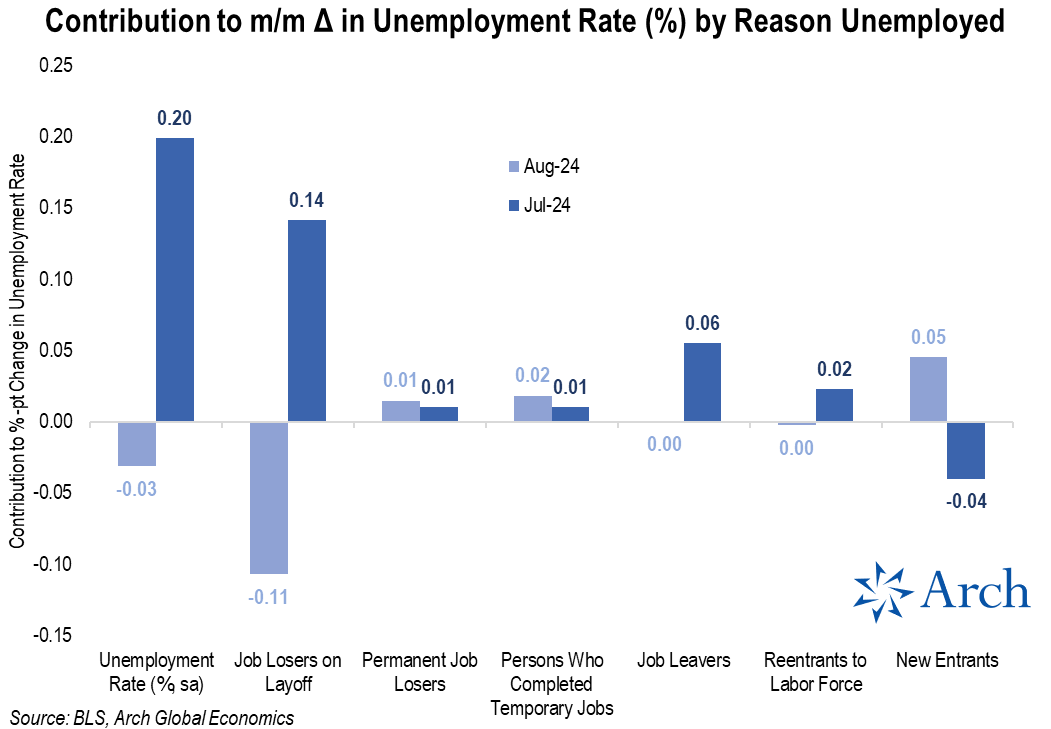

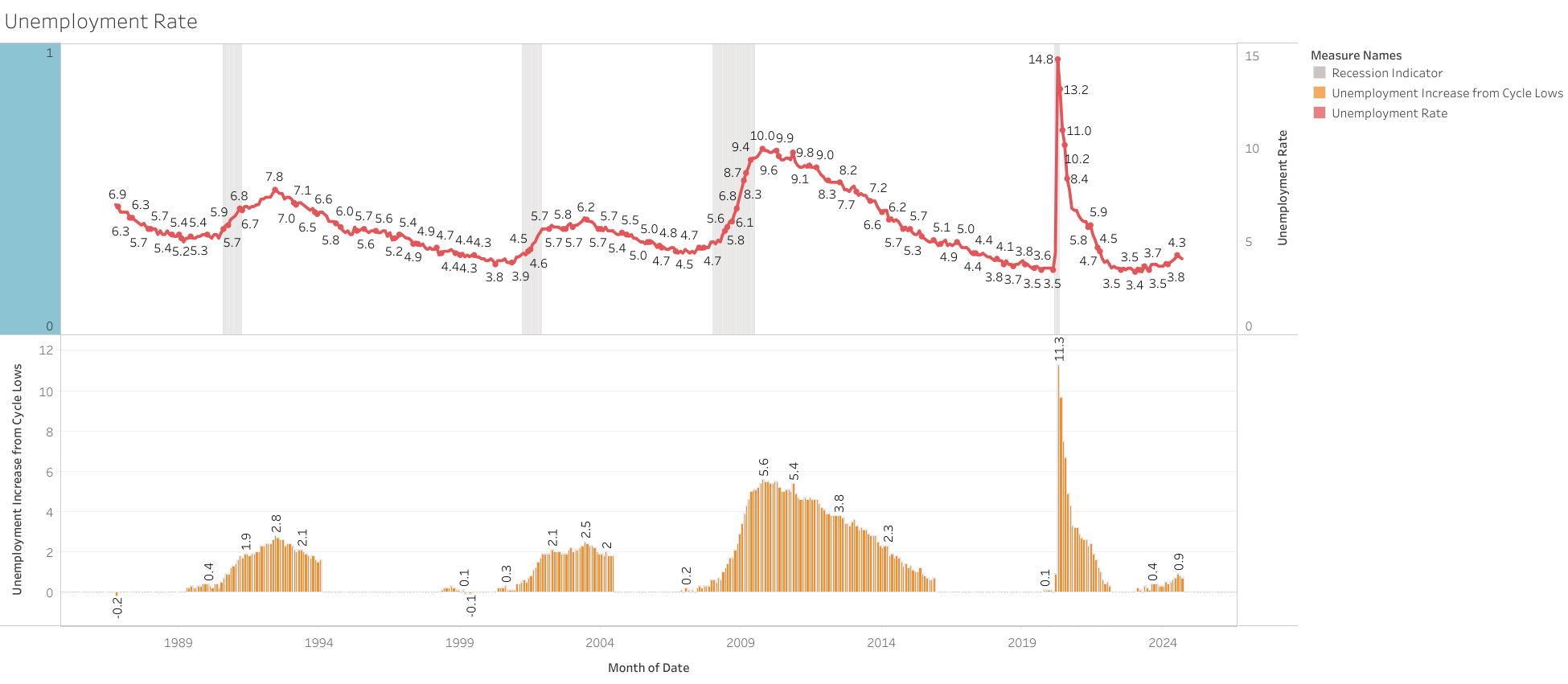

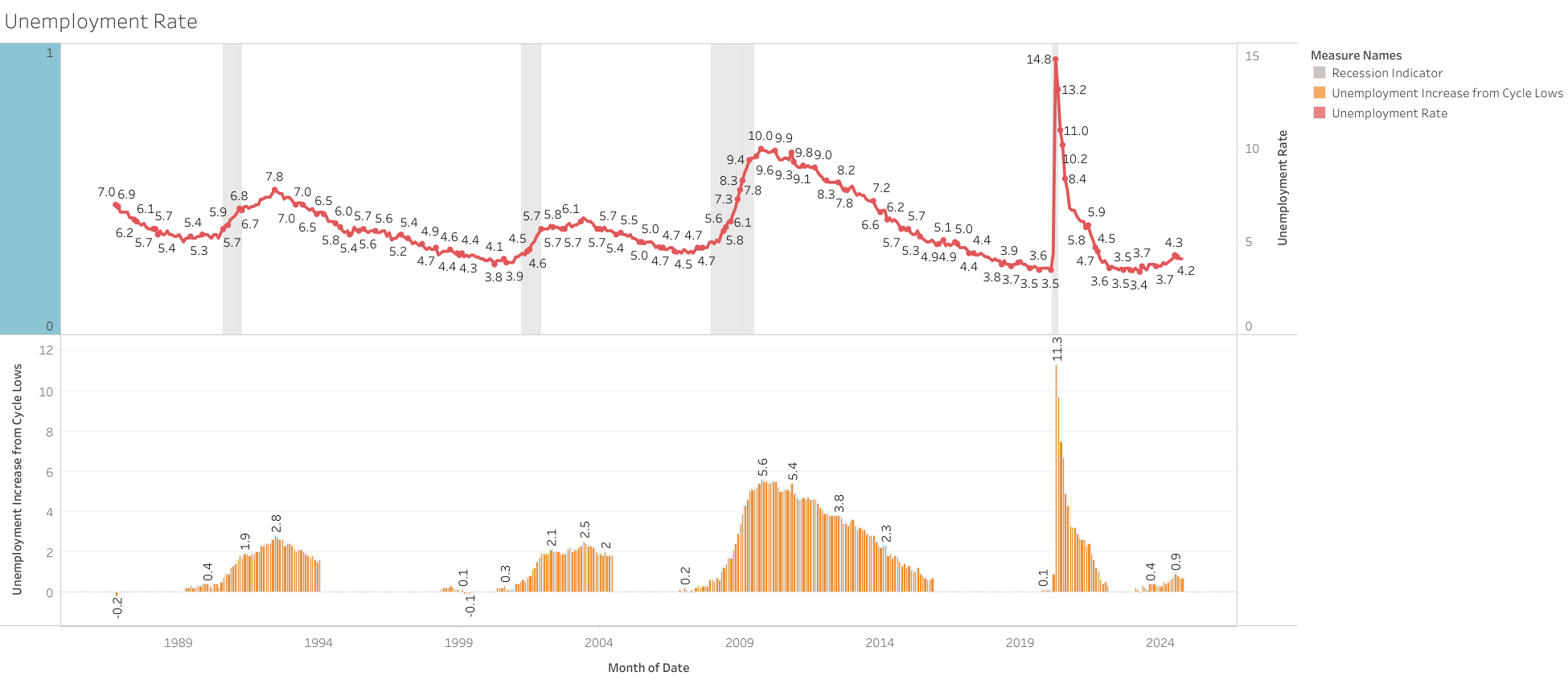

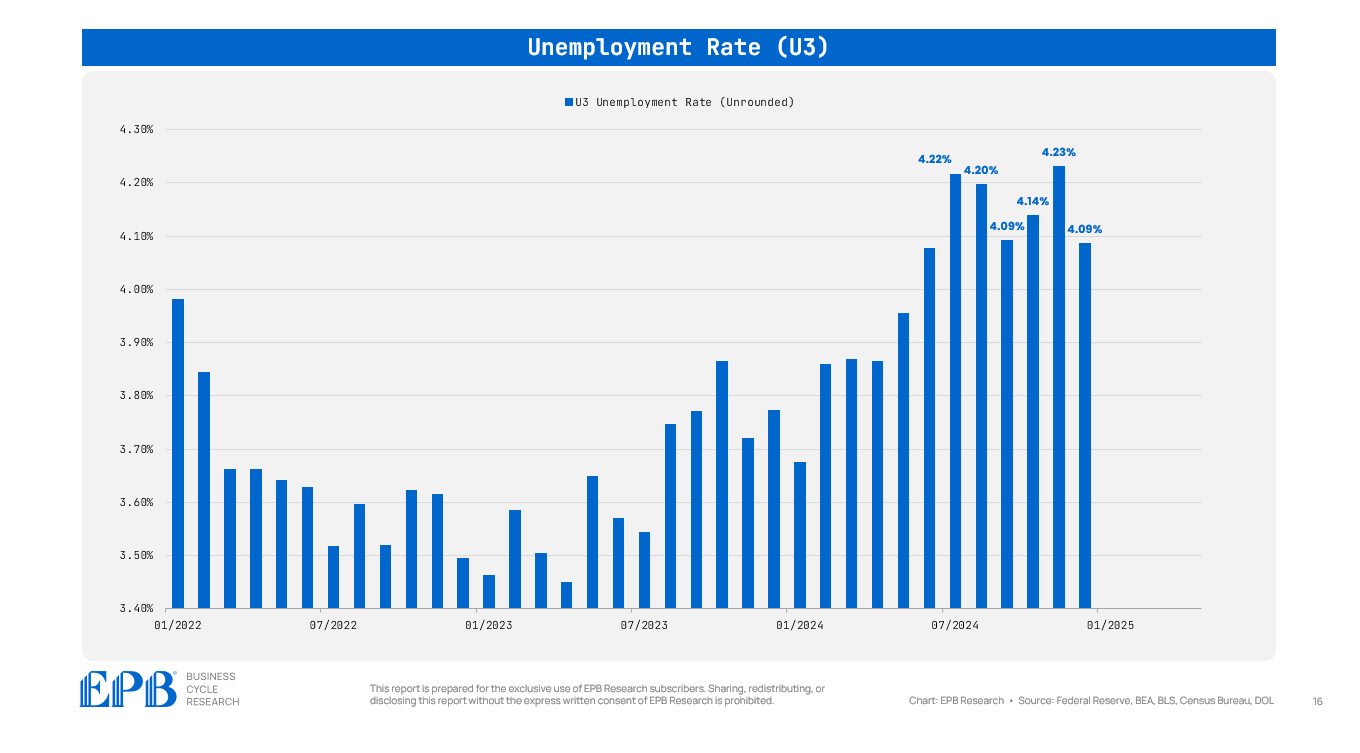

Unemployment barely declined to 4.22% in August from 4.25% in July., so those expecting a significant decline in unemployment because of weather-related effects in July were disappointed.

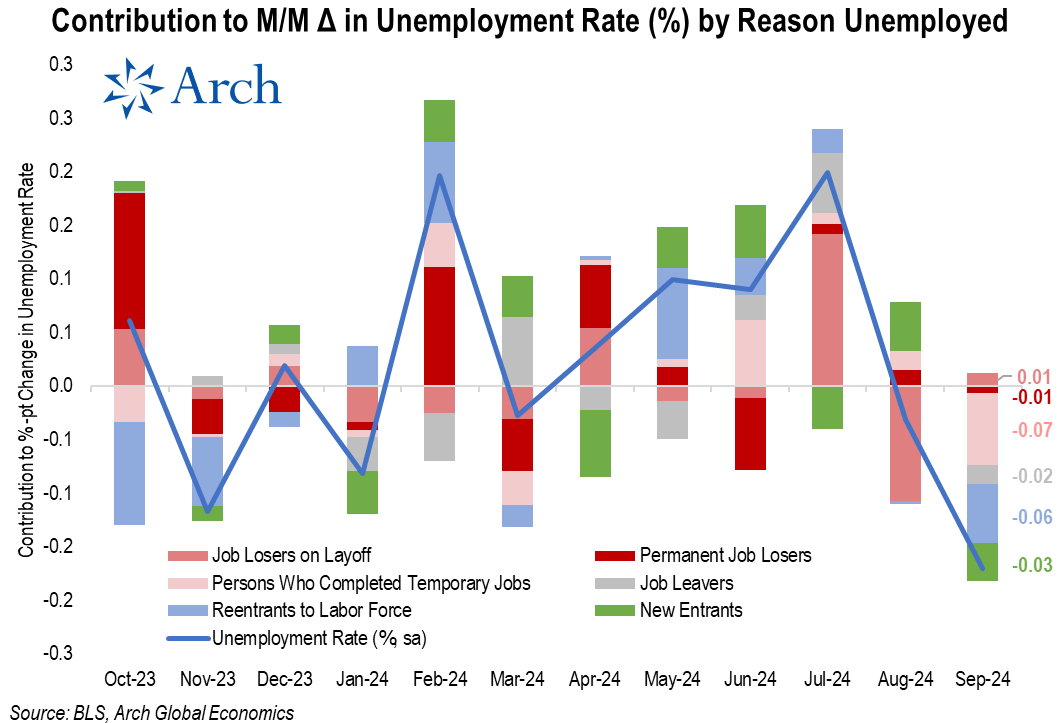

The slight decline is due to temporary layoffs as expected because of the outside surge in July

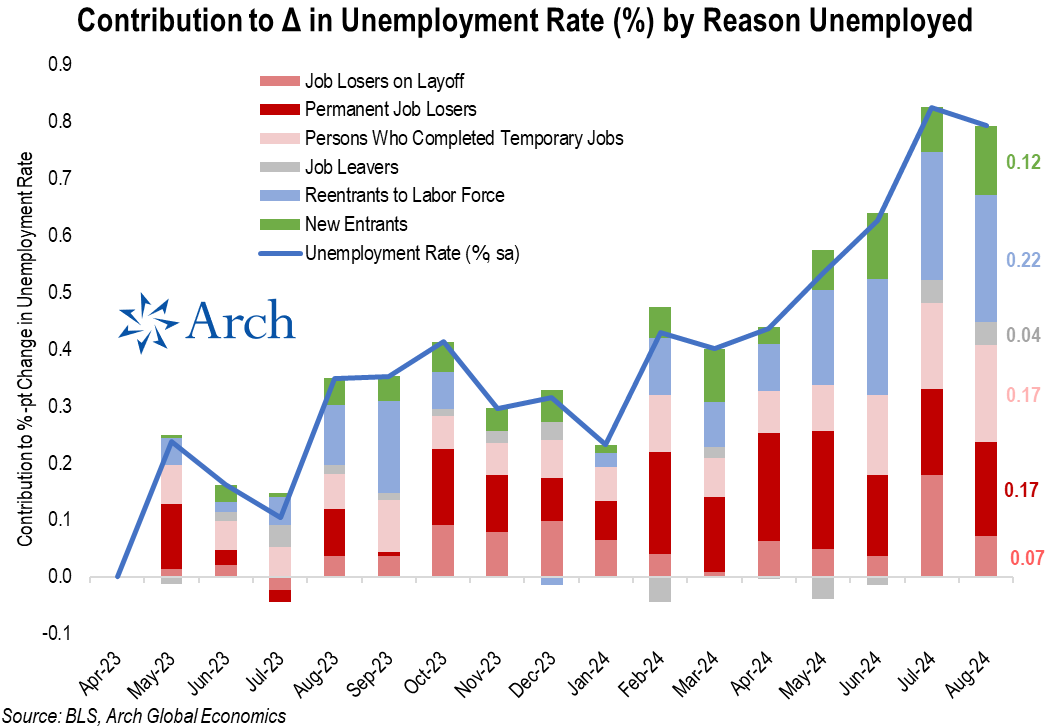

After contributing 14bps to the July increase, temporary layoffs (“Job Losers on Layoff”) subtracted -11bps from the August unemployment rate.

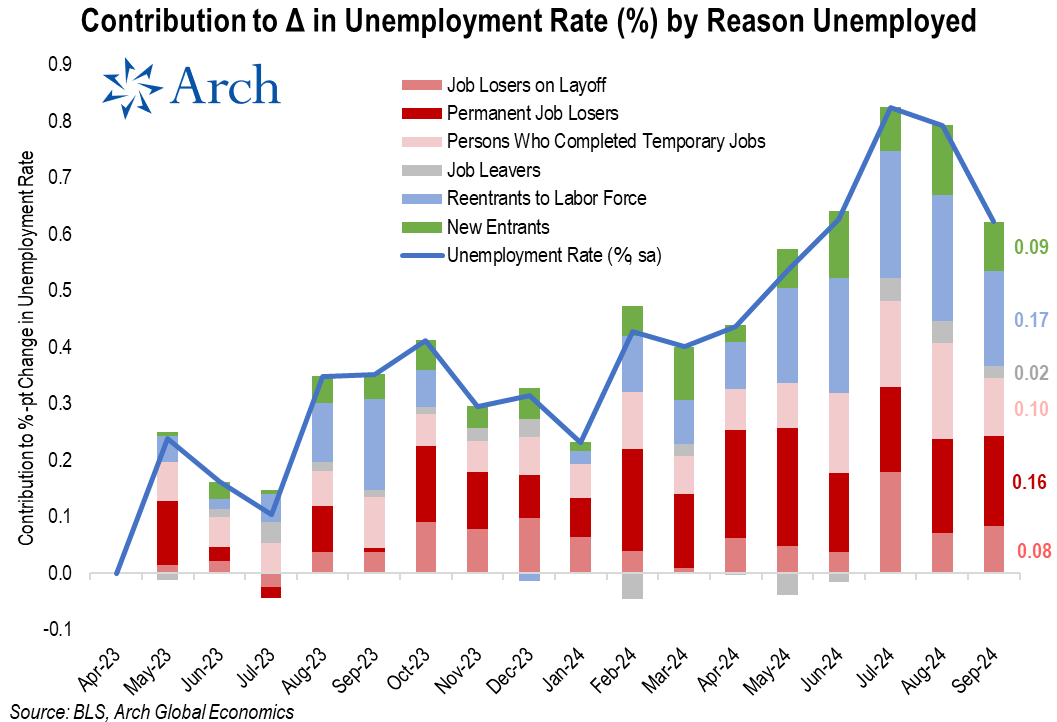

Job losers have accounted for 41bps of the 79bps increase in the unemployment rate since April 2023, with Reentrants (+22bps) and New Entrants (+12bps) combining for 34bps of the increase.

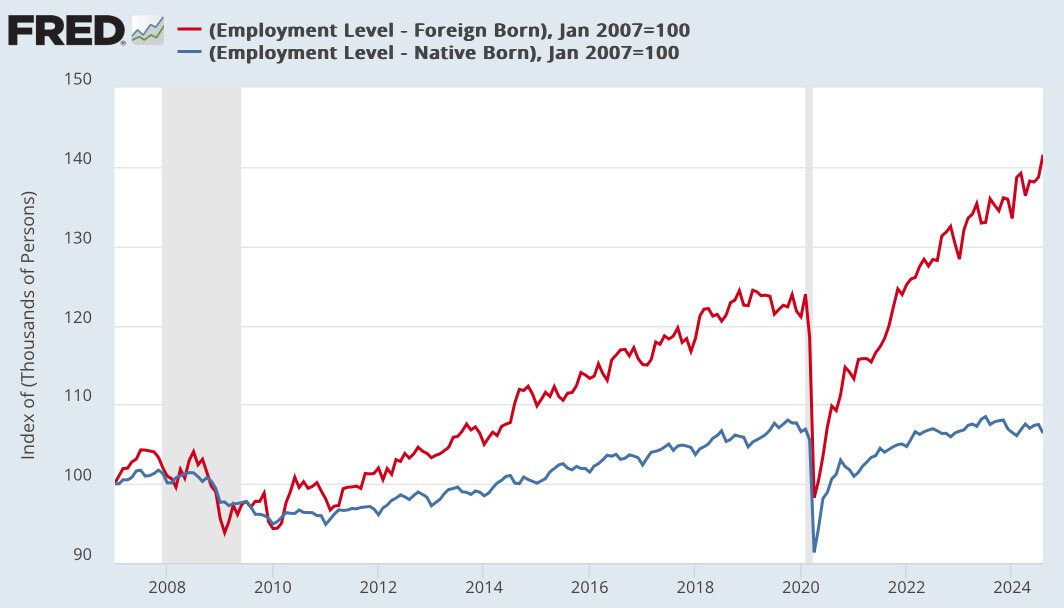

The weakness in native-born jobs continues. The data seems to indicate a clear replacement phenomenon. However, demographics could be playing a role here too.

The faster increase of foreign born jobs seems to be happening since 2007, but after covid it got worse, with native-born not recovering yet.

In just August, 635k immigrants (legal and illegal) gained a job. Meanwhile, 1.325 MILLION native-born Americans LOST their job.

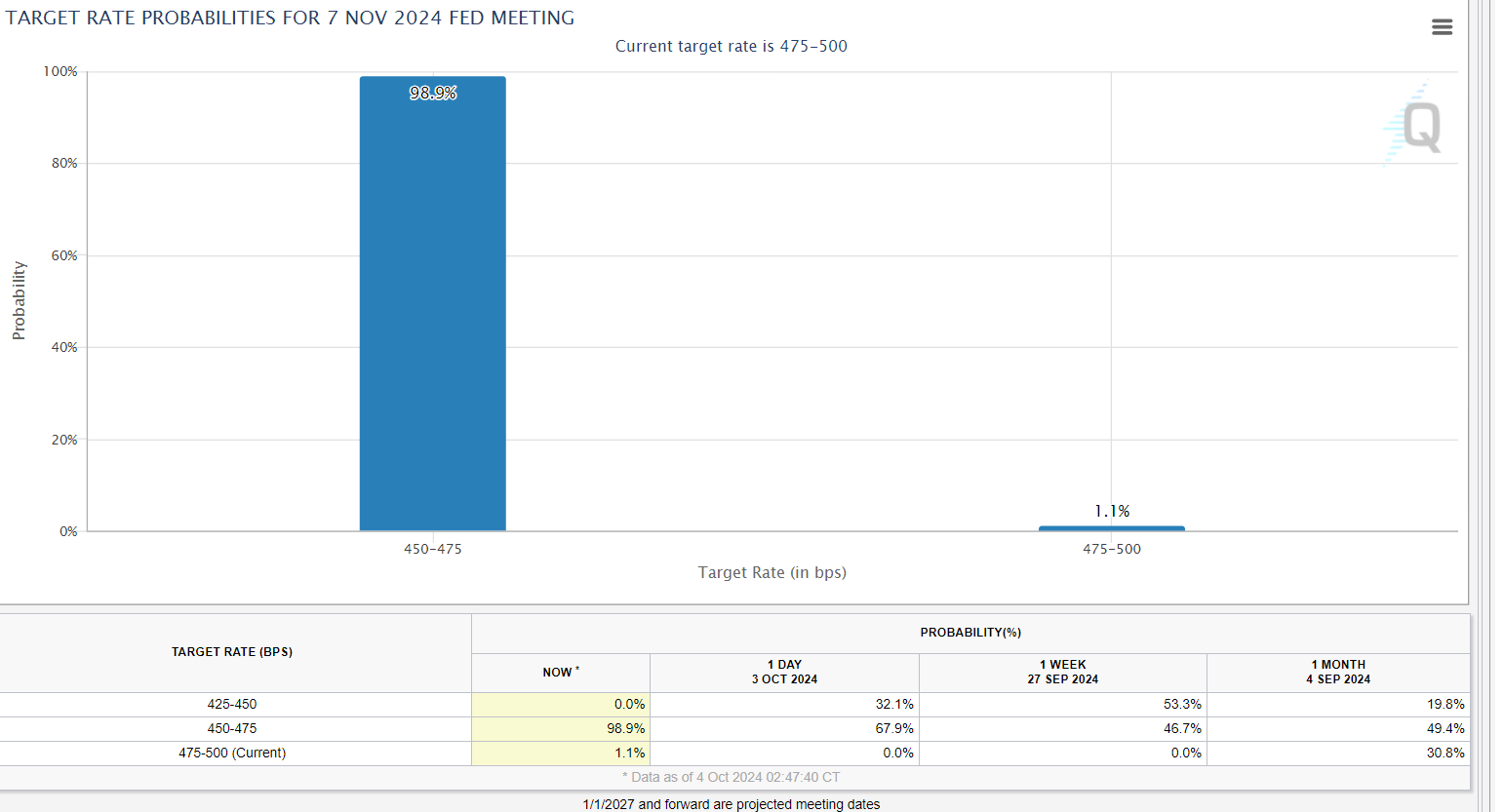

This robust labor market report is likely to prompt the Fed to slow the pace of rate cuts, particularly in light of strong wage growth.

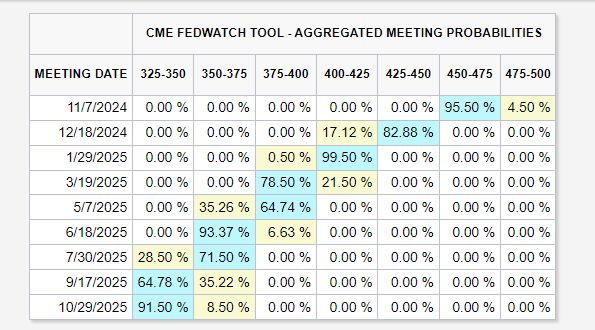

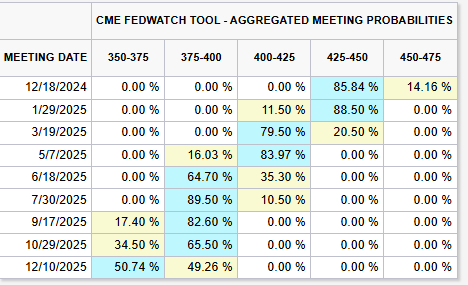

In response, markets have fully priced out the possibility of a 50 basis point cut in November. They are now anticipating just a 50 basis point reduction for the remainder of 2024, with expectations of 100 basis points in cuts during 2025

Despite this report, I still expect the unemployment rate to be higher in 2025, to a level around ~5%.

The number of unemployed persons decreased by 281k (still 7% y/y), while the labor force increased by 150k, leading to a 0.1 percentage point decline in the unemployment rate. However, the rate remains 0.7% higher than the recent lows.

The decline in unemployment was broad-based across most categories. The only upward pressure on the monthly unemployment change came from a modest increase in temporary layoffs during September.

New labor force entrants and re-entrants have now smaller impact on the labor market dynamics compared to previous reports.

U6 Unemployment also declined from 7.9% to 7.7%, still 1.2% from the cycle lows.

Any ideas why September was so good?

Maybe sentiment of businesses improved significantly due to anticipation of rate cuts and better funding conditions?

Do you have shortterm expectations how jobs are going to develop in the next months?

Yeah, it could have been an initial push in sentiment after rate cut expectations increased. It just remains to be seen if it will hold up the same after revisions, but markets/fed will react based on these for now.

The report is not aligned with anecdotal data, both PMI from ISM and SP Global12 showed weaker/contracting employment trends in September.

In other cases, I would say trusting the government data is better, but I am not so sure anymore.

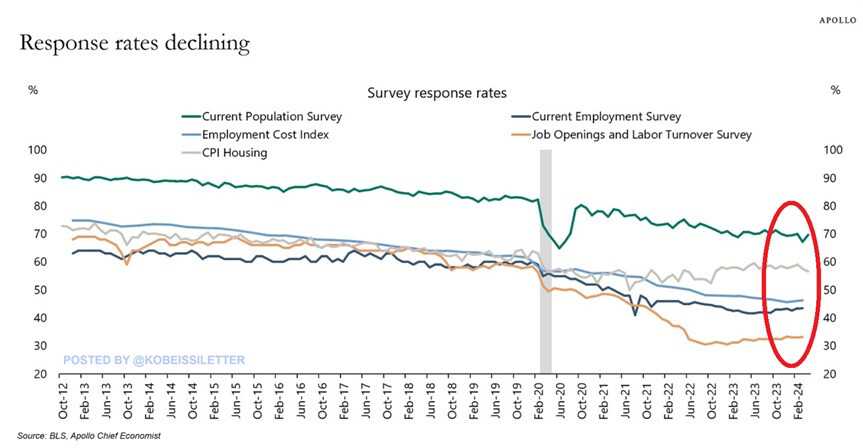

The response rate of government labor surveys is also very low currently, and it could be playing a role in the quality of data.

I don’t have specific expectations about immediate changes in jobs, but my best guess is that we’re unlikely to see significant weakness in the near term, probably still above 100k a month.

A negative payroll print doesn’t seem imminent either.

While I do anticipate a gradual increase in unemployment, especially considering that employment data appears weaker compared than the payroll numbers, but it’s likely to rise more slowly than in other periods.

The US has added on average 88k per month in the labor force since 2010, so it does not need negative payroll growth either to see unemployment increasing significantly.

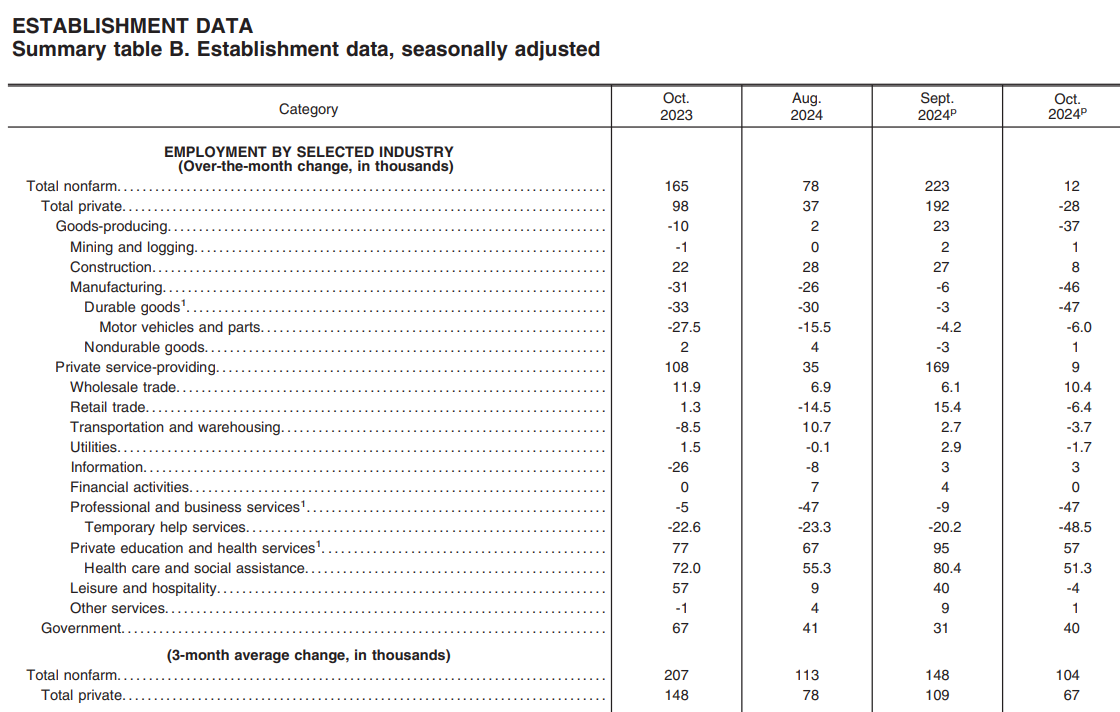

I=8 Nonfarm payrolls missed estimate, impacted by Boeing strike and hurricanes

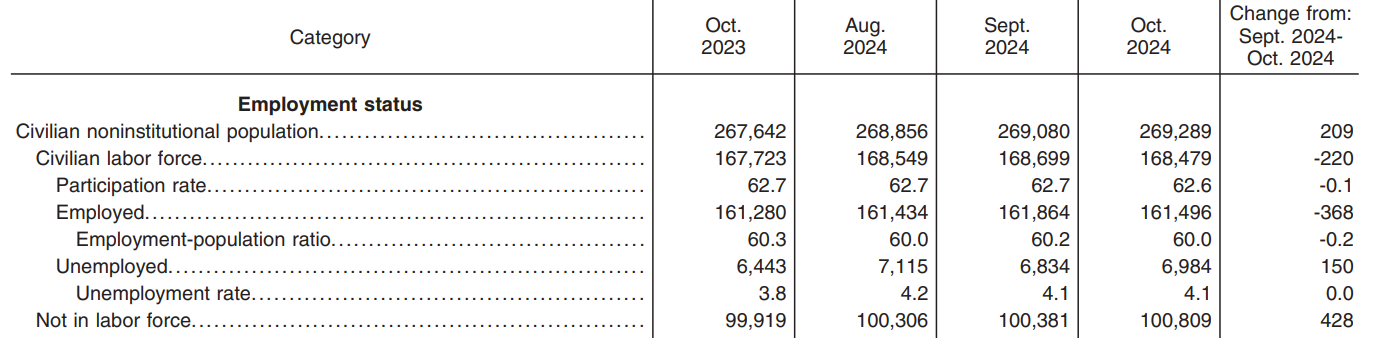

The U.S economy added 12,000 jobs in October, below 106,000 estimate and down from 223,000 in September (revised downwards from 254,000)-impacted by Boeing strike (-44,000) and hurricanes Helene and Milton.

Unemployment rate was steady at 4.1%, in line with the forecast.

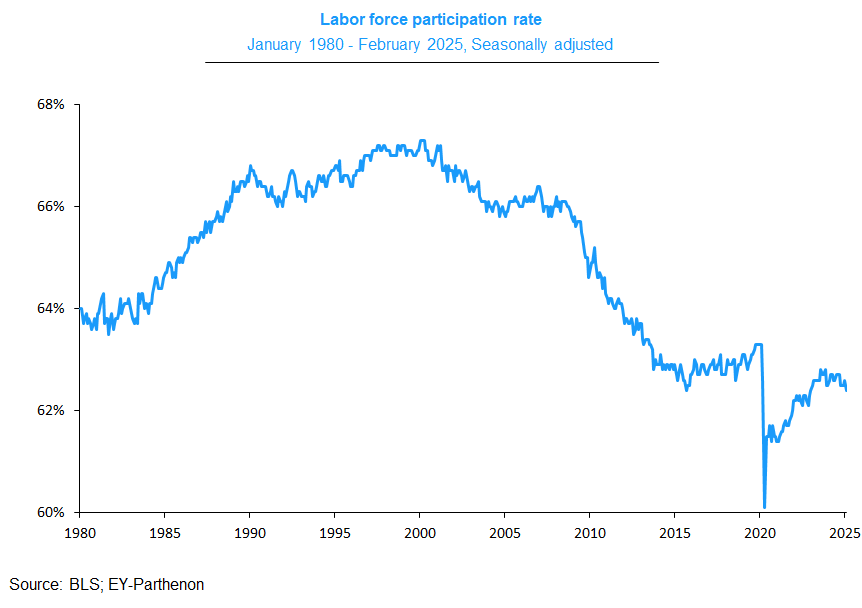

Labor force participation rate came in at 62.6% versus expectations to stay steady at 62.7%.

Average hourly earnings rate rose 0.4% on the month against expectations for it to remain unchanged at 0.3%. September number was revised downwards from 0.4%.

On a yearly basis, average hourly earnings rose 4.0%, in line with the estimate and and above 3.9% in September (revised downwards from 4.0%)

Despite data noise from weather events and Boeing strikes, the October labor report still reflected underlying softness or some concerns:

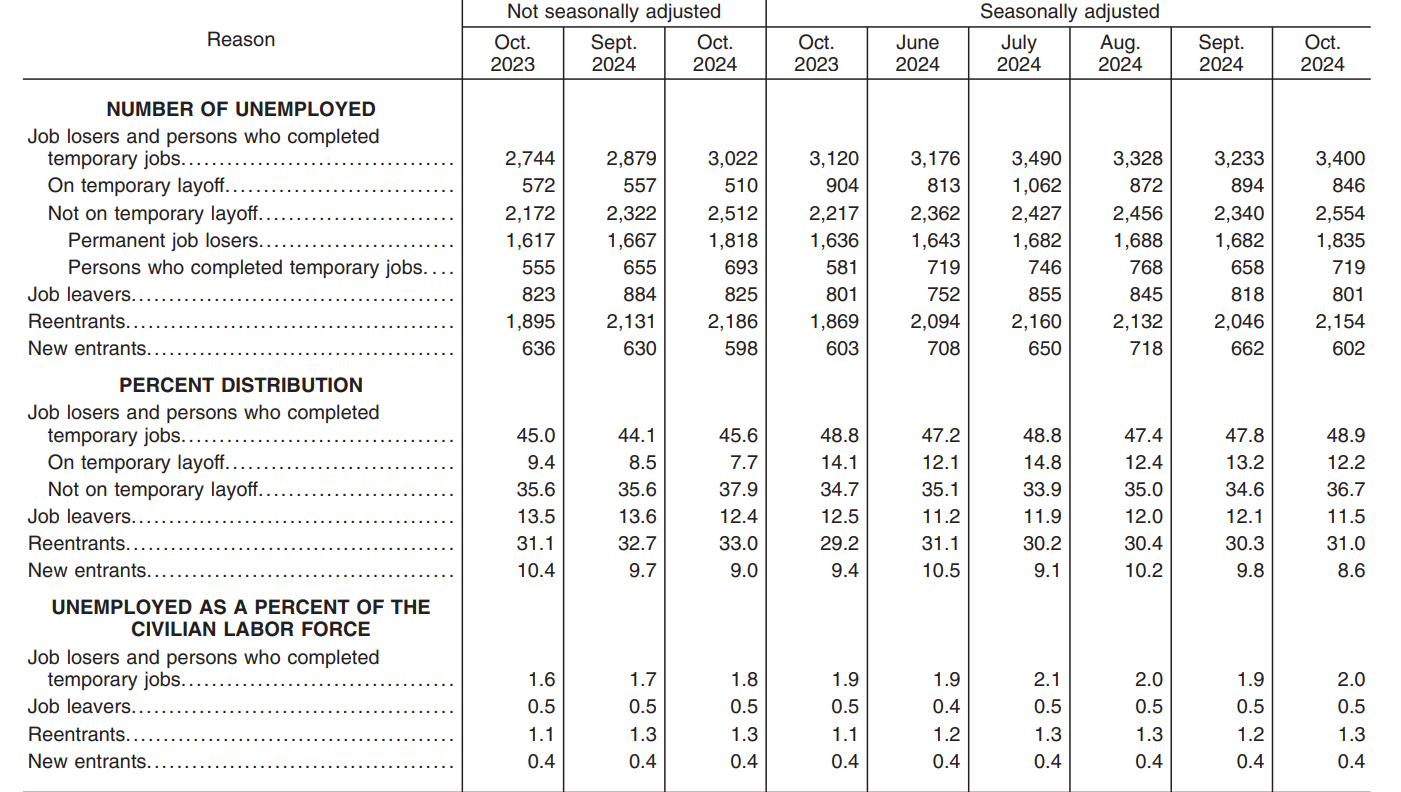

The unrounded unemployment rate did edge up by nearly 0.1%, not related to weather most likely. With permanent job losers continuing to increase.

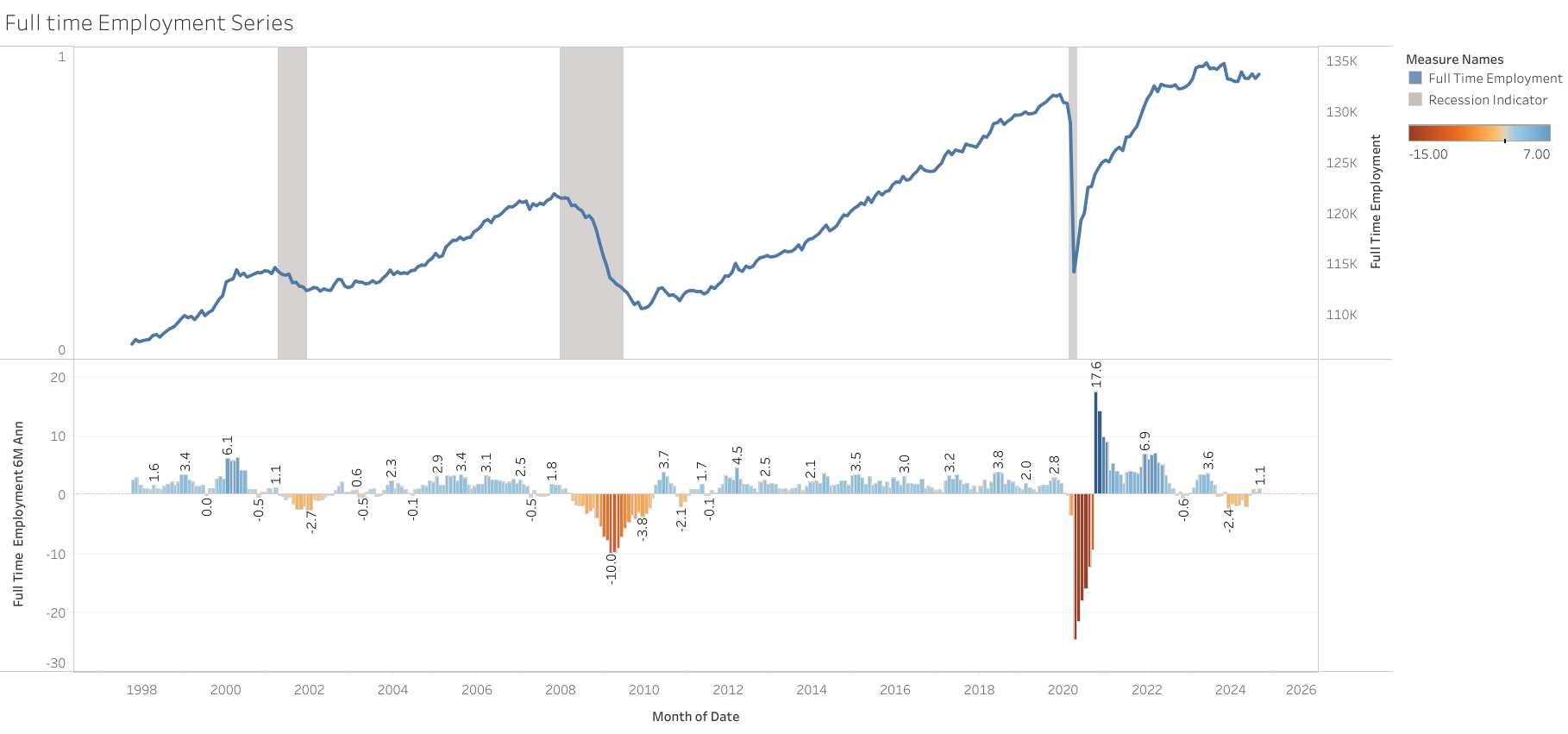

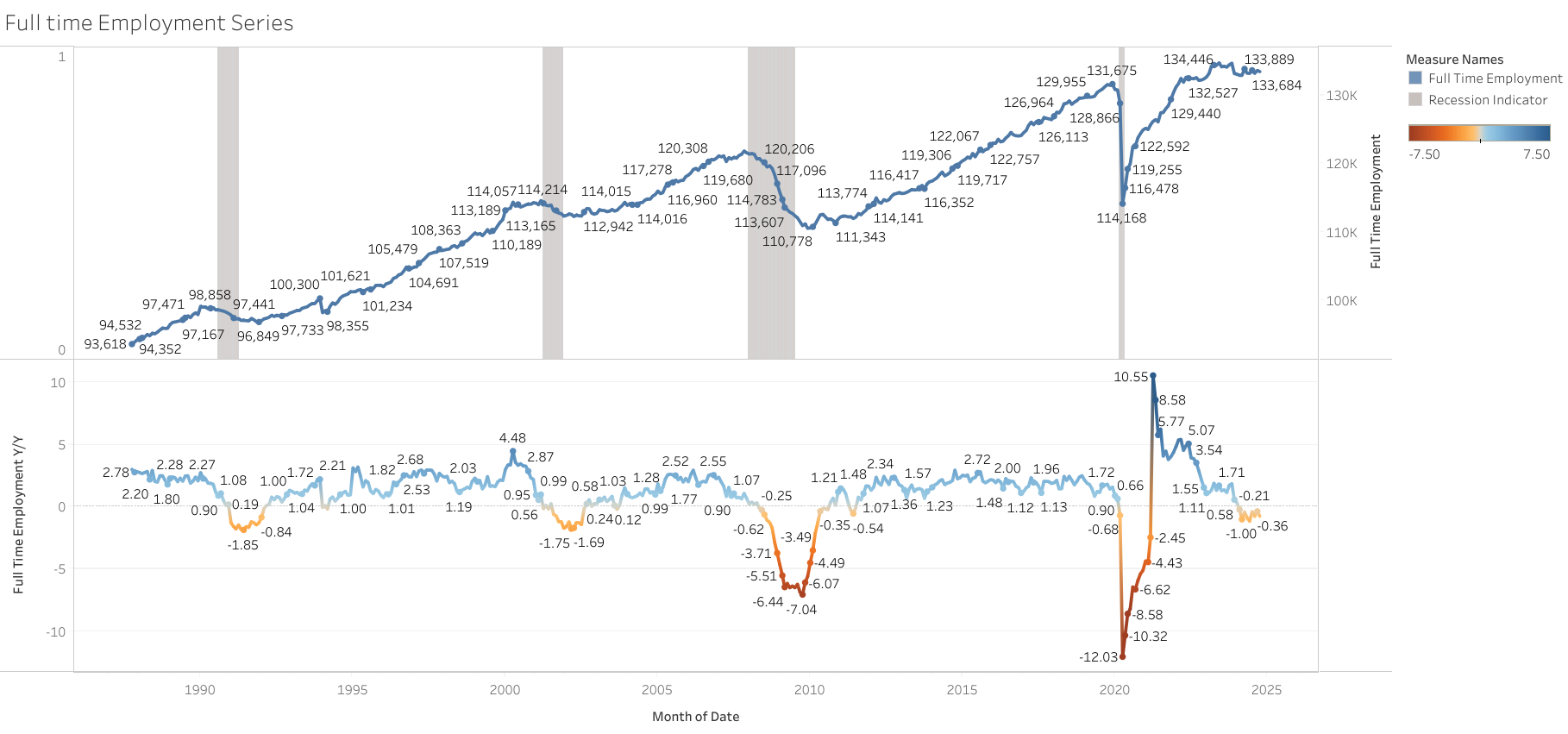

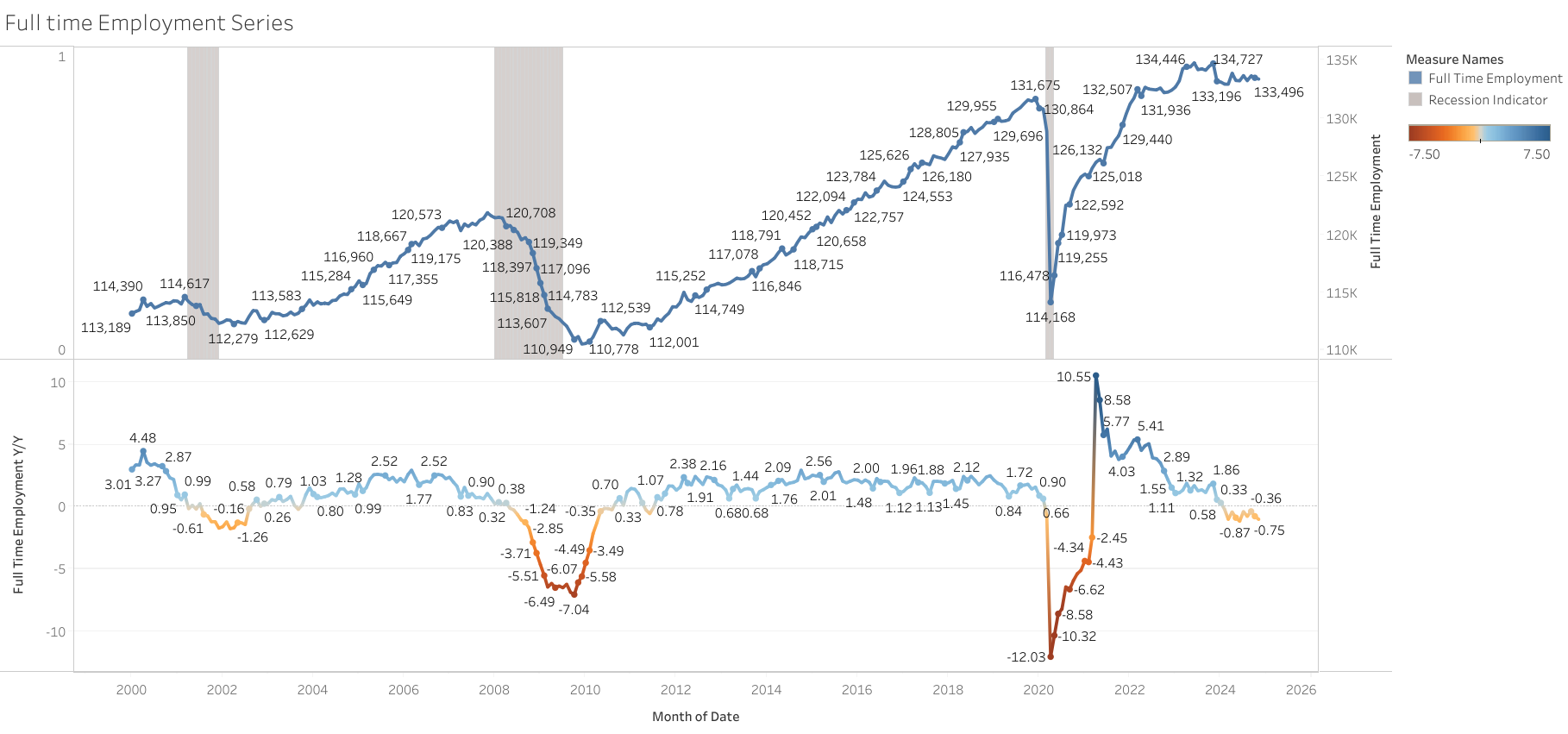

Both employment and full-time employment remain subdued, essentially flat year-over-year.

The participation rate of prime-age workers continued to decline, this could suggest some discouragement in the job search, but this is not something these surveys provide.

Overall, the labor market appears to still be on a gradual weakening path IMO, but very gradual. Given this report and the broader data released this week, a 25-basis-point rate cut next week still seems the more likely scenario.

The market continues to anticipate two more cuts in 2024, with an additional three projected for 2025.

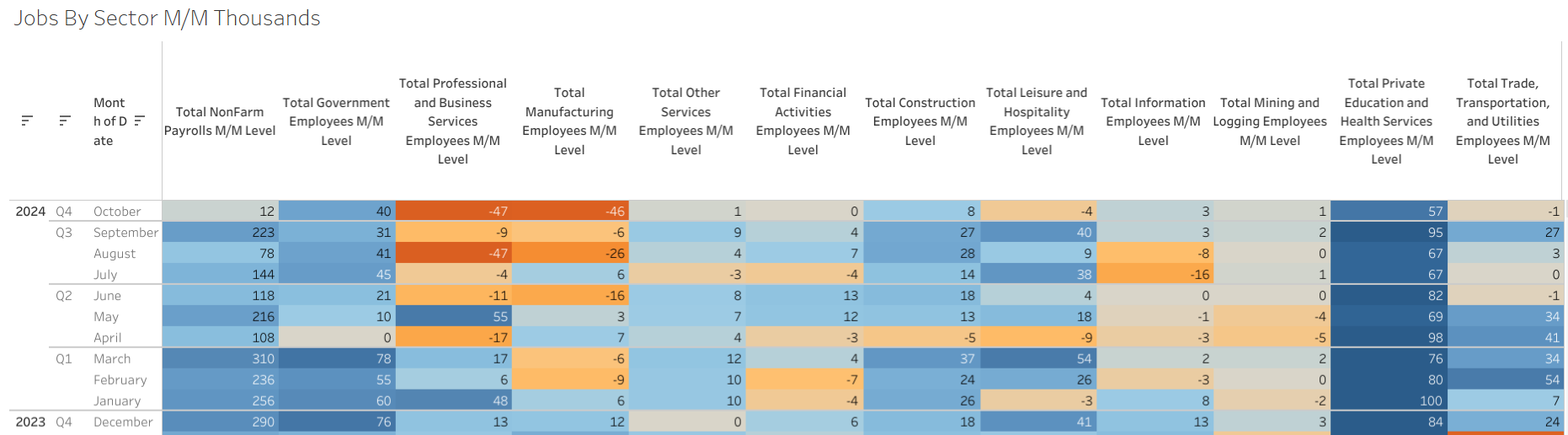

Almost all payroll categories showed weakness or flat growth, with weather unlikely to account for the full impact, but without these disruptions is most likely the report would have shown a bit over 100k payrolls:

Manufacturing declined by 46,000, primarily in durable goods, with much of this attributed to Boeing-related disruptions.

Professional and Business Services dropped by 47,000, notably in temporary services, where the downturn reflects broader weakness in the sector that has persisted for months even below 2019, independent of weather effects.

Private Payrolls Fell by 28,000, while Government Payrolls saw a rise of 40,000.

The unemployment rate did increased to 4.145% from 4.05% the previous month,

Unemployment people increased by 150k and is 8.4% y/y . The unemployment rate did not go up more due to the decline in the labor force by 220k.

Prime-age workers (25-54 yrs) responsible for the drop in the labor force. Participation rate declined to 83.5% in October, down from 83.8% last month.

Increased in unemployment due to job losers or reentrants, weather did not have any meaningful impact on the increase since people on temporary layoffs did decline instead.

Permanent job losers increased by 153k, and is 12.24% y/y

Although this month’s payroll rebound reflects a recovery from last month’s weather-induced weakness, my assessment remains that the labor market is continuing its gradual and protracted slowdown.

This dynamic, coupled with the rise in the unemployment rate, has bolstered market confidence that the Federal Reserve will cut rates by 25 basis points in its upcoming meeting. However, expectations for additional rate cuts in 2025 remain modest

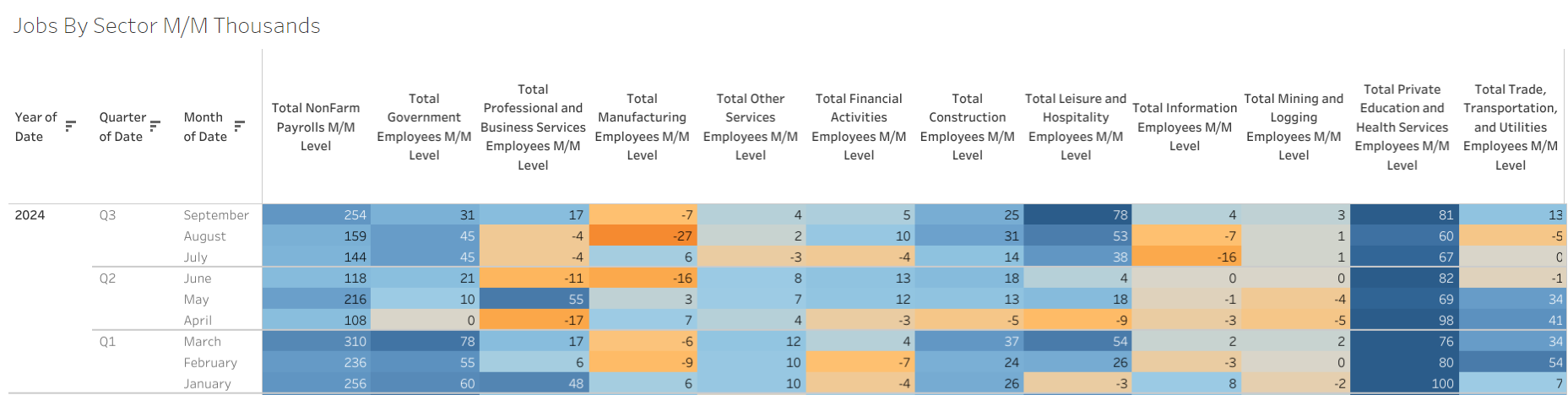

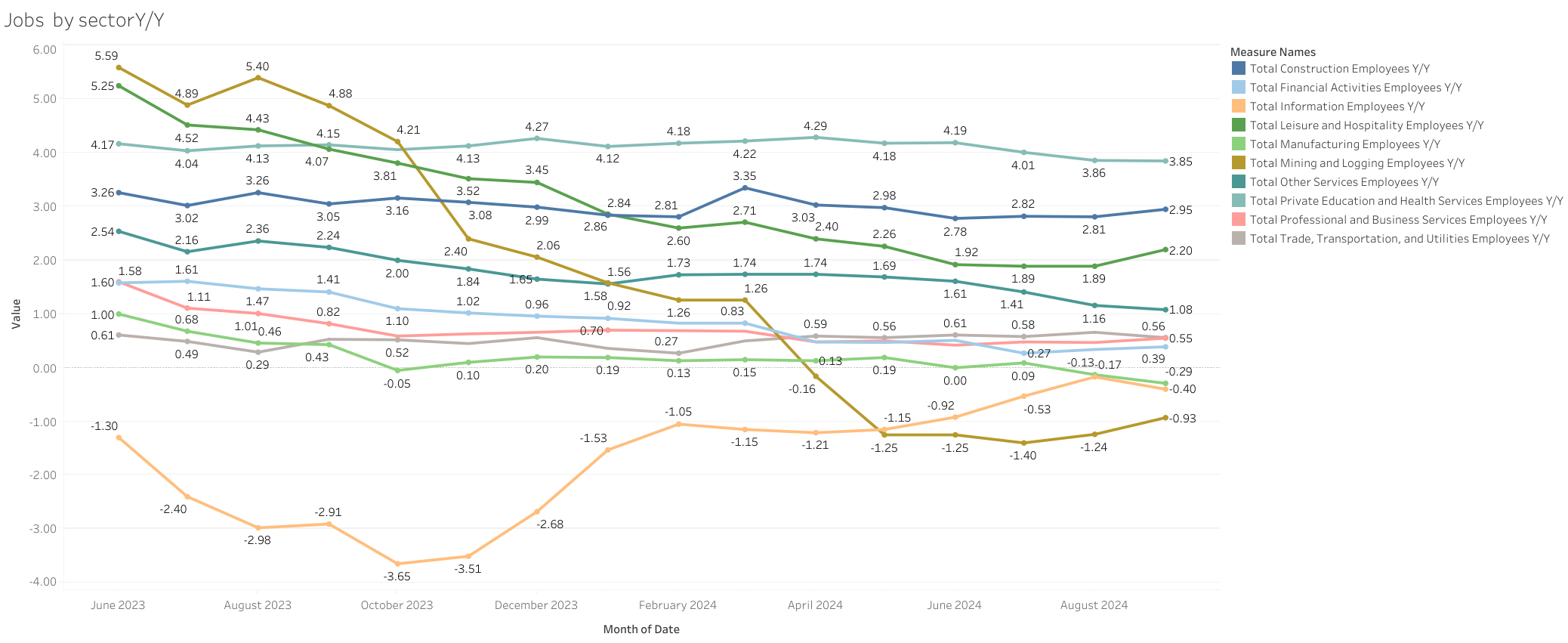

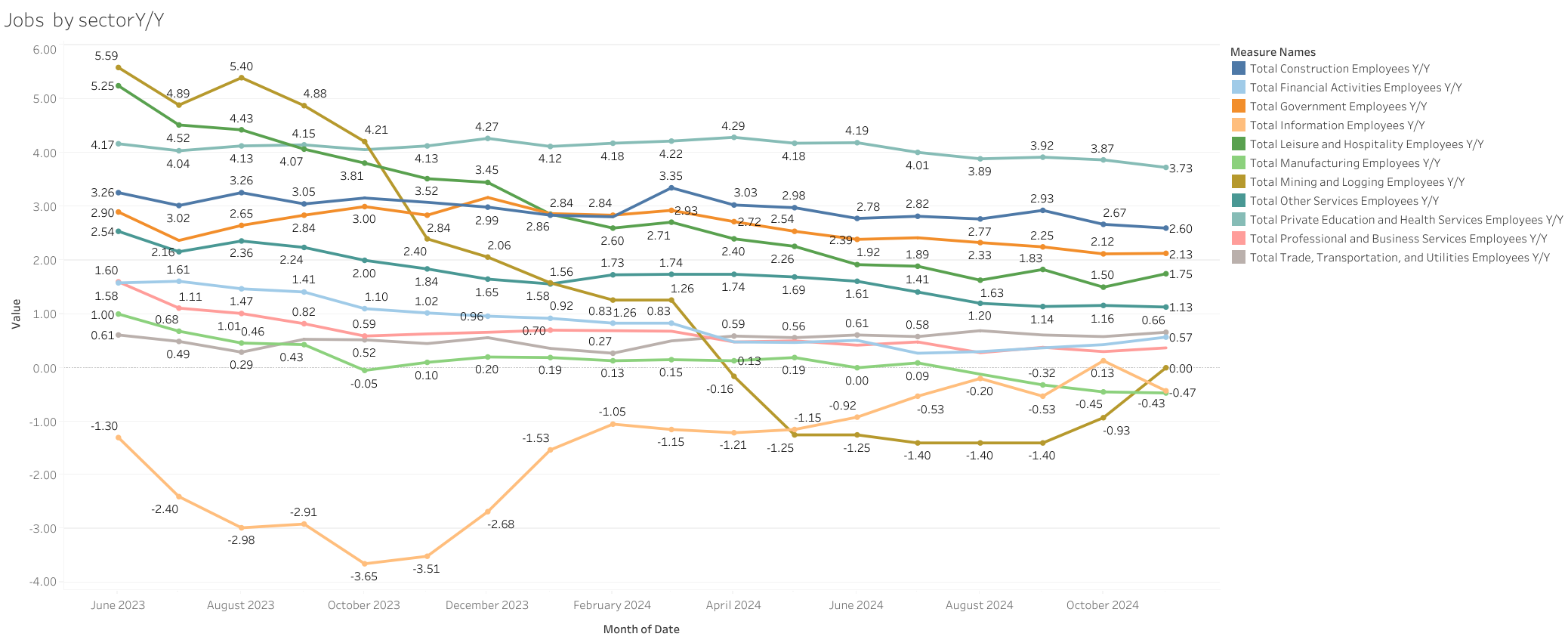

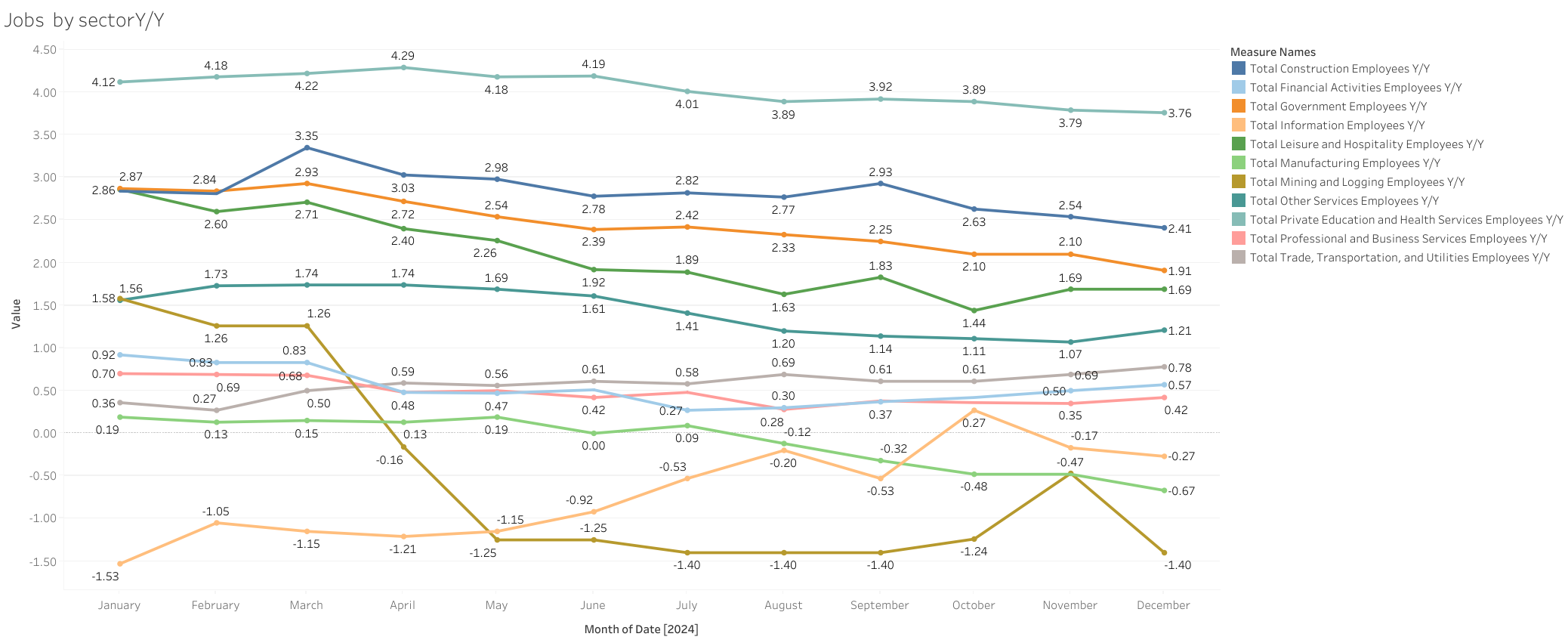

Industries such as manufacturing, information, business services, financial activities, and trade and transportation are experiencing stagnant or declining job growth rates.

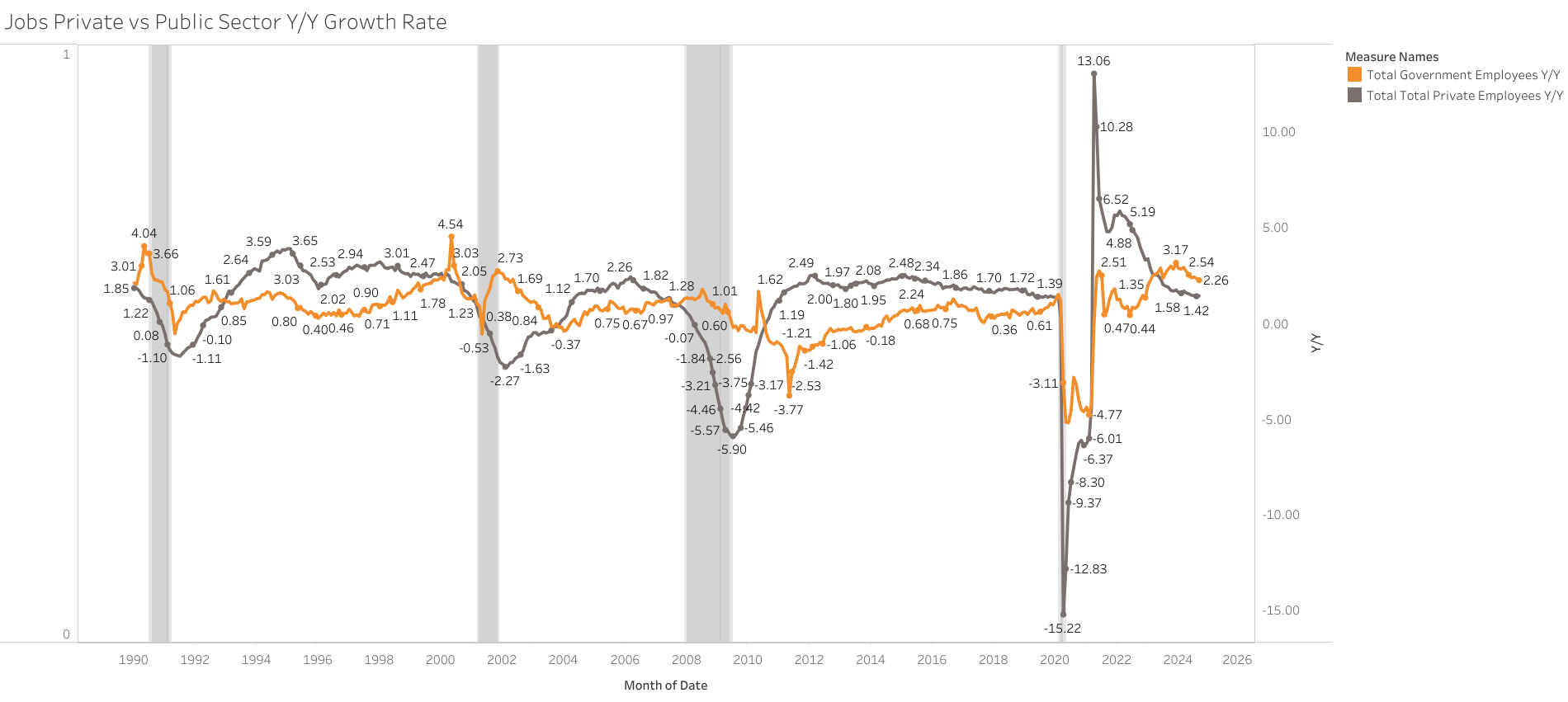

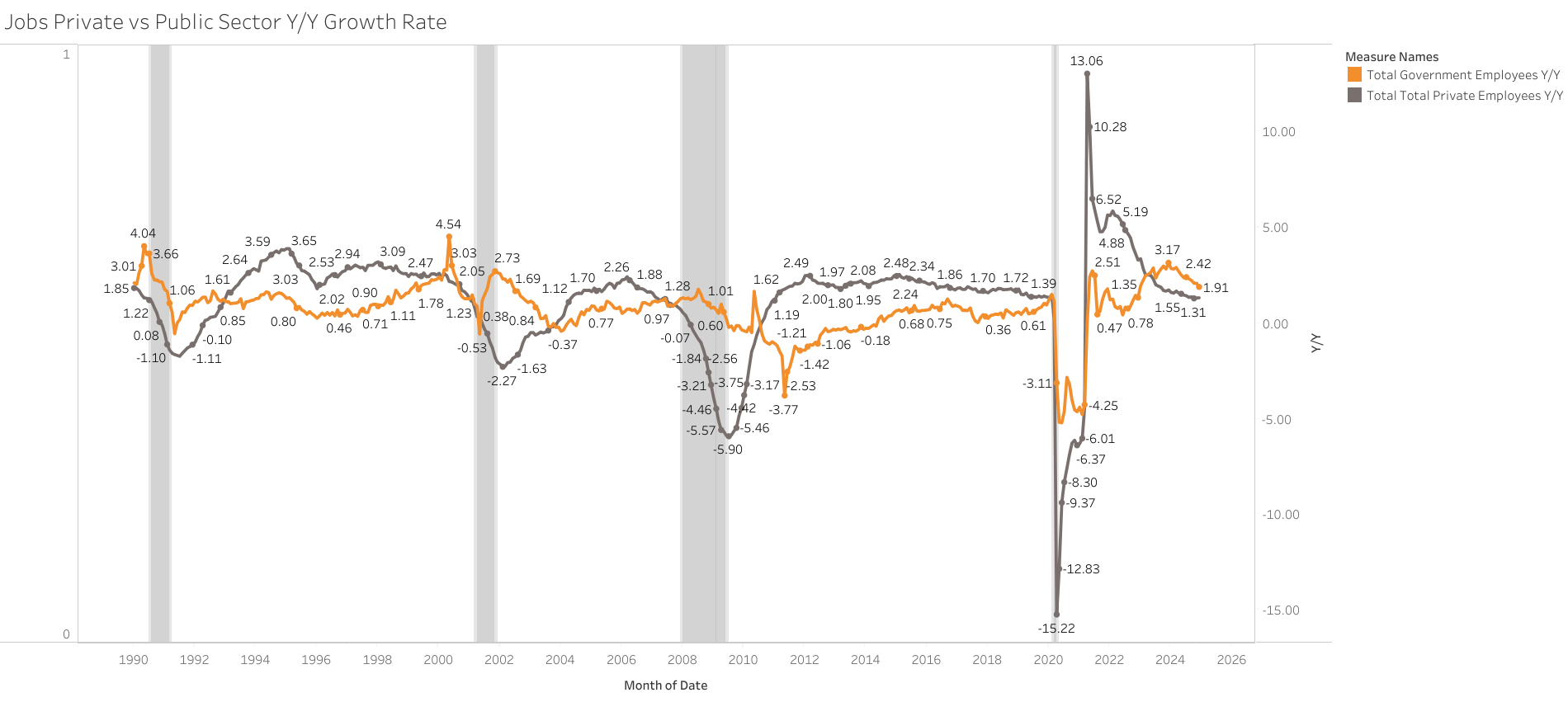

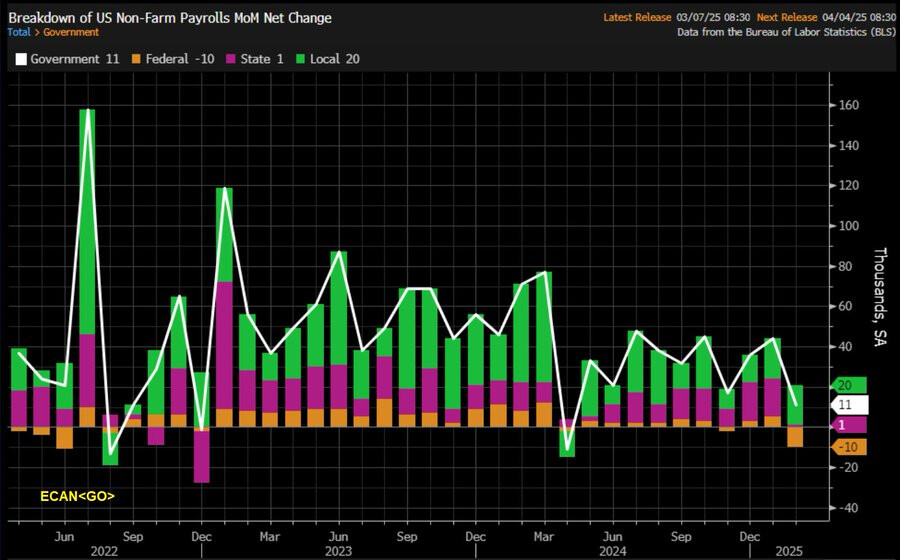

Job growth within the government sector continues to outpace that of the private sector significantly.

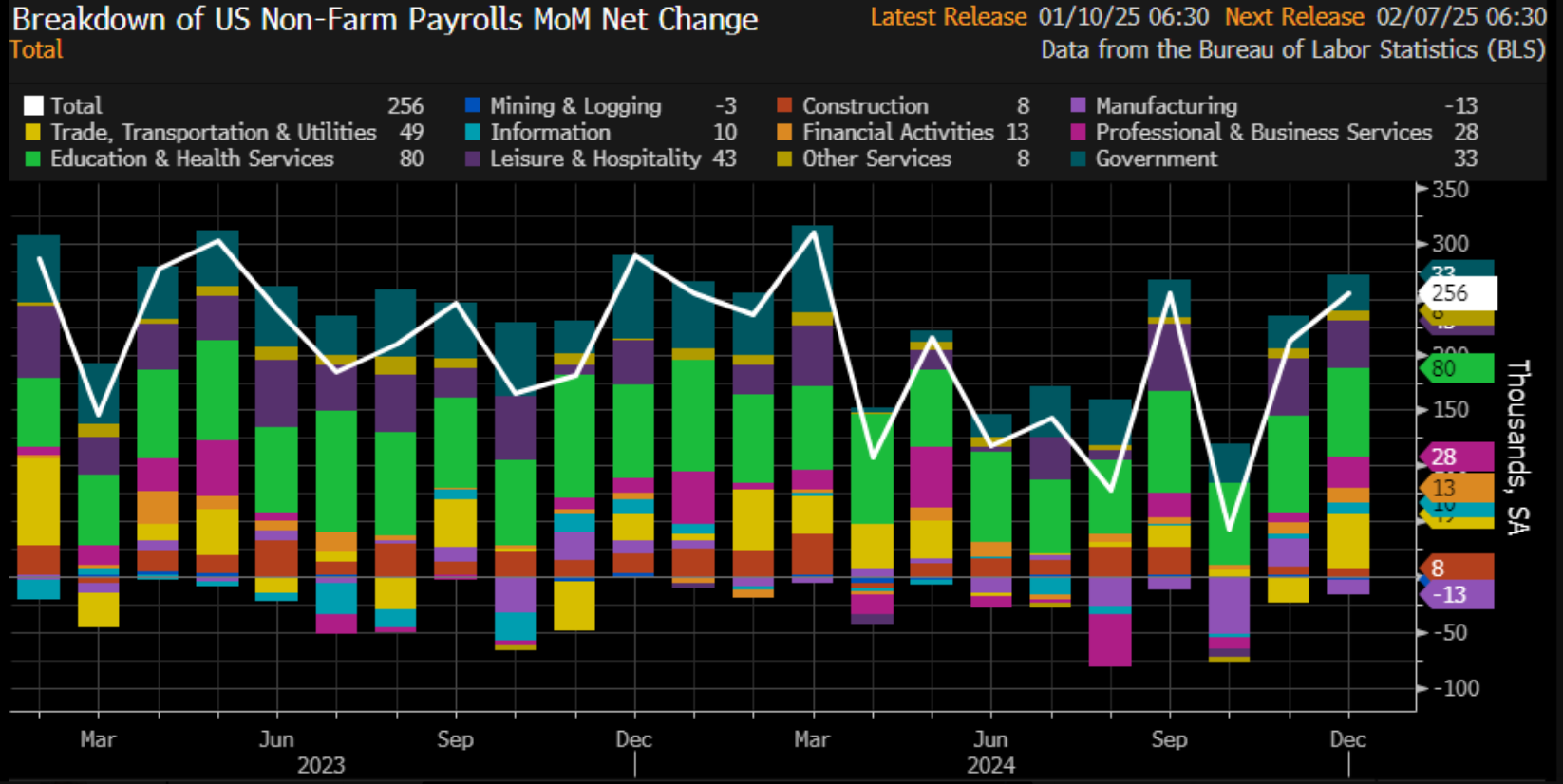

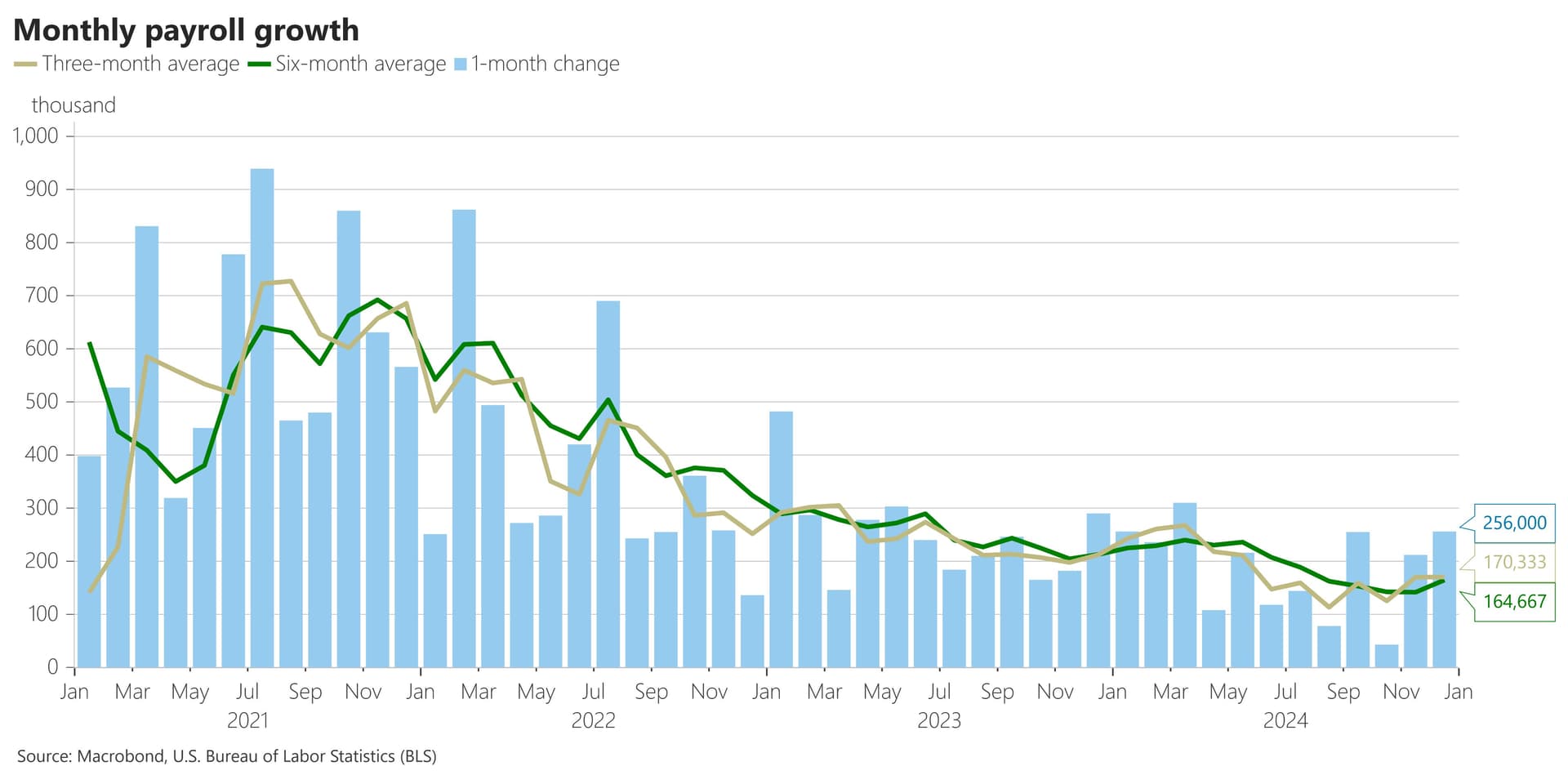

I=8 Nonfarm payrolls rose 256,000, hotter-than-expected, causing 10-year treasury yield to rise 10 basis points

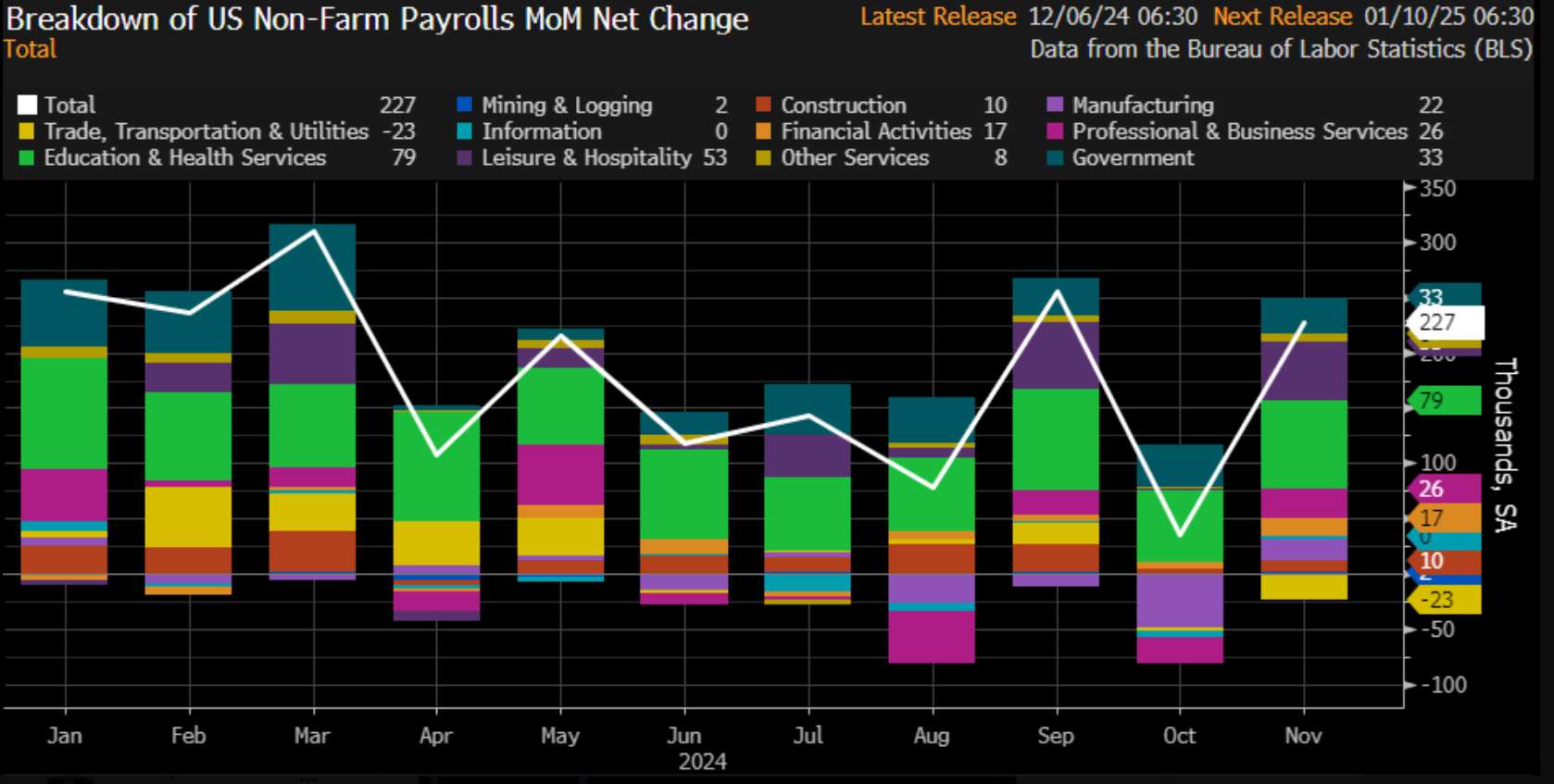

U.S payrolls grew by 256,000 in December, up from 212,000 (revised downwards from 227,000) and above the 164,000 forecast.

Unemployment rate came in at 4.1% versus expectations for it to stay steady at 4.2%.

Labor force participation rate remained steady at 62.5%.

At 0.3%, average hourly earnings was in line with expectations but down from 0.4% in November.

On a yearly basis, average hourly earnings fell to 3.9% from 4.0% in November.

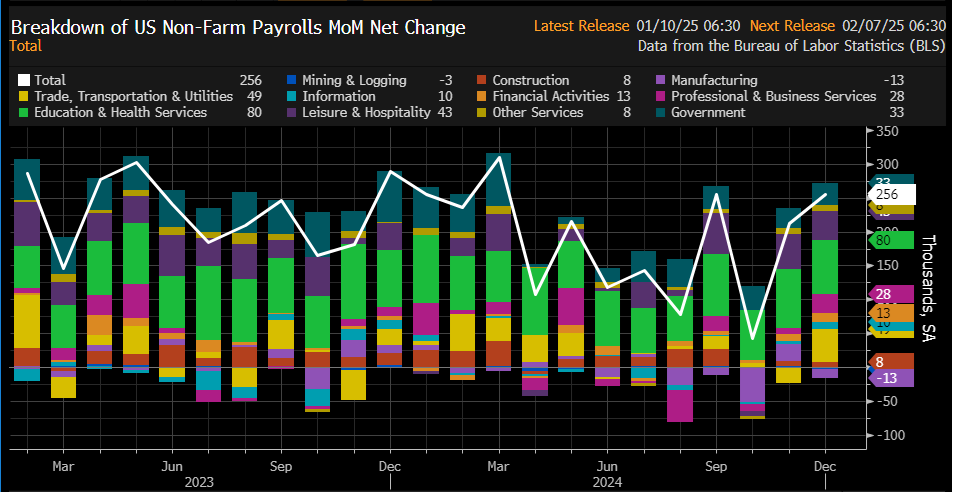

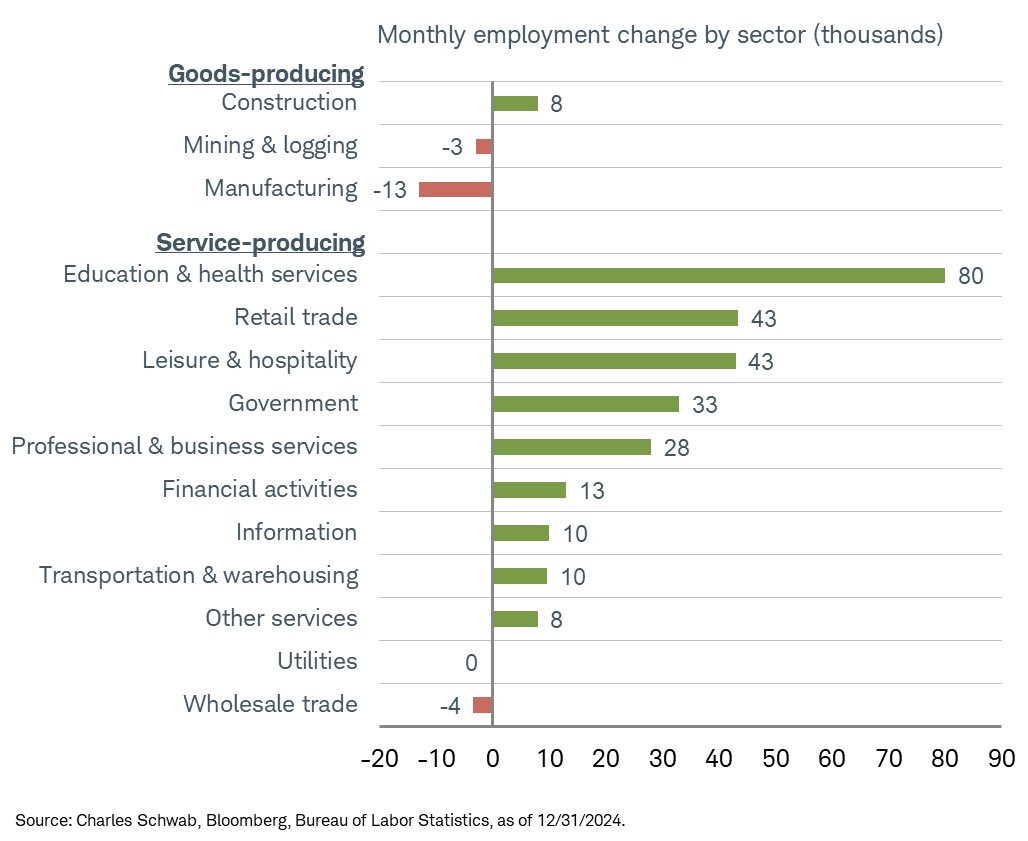

Sectors with the biggest gains were education and health while mining and manufacturing were the only ones with job losses.

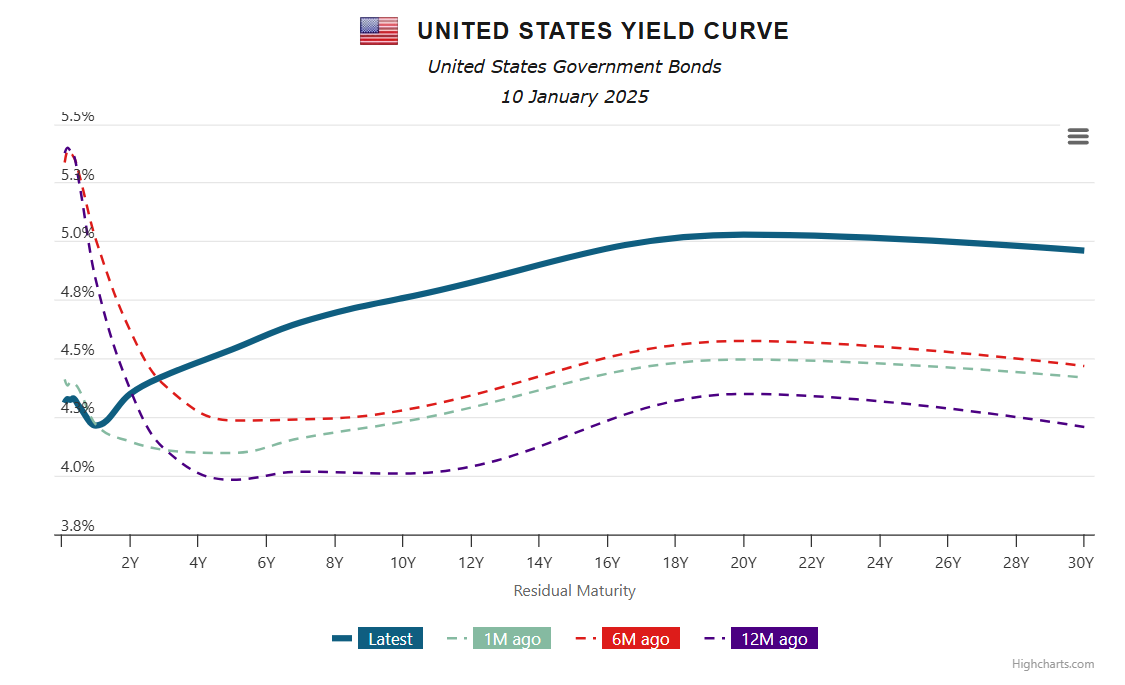

S&P 500 futures shed 1%, Nasdaq-100 futures fell 1.2%, Dow Jones futures dipped 0.8%, while 10-year Treasury yields rose 10 basis points to 4.778%, the highest since November 2023 as the report likely gives the fed a reason to halt rate cuts.

The significant market reaction stems from the substantial miss in expectations, though this report does not fundamentally change the labor market dynamics:

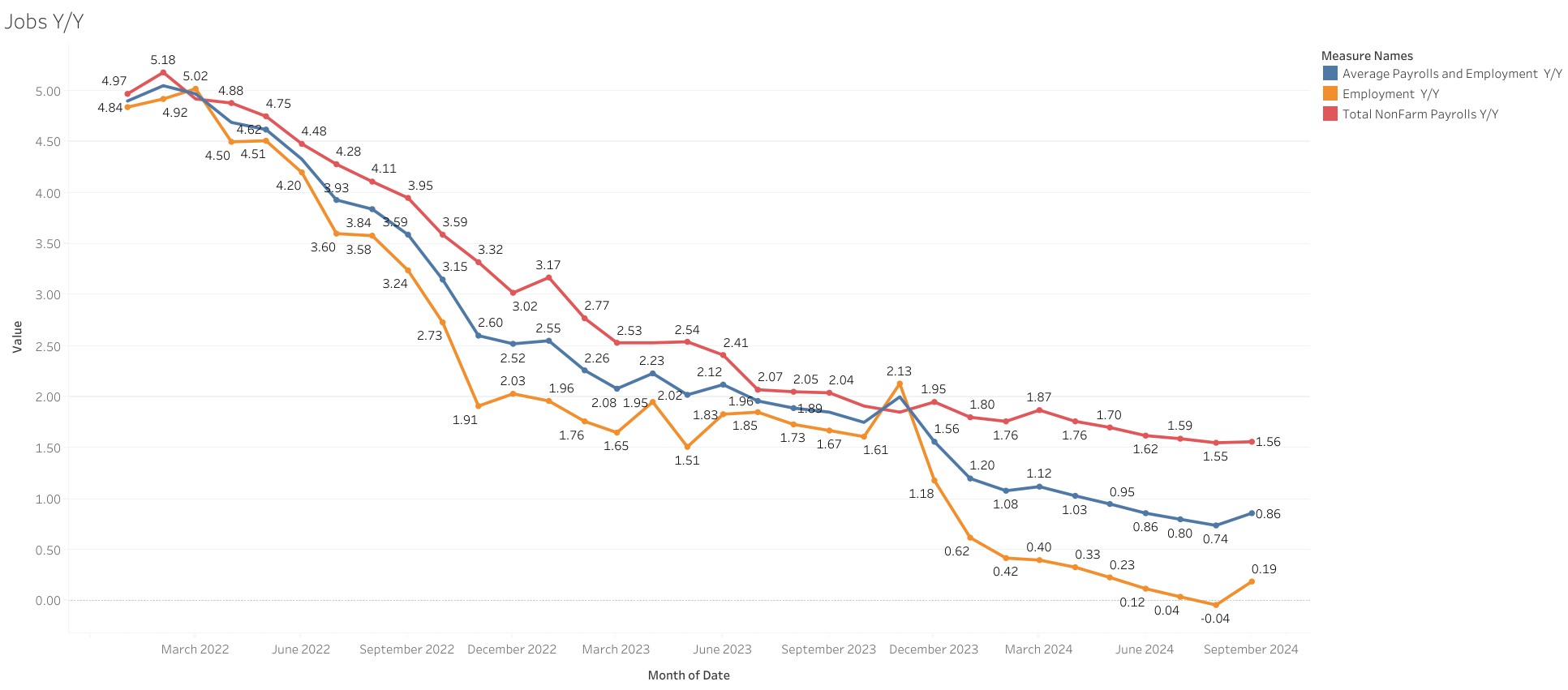

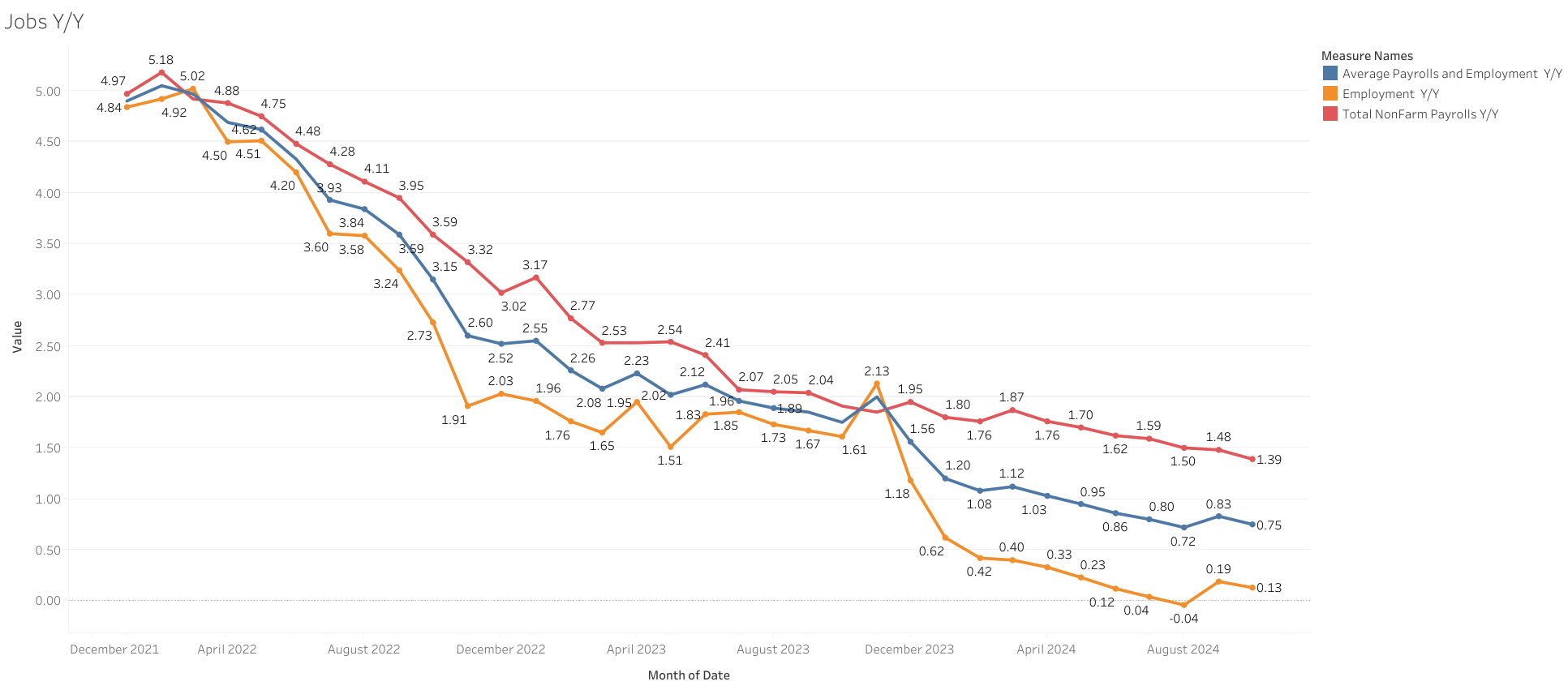

Job growth continues to slow on a year-over-year basis, currently slower than historical average

Employment and full-time employment, despite showing a positive month (there is a lot of volatility in the series), remain largely flat, with no growth since 2023

Most of the job growth continues to be part-time workers.

Unemployment has been hovering in the 4.1%–4.2% range since June, but remains up on a year-over-year basis.

Wage growth softened compared to both the previous month and expectations.

While a continued trend of similar reports could eventually suggest a reacceleration of labor market activity, the current growth remains far from the very tight conditions seen in 2021–2022. For now, the labor market appears stable, still supporting growth, but with more indicators pointing towards softening than overheating.

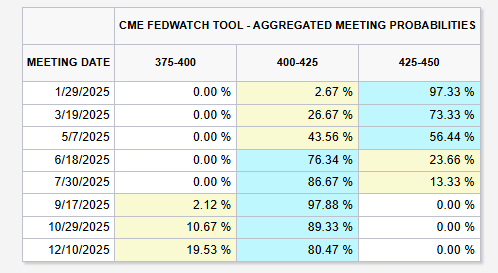

This report triggered a rise in yields, now approaching 5%, and a decline in rate cut expectations, with the next cut not priced in until June 2025.

However, rate expectations do not have much merit imo, just 4 months ago, the market had priced in nearly 250 basis points of cuts by end of 2025, while now it anticipates closer to 125 basis points.

Expectations could shift again with any dovish data at any time.

That said, based on current data, rate hikes remain highly unlikely this year, (probabilities around 10% at best)

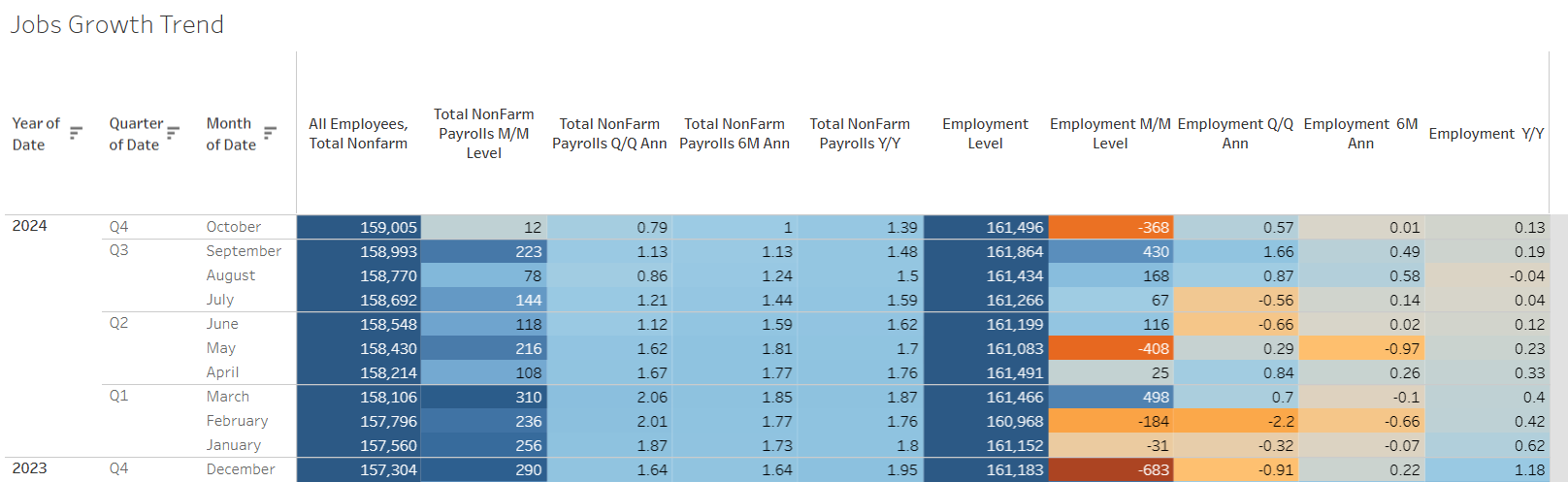

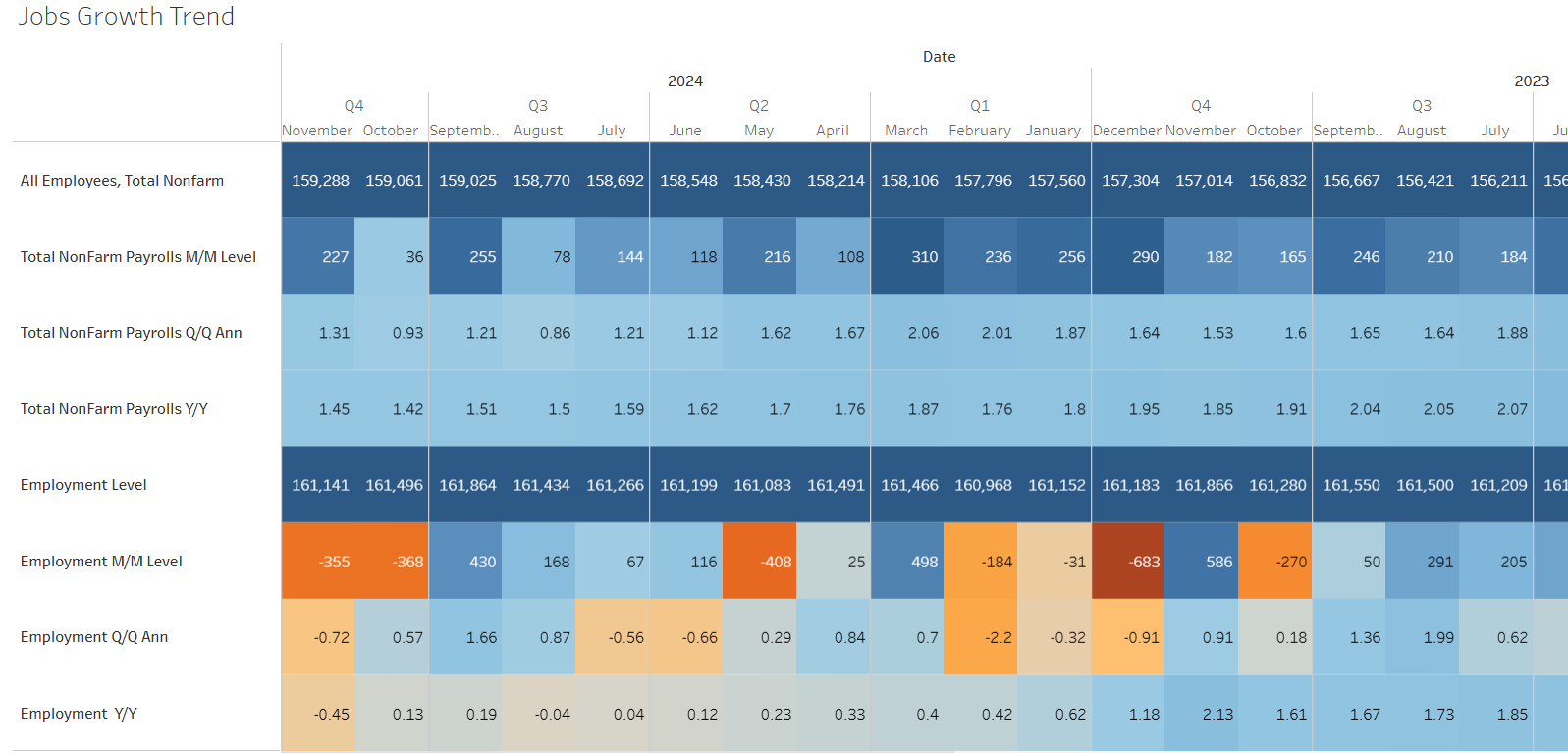

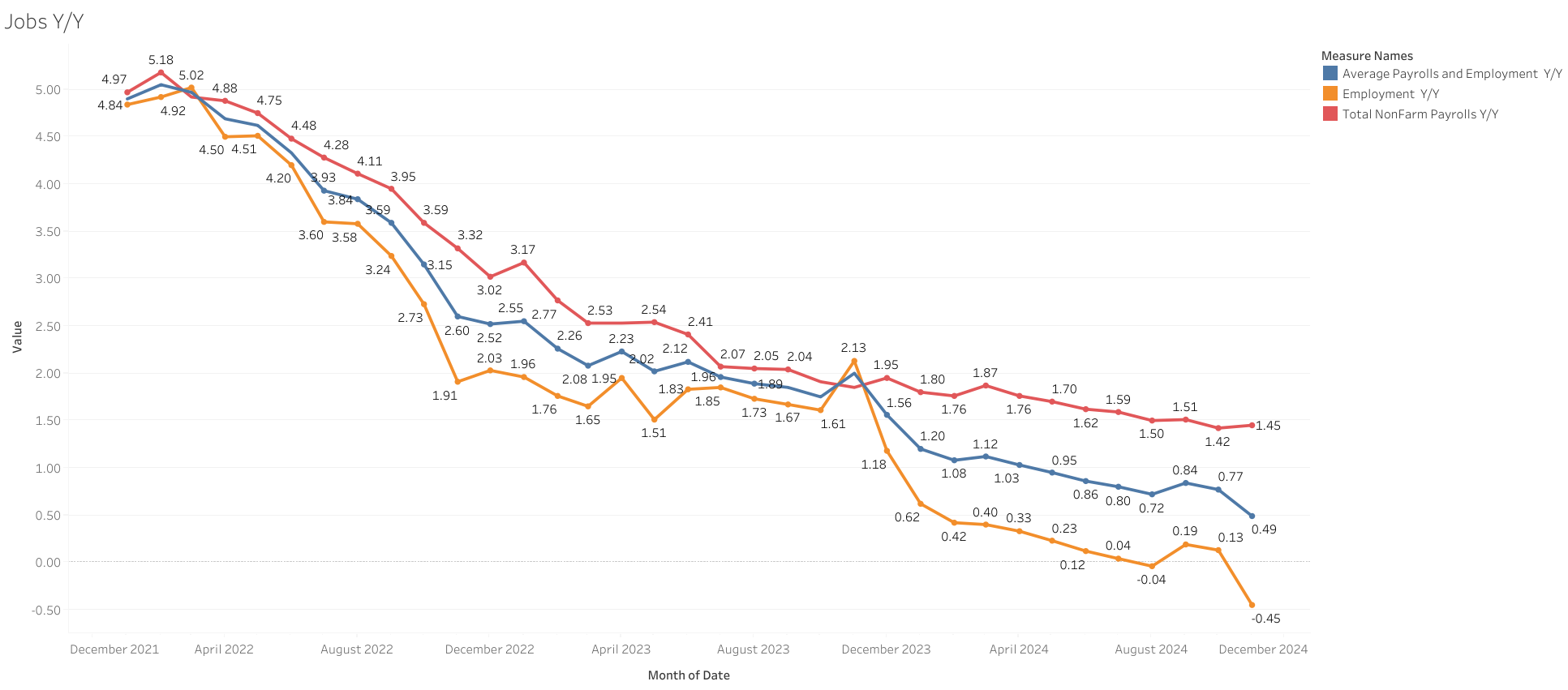

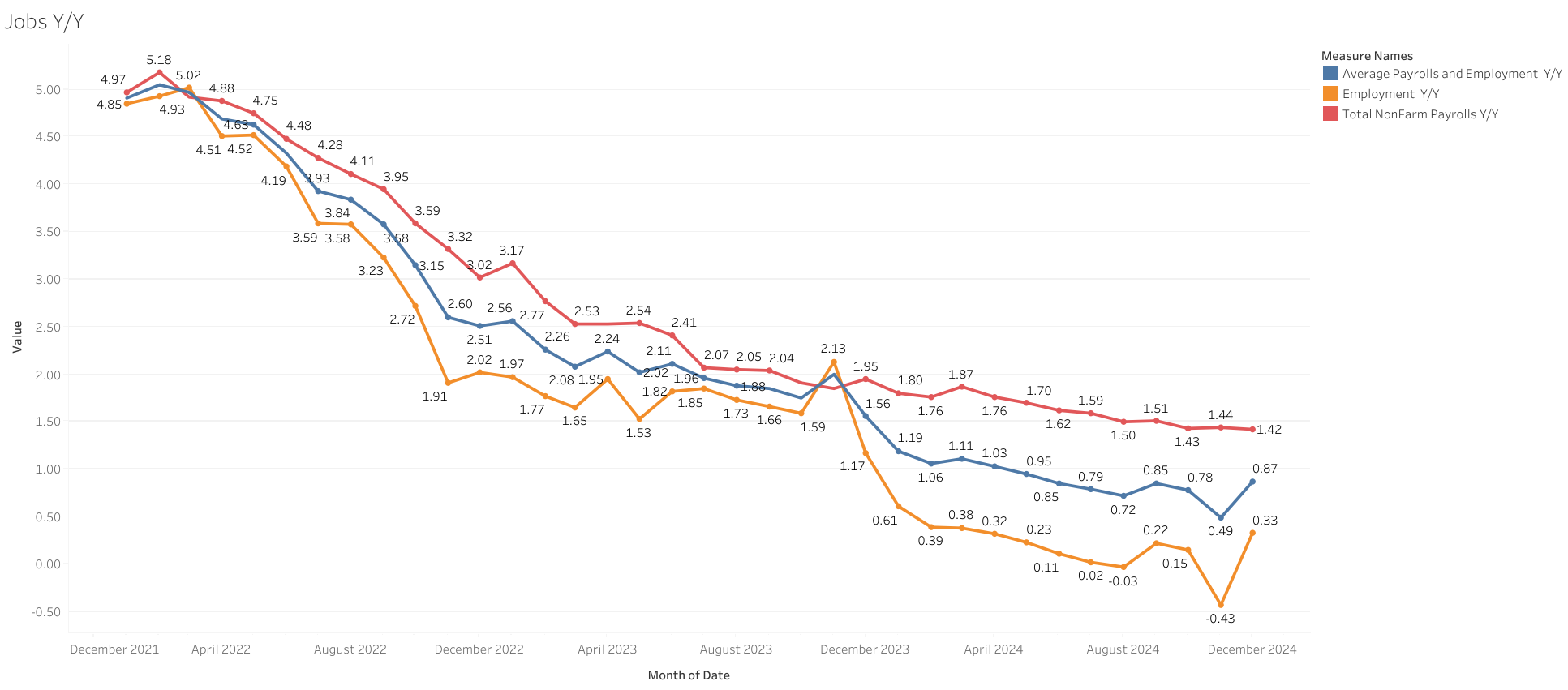

Despite strong jobs added in December, the growth rate continued to decline. The 6-month average with a slight uptick, but still no clear reversal.

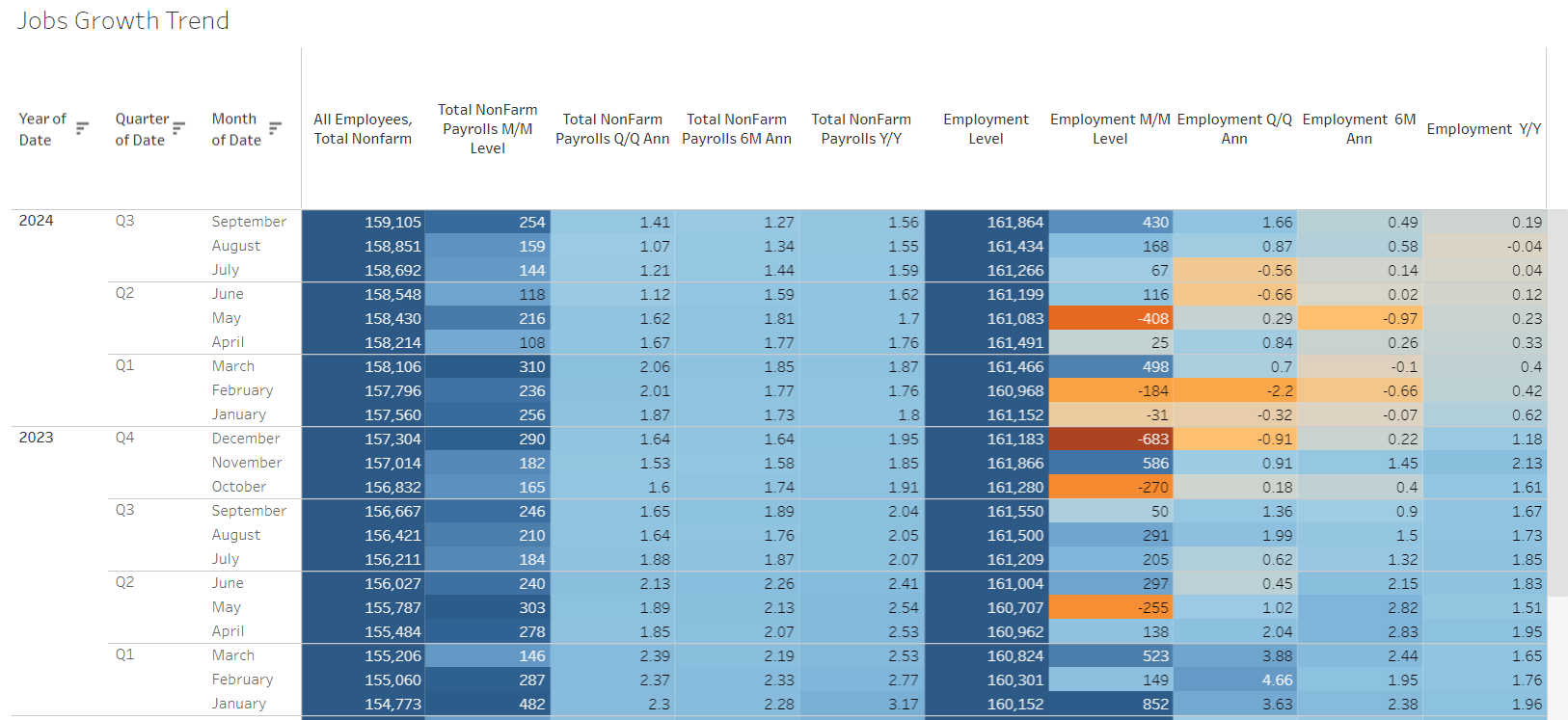

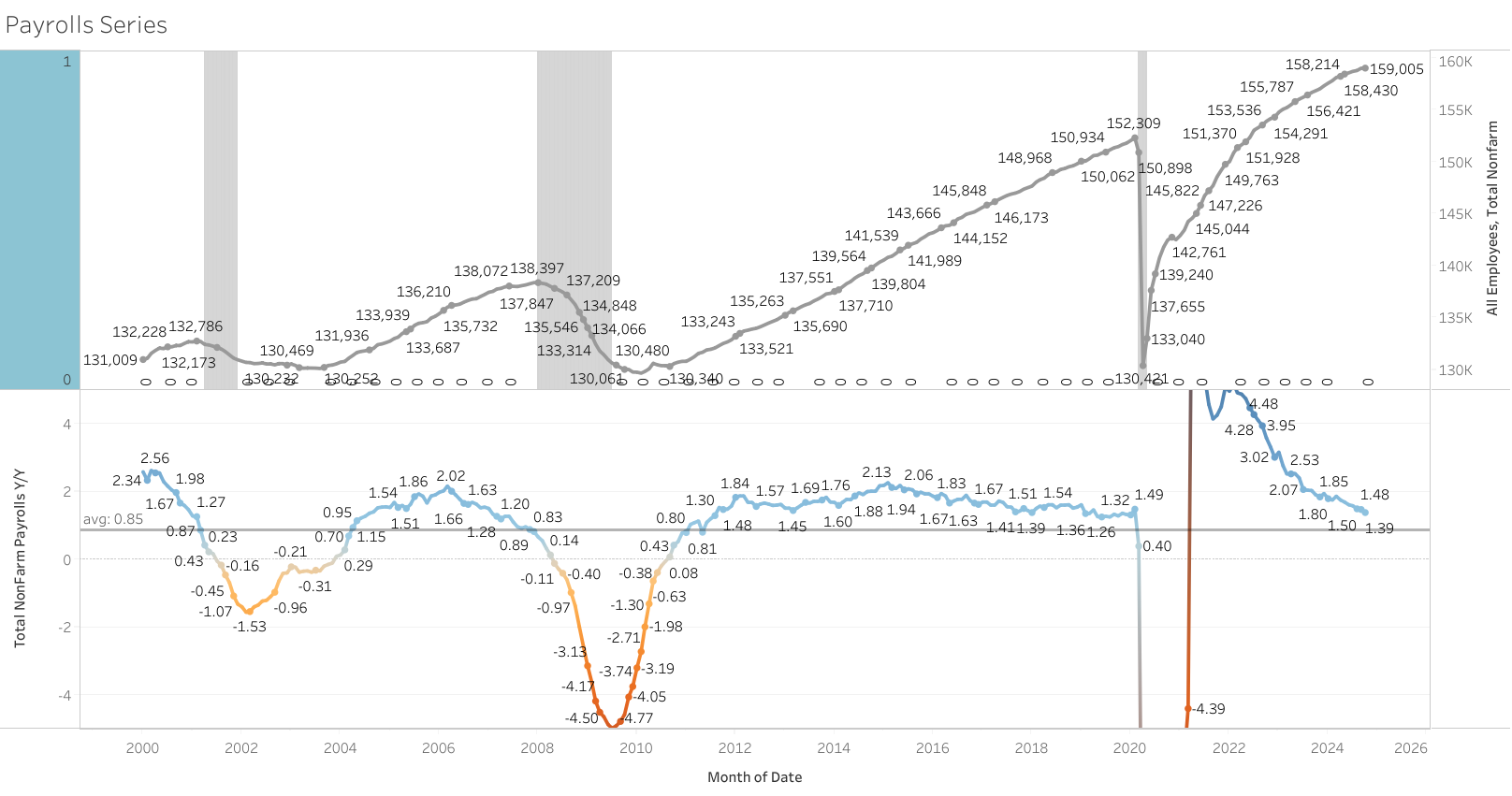

Payroll growth currently at 1.42% y/y vs 1.44% in November (2% historical average, 1.3% average since 2010). Payrolls added 2.2 M in 2024 vs 3 M in 2023 (-26%)

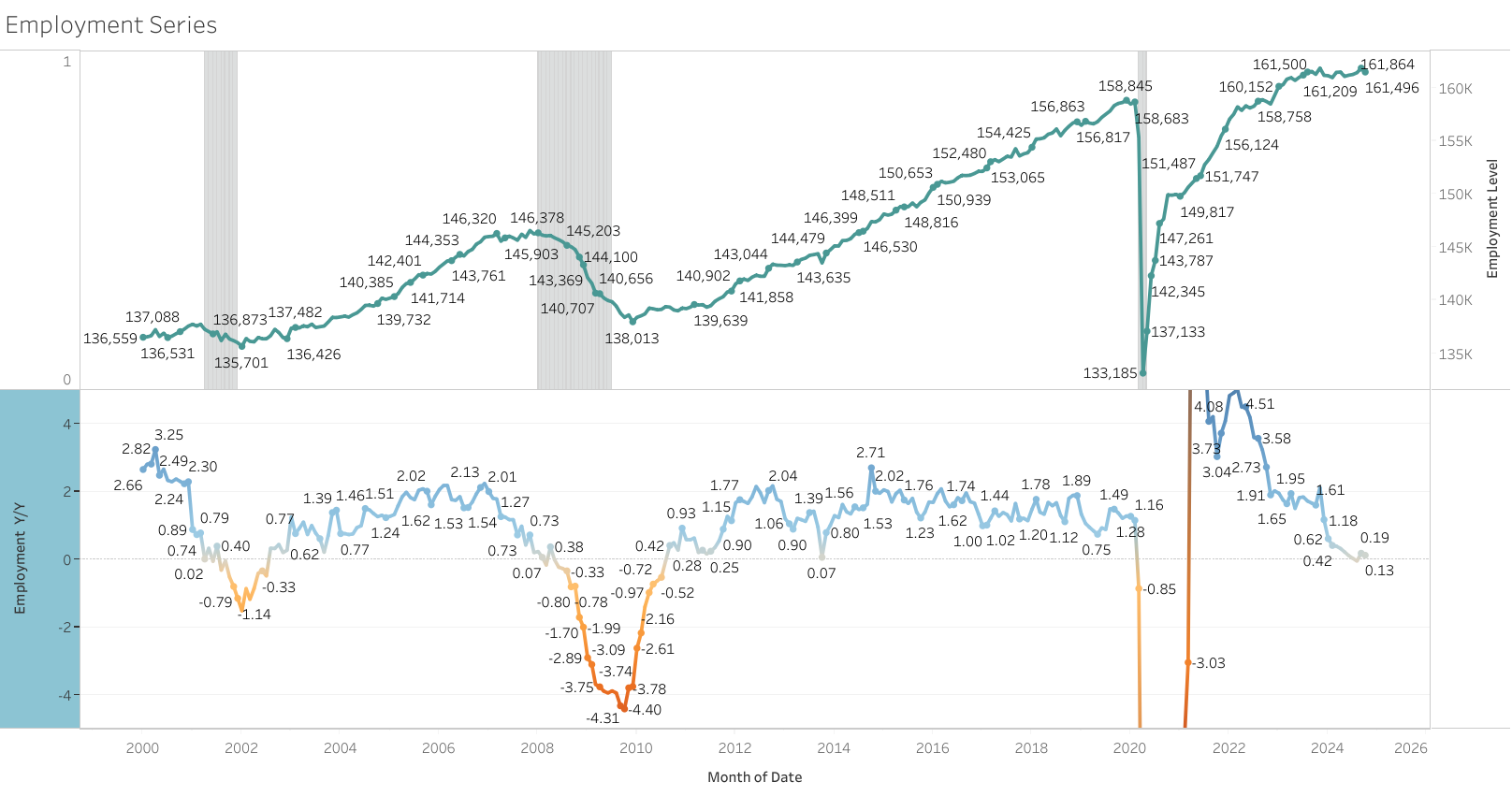

Employment growth at 0.3% y/y vs -0.43% in November (1.3% historical average, 1% average since 2010). Employment increase by 537k in 2024 vs 1.9 M in 2023. (-71%)

Despite weaker-than-expected payroll figures, the labor market appears to remain on a solid trajectory, showing a slight pickup toward the end of the year after softer readings in mid-2024.

This report is unlikely to alter the Federal Reserve’s inclination to pause rate moves in upcoming meetings, especially in light of recent improvements and wage gains. Still, the bias remains skewed toward cuts, and based on current data, the likelihood of another hike seems low for the time being.

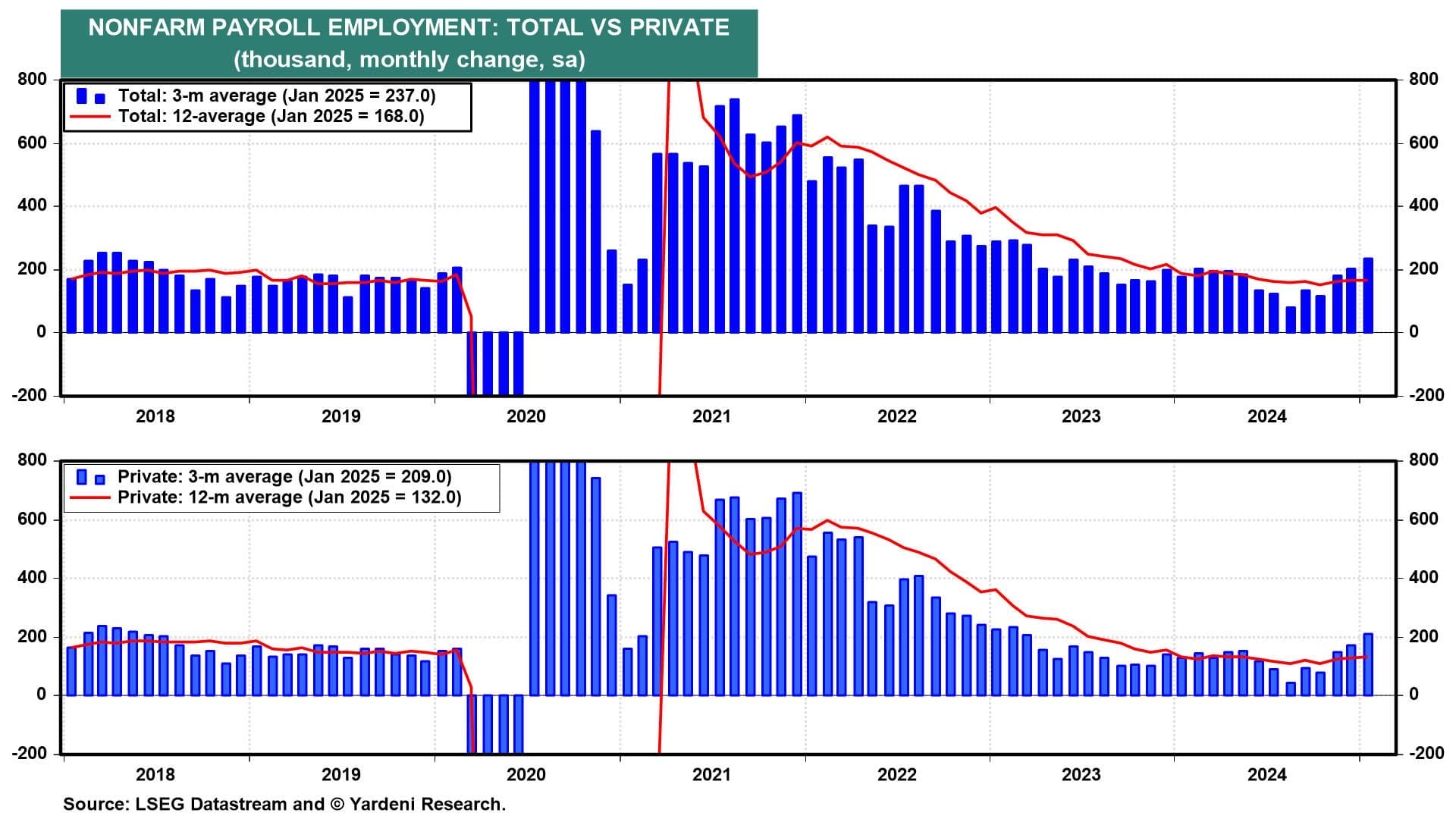

Upward revisions pull up the three-month average to +237K & rising, which signal the acceleration at the end of the year

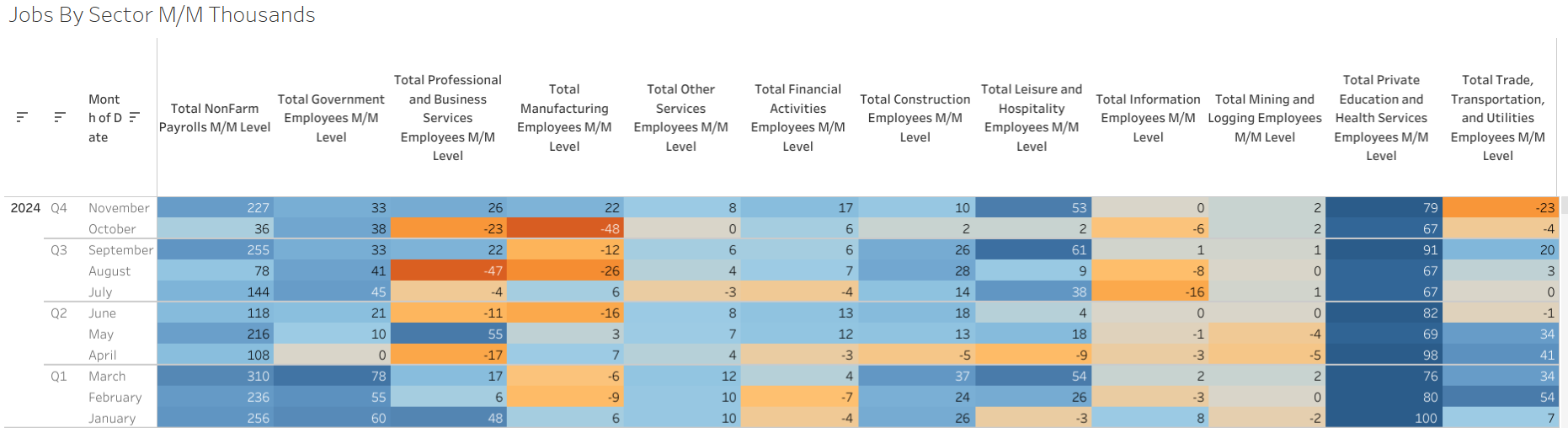

The services sector is the major contributor, and the good-producing sector still struggling in line with the weaker manufacturing sector.

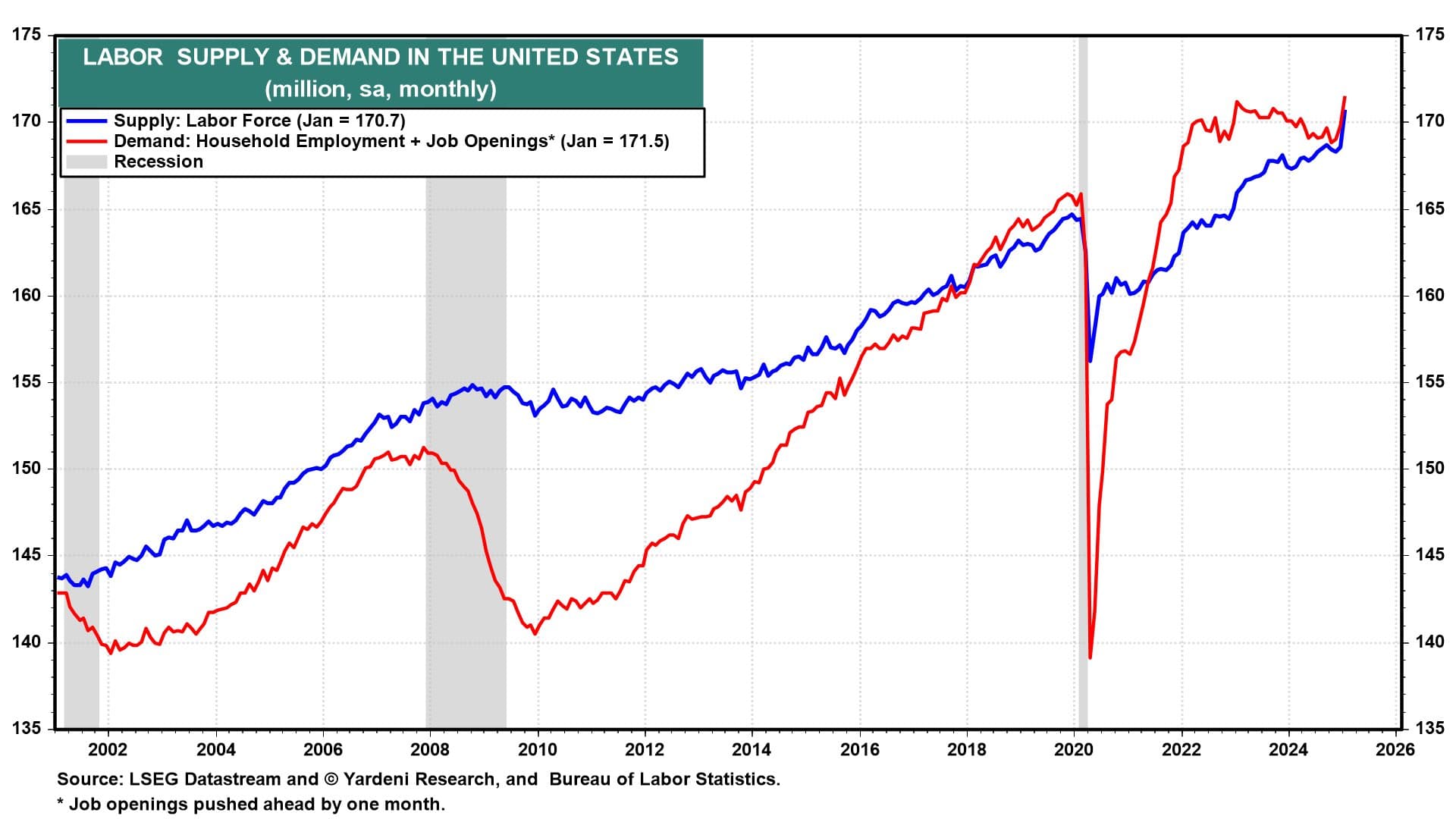

Supply and demand dynamics still in good balance after these week’s reports.

It is still worth pointing out that hiring is still low, which means the market is currently more vulnerable to any layoff shock.

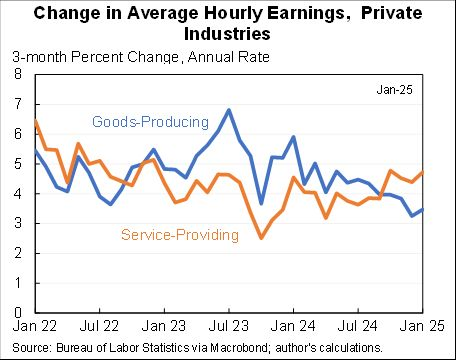

Wage growth has been picking up in service industries and slowing down in manufacturing/goods industries. This is the part of the report the FED is unlikely to like.

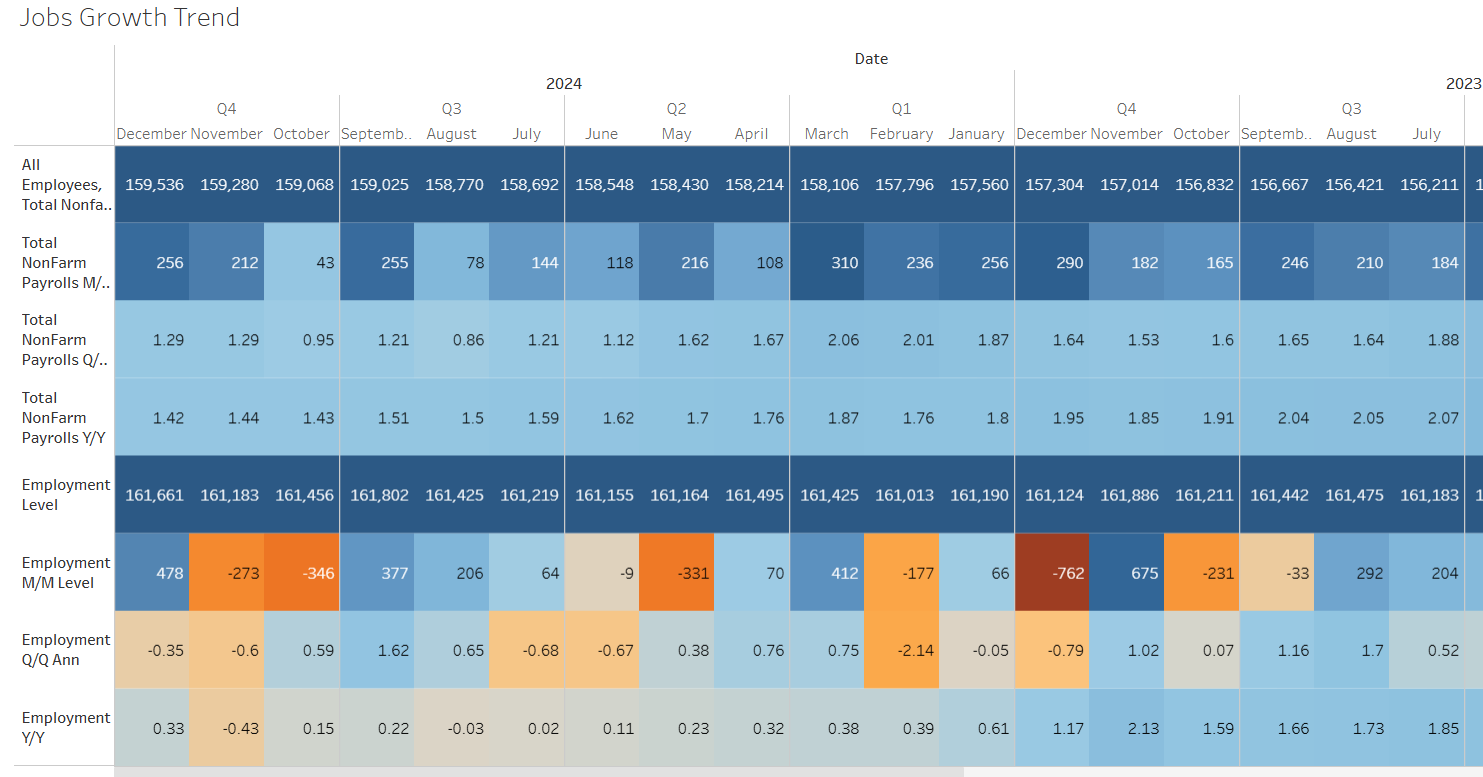

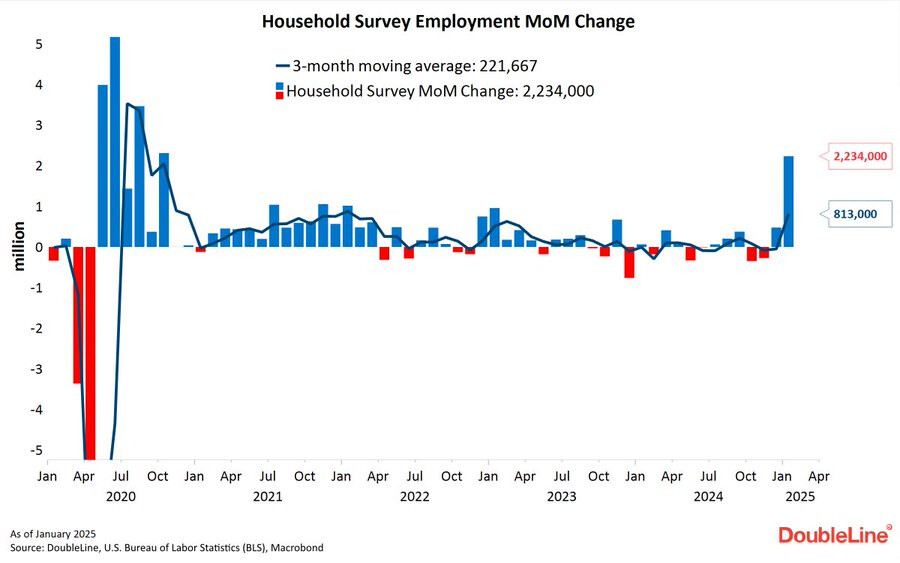

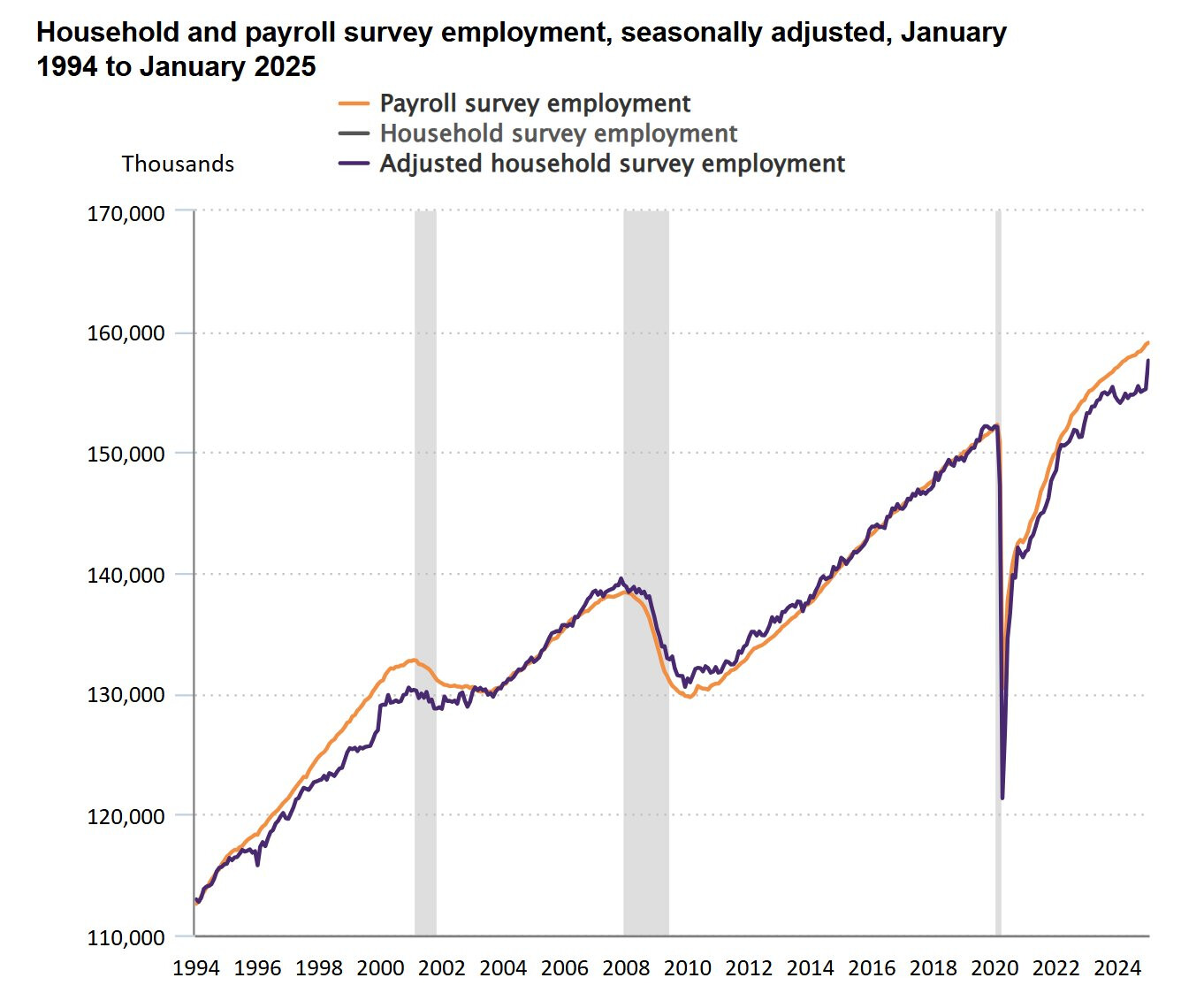

Employment level got positively revised (+2M) due to population adjustments and payrolls negatively revised (-600k). Closing the gap between payrolls and employment that lasted for months.

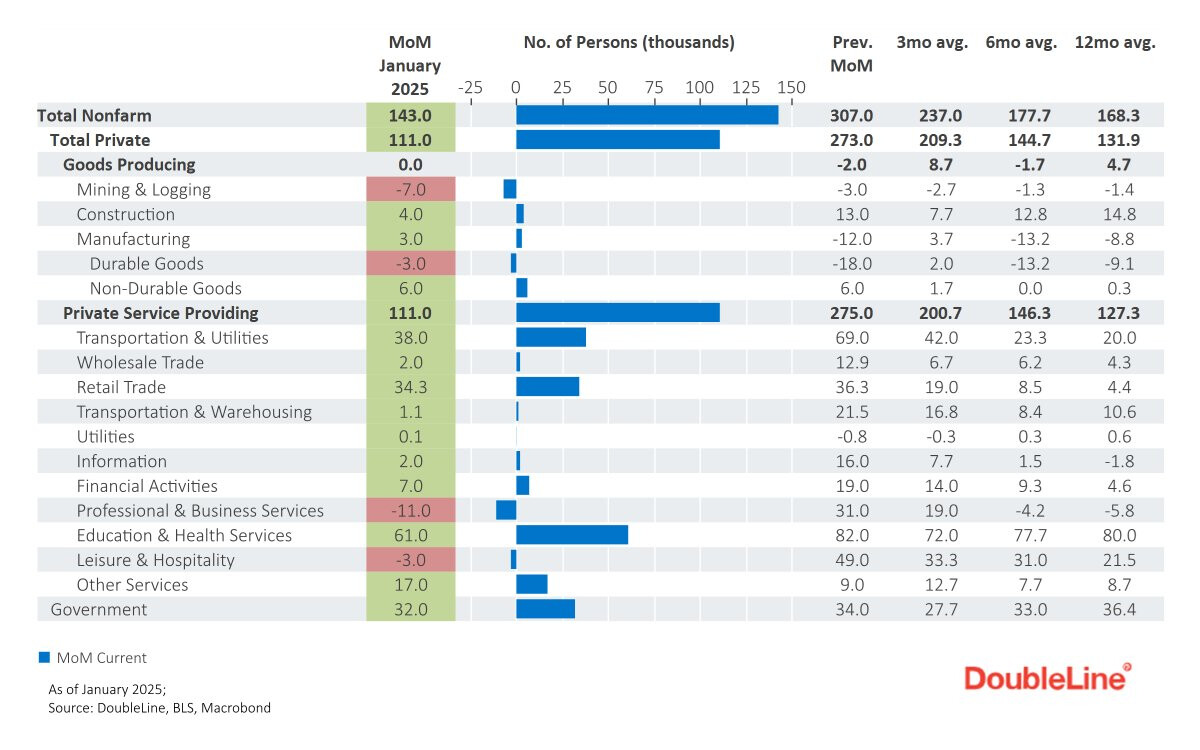

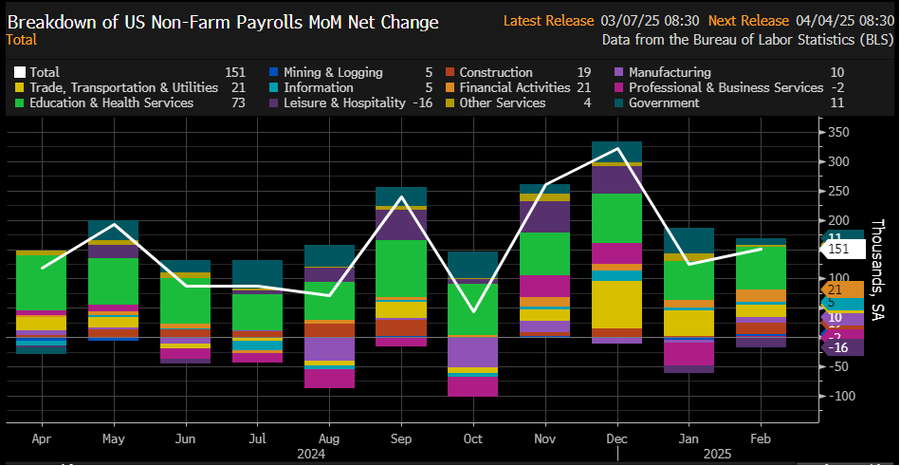

Labor Report February 2025: Soft but mostly in line payrolls and unemployment numbers

US Labor Feb Nonfarm Payrolls +151K vs Consensus +160K

US Feb Unemployment Rate 4.1% vs Consensus 4%

US Feb Average Hourly Earnings +0.28% (as expected), or +$0.1 to $35.93, year over year at +4.02%.

US Feb Private Sector Payrolls +140K and Government Payrolls +11K

US Feb Average Workweek Unchanged at 34.1 Hours (expected to increase due to January bad weather)

The aggregate payrolls index ( total # of jobs * hourly earnings * workweek, a measure of wage income) rose by 0.4% m/m and 4.6% y/y

US Jan Payrolls Revised to +125K; Dec Revised to +323K

Assessment: A soft or slowing employment report, but still decebt with no sign yet of any imminent recession as some feared. However, there are some concerns in the underlying data that could send some warning signals for the next months:

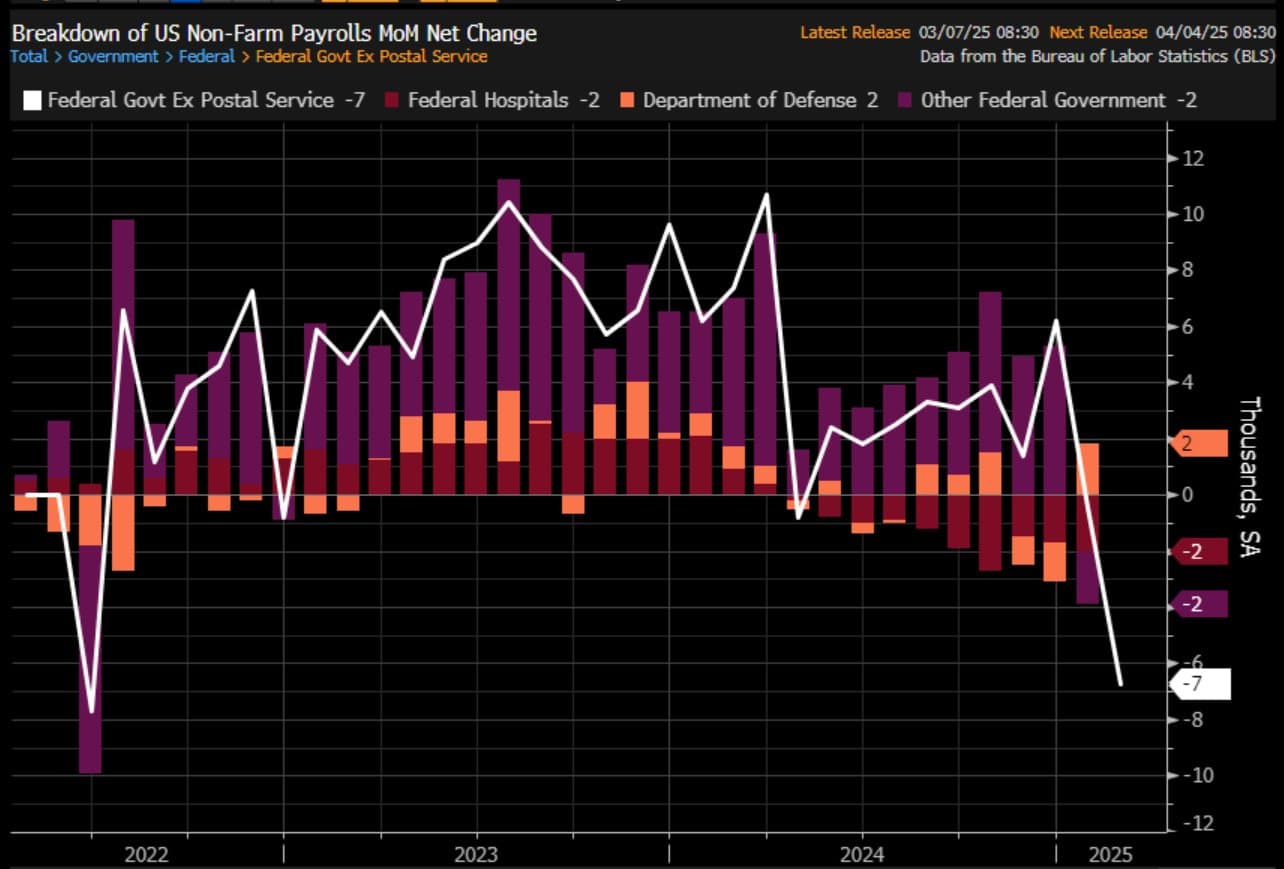

Doge job cuts are starting to appear modestly in the data, but the biggest impact is expected to come in the coming months.Beyond outright layoffs, a key concern is that government-driven job creation, one of the economy’s primary employment engines in recently, could slow, further dampening labor market momentum.

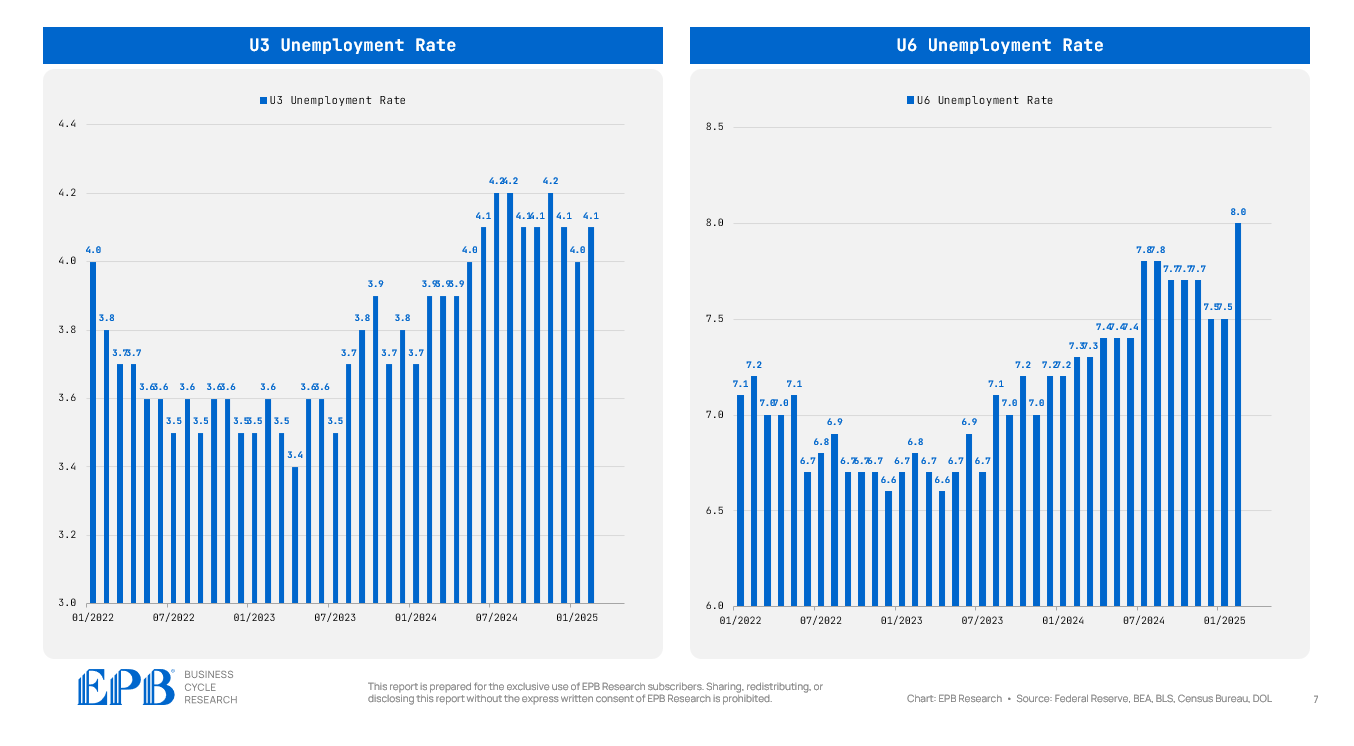

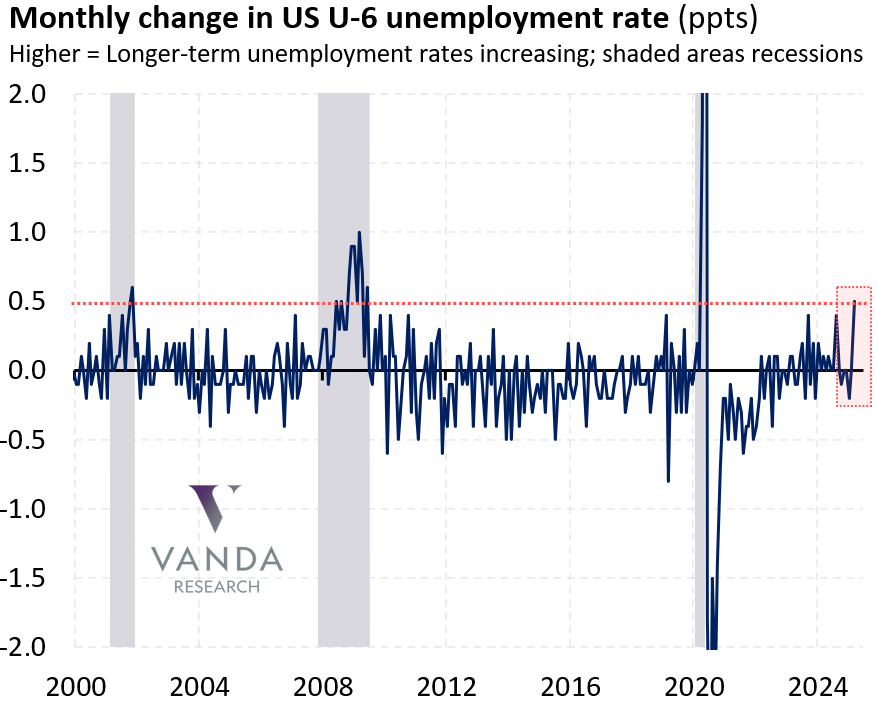

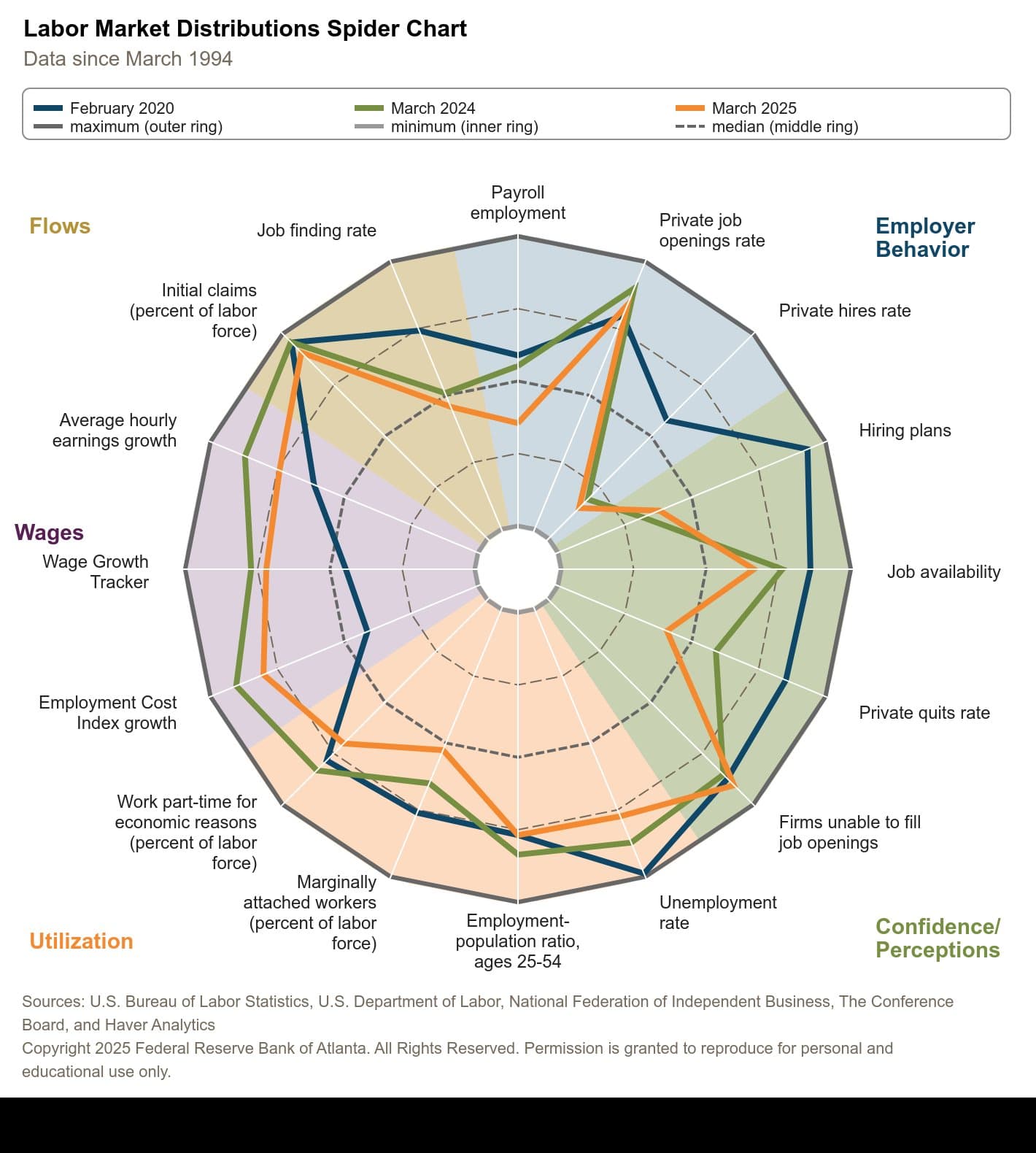

The underemployment rate climbed 0.5 percentage points in February to 8%, the highest level since October 2021. Such an increase is unusual and may signal that slack is building in the labor market, and upcoming challenges for the broader unemployment rate could come.

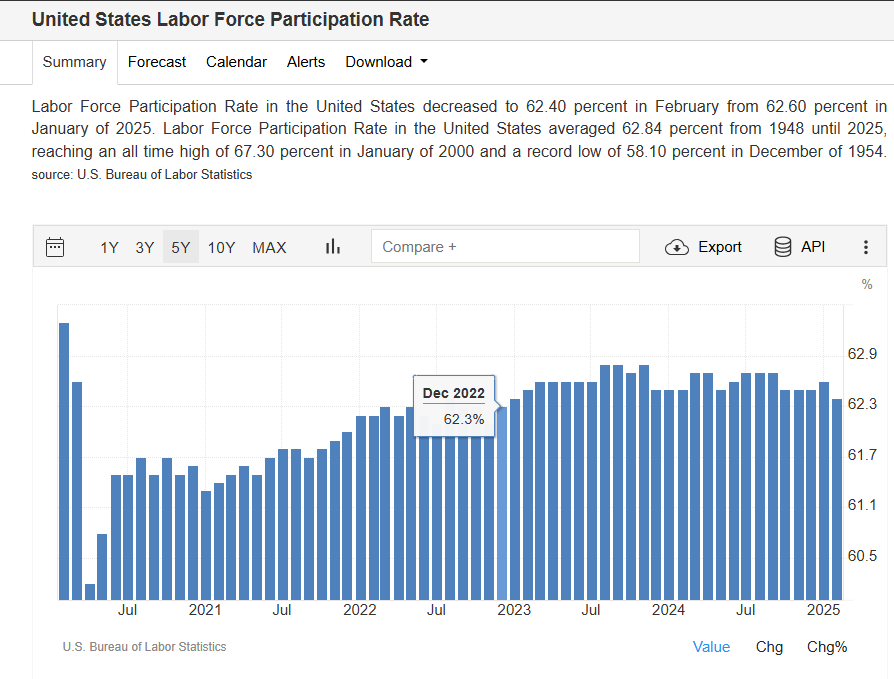

The participation rate has fallen to its lowest level since Dec 2022. A shrinking workforce reduces economic growth. Immigration policies may continue to play a key role in shaping these trends, potentially further constraining labor supply

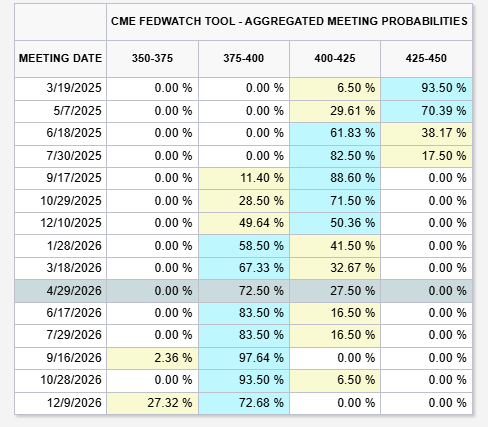

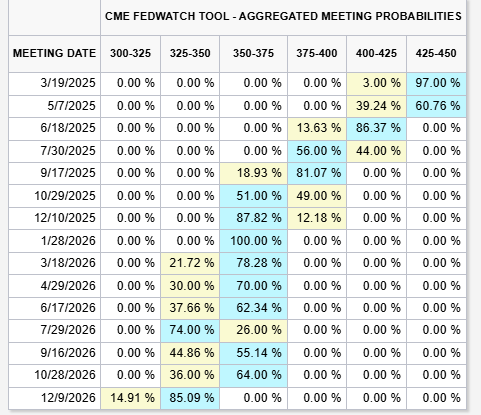

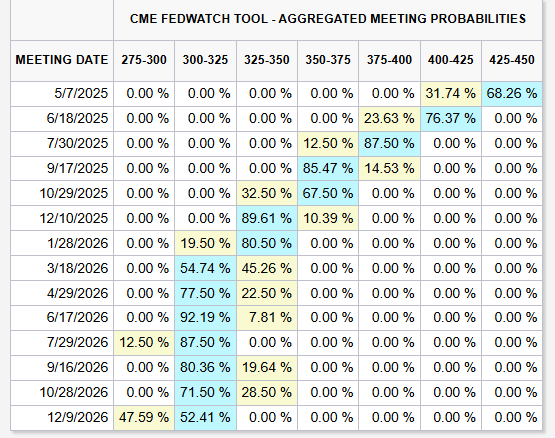

The market pricing now has about 3 rate cuts in 2025, from only 1 at the beginning of the year. The fact there are also risks to inflation, IMO will not allow the FED to cut in aggressively, as I think they would otherwise.

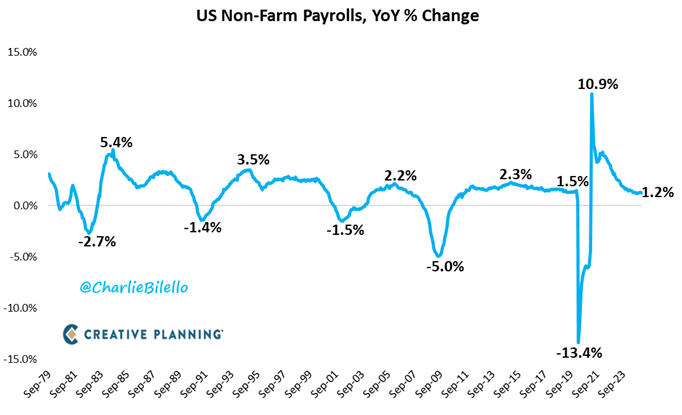

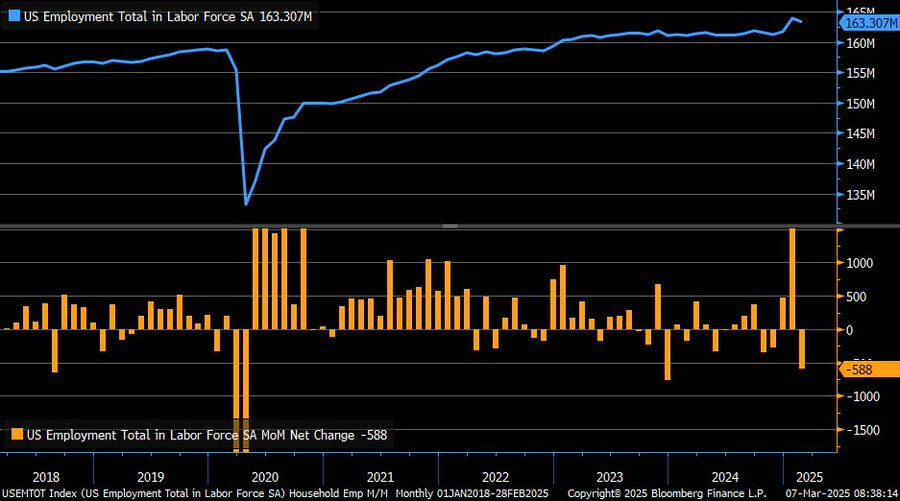

Total jobs in the US increased 1.2% over the last year, the slowest growth rate since March 2021. Household employment fell by 588k in February, the largest drop since December 2023

The unemployment rate ticked up modestly to 4.1% in February, but the underemployment rate (which includes persons marginally attached to the labor force and part-time workers for economic reasons) rose to 8%, up 0.5% from January., and the highest since 2021.

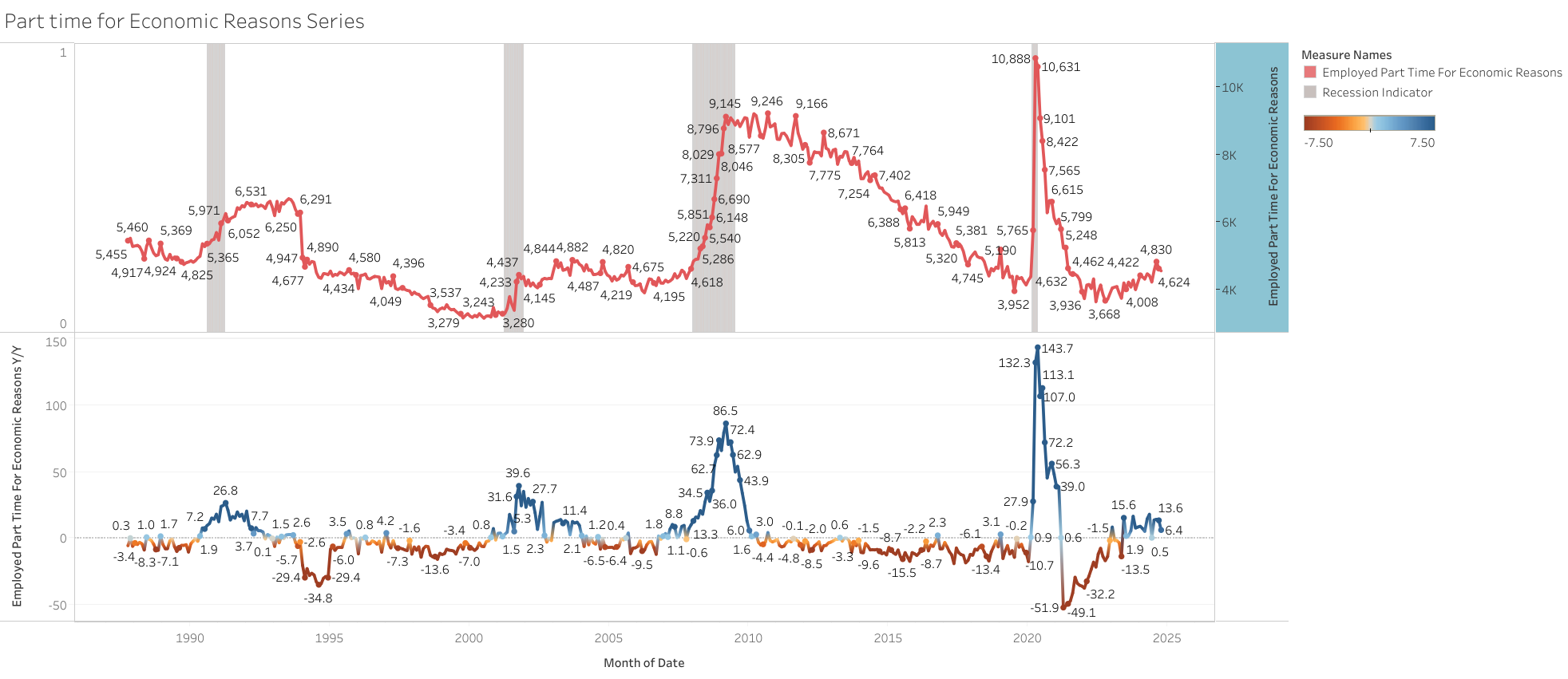

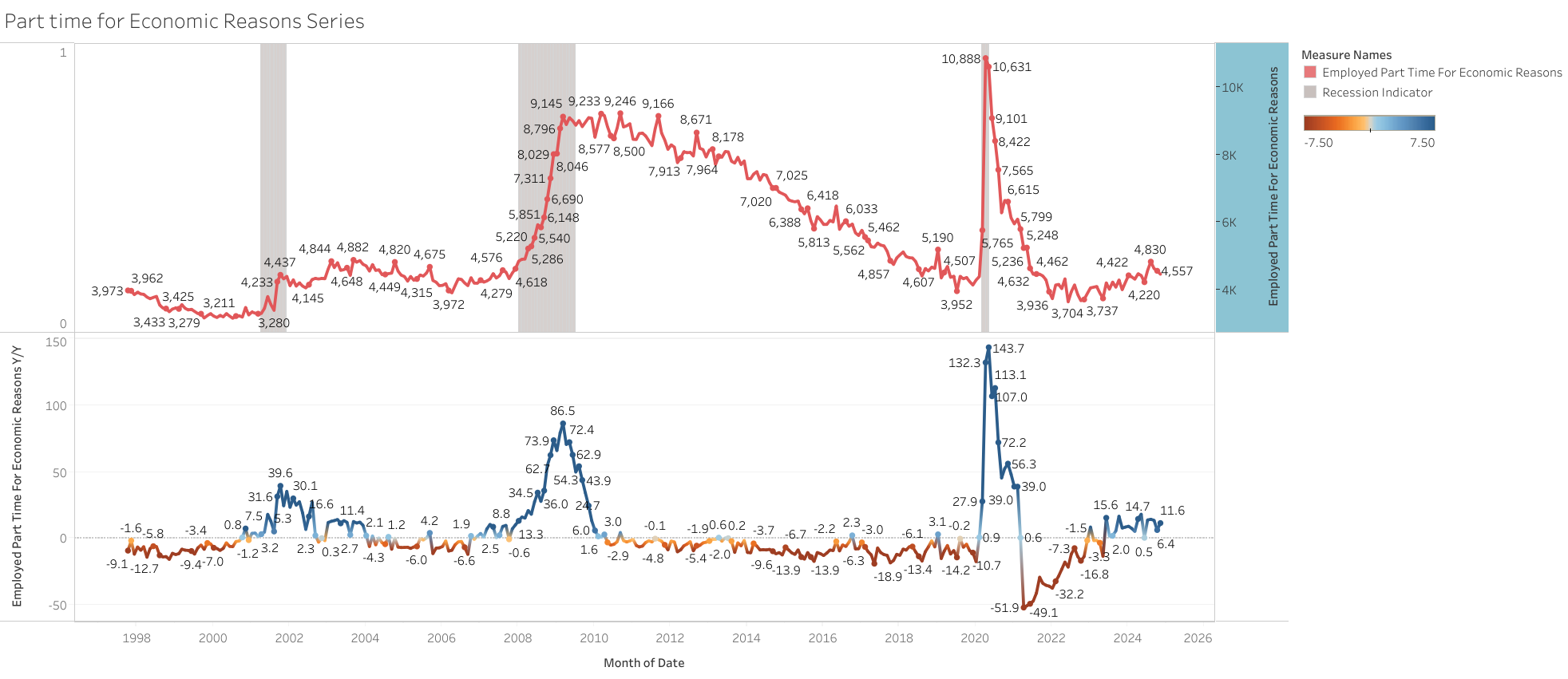

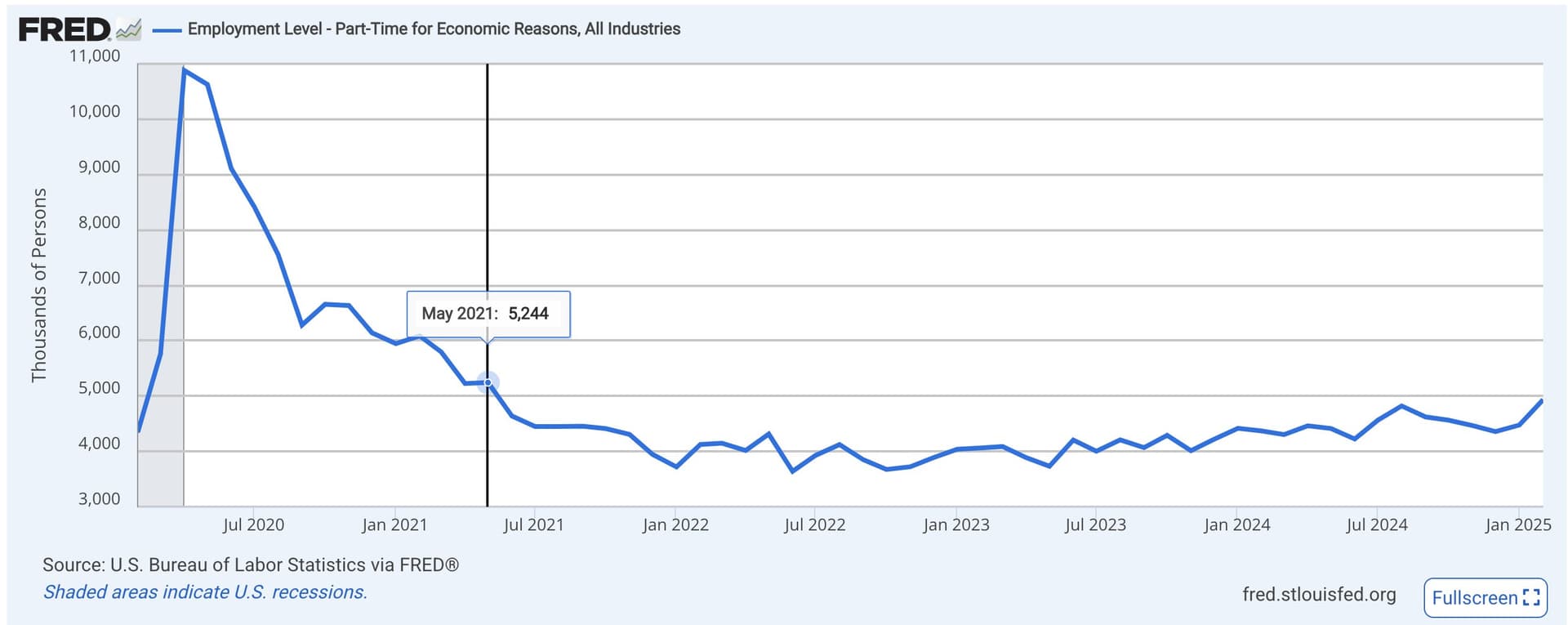

Pople working part-time for “economic reasons” (meaning they could not find a full-time job) jumped by +460,000 to 4.9 million. It’s currently at the highest level since May 2021.

Education and Health Services continue to drive job gains. Leisure and Hospitality has now lost jobs in back to back months.

Federal government employment fell by 10K, but this was more than offset by a 20K rise in local government employment and a 1K increase in state government jobs.

Fed gov’t agencies have a deadline today to submit plans for large-scale layoffs and budget cuts, which could affect 250,000 employees.

Agencies must also need to submit consolidation plans by April 14, including office closures or relocations. Economists warn the layoffs could weaken the Washington, D.C. metro economy and slow national job growth.

Notable cuts include:

IRS: Up to 50,000 jobs (half of its workforce).

Department of Defense:76,000 civilian staff (8% of its workforce).

Veterans Affairs:80,000 jobs to return to pre-pandemic levels.

Social Security Administration: Potentially 30,000 jobs (half of its staff).

Assessment:250,000 would only increased unemployed by 3.5% (currently 7.3 M), and unemployment to 4.28%. So the directs effects in the economy would not be as significant yet. What could be more impact is the pace of job growth for some months (probably at or below 100k), while government make the adjustments.

The market is expecting 135k payrolls, and for unemployment to remain unchanged at 4.1%

My current best guest is that anything below 100k payrolls, and an increased in unemployment will not be taken positive by the market, since would be taken as signs of initial slowdown by markets.

Non-farm payrolls came in much better than expected, unemployment rate ticked up to 4.2%

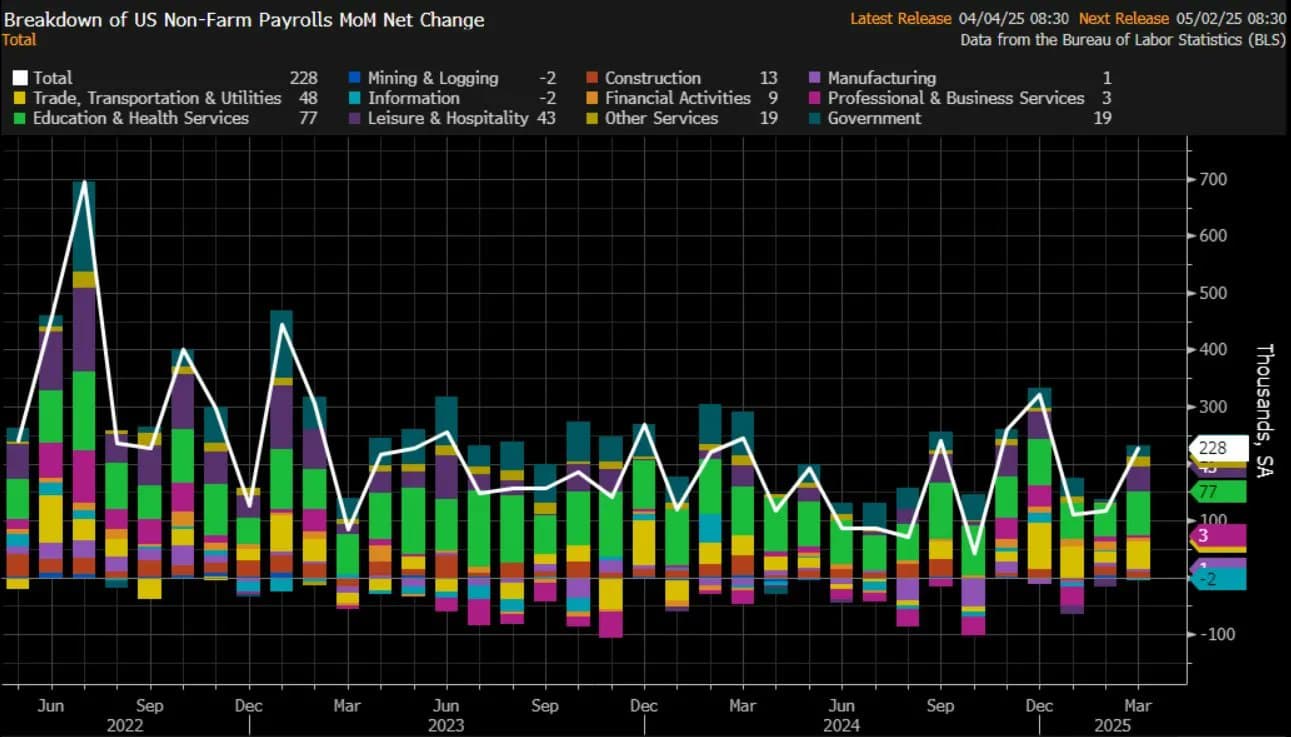

Nonfarm payrolls increased 228,000 in March, exceeding 135,000 estimate and up from the 117,000 in February (revised downwards from 151,000).

Unemployment rate came in at 4.2%, against expectations to stay unchanged at 4.1%.

Average hourly earnings rose 0.3% on the month, in line with the estimates but up from 0.2% in February (revised downwards from 0.3%).

On a yearly basis, average hourly earnings rose 3.8%, below 3.9% estimate and lower than 4.0% in February.

Labor force participation rate rose to 62.5% from 62.4%.

Growth in non-farm payrolls was driven by healthcare (+58,000), social assistance (+28,000), retail (+28,000), and transportation and warehousing (+23,000).

This is an overall good report, but I agree with some commentary from analyst that the good data as this point is not that relevant since the headwinds to the economy are greater down the road.

What is good is that the economy is at least starting from a relatively good place before tariffs impact, but at the same thing this kind of still robust data will put a high bar to the effect to be able to be proactive on possible weakness later on in the year.

The market is currently convinced the FED will provide at least 3-4 cuts this year. Which I have already stated I am not confident still this will be the case indeed.

The unemployment rate went up to 4.15% from 4.14%, the number of unemployed people only went up by 31k.

The underemployment rate went down from 8.0% to 7.9%, since part-time for economic reasons went down by 157k

The economy has added slightly more than 180,000 jobs per month over the past six months, on average. Payrolls growth is at 1.2% y/y (which is below pre-pandemic levels growth), still some signs of slowing already.

Civilian labor force went up by 232k, growing at 1.6% y/y, while employment its only growing at 1.3% y/y

Nonfarm payrolls increased by 177,000 in April, exceeding 138,000 estimate while unemployment rate was steady at 4.2%

Nonfarm payrolls rose 177,000 in April, exceeding 138,000 estimate but below 185,000 in February (revised downwards from 228,000).

Unemployment rate was steady at 4.2%, in line with the estimate.

Average hourly earnings rose 0.2% on the month, against expectations to stay steady at 0.3%.

On a yearly basis, average hourly earnings grew 3.8%, below 3.9% estimate.

Labor force participation rate rose to 62.6% from 62.5% in March.

The average monthly gain so far this year is 144,000, below last year’s 168,000 average but still above the 105,000 breakeven rate estimate- the total needed to absorb new entrants into the labor force.