August CPI is expected to come a bit hot, with a 0.6% m/m increase, 3.6 y/y from 3.2% in July.

Core CPI is more modest at 0.2%, 4.3 y/y (4.7% July)

This was expected as higher gasoline prices were (expected to hit in August. All energy prices saw an increase during August.

I don’t think these results will change the results from the September meeting of a pause, but if energy prices remain high, maybe could change the November decision for an additional hike.

Other important developments were: wages remaining sticky, housing prices continuing higher and car prices seeing a rebound higher in August.

This is not the best report overall, but keeping in mind that shelter CPI is still at 7.3%, while measures of home prices or rents are already at negative or close to zero y/y, so an additional moderation in shelter is expected due tot the lags, weighing on core CPI going forward.

Energy prices continue to increase in September, so its impact is probably not going to stop in August. If sustained higher, it could at some point flow through input prices for other industries

Super core records its biggest increase in 5 months, not a development the fed wants to see.

Much of this increase is transportation CPI, rising 2% in August (motor vehicle insurance 2.4% m/m), but most services remain sticky.

Fed Cleveland forecasting 0.36 m/m for headline and core for September.

September CPI is expected to remain mostly unchanged, with a small decline.

Energy prices had still an increase in September, and this is the first time in months they have been up y/y.

Other important developments were: wages remaining sticky, housing prices continuing higher for 6th consecutive month, and car prices increasing again since August. Not the best developments for the near future.

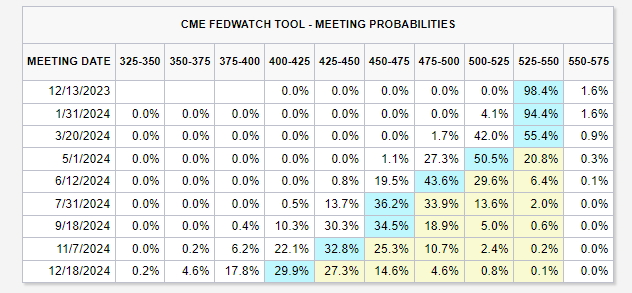

However, due to the significant move higher in treasury yield, I don’t expect the FED to hike again since they can see this as the market doing it for them.

The market is pricing a pause, and rate cuts beginning in 2024.

My first interpretation is that those numbers are positive, given that we are seeing continued services disinflation with shelter hopefully coming down at one point as well.

Interestingly new car prices continued to rise even while the supply situation is improving.

I am not sure I see this report that positive. Services, súper core Services and shelter at 0.6 m/m, is pretty hot

The 3 of them are seeing an acceleration again from pasts months

Hopefully is a 1 month outlier, but the trend in last months is not encouraging

I somehow got this wrong looking at prices of used cars, apparel, medical care commodities, transport services being down or weaker m/m while cpi core stayed at 0.3% and shelter strengthened to 0.6% I thought super core must be down.

What is the reason super core is up? What is the „other“ category in super core?

The other category is probably the remaining all of the other small services, not disaggregated by the BLS, at least not in their release.

They disaggregate some “other personal services”, but there is still some % missing.

When I was working on the weights of CPI, I also realized there is a % (something like 1%) that they don’t disaggregate. But without access to Bloomberg difficult to know how they are getting or calculating this data.

Energy prices had a significant decline in October, this could be the main reason the headline is expected to decline, but core prices to remain unchanged or sticky. We most likely won’t see a significant improvement in services.

Wages while its rate of growth is decreasing, is doing so very slowly, and still way above what we experienced pre-pandemic.

House prices continue to increase, however, rent prices are not showing the same trend, being down for 3 months, so we can most likely continue to expect slow progress on shelter CPI.

Used car prices had a significant decline in October (-2.3%), but due to lags this will no be reflected until later on. This month we could see some of the rebound in prices we saw during august and September.

Food prices continue to decline, and supply chains eased considerably during October, but PPI has been showing an acceleration in the past few months.

PMIs showed price paid still increasing for services at a slower rate, but declining for manufacturing at a slower rate than september

Nice surprise even with a softer m/m supercore and core, but still not moving incredibly fast down. Motor insurance is still out of control, up 19% y/y.

I think data like this we are getting lately will continue to support the positive sentiment in the markets, until if something meaningful bad happens, that stops the mindset that “bad news are good news”

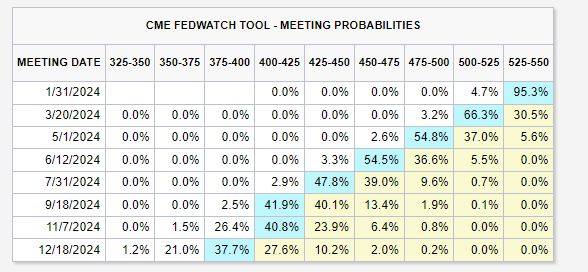

However, I also think markets are getting a bit ahead in pricing 4 rate cuts in 2024 with the first one in may. Powell not only has said they are not even thinking about rate cuts, but they only have 2 in their projections. While their projections usually are very wrong, at least inform us that even with getting to 2.6% core PCE in 2024 and economy good, they don’t plan to do more than 2 cuts.

IMO a greater amount of rate cuts in 2024 will only happen if the economy is not in good shape.

This report did not change much the market pricing.

Personally, I still don’t get their expectations, as inflation is proving to be sticky, especially in services. Supercore has been basically flat since June, and housing is contributing but very slowly.

These are the expectations for the December 2023 CPI released tomorrow.

Nothing huge is expected. Continuing disinflation on core CPI, but very mildly.

I don’t think these results would change much for the FED and the market expectations. Unless we get a big surprise.

Currently, we have to remain mindful of the increase in shipping rates happening due to the danger in the red sea, but they are still far for reaching levels seen in 2022.

CPI is expected to come at 2.9%, down from 3.4% in December. and core is expected to come at 3.7% from 3.9% in December.

This will be mostly supported by auto price declines impacting core goods, energy, and food.

Services, super core, and housing are not expected to have any significant improvements M/M this month.

As Powell mentioned at some point, goods will stop significantly impacting inflation at some point, and more improvement in services will be needed to come to the target.

(

(