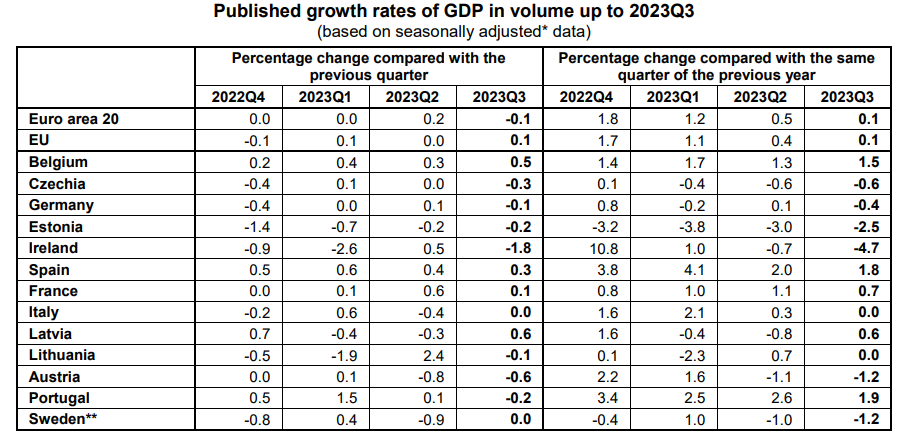

Euro zone economic growth was weaker than expected in the third quarter, a flash estimate showed on Tuesday, with gross domestic product contracting slightly quarter-on-quarter and the year-on-year growth rate slowing sharply.

The European Union’s statistics office Eurostat said GDP in the 20 countries sharing the euro fell 0.1% quarter-on-quarter in the July-September period for a 0.1% year-on-year rise. Economists polled by Reuters had expected a 0.0% quarterly growth and a 0.2% year-on-year gain.

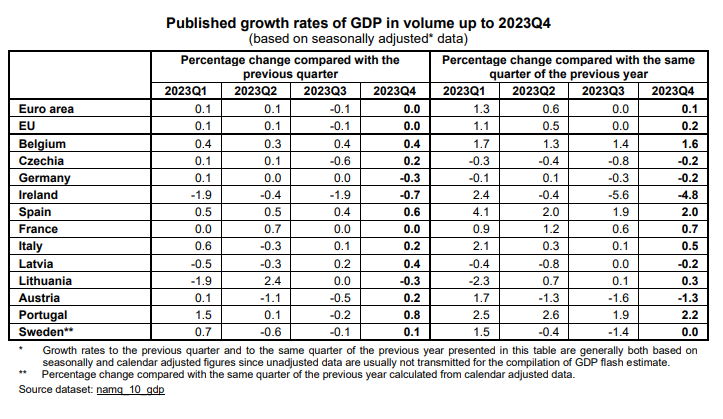

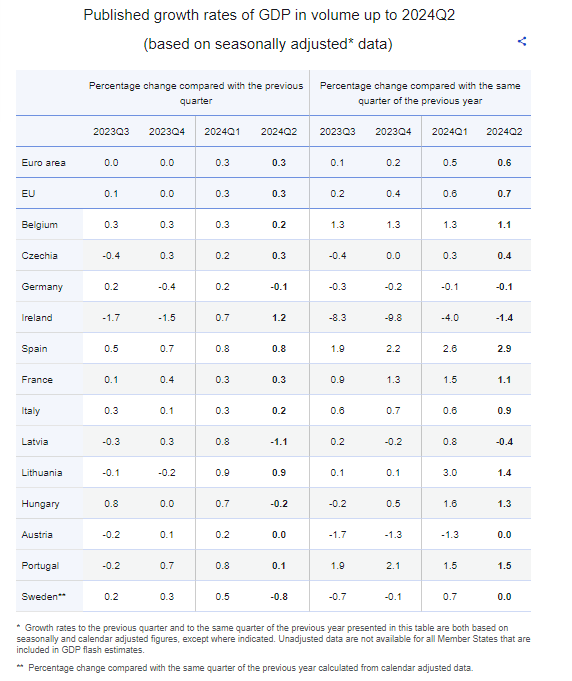

In the fourth quarter of 2023, seasonally adjusted GDP remained stable in both the euro area and the EU.

In the third quarter of 2023, GDP had declined by 0.1% in both zones.

According to a first estimation of annual growth for 2023, based on seasonally and calendar adjusted quarterly data, GDP increased by 0.5% in both the euro area and the EU

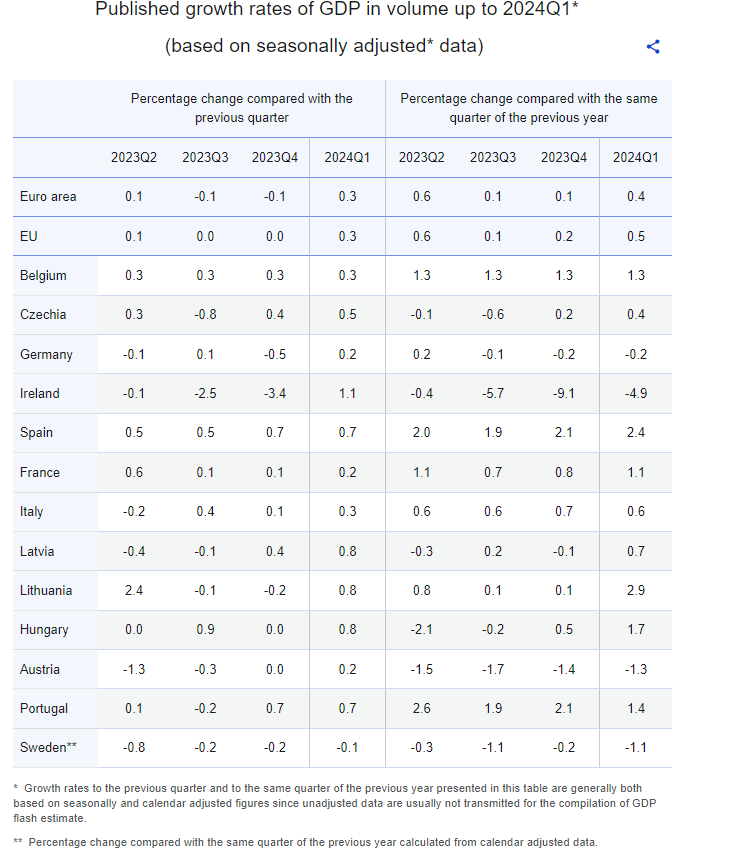

In Q1 2024, GDP increased by 0.3% (1.2% ann) in both the euro area and the EU, compared with the previous quarter. Better than the 0.1% that was expected.

GDP is on a small recovery currently, along with what PMIs have been pointing.

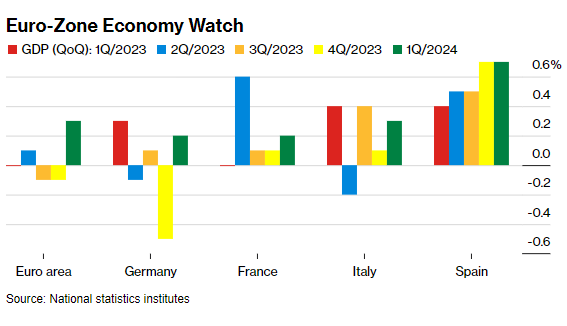

After shrinking in the latter half of 2023, the first quarter’s expansion came as Germany, France, Italy and Spain all exceeded analyst expectations.

Compared with the same quarter of the previous year, seasonally adjusted GDP increased by 0.4% in the euro area and by 0.5% in the EU in the first quarter of 2024, after +0.1% in the euro area and +0.2% in the EU in the previous quarter.

The ECB forecasts a recovery as inflation abates, household incomes rebound and foreign demand strengthens, predicting growth of 0.6% in 2024 and 1.5% in 2025.

Eurozone GDP is expected to be slightly better in 2024 and 2025, but still, not a huge surge in growth is expected.

Growth is also expected to be slightly lower than expected in October 2023 since the economic recovery has been weak and slow.

The IMF base case (falling inflation with slow positive growth) is cemented on rather optimistic assumptions in my opinion:

Labor markets need to be neither too strong nor too weak

Consumption has to pick up

Investment also needs to increase as financial conditions ease.

The recent normalization of supply conditions, which allowed inflation

to cool with little impact on labor markets has to remain intact

Combination of still-tight monetary policy and gradual fiscal consolidation has to ensure that the path of inflation stays within central banks’ comfort zones

Inflation will fall toward targets even as demand recovers. This configuration rests on inflation expectations remaining anchored, and that the recovery in labor productivity—after a years-long plateau and muted profit growth will mitigate the effects of rising wages on inflation

The soft landing could be undone by a failure of consumption—and in turn investment—to pick up, as weak sentiment lingers.

Persistently high inflation, requiring tighter monetary policy stances that ultimately lead to lower growth, is the main risk for many CESEE economies.

A possible escalation of Russia’s war in Ukraine or a broadening of the conflict in Middle East could raise uncertainty and affect supply chains and commodity prices.

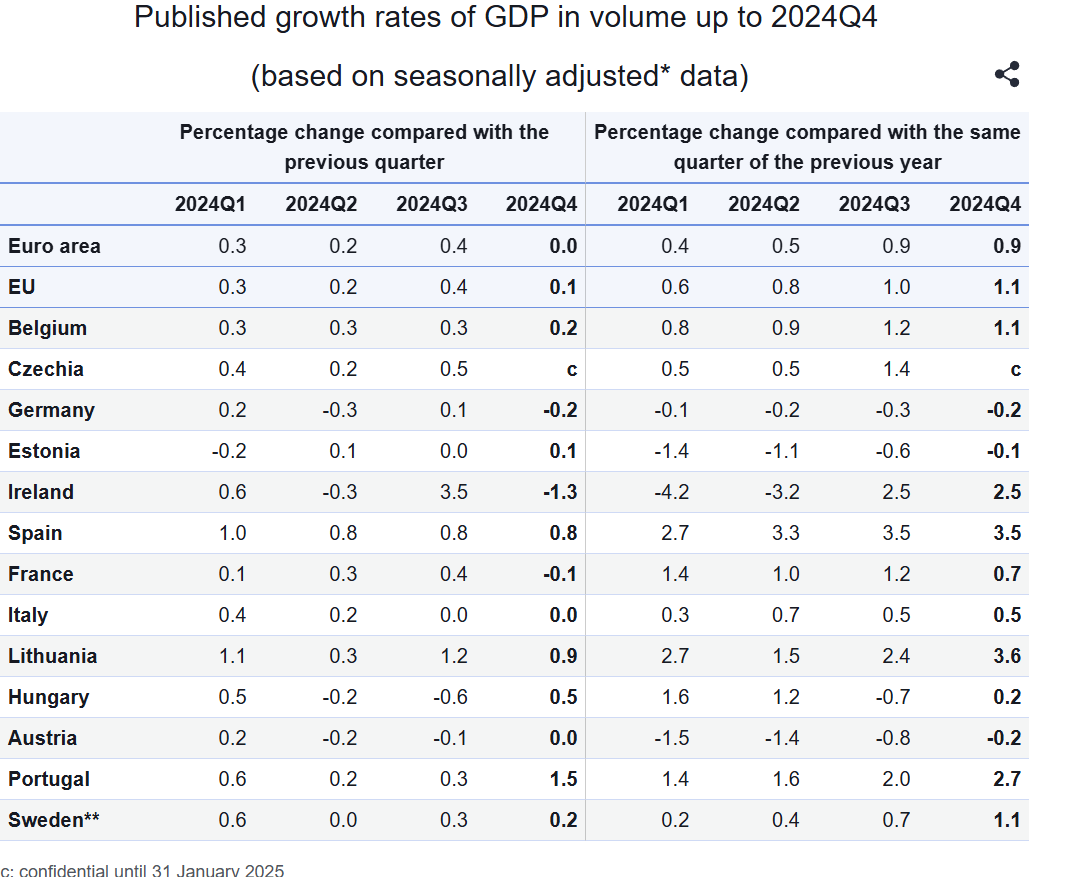

“The fourth quarter performance (for Germany) is admittedly modest yet still the best quarterly performance in the last three years,” ING economist Carsten Brzeski said.