@Aron Following our conversation on Volkswagen deliveries, I think it would be great if you could create a post outlining all your key assumptions for the model.

This way, both I and other community members can review, challenge, and provide feedback where appropriate.

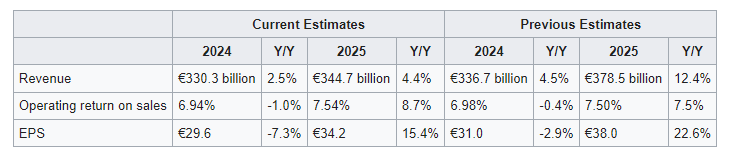

Following further research on Volkswagen’s products, especially the 2024 launches and @Magaly’s recent insights on industry estimates and macro conditions, I have adjusted my estimates for 2024 and 2025 in the valuation model.

S&P Global Mobility forecast unit sales of light vehicles to grow by 1-3% in 2024 and 2-4% in 2025.

Demand and supply of vehicles have come into better balance.

Sales of medium and heavy-duty trucks are expected to contract in Europe and North America in 2024. A pick up in sales is expected in 2025 due to greenhouse regulations that take effect from 2026.

Unit sales:

Though Porsche’s 2024 models look great, I expect a slight decline in unit sales in 2024 due to the transition from the old models to the new ones (as it has been the case). The changes in 2024 should lead to a positive unit sales growth in 2025.

I still expect Audi unit sales in 2025 to benefit from weak comparison period (due to supply issues affecting V6 and V8 engines in 2024). However, the product changes in 2024 appear too minor for models that are considered dated. Also, the highly anticipated models, Audi Q6 e-tron and Audi A6 e-tron are pricier than its main rivals at a time when residual value of EVs is declining. Hence, I significantly lowered the 2025 deliveries estimates for Audi models.

I don’t expect model changes at Volkswagen Brand Group Core to lead to significant sales since only few model launches (such as Passat, Golf and Skoda models) look impressive.

Pricing:

Almost all the 2024 Volkswagen Group model launches come with a higher price compared to their predecessors.

New vehicle prices is expected to remain elevated in 2024 and 2025. I expect price growth for VW models in 2025 to be mild though since most price changes will occur in 2024.

Used car prices are expected to decline further in 2024 in U.S and Europe. This will impact the operating result of Volkswagen Financial Services. However, the brand expects to compensate for this through higher business volumes and contracts. I don’t have a good understanding of this brand though.

Competition:

Though Volkswagen plans to increase its market share in China to 15% by 2030 from 14.5% in 2023, I don’t expect its current strategy in the country to boost its sales over the short-term. As search, I project that the share of its operating result in China will continue to suffer due to rising competition.

Volkswagen Group is competitive in Europe, hence I expect its market share in the region to be stable over the short-term.

I expect Volkswagen’s market share in North America to stay stable over the short-term, especially now that U.S has imposed 100% tariffs on China EV imports.

Costs:

The product launches in 2024 will likely lead to higher costs in 2024 than in 2023.

The cost-savings programs implemented last year at the Brand Group Core will likely boost its results in 2024 and 2025 since they are already paying off.

The above 2025 estimates doesn’t consider that a recession will occur in 2025. If there will be a recession, I forecast revenue in 2025 to decline by 11% to €291.2 billion, operating return on sales of 1.6% and EPS to come in at €2. These estimates are mainly based on the company’s performance in the 2009 recession.

Good format of comparing previous and current estimates in a clear overview when making updates to the valuation model.

What are your confidence levels when it comes to your key assumptions? Which of them are you more or less certain of?

What are risk factors where you could see things going wrong and what are potential tailwinds to this base case scenario?

When it comes to a potentially recession I think it is quite unlikely that we will get a global 2009 style recession based on informations as of today. (@Magaly please link to a relevant topic where this could be discussed if you think I am wrong)

In my opinion the question should not be if there is going to be a technical recession or not but how deep a recession is going to be and how much it will affect different industries in different parts of this world. This is going to be the most important factor for companies in this industry and helps us to understand how bad things could get.

Europe and U.S competition (70% confidence level): I am confident that Volkswagen can maintain its market share in Europe and U.S over the short-term. I don’t expect any noticeable gain in market share in the two regions in 2024 and 2025.

Costs at brand group core (75% confidence level): Based on the trends seen in 2023 and Q1 2024, I am more certain that the brand group core would continue reigning in on costs. However, I don’t expect any significant cost tailwinds in 2025 since most of it will likely come in 2024.

Costs at Audi and Porsche in 2024 (55% and 65% confidence level, respectively): I think it makes sense to project that costs at Audi and Porsche will rise significantly in 2024 due to the model launches. However, my confidence level on Audi’s costs is lower than that of Porsche due to the supply chain issues that Audi V6 and V7 models encountered in the first-half of 2024.

Pent-up demand (60% confidence level): I agree with @Magaly that there’s little pent-up demand left. Volkswagen’s order backlog in the passenger cars segment was down 16% y/y in 2023.

China competition: I am 60% confident that Volkswagen will continue losing market share in China until 2026. I don’t currently see any tailwinds that could lead to outperformance in the region.

I am less certain on the following:

Overall pricing in 2025 (28% confidence level): In 2025, the first cheap EVs are expected to arrive in the market. This would possibly impact pricing for ICEs. Also, pricing projections in 2025 especially in Europe aren’t clear. Additionally, worsening macro conditions could lead to discounts. That said, further research by @Magaly on pricing in 2025 would help. Also, I think it would be good to map out all the cheap EVs (less than 30,000 euros) that will come in 2025 and 2026.

Overall unit sales in 2025 (30% confidence level): Volkswagen’s unit sales in 2025 could be impacted by a number of factors such as macro, EU CO2 regulation, and the shift to EVs. The EU CO2 regulation is expected to drive up costs of producing light vehicles. Given that Volkswagen is far behind in meeting the 2025 CO2 regulation, costs could increase significantly. Hence the company may choose to phase out the less profitable models leading to a decline in sales.

Porsche’s unit sales in 2024 (47% confidence level): The main assumption in my Porsche’s unit sales projections in 2024 is that it will likely be affected by the transition from one generation to the next. However, as noted above, Porsche’s upcoming models look great and the headwinds from transition as seen in Q1 and deliveries of Cayenne in 2023 may not repeat itself in the coming quarters leading to higher sale units than projected. My projection also assumes that Porsche could offset its declining sales in China by increasing sales in other regions such as the United States. If it fails to do that (eg by failing to get license for new models in time), the projected unit sales in 2024 could be lower.

Audi and Porsche pricing in 2024 (40% confidence level): Most upcoming Audi and Porsche facelifts don’t have a confirmed launch date. We only know that they will arrive in 2024. If they arrive at the end of the year, it means that pricing in the first quarters of 2025 could benefit from weak comparison period and that my projected 2024 pricing could be lower.

2024 pricing at the brand group core (45% confidence level): The increased pricing for brand group core 2024 launches may lead to reduced sales since only few of them have seen significant changes. Given the company is currently chasing value over volume, we can expect limited discounts.

Industry growth rates (45% confidence level): As mentioned in my other post, the industry growth rates are less certain. I think the estimates are adjusted as data come in. @Magaly will look into correlation between Volkswagen unit sales and industry growth rates.

Performance at Volkswagen Financial Services (30%): Though I am almost certain that used car prices will decline throughout 2024, I don’t understand the business’s other drivers of revenue. Tailwind could arise from this business since the brand’s guidance for operating result exceeds my projection.

Alright, thank you for the insights.

I think it is always good to develop an action plan of all tasks, priorities, timelines etc. in smartsheets of how we plan to progress in our understanding of a certain topic/company and where we want to invest research first.

The goal of this research could either be to increase confidence levels in our predictions (on areas in which this is possible) or research new areas that we did not cover before.

I would be personally pretty interested in insights into CO2 regulations given the EU’s aggressive targets, what those could mean financially for Volkswagen, and whether the EU might ease its regulatory stance given that mainstream adoption of EVs is progressing slower than hoped.

One important qualitative factor which I usually try to factor into my predictions of how a company will perform is the trust I have into the management and the ability of the company as a whole to perform against their goals.

In that light, I agree that the efficiency gains of the brand core group look promising and I overall have some level trust in the management of Volkswagen (7/8 out of 10) even though the organization is certainly slower and less agile as a smaller competitor like Tesla. (Maybe 4/5 out of 10)

When it comes to the upgrade cycle i would be interested in more context. How large and important is the cycle compared to previous upgrade cycles? That would make it easier for me to even better understand it’s significance. (Insights/Context could be organized under Volkswagen deliveries and in the Wiki under Volkswagen Product)

Finally i would be very interested in risk factors, tailwinds and scenarios.

Which key factors could cause results to differ materially?

As an example how large would be the impact on numbers in adverse scenarios when it comes to pricing?

I think it would be interesting to calculate a few scenarios that are possible in the Volkswagen sheet maybe in a new tab. This could give us an impression how large impacts could be in case things are developing differently from how we are expecting them to develop.

I would also be quite interested in insights or challenges from others e.g @Magaly on what we might miss or how certain components might develop.

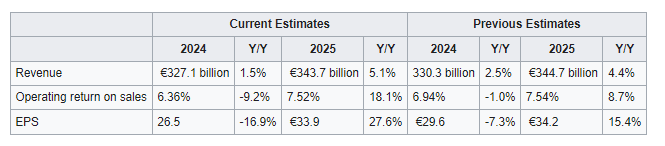

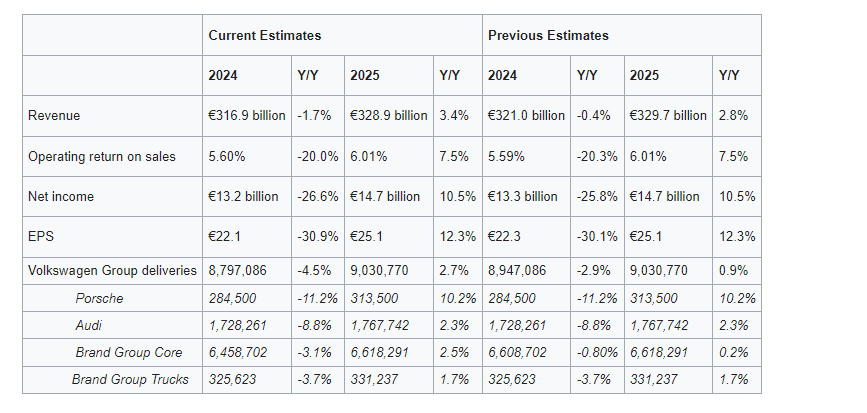

Following my update on deliveries projections and a charge of 1.7 billion euros due to the restructuring of Brussels plant, I have adjusted my previous estimates as follows;

Management is guiding revenue of €338.4 billion (+5% y/y) and operating return on sales in the range of 6.5% to 7.0% (lowered from 7.0% to 7.5% due to Brussels plant restructuring).

I am currently looking into the EU CO2 regulation which could have an impact on the 2025 operating results. As such, further update on the 2025 projections will come soon.

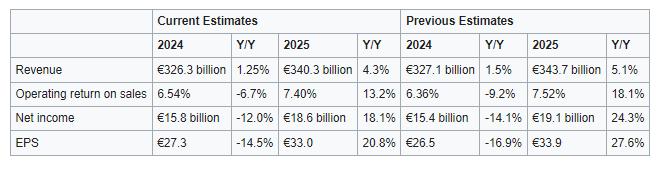

I have updated my Volkswagen’s earnings estimates for 2024 and 2025 as follows:

The update takes into account the following;

My improved confidence in the ability for Audi to deliver better performance in H2 following its stabilized earnings in Q2.

Lowered 2024 guidance at Porsche due to supply chain issues.

My forecast that the Cyber security law could lead to an headwind of 65,000 units in 2024.

Pricing pressures as observed in United States and as signaled at Mercedes-Benz and Renault in Q2. This is likely to be witnessed at the Volkswagen Brand Group Core only (given economic brands are more sensitive to price increases compared to luxury brands and Traton saw better pricing in Q2). Also, Porsche and Audi results suggest growth in pricing in Q2. Accordingly, I have slightly adjusted pricing estimates for the Brand Group Core and Traton.

Around 500 million euros headwind on operating profit in 2025 as a result of failure to meet the EU emissions target.

Awesome. I love updates to models.

Not sure if this should be a standard but maybe it makes sense to include the impact on revenue and net income that each of those changes has? (And add net income as a line to the table - as it is universally comparable and highlights the dimensions of profitability to people)

Maybe we can add the impacts in future estimates. For now, my estimated calculations are too complex to pinpoint how each one affected the revenue or net income.

Ok sounds good. You could simply record the starting points of revenue and net income before you make one change e.g. expectations for Audi performance and then see how much revenue and net income changed after you made this one single change and note down the difference. If you do that before and after each change you can highlight to the readers which of the changes to the valuation model that you made are the most significant by showing the impacts in terms of numbers for all changes.

Example:

My improved confidence in the ability for Audi to deliver better performance in H2 following its stabilized earnings in Q2. (Revenue +500 million, Income +200 million)

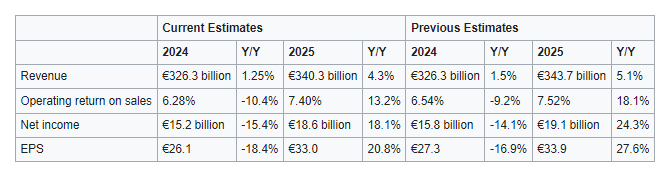

Following Handelsblatt’s report that Brand Group Core could miss its 2024 cost-cut target (4 billion euros) by 2-3 billion euros, I have lowered my estimates for Volkswagen Group’s 2024 operating return on sales to 6.28% from 6.54%. The changes are as a result of reduction in Brand Core’s 2024 operating result before special items by 840 million euros.

N/B: Volkswagen expects a range to the lower end of the guided 6.5% to 7%.

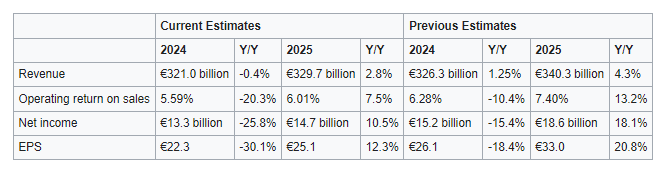

Following recent management update on the 2024 guidance, new restructuring measures, and rising competition coupled with the 2025 CO2 regulation, I have lowered my estimates for 2024 and 2025 as shown in the table above. I believe that until we are more confident on how demand and pricing will develop next year, it’s best to have conservative estimates. At the moment, I believe that prices in 2025 will be lower than in 2024 due to the CO2 regulation and rising competition. Automakers will likely try to sell more EVs next year so as to meet the CO2 targets. Additionally, before the regulation enter into force in July 2025, automakers will likely attempt to sell as many ICEs as possible. These actions will probably drive down prices.

Here are the changes in the valuation model;

I slightly lowered my 2024 pricing estimates for the Brand Group Core leading to a revenue headwind of 4 billion euros.

I slightly lowered my 2024 pricing estimate for Audi leading to a revenue headwind of 500 million euros.

I lowered my 2024 pricing estimate for Traton leading to a revenue headwind of 650 million euros.

I reduced the 2024 operating result estimate for Volkswagen Financial Services by 900 million euros.

I lowered the Brand Group Core’s 2024 operating result estimate by 1.6 billion euros.

I also lowered the 2025 pricing estimate for Brand Group Core leading to a revenue headwind of 9 billion euros.

I lowered my 2025 pricing estimate for Audi leading to a revenue headwind of 1.2 billion euros.

I lowered my 2025 pricing estimate for Traton leading to a revenue headwind of around 700 million euros.

I considered 4 billion euros restructuring costs in 2025 at the Brand Group Core.

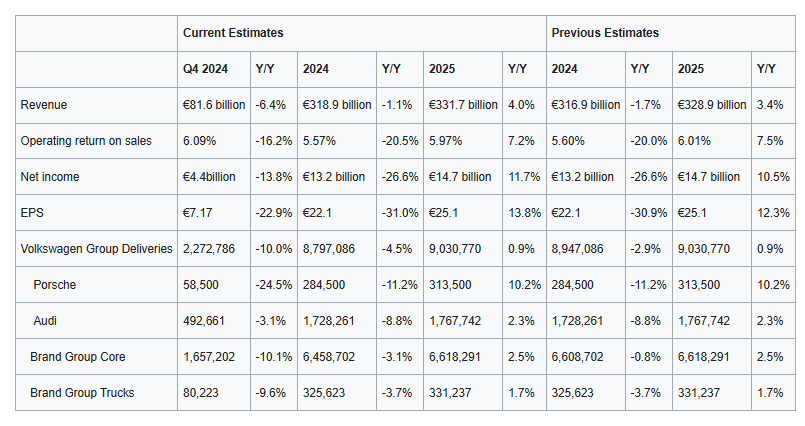

Following resilience in average revenue per unit at the brand group core in Q3, reduced expectations at Audi and underperformance in pricing at Brand Group Trucks during the quarter, I have updated my forecasts as follows:

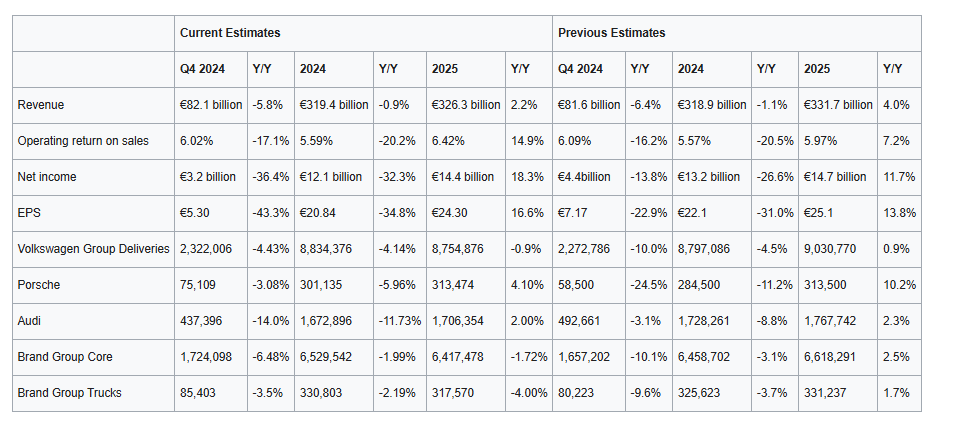

Following my update on deliveries projections, I have adjusted the valuation model forecasts as shown in the table below. The new projections also consider the recently announced cost-cut measures at the Volkswagen brand. While it’s unclear what they refer by the “medium term”, there are reports signaling that most of the cost benefit will come from 2027. As such, my 2025 projections only consider cost-savings of only 500 million euros (guestimate).