@moritz New update from Magna. Interesting that global ad spend growth declined a bit, but social was revised significantly higher than the previous forecast.

The weakness until now they are mostly attributing it to traditional media

Advertising spending slowed down to a halt in the first quarter of 2023 (+1.5% globally, flat in most Western markets) due to economic uncertainty and the lack of cyclical drivers.

The one from Dentsu. Interesting the point about the impact of inflation, its positive effect on revenues could decline as inflation does too

“The adjusted for 2023 points to continued growth, albeit adjusted marginally downwards from the 3.5% predicted in the December 2022 report, in the most part due to macroeconomic factors. Exploring behind the headlines, the report also shows growth driven by media price inflation rather than increased advertising volume, where advertising spend at constant prices is expected to decline slightly, with –0.6% reduction year on year”

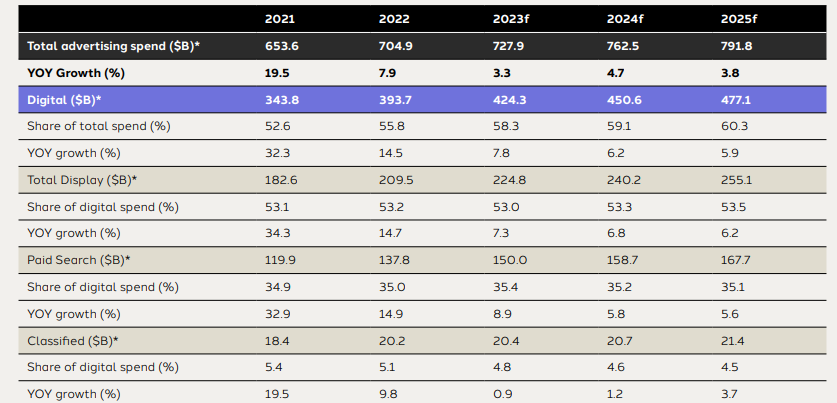

Global advertising spend expected to grow by 3.3% in 2023 with inflation driving increase to reach US$727.9 billion

Stronger growth ahead, with 2024 global advertising market now expected to increase by 4.7%, to reach US$762.5 billion, with a further 3.8% growth into 2025

Digital is projected to settle into almost consistent incremental growth for three years, to account for around $3 in every $5 spent in advertising worldwide.

Social spend is forecast to grow by a 12.8% three-year CAGR, driven by new platforms, social commerce, and the popularity of short-form video content across platforms such as TikTok and Instagram Reels

This is the Q3 update from Magna, however, they have only updated for US markets and not a global update. Significant improvement in the forecast for social media.

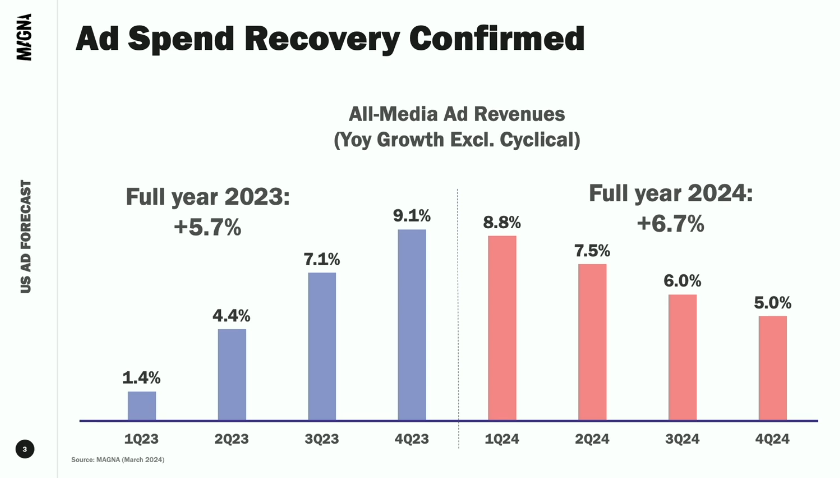

With the economic outlook improving and yoy comps becoming even easier, MAGNA maintains its growth forecast for the second half of the year. Total ad spend will grow by +7% to +8% in 3Q23 and 4Q23 (compared to +2.9% in first half) to bring full year growth to +5.2% (excluding cyclical), up from +4.2% in our previous update (June 2023).

Bofa projects that the global online ad industry will grow by 12% y/y in 2024 to $629 billion, aided by improving macro conditions, growing short form video monetization, and AI driven improvements in ad targeting and measurement.

“2023 was a year of recovery for the Online media sector after significant spending cutbacks and ATT changes weighed on growth in 2022,” BofA said.

However, the sector could face risks arising from Google eliminating Cookies and implementing Sandbox, rising competition from ecommerce platforms and streaming platforms.

These are the 2024 predictions for the companies we followed:

*Each one has its own clients, and methodology, and that’s why they numbers varied between each other.

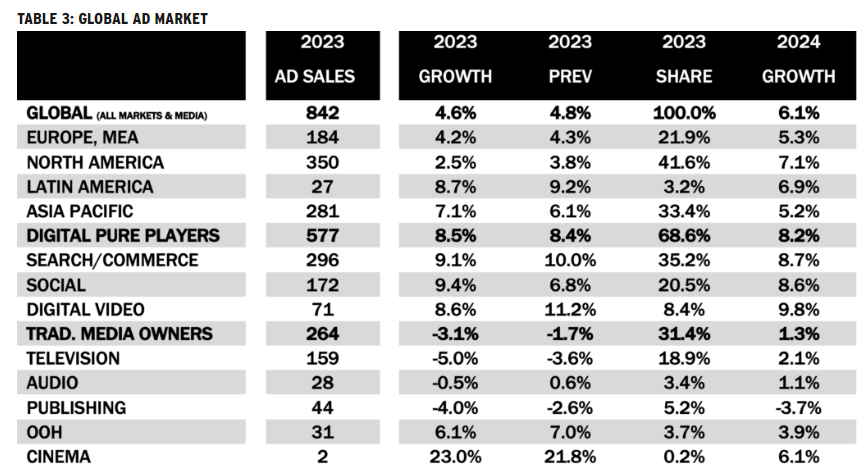

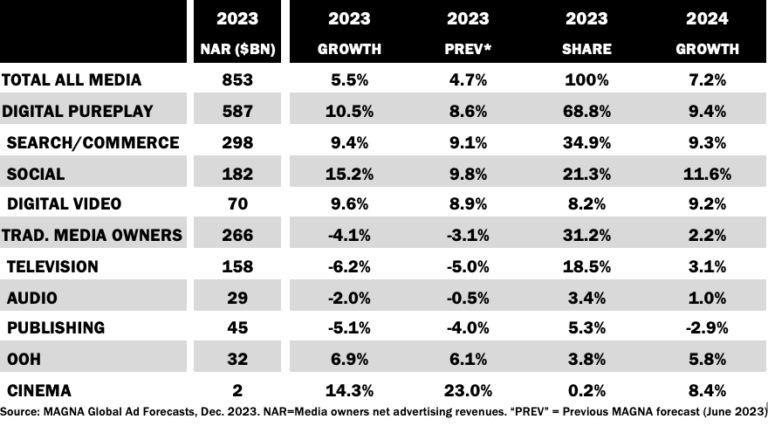

Global media owners net advertising revenues (NAR) reached $853 billion in 2023, +5.5% above the 2022 level.

In 2024, economic stabilization, lower inflation, digital innovation, and the return of major cyclical events (elections, international sports events) will drive ad spend +7.2% to $914 billion, +8.4% in the US. TMO ad revenues will recover by +2.2% while digital pure players ad sales will increase by +9.4%.

5.3% global advertising growth for 2023, which is above initial expectations given a healthier than expected Q3 for major digital advertisers.

Global adspend growth is expected at 4.8% in 2024, excluding U.S. political spending*, aided by events such as the Olympics as well as a combination of continued advertiser spending in support of their brands and the positive impact of Chinese brands fueling growth.

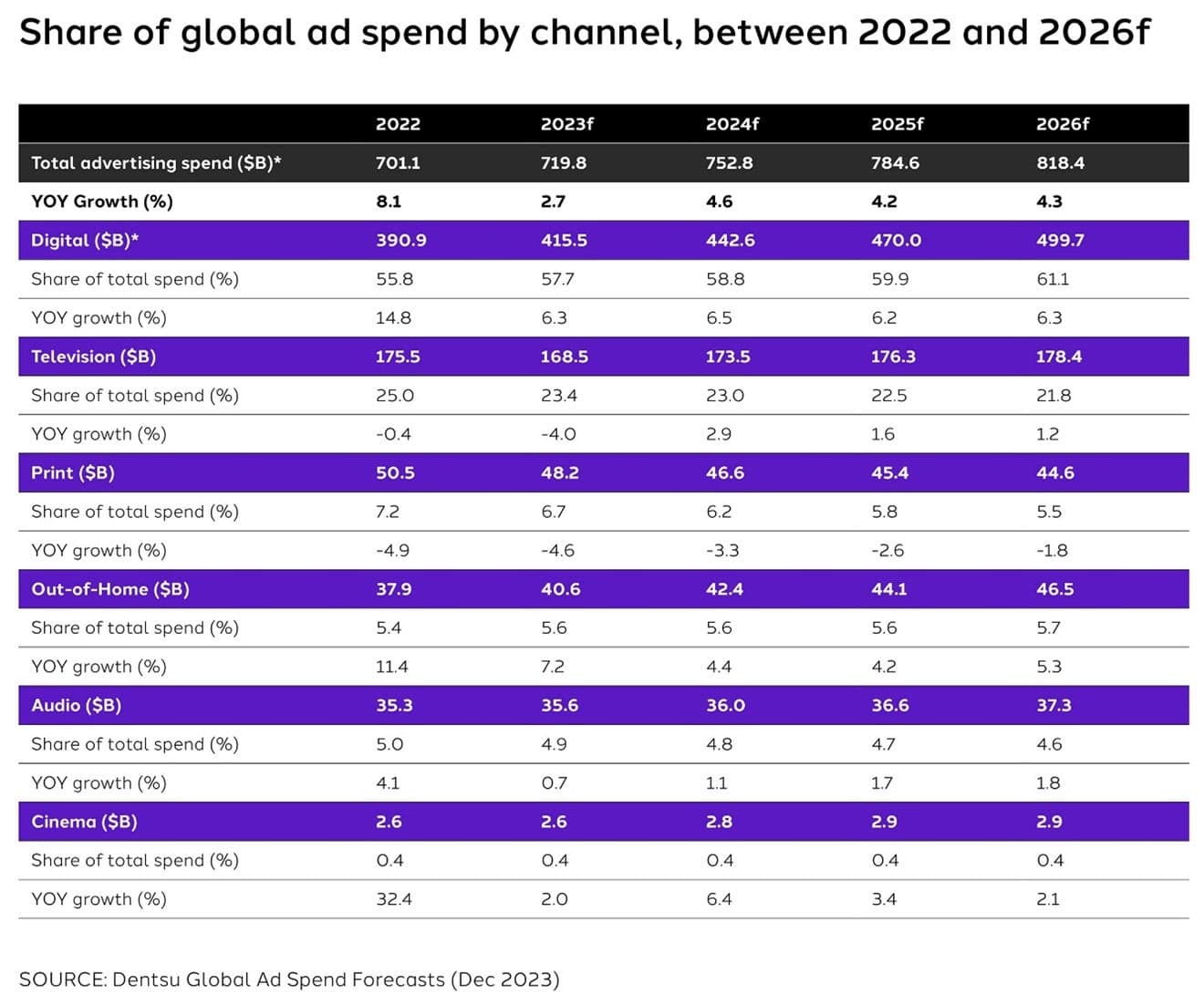

Advertising will expand by $33.0 billion in 2024 to reach $752.8 billion. This represents a 4.6% growth year-over-year for the ad industry – much faster than the pace seen in 2023 (+2.7% vs. 2022).

Global advertising spend at constant prices actually decreased by 0.7% in 2023.

In 2024, advertising spend is forecast to represent, on average, 0.75% of the gross domestic product (GDP) of the countries we track, which is consistent with the average annual ad spend/GDP indicator observed in the last 20 years (0.70%).

Digital It is forecast to grow by 6.9% in 2024, and by a 6.5% three-year CAGR to 2026.

In the digital space, retail media investments will accelerate the fastest with a 17.2% three-year CAGR, followed by paid social investments (12.3% three-year CAGR), especially in Asia-Pacific (21.0% three-year CAGR). Programmatic channels, that already account for more than 70% of digital ad spend, are also expected to continue growing by doubledigits (10.2% three-year CAGR).

According to Insider Intelligence, U.S. digital political ad spending will grow by 156% to $2.4 billion in 2024 from $951.8 million in 2020, with Meta and Google expected to see strong growth.

“Campaigns and issue advocacy groups are shifting more spending to digital channels in line with the wider changes to the contours of the ad market,” said Peter Newman, forecasting director at Insider Intelligence.

Founded in 1996, Insider Intelligence employees around 500 people worldwide and provides subscription-based market research on digital marketing, media, and commerce to more than 1,100 companies.

Baird post-holiday survey of 1,000 internet users points to “healthy increases” in engagement on short-form video apps such as TikTok and Instagram, continued trends in social media commerce and positive ad spending intent in 2024 especially in social media, video and search.

“We view our survey as most positive for Meta within our coverage,” Baid analysts wrote.

Time spent intent for TikTok increased by more than six points while that for Instagram gained more than three points, suggesting this is the third quarter in a row of increasing time spend for the two apps.

The analysts expect TikTok to continue taking ad share.

“We expect TikTok to continue taking share of ad budgets, corresponding to ramping time spent and user growth, along with new initiatives such as TikTok Shops,” they said.

TD Cowen raised their global digital advertising forecast by 5% on average from 2023 to 2028 due to better-than-expected digital advertising in 2023 and slightly better ad buyer sentiment.

They forecast global digital advertising market (ex-china) to grow by 11% y/y to $524 billion in 2024 driven by digital video and search.

They forecast U.S. Digital advertising market to rise by 11% y/y to $291 billion in 2024.

Digital share of total U.S. advertising market is expected to rise by 6% in the next two years.

The forecasts are based on its proprietary annual survey of 54 senior U.S. advertising ad buyers whose ad spend amounted to $25 billion in December 2023.

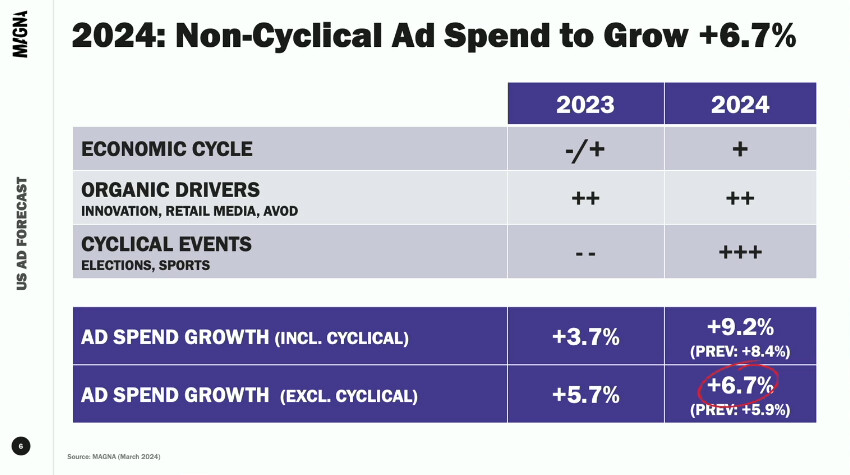

Only Magna has given an update in Q1 2024, which is for the US market only. (They also changed reporting, table is not available as before)

They have revised up its expected growth for 2024, especially for digital segments.

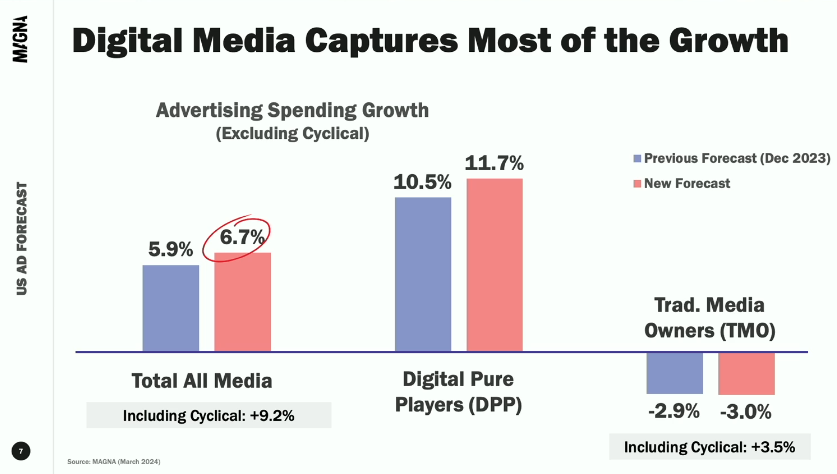

MAGNA expects non-cyclical advertising spending to grow by +6.7% this year to reach **$360 billion.*, vs +5.9% in the December 2023 report. Including cyclical spending, total media owners’ ad revenues will grow by +9.2% to $369 billion.

“Several factors led MAGNA to increase its US ad market growth forecast. That includes an improved macro-economic outlook with GDP growth raised from 1.7% to 2.4% in the last few months, the momentum of digital media formats: social media, retail media, and streaming. The latter is driven by a strong expansion in the reach and marketing opportunities offered by ad-supported streaming. That leads MAGNA to raise the non-cyclical growth forecast to +6.7%. We are slightly reducing the forecast for cyclical spending (due to a slowdown in political fund-raising) but, overall, we now expect total media owner ad sales to grow by +9.2% this year (compared to +8.4% in our previous update) to reach $369 billion.”

DPP ad sales growing by +11.7% to $260 billion (previous forecast +10.5%).

Short form, pure player digital video ad sales (primarily YouTube and Twitch), will grow by +12% this year to reach $22 billion.

Social media sales will feel the wind at their back and will rise +14% to $81 billion. Artificial intelligence (AI) is becoming an increasingly important tool used by advertisers to set up, run, and optimize their social media campaigns. MAGNA looks for this to drive additional sales in 2024, especially for small businesses setting up their first campaigns.

Search/Retail ad sales will increase by nearly +12% to $146 billion in 2024 and will also benefit from increasing AI functionality in helping brands set up and run new advertising campaigns.

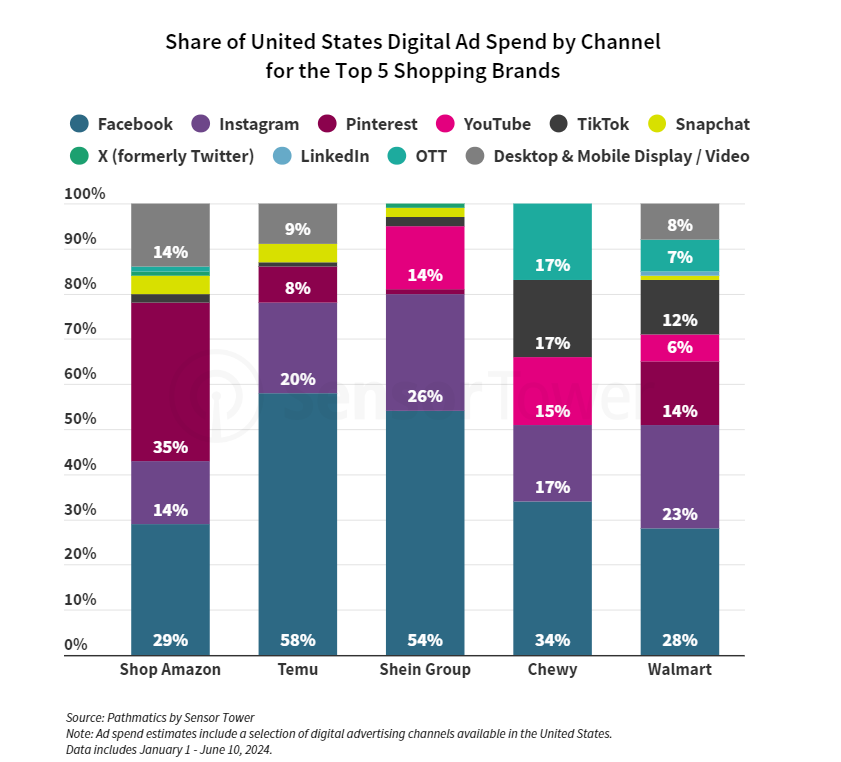

According to market intelligence firm Sensor Tower, Temu and Shein share of digital ad spend between January 1 and June 10 was 24% and 21% respectively, coming behind Amazon which took a market share of 33%.

Facebook took a large share of the ad spend by Temu and Shein, 58% and 54% respectively.

In seperate Sensor Tower study, Temu dominated the Iphone and Android app stores in the U.S this year.

Assessment

The insights above indicates that the two Chinese retailers, Temu and Shein continue to spend heavily on digital advertising in the United States.

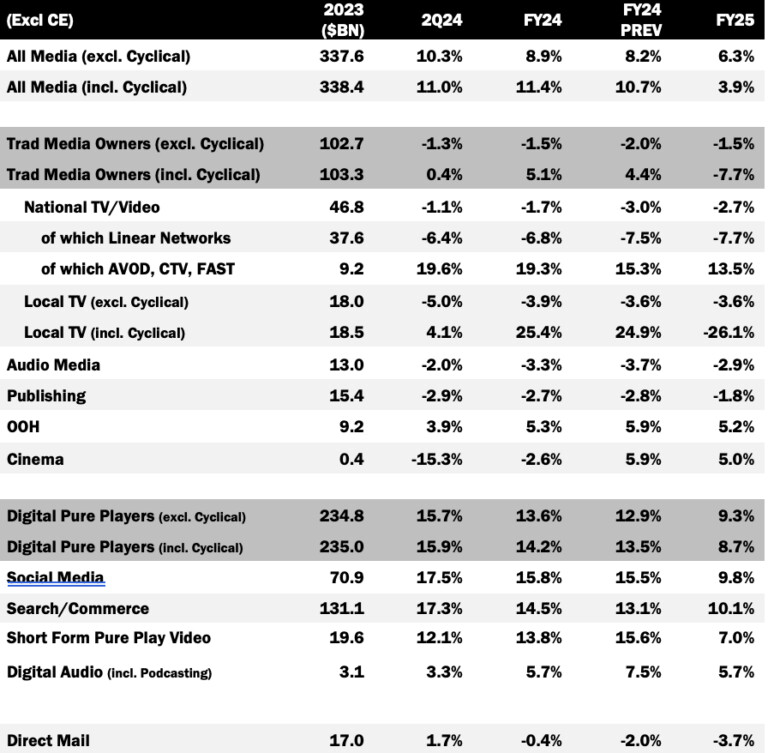

MAGNA is raising its 2024 forecast to 10% from 7.2% in December (+6.4% in 2023), following a stronger-than-expected ad market in the first quarter (+12%) and an improvement in the economic outlook (real GDP growth +3.2%, US +2.5%)

Social media revised up to 17.5% vs 11.6% in December.

Q1 2024, the leading global digital vendors reported the strongest growth rates in more than two years. Global Search ad sales grew by +16% year-over-year, pure-play video by +21% and Social Media by +28% year-over-year.

Quarterly growth rates are bound to slow down as comps will gradually get tougher, but MAGNA anticipates double-digit growth for all key digital formats and vendors this year.

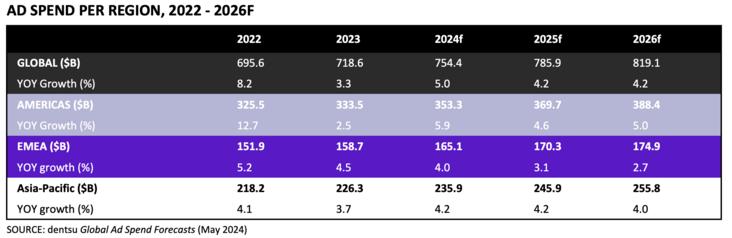

As we established before Dentsu has a different methodology, but they also raised their 2024 forecast to 5% from 4.6% in December.

Digital is now predicted to increase by 7.4% (vs 6.5% in Dec) to capture 59.6% of global spend in 2024

Substantial ad spend increases are forecast for retail media (+32.0% YOY, 17.7% three-year CAGR to 2026), paid social (+13.7% YOY, 12.5% three-year CAGR to 2026), and programmatic (+10.9% YOY), while paid search (+7.7% YOY) and online video (+6.7% YOY) are set to maintain strong growth.

In the top 12 markets,** inflation-adjusted growth is projected at 2.6% in 2024 (vs. 5.2% at current prices), as media inflation shows signs of coming down but remains high, especially for TV and sought-after digital video formats such as social video.

Thank you for this update. I was also already wondering how advertising markets are doing and are projected to do to factor it into my current assessment of Meta. So this comes at the perfect time.

It is important to note that a major part of my theories around the trajectory of Meta are centered around secular advertisement trends with growing marketshare of digital.

This means that I am currently not overly worried about a slowing U.S economy (although we get first signs of it) because I think that Meta can keep growing even in a slowdown or mild recession simply by gaining marketshare even if the overall ad-market would decline.

In line with this your work on how positively google behaved in the 2008/2009 recession influenced me. (If I remember correctly it only stagnated even though there was a major recession)

Do you agree with that take?

Ps: I am factoring in that Magna & co take a while to adjust their models to economic realities so I am not overly relying on them and I think that growth for Meta could come down significantly from current strong levels but I think it could still be positive in an mildly adverse scenario. (Assuming no deeper recessions or major shocks to the economy)

We have definitely seen an increase in market share in recent years for social, and I don’t think there are reasons to think this will stop.

I am not exactly sure the growth they experienced back then is the same as currently for social, the industry is way bigger now too, so I think in a recession digital/social could be affected more than back then. But I think these companies have a lot of ways to quickly adapt to these circumstances.

While Google behaved incredibly well during 2008/2009, its stock price still had like a ~60% drawdown.

Probably because of the EPS, the market is particularly susceptible to that I think, especially in recessions.

When you say mild recession, what do you mean by that?

I think we could have a very normal/average recession or could even be a bit more serious depending on how well the FED react to cut, or fiscal responses.

But if by mild you mean, not a 2008-style recession, I guess I would agree more with that.

Yes, I would think of more conservative numbers, especially because it seems Magna and Dentsu updated their forecast with data as of Q1 2024, and it was Q2 2024 that was softer in some aspects but also not by much either.

It also seems they use mostly current circumstances/data to make their forecasts, which we know could change at any moment.

Divesture is one of the options being sought by the Justice Department, experts see it as unlikely but Google’s business is expected to be impacted

Breaking up Google is one of the options being considered by the Justice Department after a recent court ruling that Alphabet monopolized the online search market, Bloomberg reported citing people familiar with the matter.

Other options being pursued include forcing Google to share data with competitors and initiating measures to prevent it from gaining unfair advantage in AI products.

Units that the prosecutors are seeking to be divested include the Android operating system, Chrome and AdWords (Google’s advertising sales tool).

The ruling found that Google requires device makers to sign agreements to gain access to its apps such as Gmail and to have Google’s search widget and Chrome installed on the devices ( pointing out that Google paid 26 billion to device makers in 2021 alone) hence preventing other search engines from competing.

The ruling also established that Google forces websites to allow their content to be used in its AI products and monopolizes advertisements which appear at the top of the search results.

A separate trial to determine the remedies has been set for September 14 but Google already said that it will appeal the ruling, a process that is projected to take at least two years to complete.

Experts say the ruling bears resemblance with that of Microsoft. Microsoft was found to have monopolized the PCs market and was asked to divest its operating system or applications business. However, Microsoft’s appeal was successful and was only asked to allow multiple operating systems in PCs.

Experts also believe that the most likely remedy will be asking Google to do away with certain exclusive agreements with Sam Weinstein, law professor at Cardozo Law School and a former DOJ antitrust lawyer pointing out that a divestiture is rarely ordered for a Section 2 case. However, this will still lead to a significant market share lose for Google unless the firm can successfully defend itself using the rise in competition from ChatGPT.

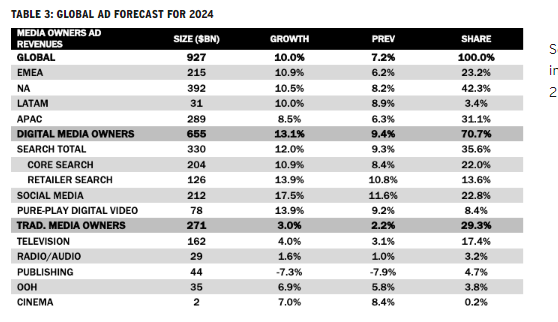

MAGNA expects full-year 2024 ad revenues to grow by 11.4% to $377bn, with non-cyclical growth at 8.9%—the highest in over 20 years, excluding 2021’s post-COVID rebound.

US ad revenues rose 11% YoY in Q2, slightly exceeding MAGNA’s 10.4% projection.

MAGNA increased its forecast for non-cyclical H2 ad spend growth to 7.4%, up from 6.4%.

Search/commerce sales will rise +14.5% (13.1% prev) to $150bn. Retail media networks will see growth of +20% and near the $50bn ($46bn), which is expect them to surpass next year, while core search (i.e., keyword search) will gain +12% in 2024.

Social media sales will rise +15.8% (15.5% prev) to $82bn, thanks in large part to the AI tools.

Ad-funded streaming has become one the fastest-growing ad channel in 2024, with a +20% increase in ad spending

Given the lack of cyclical events, total ad sales (incl. cyclical) will rise only +3.9% above 2024. Digital pure players will again drive the market, growing +9.3% to $289bn, while traditional media owners will erode by -1.5% to $102bn.

2024 Temu State of Digital Advertising 2024 Report

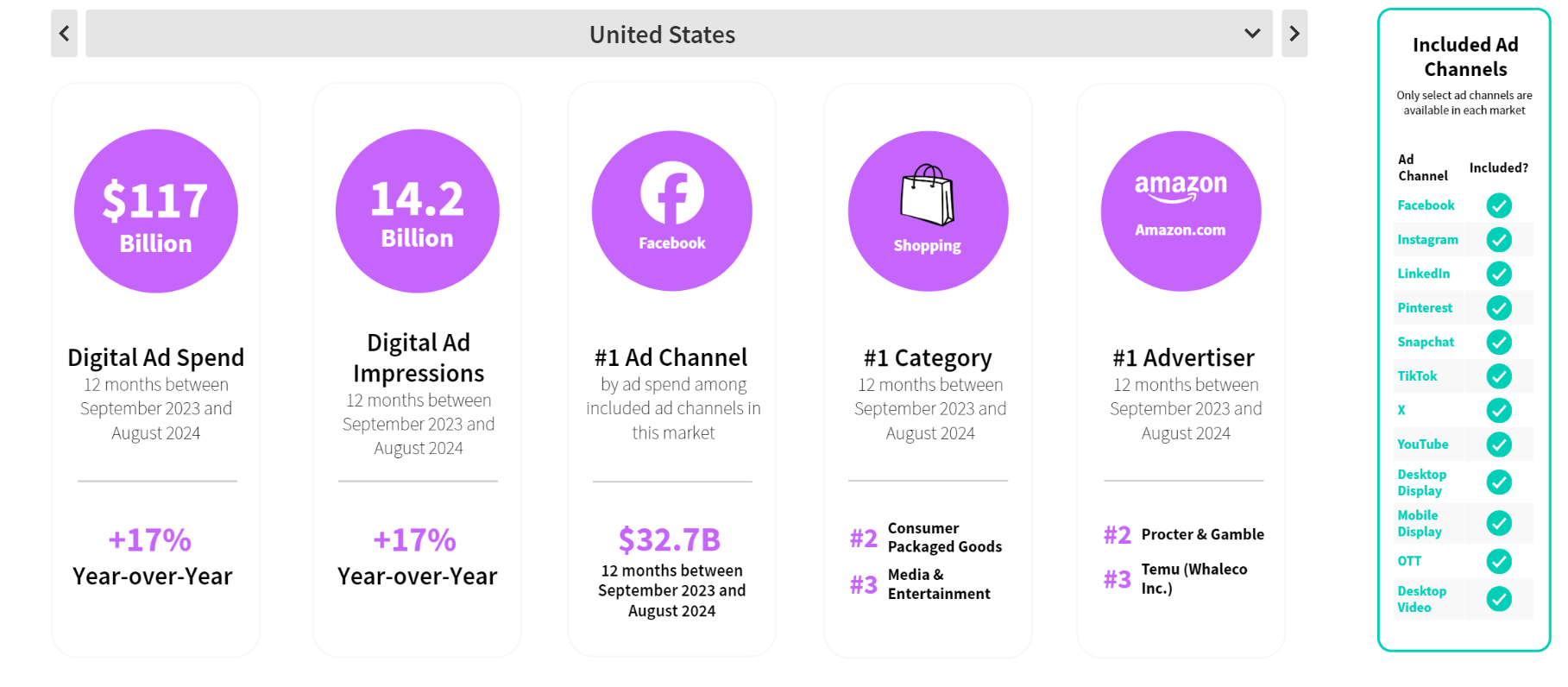

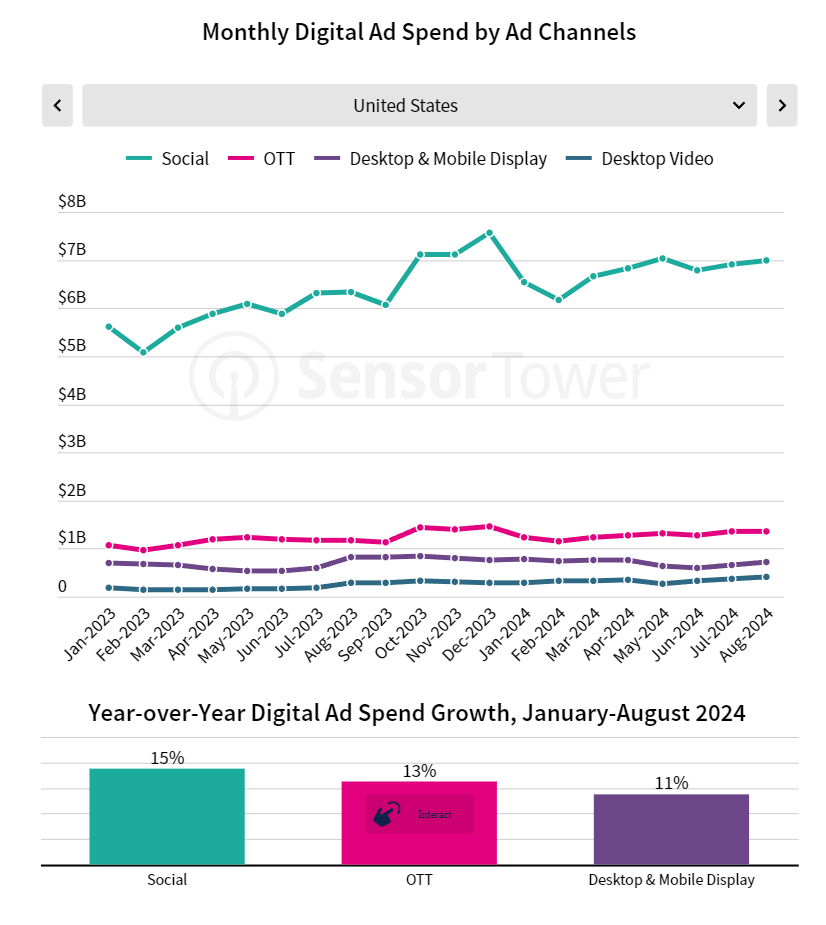

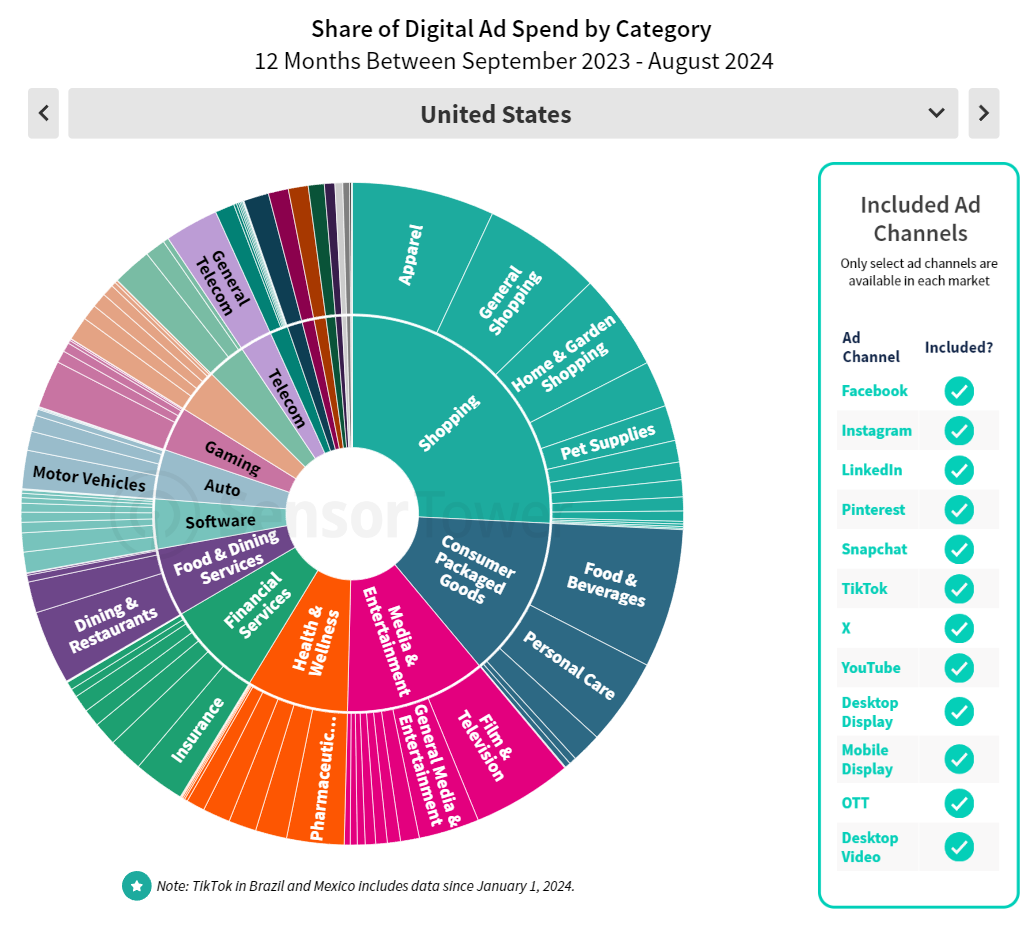

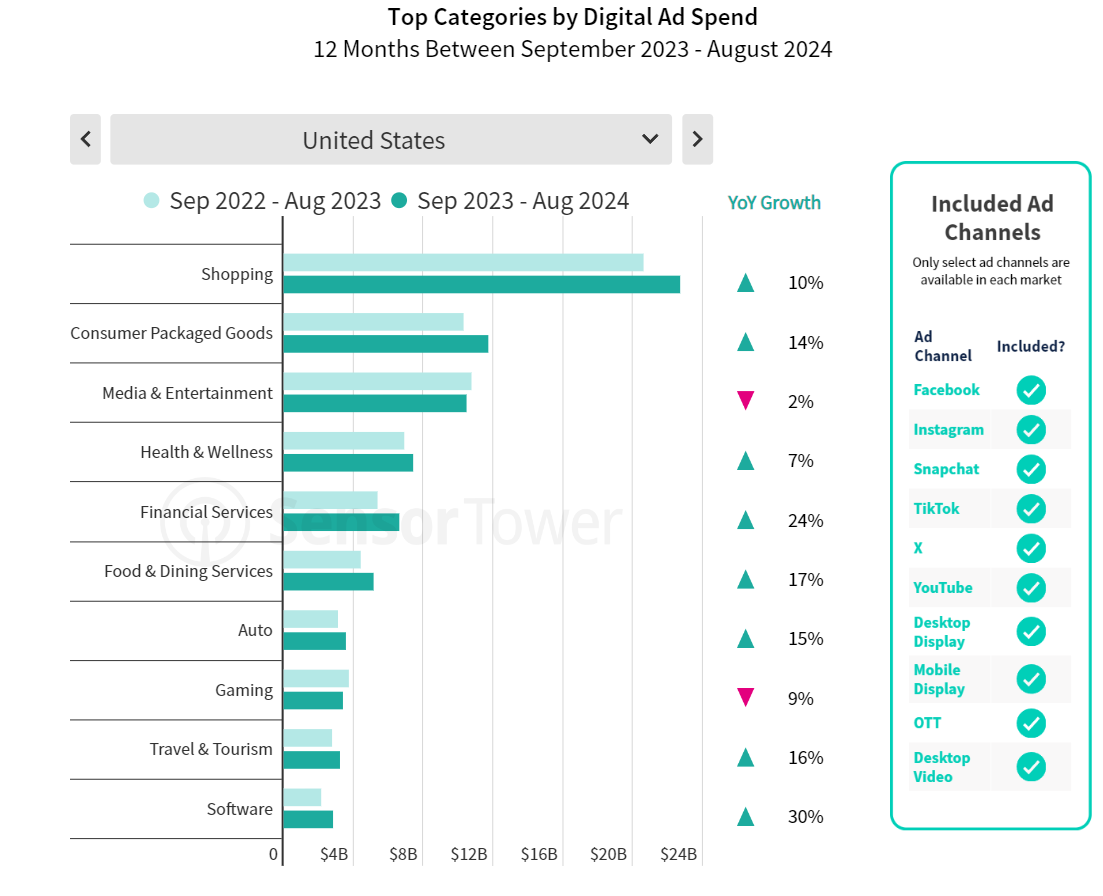

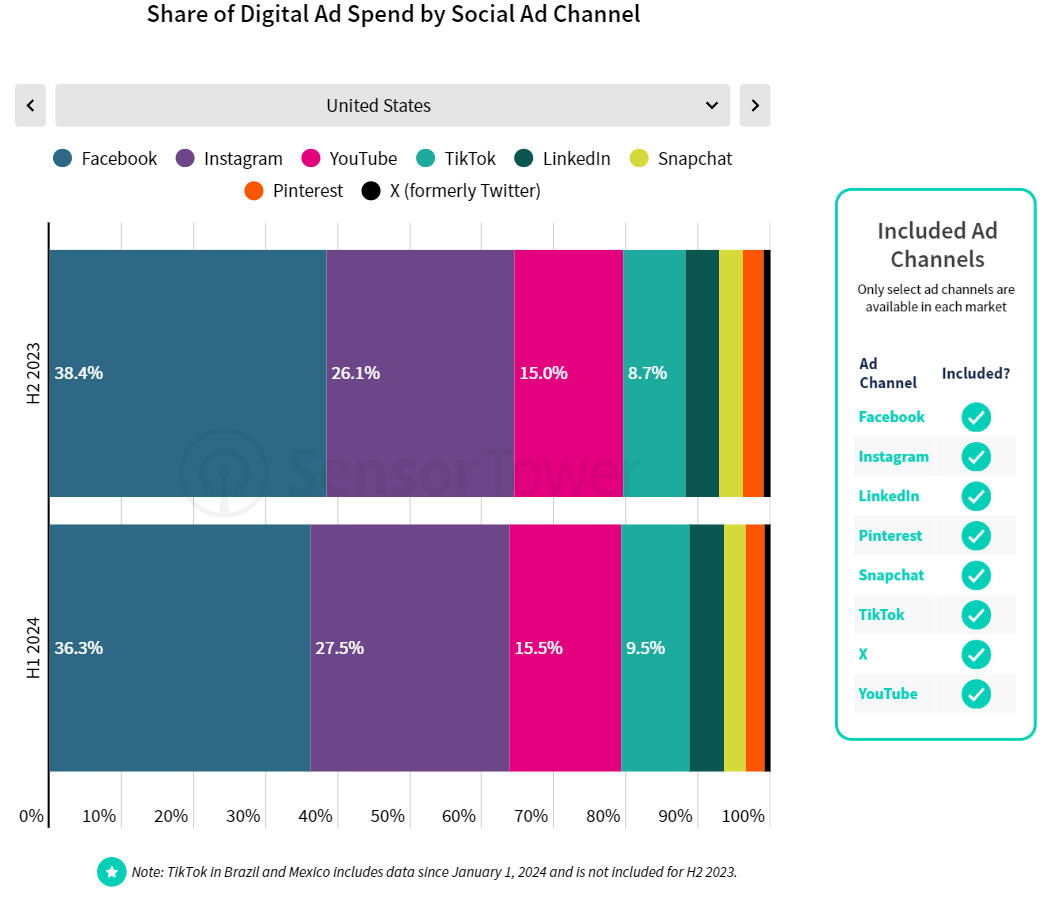

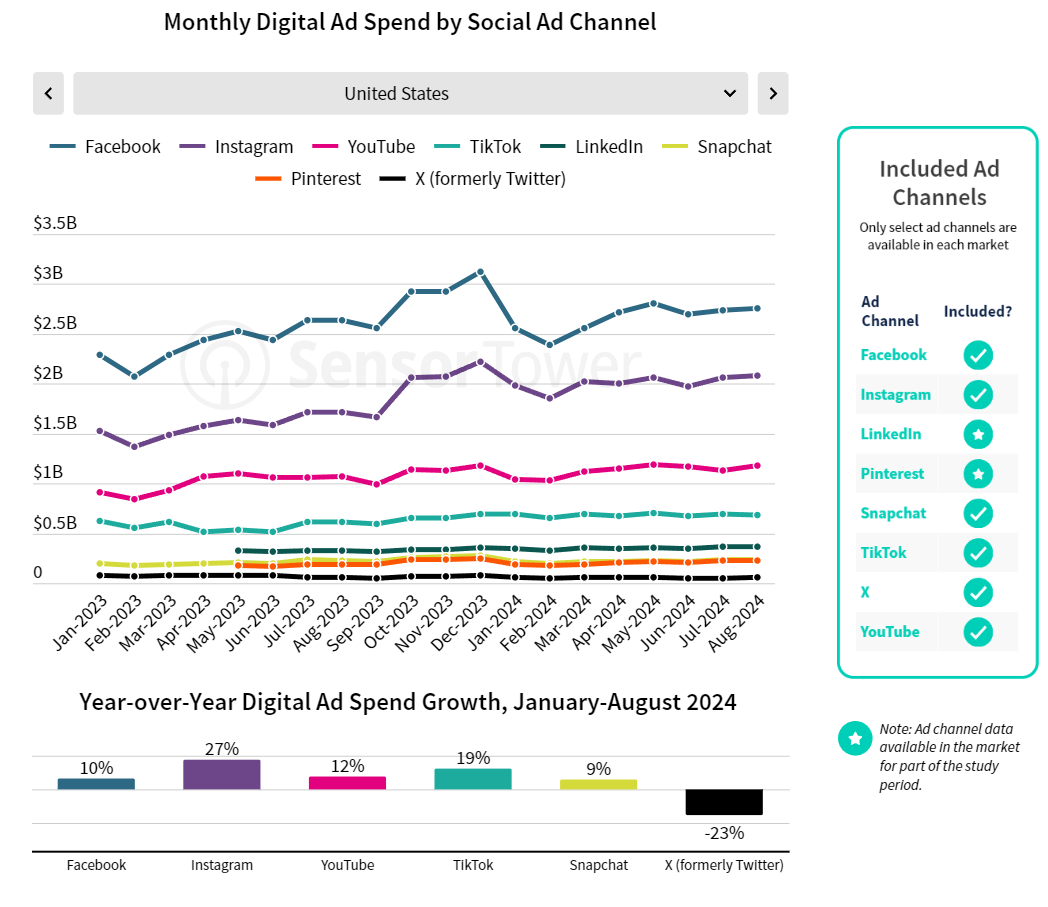

In the United States, digital ad spend reached $117 billion covering more than 14 billion total impressions over the 12 months between September 2023 and August 2024.

Instagram, the #2 social ad channel by spend in the US, had the highest year-over-year growth in the first eight months of 2024 at 27%.

Instagram didn’t just find success as an ad network in the US. The Meta-owned social network had at least 25% YoY growth in all of the other markets where we have data available including Australia, Canada, France, Germany, Italy, Spain, and the UK.

Data Collection: Pathmatics collects a sample of digital ads from the web. In order to report the most complete picture of the digital advertising landscape, we utilize two leading data sourcing technologies: panels and data aggregators. Pathmatics uses statistical sampling methods to estimate impressions, cost per thousand impressions (CPMs), and spend for each creative. Each impression served to our data aggregators and panelists is assigned a CPM, which when combined with impressions results in our spend estimates.