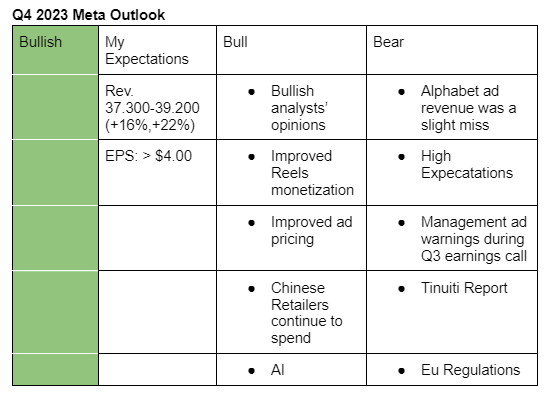

Note: My expectations are guestimates based on weak Tinuiti ad spend data and the fact that Meta has beaten its revenue mid-point guidance in the past five consecuitive quarters.

I am positive on Meta’s fourth-quarter results given that;

-

Alphabet’s ad revenue miss was small, and the likes of Mark Mahaney of Evercore believe that it was in line with the estimates. Also, as @Magaly notes above, social is the one growing the fastest; hence Meta’s ad revenue won’t necessarily follow in Alphabet’s steps.

-

Chinese retailers who contribute a significant portion of Meta’s ad revenue continue to spend.

-

Magna projects that social media ad spending will grow significantly in H2 compared to H1. The firm also raised its 2023 revenue forecast for digital media owners from +7.9% to +9.6% in the September report.

-

Analysts such as Mark Mahaney (Evercore) and James Lee (Mizuho) whose projections in the past were in line with actual results are bulish on Q4 2023 earnings.

-

Tinuiti and Skai reports indicated that there was an improvement in ad pricing in Q4 2023.

-

Data checks by some of the top analysts (such as Ronald Josey of Citi) ranked by TipRanks points to improvement in Reels ad loads and monetization.

Some of the risks include;

- Market expectations on Q4 2023 results are high: A small miss could cause the stock to fall by alot. In my opinion, this is the greatest risk given that Meta is depleting its weak comparison periods. Though highly unlikely, my worst case scenario is a revenue growth of 16% y/y.

- Management ad spending warning given during Q3 earnings call: Though the management said this was included in the guidance, there tend to be miscalculations.

N/B:

Management Guidance (Revenue): $36.5 billion- $40 billion (13.5-24.3%)

Analysts’ Estimate (Revenue): $39.09 billion (+21.5%)