Sixt Q2 2025: Rebound in Used Car Prices and Resilient Rental Demand Support Bullish Outlook, Justifying a Buy Rating

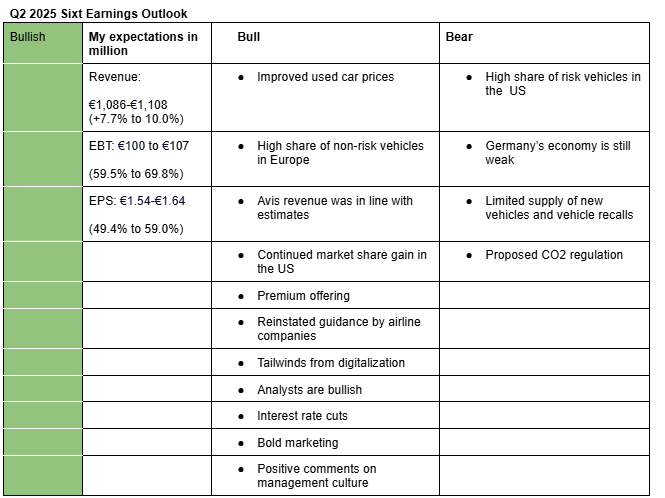

I am bullish on Sixt’s Q2 2025 earnings. My estimates (valuation model) take into account improved used car prices, positive commentary from Avis and other industry players, continued U.S. expansion, the premium nature of Sixt’s offerings, its fleet composition, tailwinds from digitalization, bold marketing, favorable remarks on management culture, and a potential revenue headwind from the macro slowdown in Germany. Here is a description of my bullish and bearish points.

Bullish factors

- Improved used car prices: Auto1 Group data indicates that used car prices in Europe rose about 3% year over year during the quarter. This marks the first increase in two years. Likewise, Manheim data indicates that used car prices in the U.S. increased by approximately 5% year over year during the quarter. A decline in residual values has been one of the main factors behind the drop in Sixt’s earnings over the past two years.

- Avis revenue was in line with estimates: Avis’s Q2 2025 revenue was flat y/y at $3.039 billion, in line with analysts estimate of $3.022 billion. In the earnings call, management said demand for car rentals is strong, especially in the leisure segment ( Business to Business (B2B) and Business to Partner (B2P) sales channels account for 72% of Sixt’s revenue-page 17). It also pointed out that pricing is stabilizing. Its International Revenue per Day (RPD) rose 7% y/y while Americas Revenue per Day (RPD) was down 2% y/y. Commentary from the Sunny Cars CEO on pricing and demand during the quarter was also positive.

- High share of non-risk vehicles in Europe: Sixt’s share of non-risk vehicles in Europe is now almost 100% compared to at the end of 2023 when it was 87%. This means that Sixt is now in a better position to dispose off its used vehicles in Europe than in Q2 2024.

- Continued market share gain in the US: Sixt continues to make strides in the US. For instance, the new Delta Air Lines SkyMiles partnership, the first of its kind in United States keeps the U.S. growth story in focus. Also, Avis flagged Sixt during its Q2 2025 earnings call, saying it stepped up competition this year.

- Premium offering: Around 50% of Sixt’s fleet are composed of premium vehicles. Sixt’s premium positioning commands 30%-40% higher average revenue per unit compared to Avis and Hertz, according to S&P Global. This premium focus provides resilience during periods of macro slowdown.

- Reinstated guidance by airline companies: Both Delta Air Lines and United Airlines see upside to their 2025 earnings due to stabilizing demand.

- Tailwinds from digitalization: Sixt’s digitalization efforts are expected to enhance operational efficiency, resulting in cost savings for the company and time savings for customers. For example, its Car Gate inspection technology is designed to materially reduce repair costs. Data from Hertz indicate that similar AI-based inspection systems lead to three times more billable damage than the industry average. Similarly, Sixt’s in-house tech division, which consists of 731 employees and has deployed over 100,000 software updates in the past year, gives it a competitive edge in the AI era. This technological capability could prove especially valuable in dynamic pricing, where personalized price offerings are emerging. Notably, there are reports that airline companies are testing AI-powered dynamic pricing models.

- Analysts are bullish: Jefferies, DZ Bank, Deutsche Bank and Warburg Research analysts expect Sixt to post solid results for Q2 2025.

- Interest rate cuts: The ECB’s key interest rate now stands at 2%, down from 3.75% in June 2025. This reduction should lower Sixt’s interest expenses over time, supporting earnings and freeing up capital for investment.

- Bold marketing: Sixt’s provocative political-themed advertising has long been central to its marketing success. While some feared this strategy might fade after Erich Sixt stepped down as CEO, the company has continued to launch bold campaigns that consistently draw public attention. Former CMO Tobias Seitz is said to have left the company after his creative freedom was curtailed. However, the continued strong performance of part of the marketing division helps ease concerns about Sixt’s management culture.

- Positive comments on management culture: Moritz interaction with a former Sixt employee who reported directly to Alexander Sixt was positive. In addition the CEO of a direct competitor to Sixt told

Moritz that Sixt is performing well when it comes to Software and has a good performance culture.

Bearish factors

- High share of risk vehicles in the US: At the end of 2024, Sixt’s share of vehicles not covered by repurchase agreements stood at 87%, up from 75% in 2023. This means that its depreciation of rental vehicles in North America may not fall significantly in 2025.

- Germany’s economy is still weak: Germany’s GDP shrank by 0.1% in Q2 2025, signaling continued weakness in one of Sixt’s largest markets.

- Limited supply of new vehicles: Avis stated in its Q2 2025 earnings call that tariffs are causing OEMs to delay vehicle production and deliveries, leading to postponements in its in-fleet schedule. Most vehicles in Sixt US fleet are imported. This may lead to higher maintenance costs, residual value risk, and margin pressure. Avis also flagged vehicle recalls during the quarter, which affects 4% of its US fleet and could affect vehicle supply in summer and 2026. It said that vehicles recalled cannot be sold.

- Proposed CO2 regulation: The EU Commission is drafting a regulation that would ban rental companies from purchasing internal combustion engine (ICE) vehicles starting in 2030. Although the likelihood of it passing is low, the surrounding uncertainty could weigh on the share price in the short term.

Here are analysts estimates for Q2 2025 and FY2025:

Q2 2025 analysts estimate for EBT: €107.8 million (+71.5%)

Q2 2025 analysts estimate for EPS: €1.63 (+58.14%)

Q2 2025 analysts estimate for revenue: €1,070 million (+6.2%)

2025 analysts estimate for EBT: €440.3 (+31.4%)

2025 analysts estimate for EPS: €6.74 (+30.23%)

2025 analysts estimate for revenue: €4,269 million(+6.7%)

Management guidance for 2025:

2025 revenue guidance: €4,202 to €4,402 (+5% to +10%)

2025 EBT guidance: €420.2 to €440.2 (+25.8% to 31.8%)