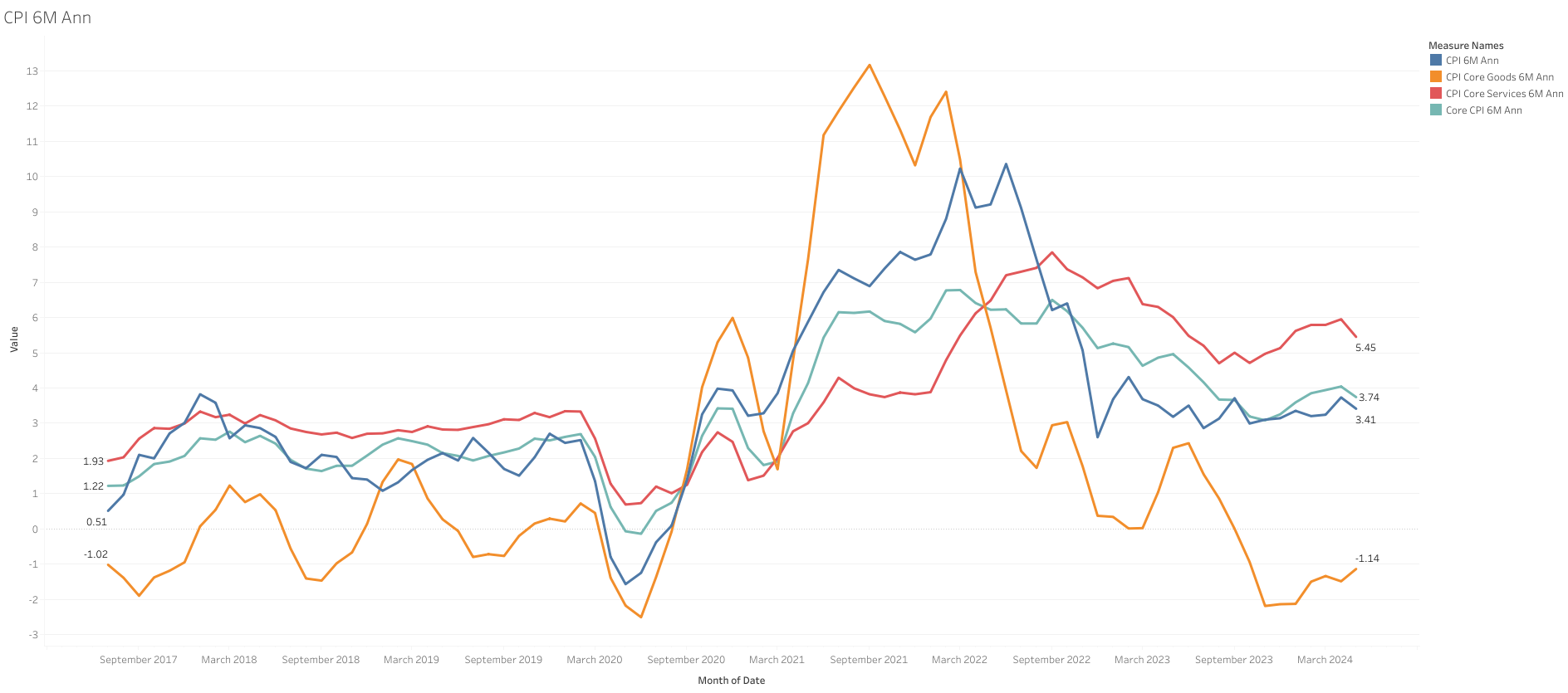

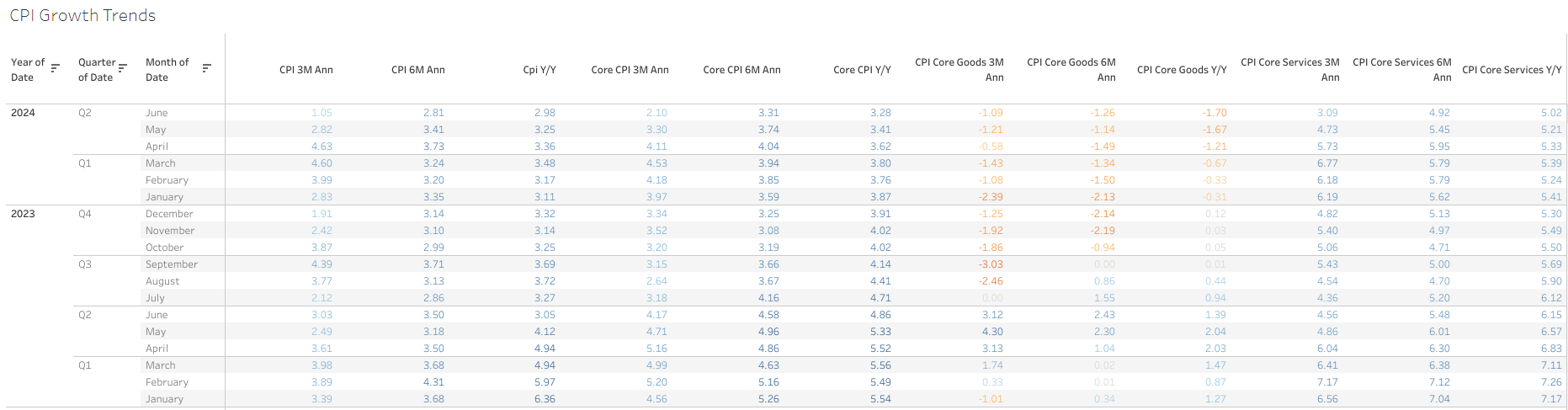

3 month and 6-month annualized rates are accelerating, especially for services. All bottoming around October.

Shelter is moderating very slowly too, and 3/6 months trends are not the best either. I still expect more moderation from shelter, but it could end up taking longer and maye more modest than anticipated. Especially with home prices at again ATH.

Seems as PMIs pointing to increased inflationary pressures, especially in services, were not wrong.

And appears it will be difficult to control inflation or bring it to target when the economy continues at this pace, and with the huge loosening of financial conditions since October.

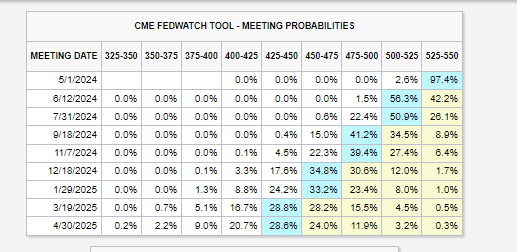

After the report, cuts are not expected until June now, with 4/5 in total. I still think 3 cuts as the FED signaled could be reasonable, but no more than those if numbers continue to cool this slowly and remain sticky.

I do like Mohamed’s thinking, is not that this is huge miss and is in line with the recent trend, but current expectations are so high due to la la land thinking in the markets, that anything that is a treat for their desired rate cuts and liquidity will have an overreaction, and vice-versa.

Mohamed:

Wondering how a small miss on the US inflation numbers can result in such a spike in yields on US government bonds.

A lot of it has to do with the extent to which markets had embraced, subject to limited critical thinking, the narrative of a very soft landing that allows for sizeable early cuts by the FederalReserve.

Today’s data release does more than serve as a soft reminder of the challenges of the last mile in the inflation battle. It also points to complex analytical issues (such as the level of the neutral rate) and the insensitivity of certain sectors of the economy (e.g., services) to higher interest rates.

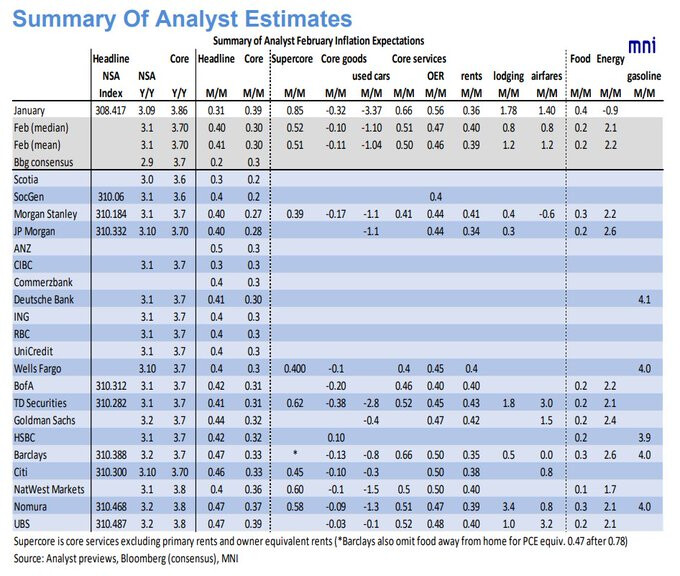

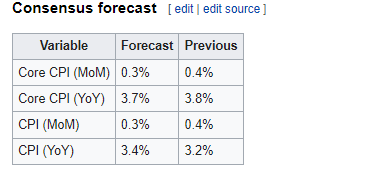

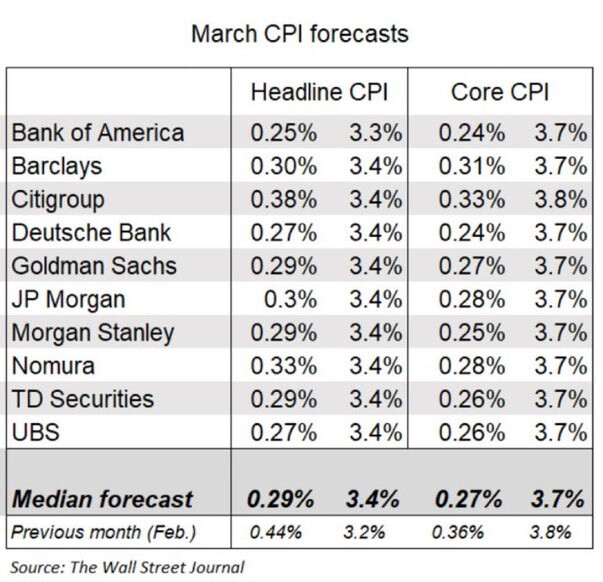

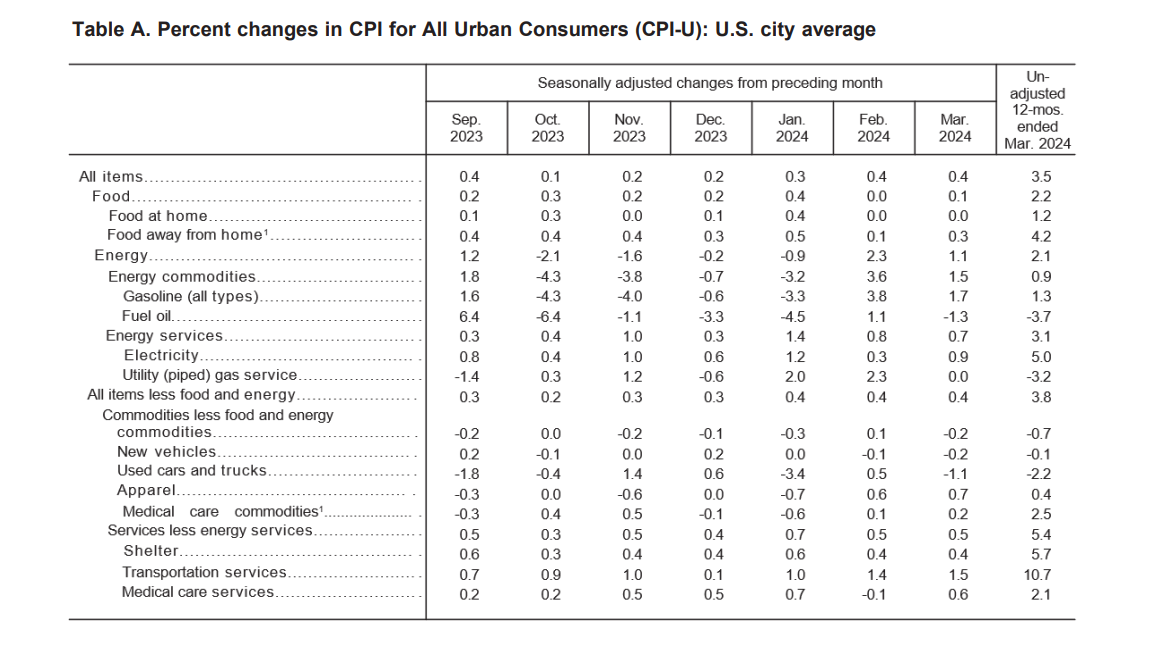

There is not much improvement expected for February CPI. Actually, I would say the expected M/M increases remain high, including super core, services, and rents.

Energy had a significant increase in January, which will most likely put pressure on headline CPI

Used and new car prices declined again in February, continuing to put downward pressure on goods CPI.

Wages had a nice downside surprise, but remain ~4% y/y, so don’t expect that much impact on services yet.

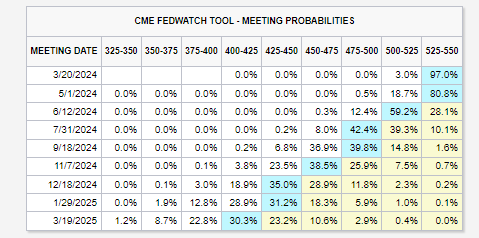

From last month rate expectations have changed very significantly. Now cuts are expected to start until June, and on average ~3/4 cuts for 2024.

If inflation continues to surprise, IMO cuts could continue to be pushed further.

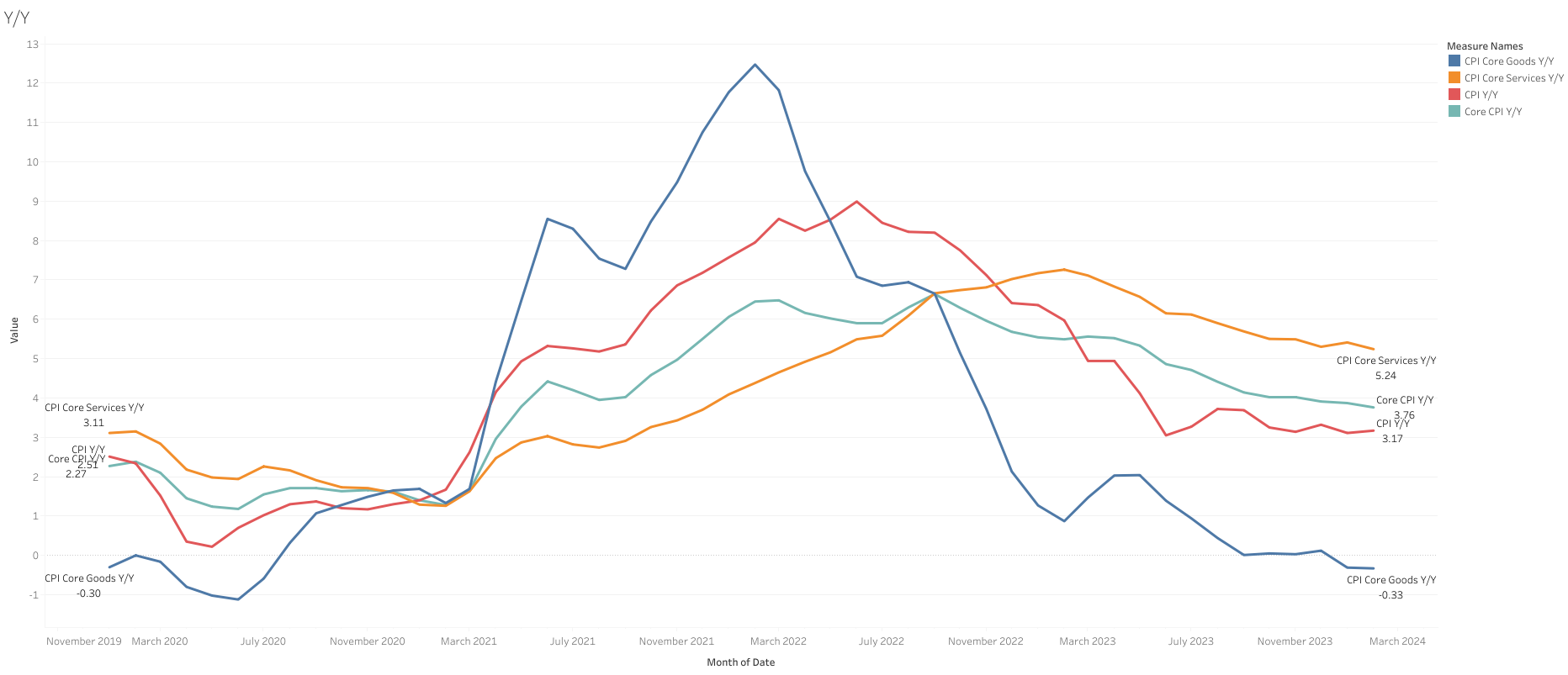

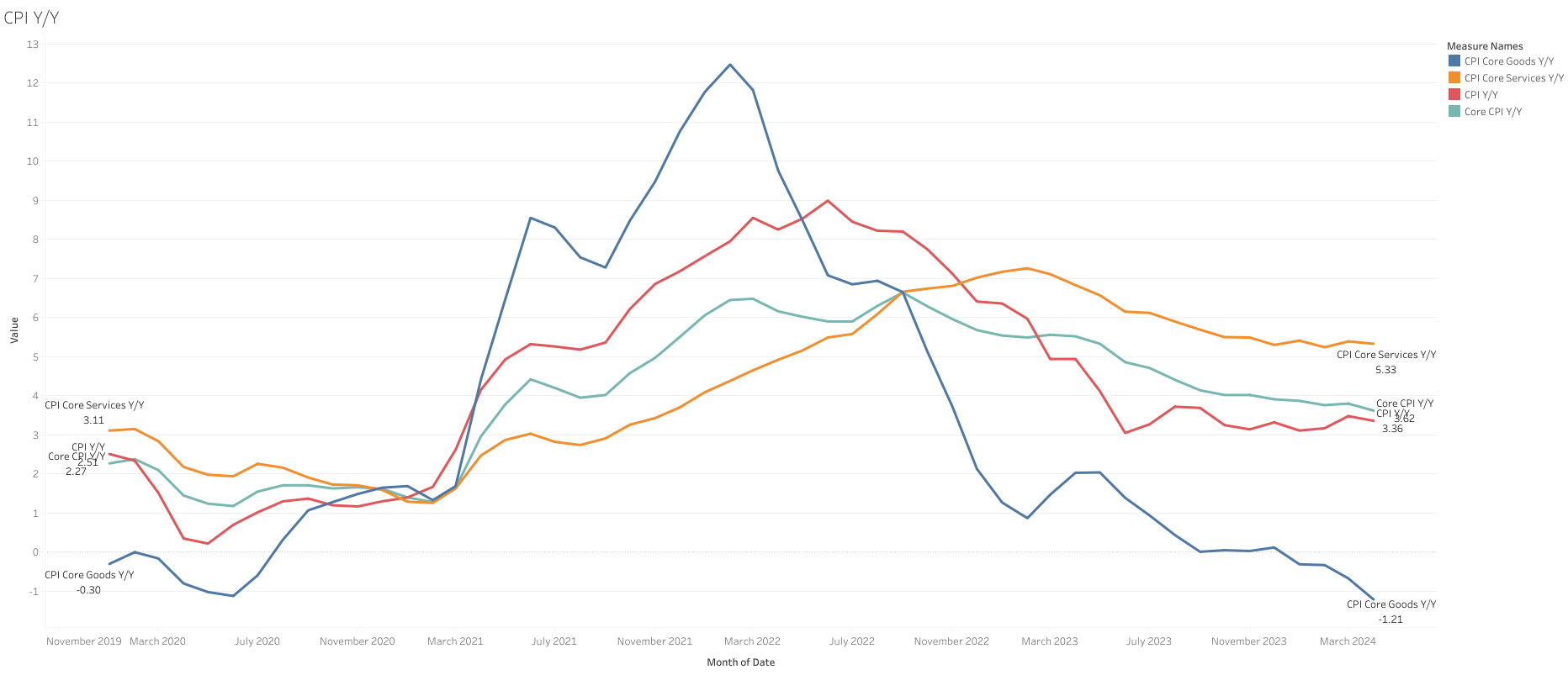

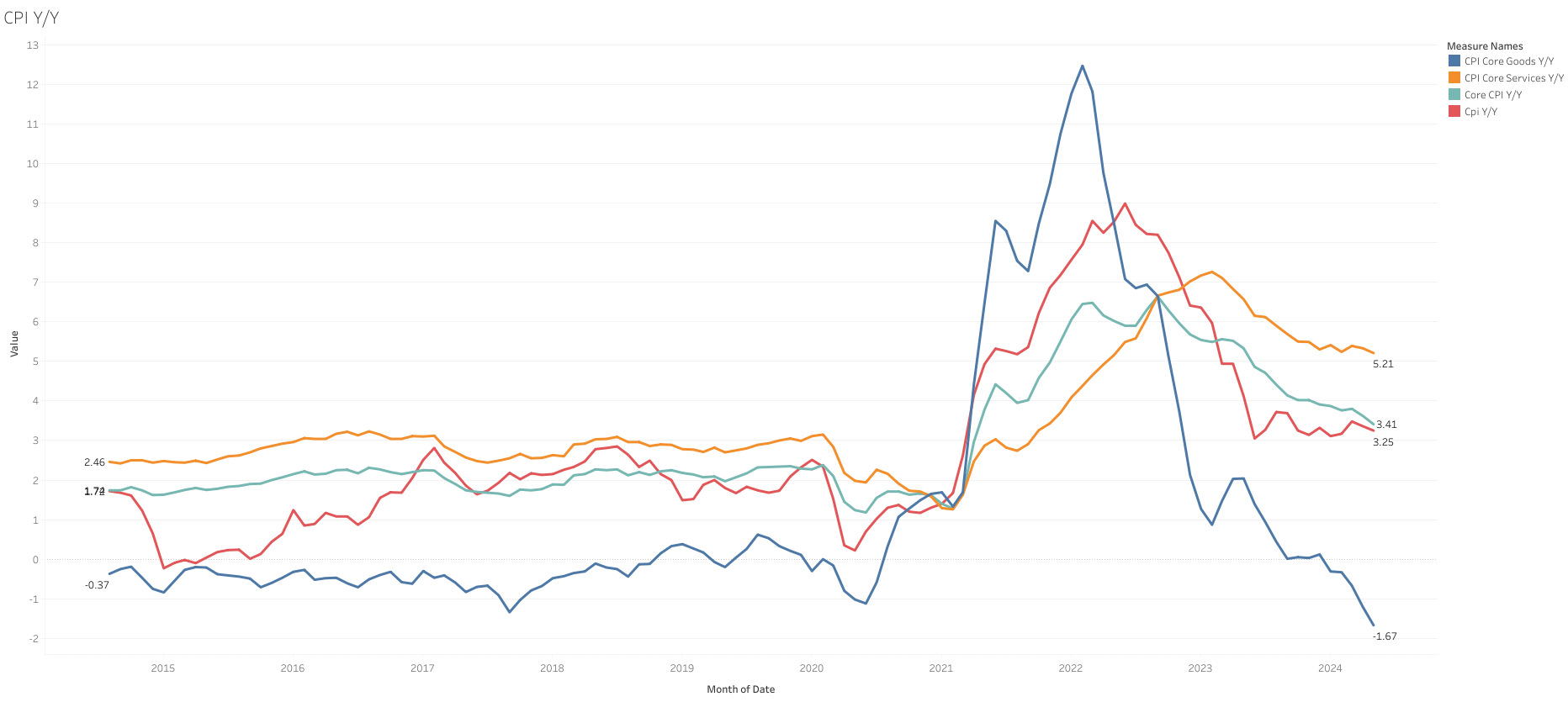

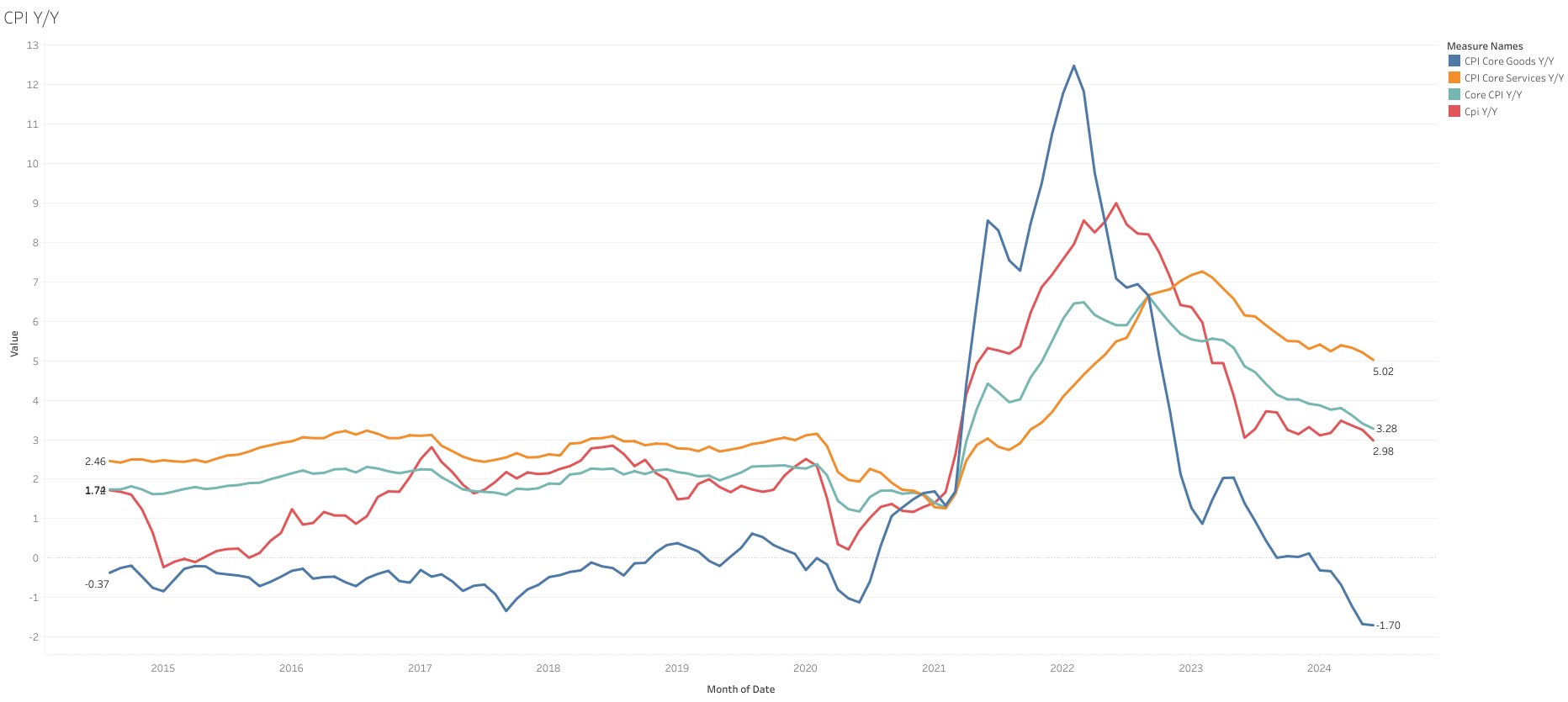

Overall CPI has stopped improving since June 2023, but core CPI is still slowly going down.

I do not expect rate cuts soon with these numbers, and the market’s reaction today makes no sense to me, unless they are starting to feel they need to protect against a potential higher inflation with assets like stocks and real estate.

Putting all together, most of the more important markets/indicators developments were not great this month, except for car price declines, and wages with more moderate increases.

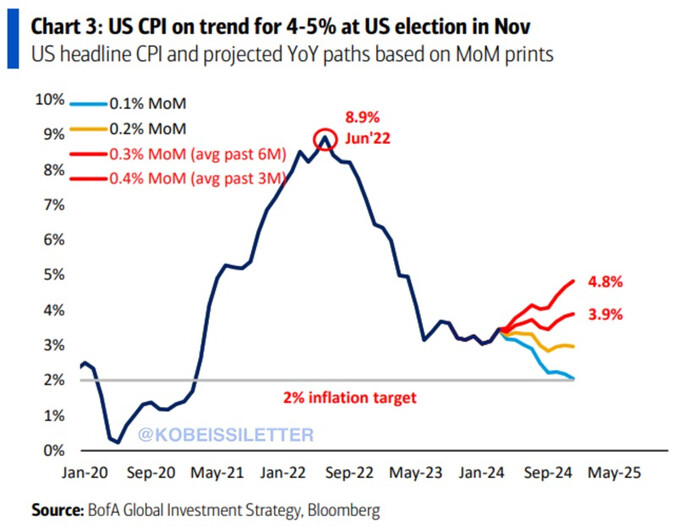

The increases seen are still not indicative that inflation will be 8-9% again or something, but it is worth monitoring more closely because if these developments continue I would start to become more and more concerned about inflation reaccelerating again (maybe 4-5%)than a recession in the short term. Indicative that the FED could not be restrictive enough yet, or needs to stay this high for longer.

*There are always lags in CPIs, so so these developments are sometimes more important for future CPIs releases, than the current one *

Energy continued to increase, with both oil and gasoline up more than 5% m/m. Oil is currently 10% Y/Y.

Food prices also increased in March 1.1% m/m, after 7 months of declines. Still -7% y/y.

Rents also experienced the second month of increases 0.6% m/m, while at least housing prices have started to moderate again with second month of declines -0.1 m/m

New and Used car prices both experienced declines during March again, 0.4% m/m and 0.9% m/m respectively.

PPI came in significantly hotter in February 2024, at 0.6% m/m.

As of today, the markets still are pricing on average ~3 cuts this year starting on June.

I think they are maybe too much still with the state of the economy, and I would also start to question it more if developments continue this way.

4 month consecutive readings being above expectations with an upside trend could be something more, and not just noise.

I somehow think it would be the FED fault, they never should have been that dovish after November/December, allowing financial conditions to get so loose, and everyone thinking everything was perfect and solved.

On top of that, we have the fiscal spending without any moderation.

But at the same time still think that there is still disinflation forces going forward in shelter, autos, car insurance, but I have been thinking this for long already without materializing, and maybe I should start to question it more.

3M and 6M trends continue on an upside trend, especially services.

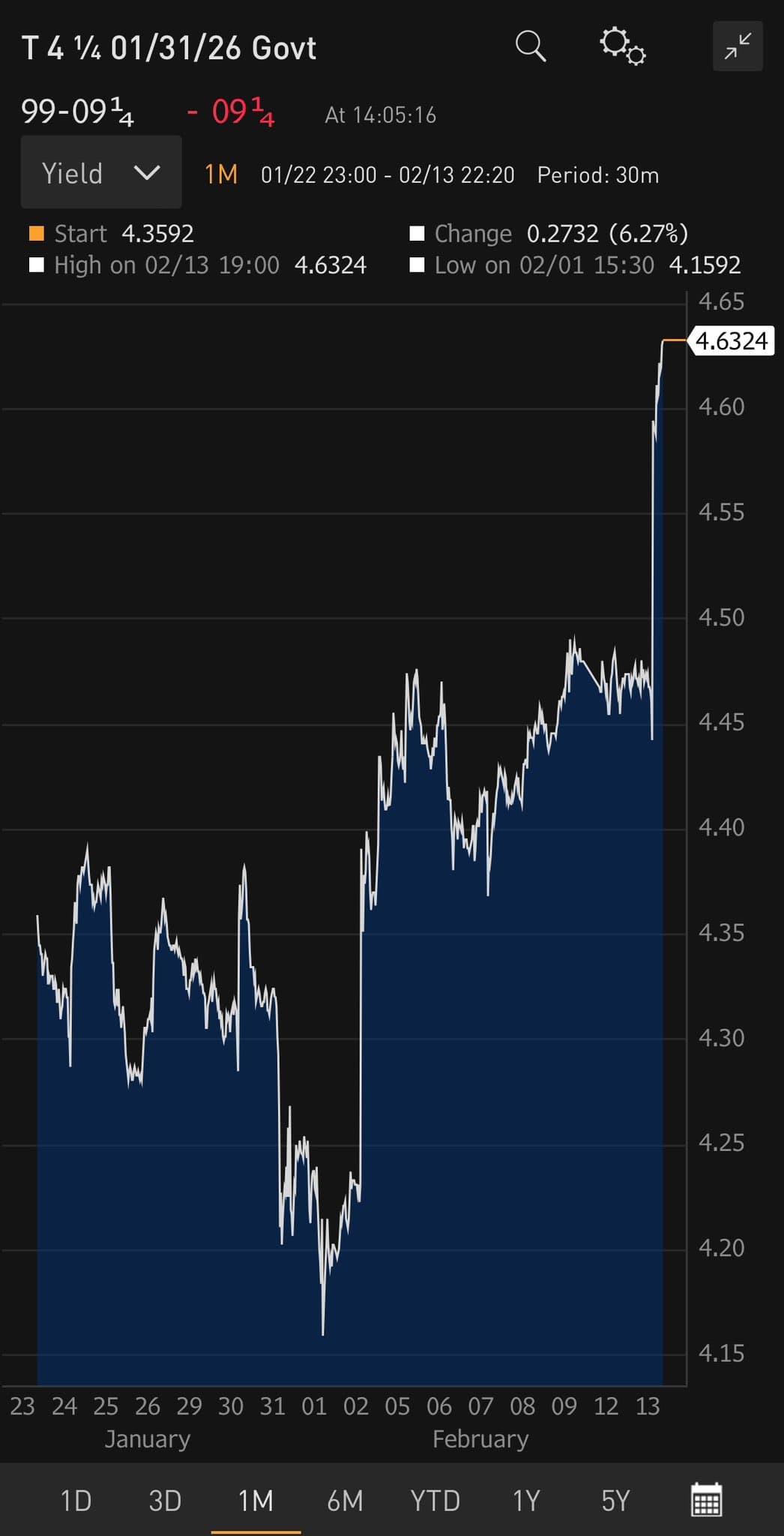

Markets completely changed rate expectations. Now rates are expected to come until September, with 1-2 cuts in 2024. Yields also went up. 10Y yields at 4.53% currently.

Powell said in the last conference that inflation was just expected to have a bumpy road in its way to 2%, I just hope this is not really becoming their new “inflation is transitory” mistake.

But to be fair he also said he was uncertain if this was only a bump in the road or something more.

Path for CPI becoming more difficult. Even a 0.2% m/m would mean around 3% inflation at year end.

And, both CPI and Core CPI have had an average average ~0.3m/m in the last year. So the probability of having less than that is low currently, more so in a strong economy.

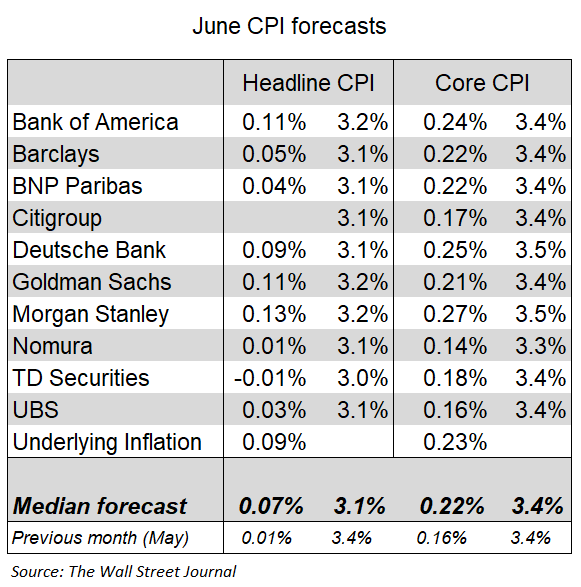

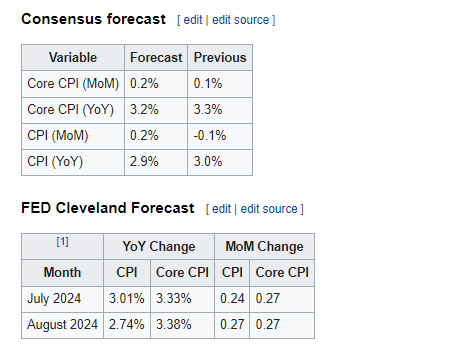

These are April 2024 expectations. Month-over-month increases are still relatively high.

This month’s underlying developments were again more inclined to upside risks, but maybe more mixed as important components such as wages that have been moderating and used car prices declining very significantly.

These are components that could be important for CPI, but I haven’t studied correlations yet to know the real impact between these metrics and CPI, including lags between them

Wages have been having more moderate increases in the last 3 months. The 6M annu rate is running at 3.85% currently, still a bit higher than before covid.

Oil and Gasoline continued to increase in April, both up over 5% m/m. However prices have started to decline in May.

Food Index had the second consecutive month of increases at 0.3% m/m, but still down 7.5% Y/Y.

Housing prices recorded an increase of 0.6% m/m during April, after a few months of declines, at 6.5% Y/Y currently. Rents also increased by 0.5% m/m.

Used car prices continued to decline in April being -2.3% m/m, but new car prices recorded a 2.2% increase during april 2024.

Import prices continued to increase being up 0.6% in March 2024, reverting the deflation experienced during 2023.

Both the ISM manufacturing and services prices paid index continued to accelerate its rate of increase during April. Manufacturing increased 6.1 points to 60.9 (14.5%Y/Y) and services up 5.8 points to 59.2 (-0.6 Y/Y)

US PPI during April was 0.5% m/m, higher than expected, but mostly due to prior down revisions. Still increasing Y/Y at 2.2%.

Small business planning price increases declined 7 points during April, to the lowest in a year.For now, dissipating fears of an acceleration in prices for small businesses.

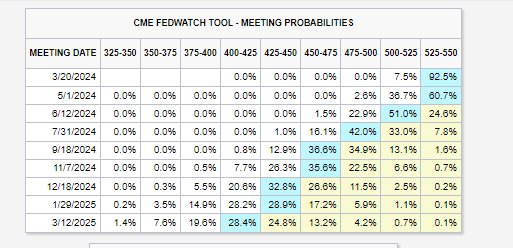

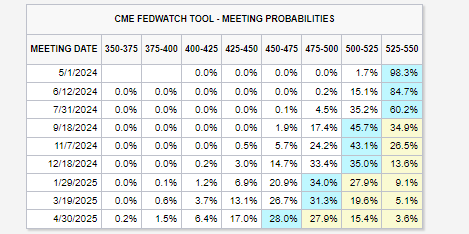

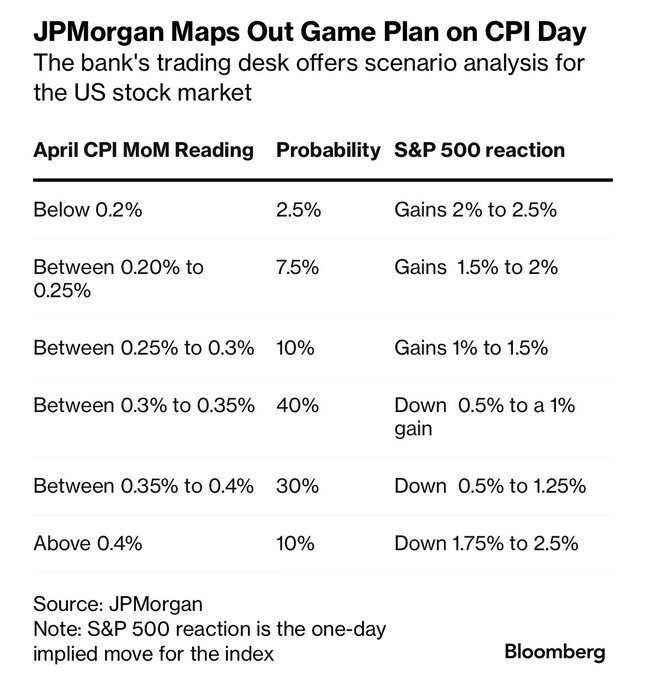

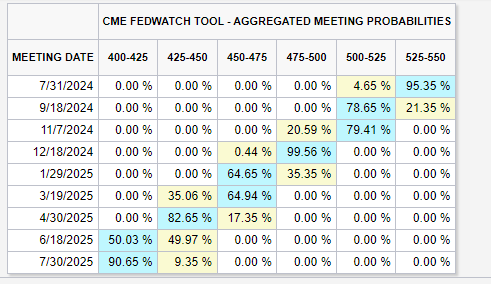

These are JPM probabilities and expected market reaction.

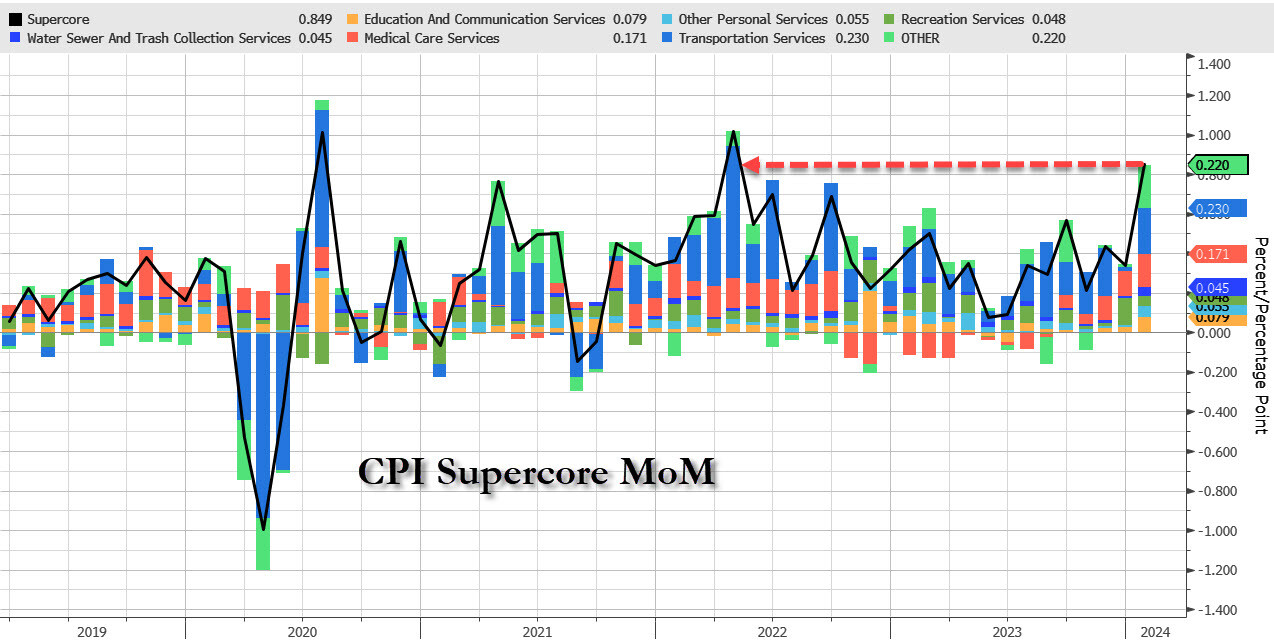

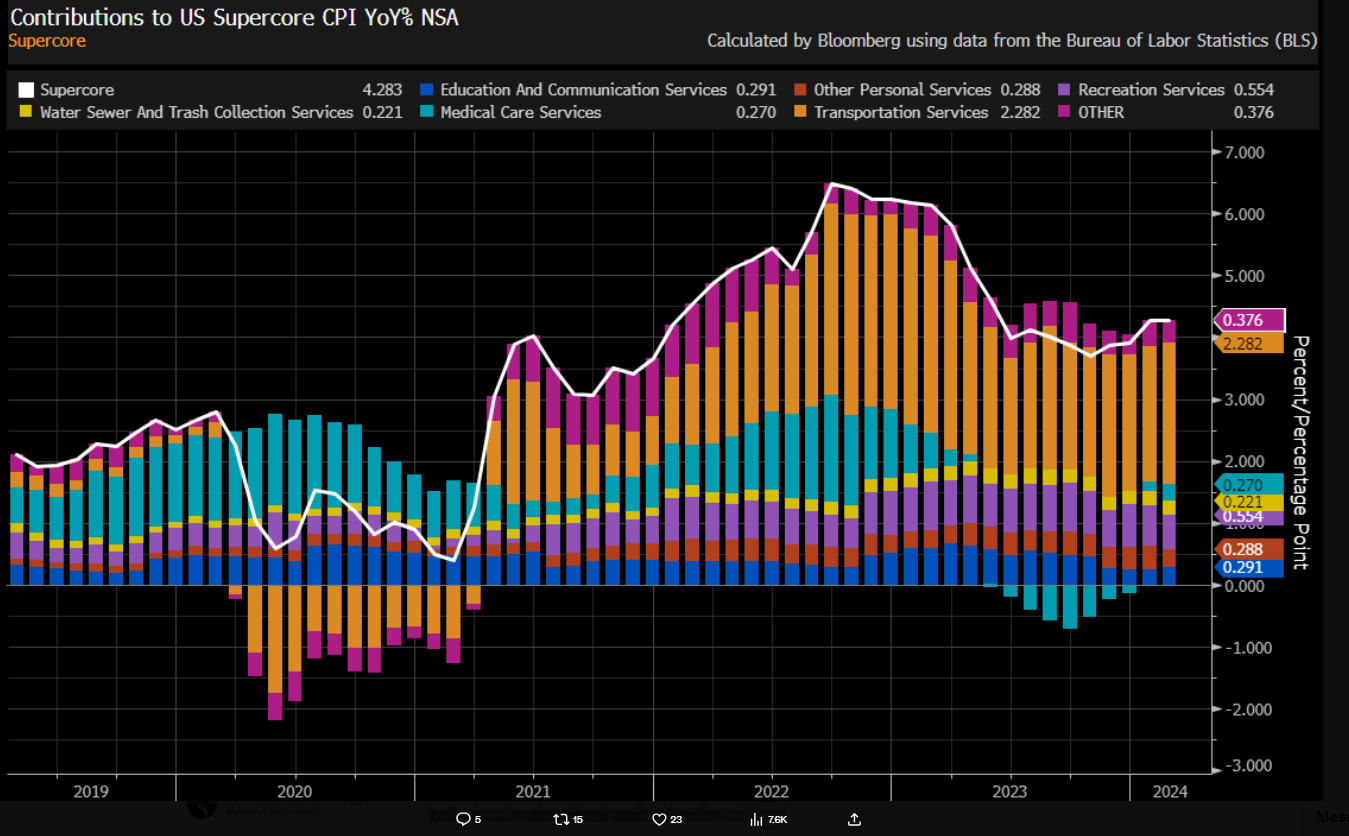

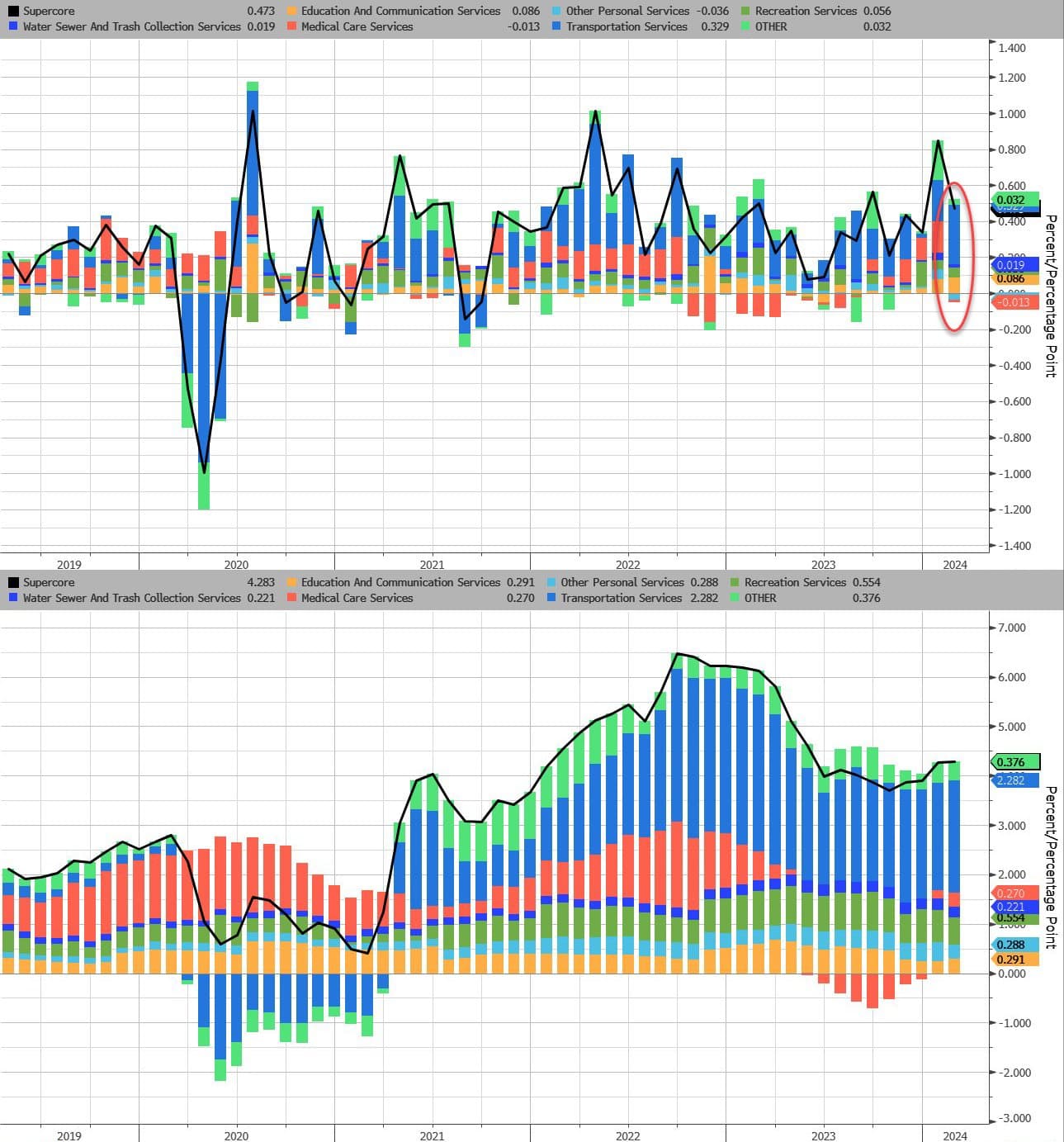

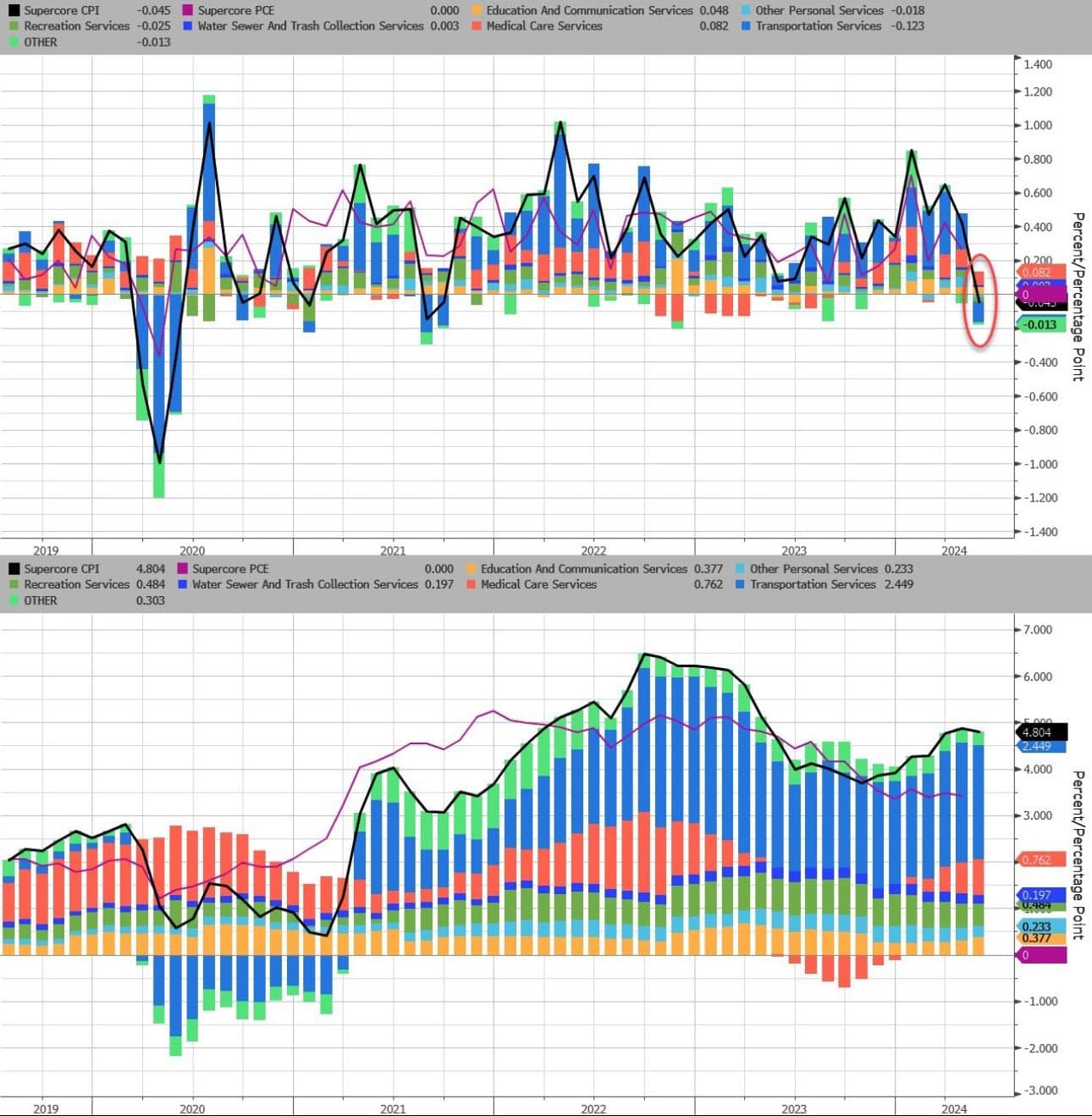

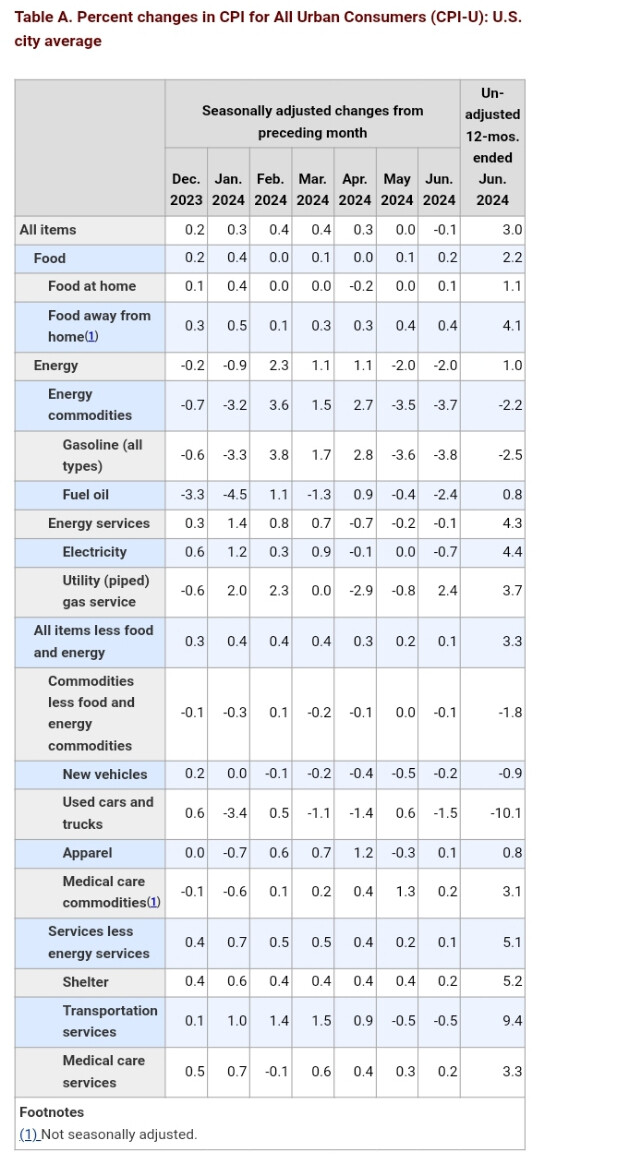

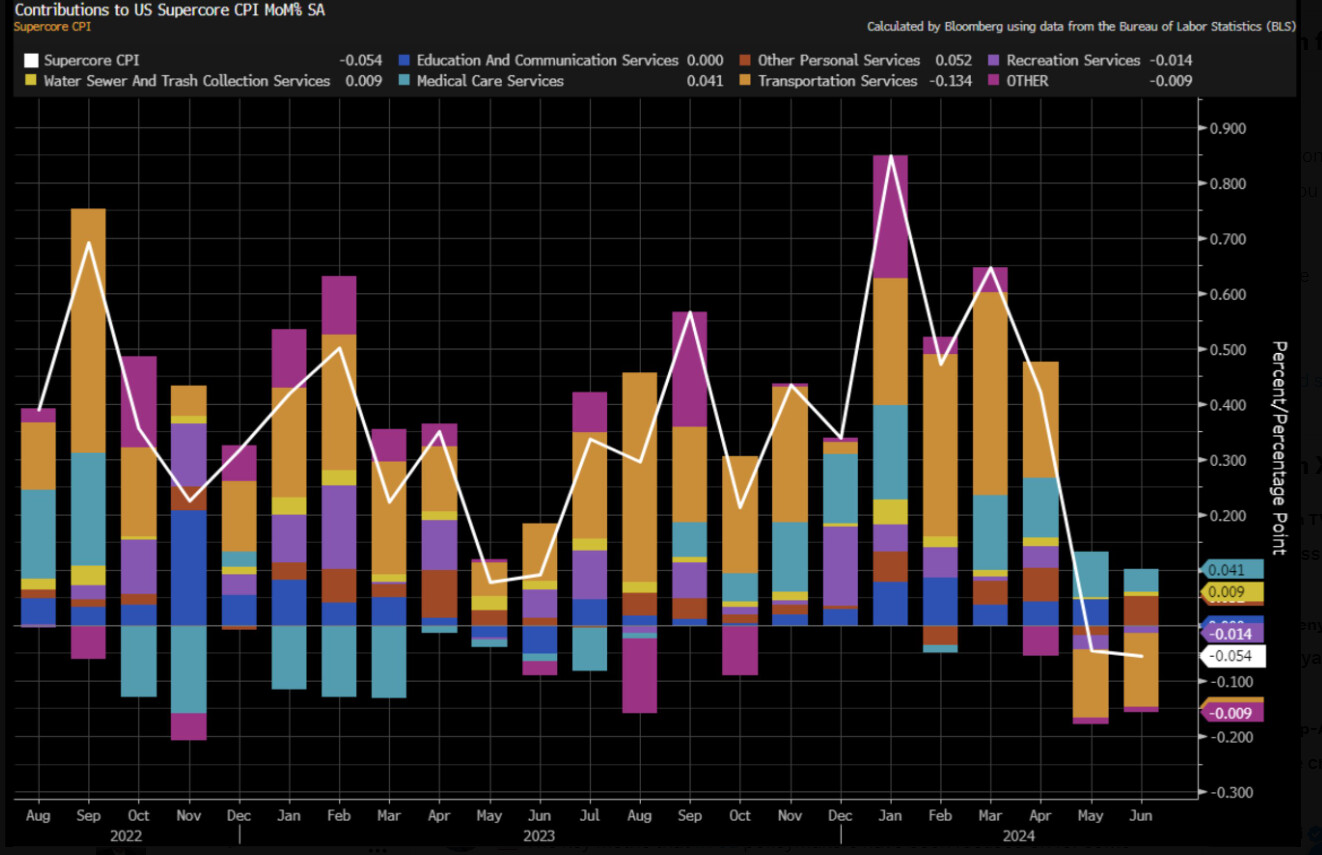

While CPI came in somewhat cooler than expected, there was not much improvement during the month, especially supercore, but a least not additional deterioration either.

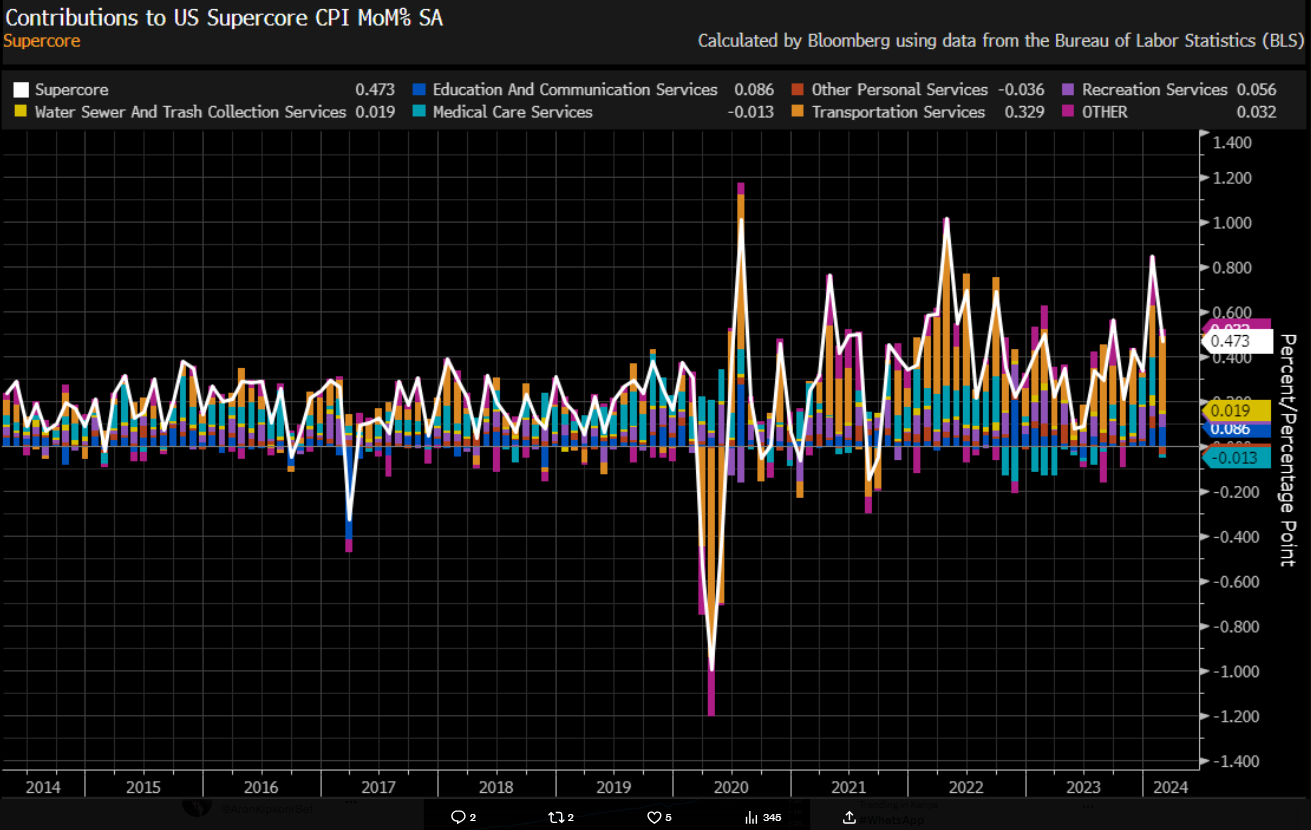

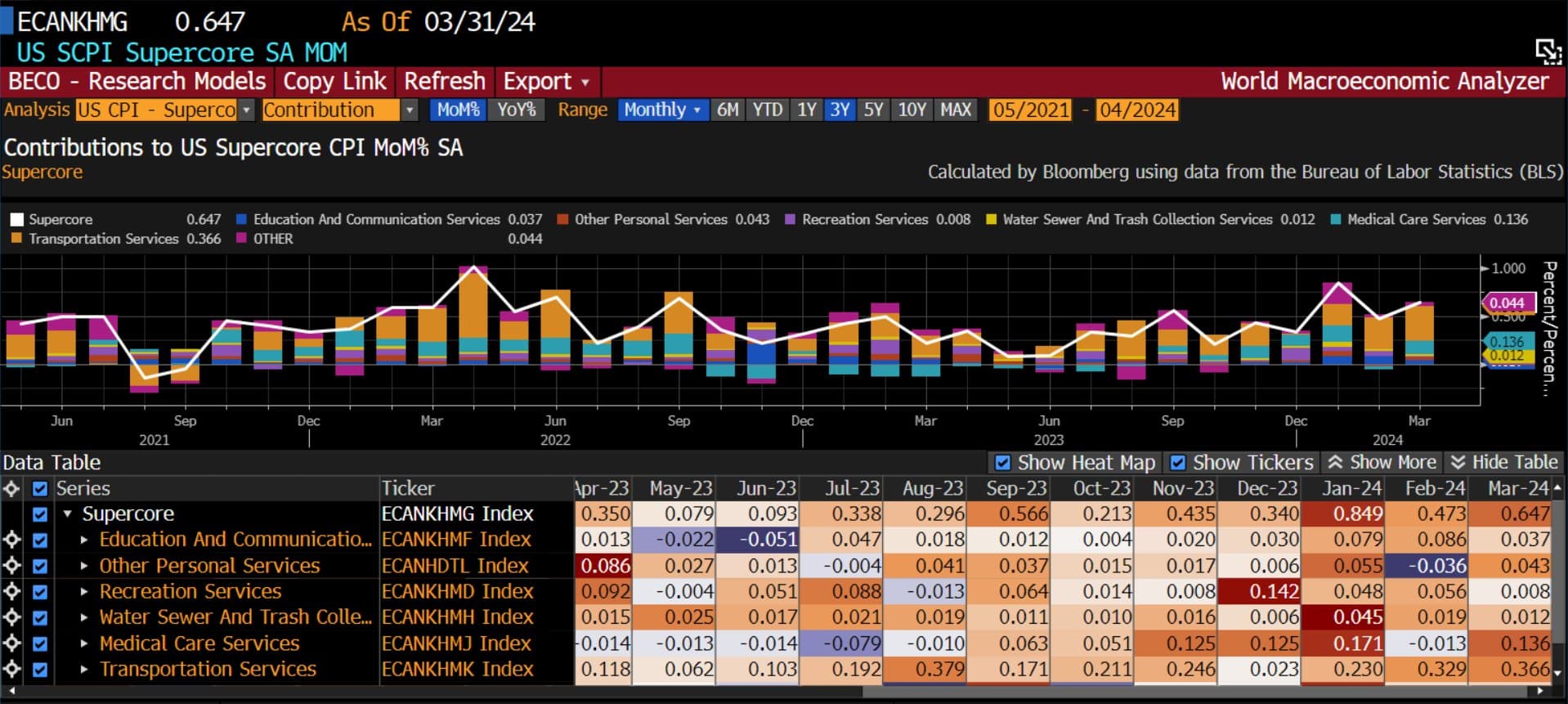

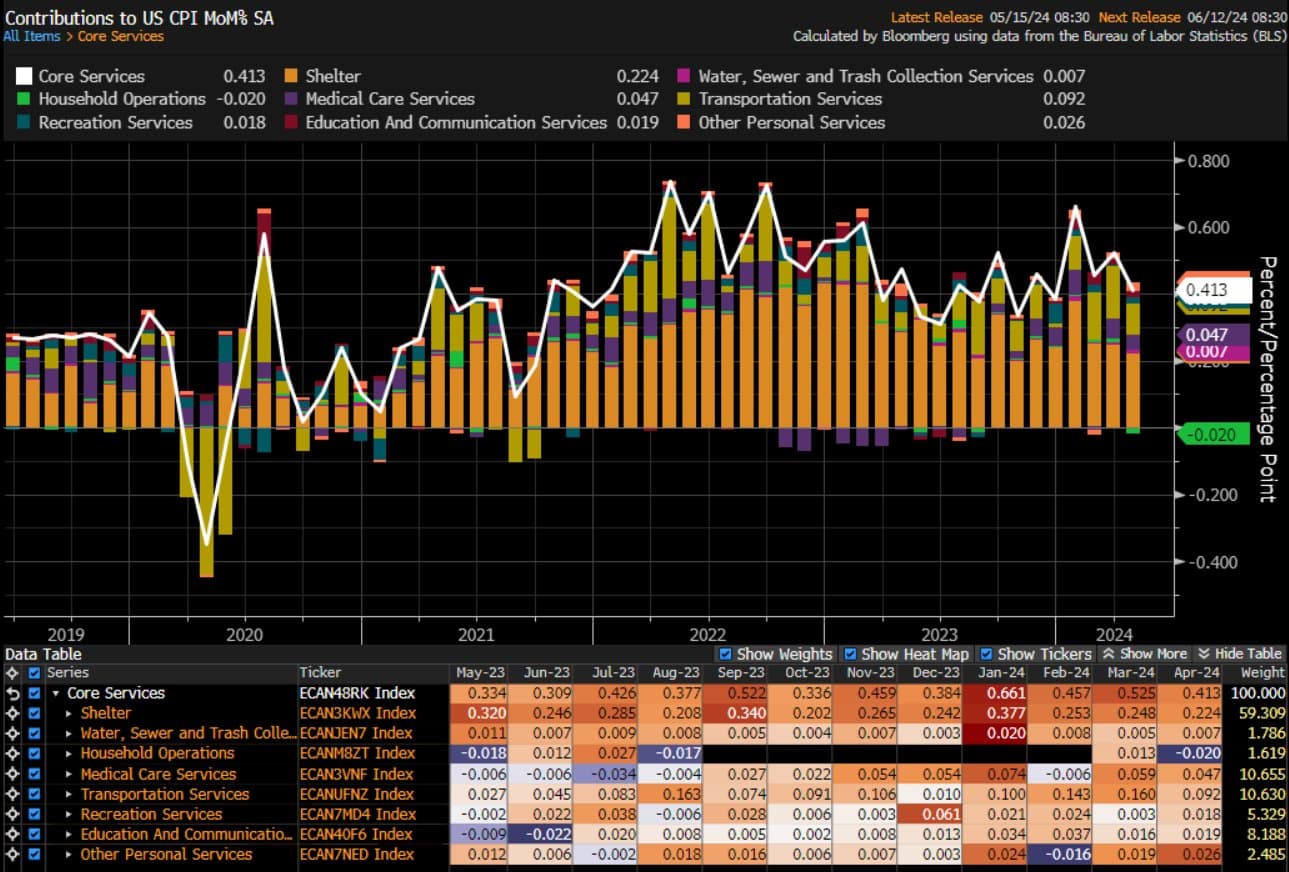

The history continues to be the same, services inflation continues to drive inflation, especially concentrated on shelter 0.4%m/m, transportation 0.85%m/m(vehicle insurance mostly), and medical services 0.45%m/m.

There is no significant improvement shown in any of them, I would expect continued improvement, but probably slowly.

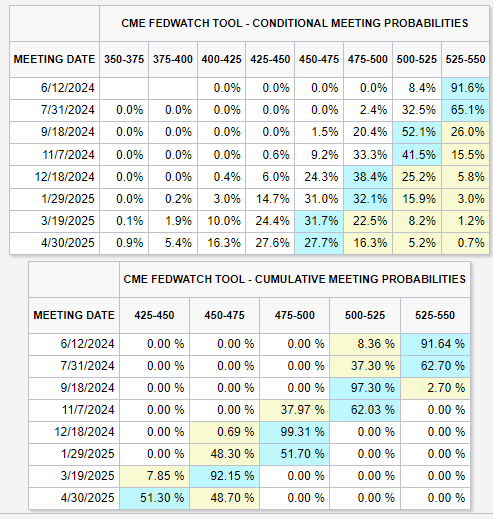

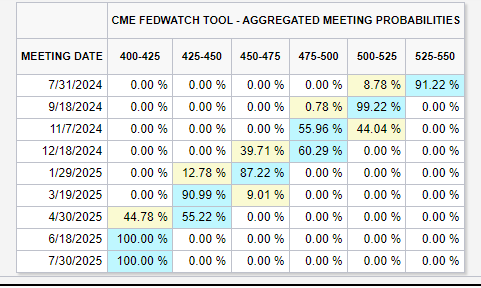

The CPI release, probably in combination with weak retail sales, made the markets more sure about the cuts in September and December.

Is definitely a tricky environment for the FED.

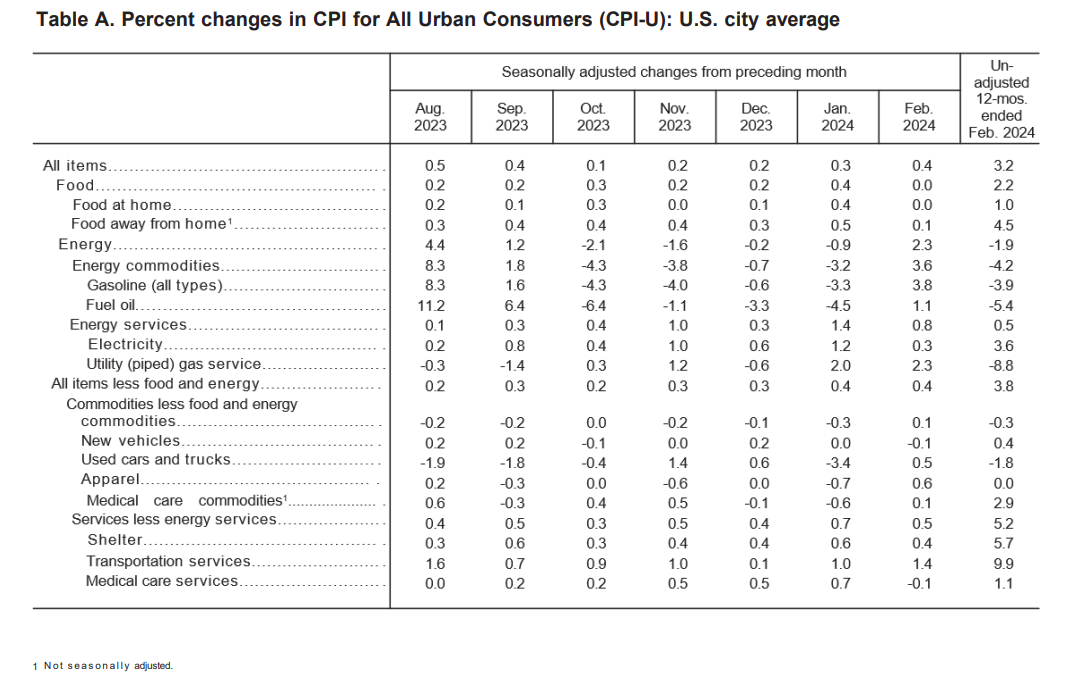

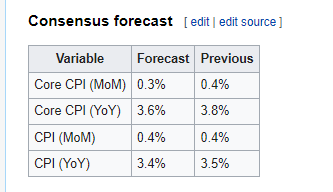

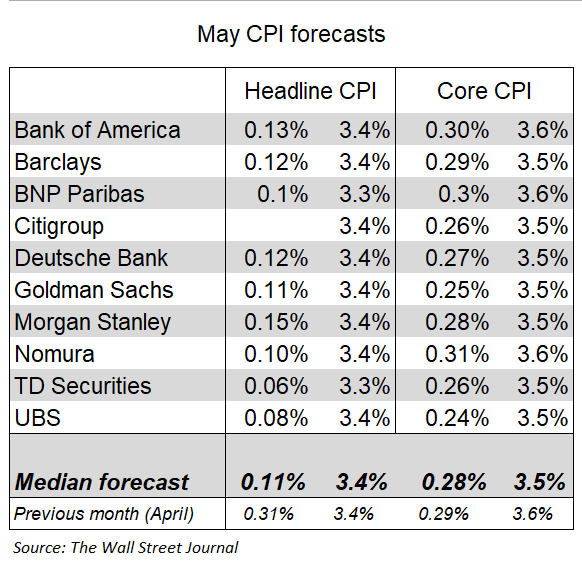

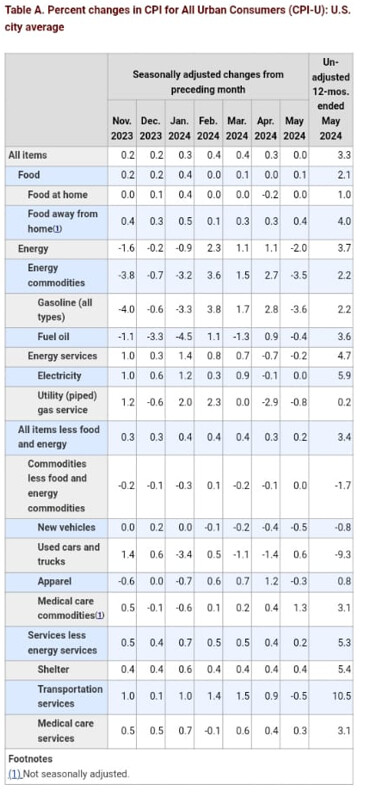

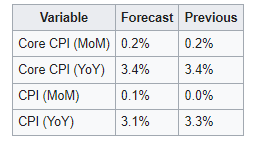

Headline CPI was unchanged in May versus expectations for a 0.1% increase.

On a yearly basis, headline CPI was up 3.3%, lower-than 3.4% estimate.

Core CPI rose 0.2% in May and 3.4% from a year ago, below estimates for a 0.3% and 3.5% increase.

Stock futures were up following the report, Dow Jones Industrial Average rose 0.7% while S&P 500 and Nasdaq 100 futures gained 0.8% and 1.1%, respectively.

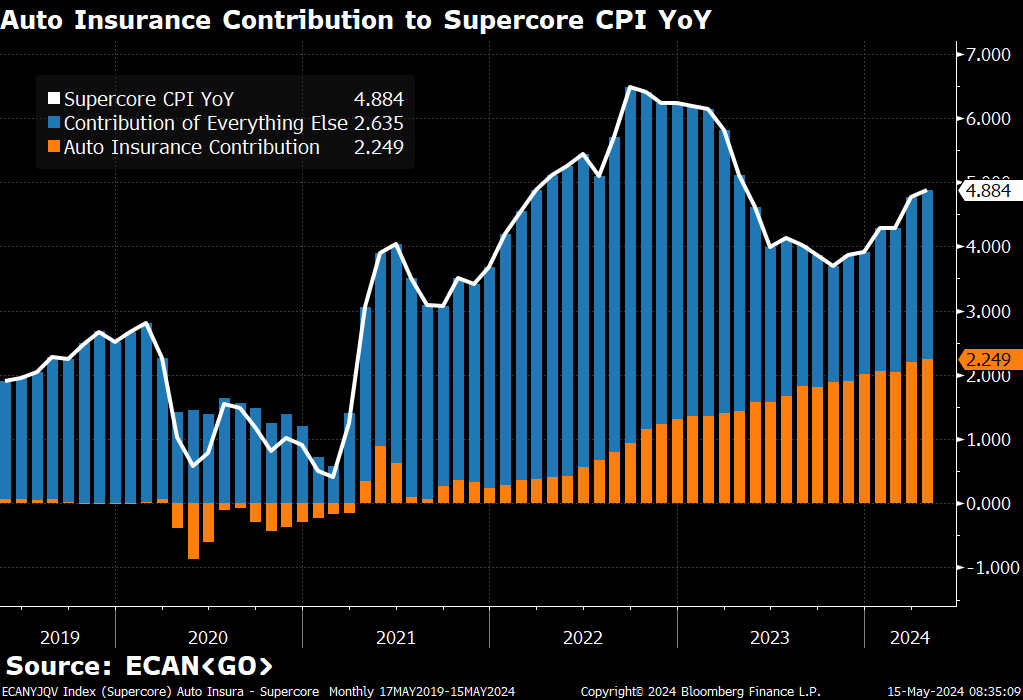

Definitely a dovish report, especially seeing improvement in stubborn components like vehicle insurance.

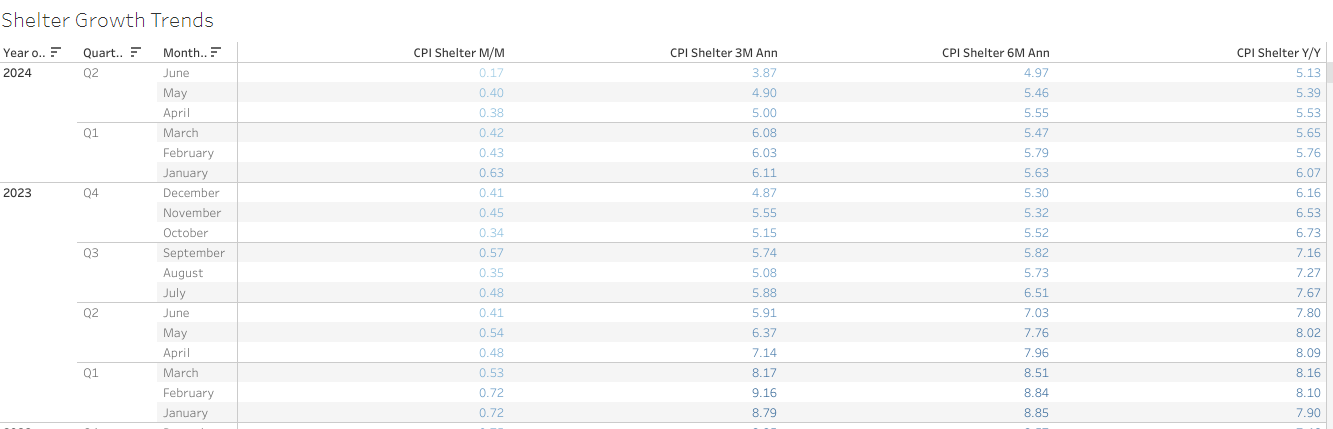

However, shelter is still a problem without much progress.

I would still be cautious to extrapolate much from this report, since is only 1 month of good data after a few months of upside surprises, hence additional data is going to be needed. However, is still a welcome sign.

Also, the fact that very rapid disinflation could mean a softening of the economy or a nearer recession.

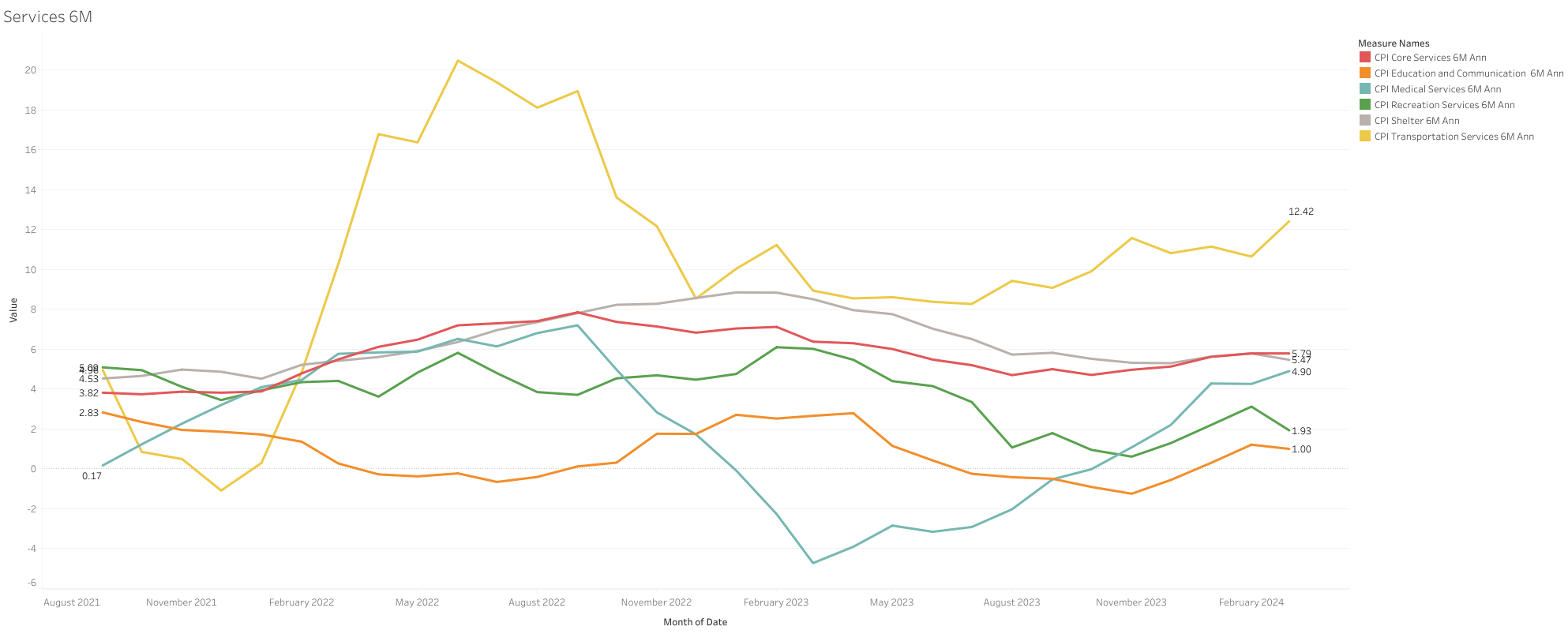

Super core in actual deflation for the month, especially due to the vehicle insurance going from 1.8% m/m in April to -0.1% in May.

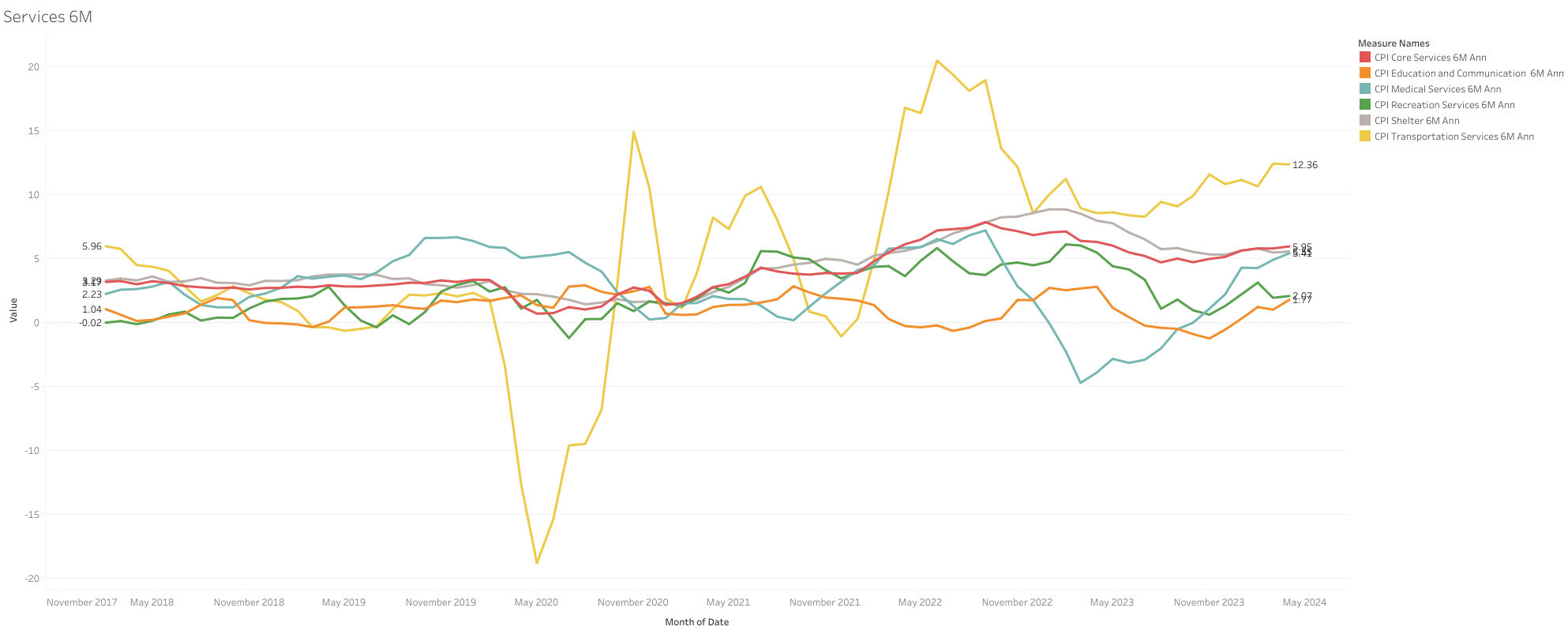

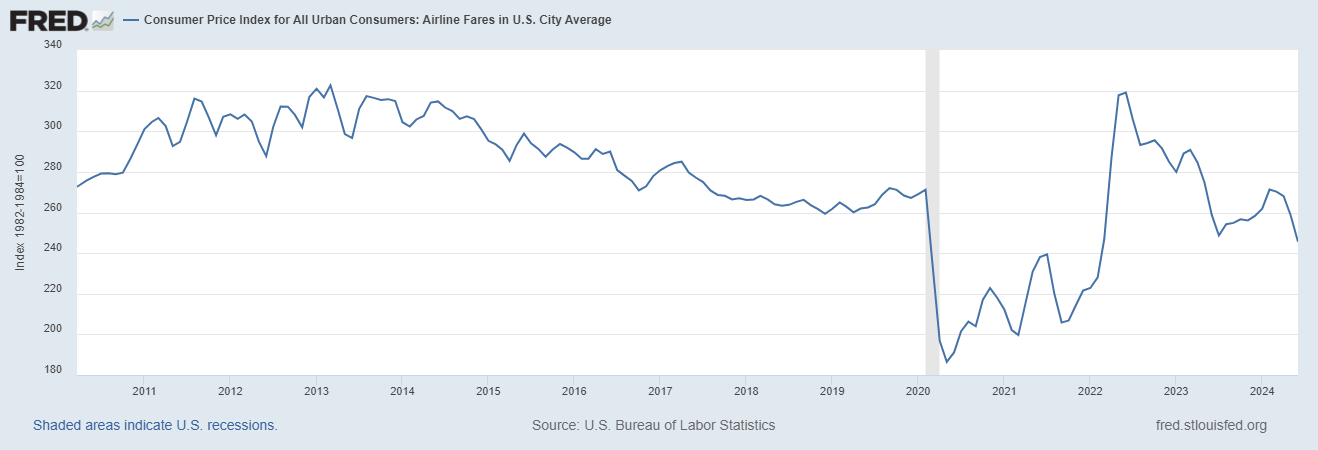

A welcomed improvement in transportation services CPI 6M annualized rate, especially due to vehicle insurance -0.1m/m, and with less weight airfares -3.61% m/m

Some insights during the month, most of them lower readings than in May:

Wages were on line with estimates in June, with a 0.3 m/m increase (vs 04% in May), in line with the average increase of the past few quarters.

Gasoline had a decline of -4.12% m/m (vs -0.23 in May), while oil had an increase of 3.2% m/m (-6.12% in May). However, gasoline has a higher weight in CPI (3.6 vs 0.08)

Food index was unchanged during the month (vs 0.9% in May)

Housing prices increased 1.17% m/m during April (1.30% in March), reaching 6.29% Y/Y. Rents in june increased by 0.4% m/m (vs 0.5% in May), down 0.7% y/y.

Used car prices continued to decline in June being down -0.6% m/m equal to May, while new car average transaction prices increased ~0.5% m/m (unchanged in May).

Import prices had a decline of 0.6% m/m in June 2024, and are still slightly up now 1% y/y

Producer price index fell 0.2% in May versus growth of 0.5% in April and against expectations for a 0.1% increase

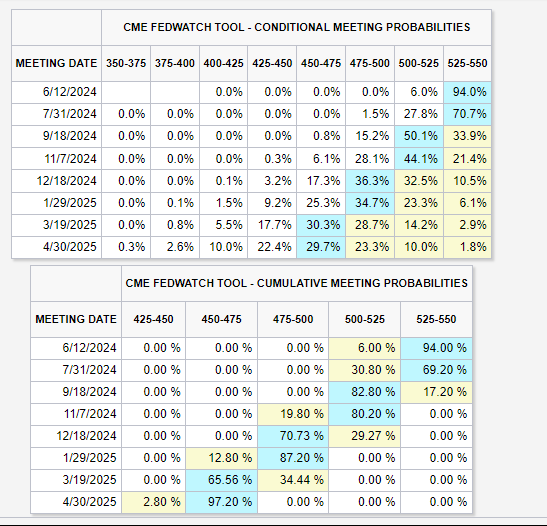

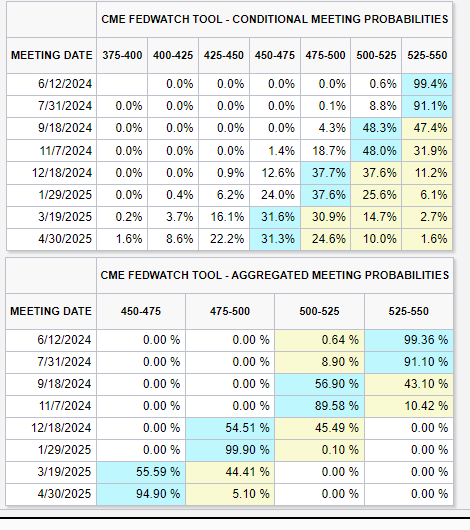

The market is still expecting with higher confidence 2 rate cuts in 2024, despite the FED projections for only 1 cut.

I think money rotating out of tech with those positive developments into the Russel makes sense as capital intense and leveraged companies in it could profit most from a rate cut?

Yes, it makes sense, Russell companies are the ones with more debt and with a large percentage unprofitable (~40%)

I also heard there is a lot of short covering on the Rusell today that helped with the big move.

The probability of a rate cut in September jumped to almost 100%, and now expecting the other 1 in November (not sure the FED would cut close to the election, thought)

However, I still don’t know what 25bps cuts are going to do to help the economy that seems to be cooling faster or these companies, but I still think based on recent data they should start soon if they don’t want to be extremely late or make a mistake.

Rapid falling inflation could also be a signal of a cooling economy.

Shelter is not down, it still increased by 0.2%, but the rate of increase has cooled, from 0.5% monthly increase on average in Q1 2024 to 0.31% in Q2 2024.

All growth trends got better during the quarter too.

Transportation has been one of the big contributors to supercore negative readings, this mostly due to airline fares falling.

Vehicle insurance had a 0.9% m/m increase again.

Another soft report is expected for July 2024, above June numbers on a m/m basis, but the Y/Y trend is expected to continue to decline.

Given the current economic slowdown, it’s likely that inflationary pressures will continue to ease in the coming months. Unless there are any new disruptions to the supply chain or energy markets.

Used car prices increased 2.8% m/m in July (-4.8% Y/Y), while new car average transaction prices remained mostly unchanged during the month and -0.2 Y/Y (final numbers not available yet).

Import prices remained unchanged during June and 1.58% Y/Y.

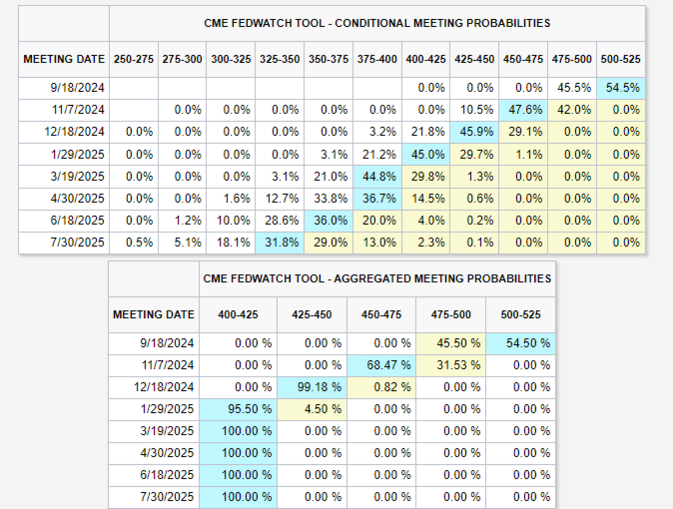

The market is currently pricing 100 bps of cuts in 2024.

For September, the market remains undecided between a 25 basis point cut or a 50 basis point cut, with 25bps having a slight higher probability.