I=8, Porsche Porsche excpects sales volume to decline in 2025 due to the end of ICE Macan and 718 in the EU and further 911 supply chain issues

In a call with investors, Porsche confirmed its outlook for 2024 of a 14-15% profit margin and reiterated that it expects 2025 to be challenging, that’s according to Bernstein Research analysts.

Porsche said it expect sales volume to decline this year due to the withdrawal of the combustion-engine Macan and 718 in the European Union at the end of June last year and possible further supply chain issues the 911 model.

As a result of the 2025 update, Jefferies lowered their forecast for 2025 Porsche Group EBIT by 930 million euros (14%) to €5.75 billion.

Oddo BHF said it lowered its Porsche Group EBIT estimate for 2025/26 by 16%/20%, placing it 11%/15% below consensus.

Assessment

Porsche’s 2024 sales volume were boosted by the new EV Macan which was delivered to over 18,000 clients in 2024. However, recent comments regarding this model have pointed to uncertainty regarding its sales volume. For instance, it’s now said that Porsche is considering bringing a new ICE Macan. Similarly, it’s said that most of the EV Macan clients are new to the brand. This is probably not good for demand since it means existing clients, especially those who had the ICE Macan could shying off from the model.

We had also projected that the end of ICE Macan and 718 Boxer in June would be an headwind in the second half of 2024. However, there’s the likelihood that most clients bought the two models before the June dateline (EU Cybersecurity law), hence keeping the sales volume stable during the year (718 deliveries in Q3 were up 38.5%). That means the headwind as a result of the end of ICE Macan and the 718 will now be felt in 2025.

Around 23,458 units of the ICE Macan and 5,000 units of the 718 were sold in Europe in 2023 and 2022, respectively. That brings the total headwind from the EU Cybersecurity law will be around 30,000. However, the EV Macan could reduce this by maybe 15,000 units (guestimate based on those demand insights). There have also been reports that the Northvolt bankruptcy may delay the rollout of the EV 718 in 2025.

It’s currently hard to estimate the impact of supply chain issues on the 911. But given the importance of the model to the company (it contributes a third of the company’s profit), I expects Porsche to keep its production stable by increasing the cost associated with supplies.

Overall, I estimate that Porsche deliveries in 2025 could fall by around 20,000 units. This will reduce my estimate for its operating result before special items by around 600 million euros.

I=8 Volkswagen reiterates that it expects a strong Q4, maintained its outlook for 2024

During its Q4 2024 pre-close call, Volkswagen reiterated that it expects a strong fourth quarter driven by higher volume and mix.

It also reiterated its 2024 outlook- revenue of €320 billion and operating margin of 5.6%.

Volkswagen announced that beginning from Q1 2025, they will stop reporting Power Engineering as a separate segment and that individual financial figures of the likes of Skoda, Audi, etc will no longer be reported i.e automotive divisions will only be reported. Man Energy Solutions will also be moved into “others”.

Analysts grew more positive on Volkswagen following the Q4 pre-close call

Stifel and HSBC said the strong momentum seen in Q4 is likely to continue into 2025.

“The fourth quarter proved to be the strongest of the year in terms of volumes, and this momentum is set to continue into 2025”, Stifel said. “VW even considers that consensus might seem a little cautious.”

“We believe that the Group could report a slight increase in sales in 2025”, add HSBC analysts.

Bernstein Research said Volkswagen sounded more optimistic than Porsche.

I=8 Porsche expects operating return on sales for 2024 to come in at the lower range of their guidance, 2025 operating profit to be impacted by vehicle development costs

Porsche said for 2024, the return on sales is likely to come in at the lower range of the guidance (14% to 15%), automotive net cash flow margin will be over 10% (guidance: 7 to 8.5%) while other key performance indicators do not show significant deviations from the forecast.

It expects 2025 revenue in the range of €39 to €40 billion (analysts estimate: €40.3 billion) and operating margin in the range of 10% and 12% (analysts estimate: 15.0%).

The guidance takes into account the decision by the board to include additional vehicle models with combustion engines or plug-in hybrids, battery activities, expansion of the Sonder- and Exklusivmanufaktur and adjustments to the corporate organization which will impact operating profit and the automotive net cash flow by around €0.8 billion.

Assessment

Taking into account the 800 million euros associated with the product developments, the operating margin guidance for 2025 will be almost in-line to forecasts by analysts who attended the recent pre-close call. Their revenue forecast for 2025 is unchanged from that of 2024, hence much better than I had expected given the recent dampened expectations by analysts.

What have been the recent dampened expectations for revenue by analysts? Something less than €40.3 billion? I think as a best policy most recent analyst expectations should be put in brackets of a post, what do you think?

Yes, Jefferies said it lowered its revenue forecast for 2025 by 2%. They had not provided their intial forecast. But basing on the consensus (€40.3 billion), that would be a reduction of around 800 million euros to €39.5 billion. Similarly, Oddo BHF said they lowered EBIT forecast for 2025 by 16%, making it 11% below consensus ( €6.0 billion). I will point out that Jefferies and Oddo BHF had not taken into account yesterday’s announced plant developments, which will have significant impact on the results, hence the guidance given by the management downplays the analysts earlier concerns associated with supply chain issues and end of sales of ICE Macan and 718 Boxer in Europe.

I agree with your thoughts about putting recent analysts estimates in brackets, it was an oversight on my end.

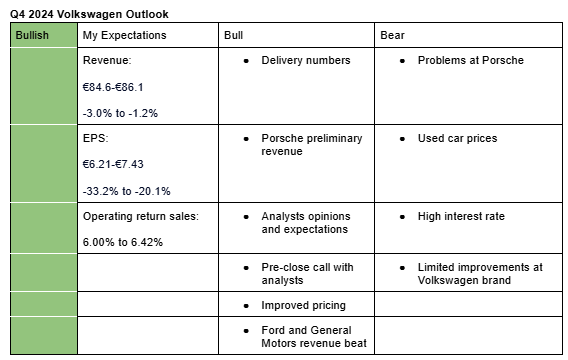

I am bullish on Volkswagen’s Q4 2024 earnings. My estimates are based on vehicle delivery numbers, insights from the recent pre-close call with analysts, further pricing tailwinds in Q4, and Porches’ preliminary results. Here is a description of by bullish and bearish sentiments:

Bullish sentiments,

Delivery numbers: Volkswagen’s 2024 delivery numbers came in line with management’s guidance of 9.0 million.

Porsche’s preliminary revenue: Recently, Porsche announced that its revenue for 2024 is unlikely to deviate much from their guidance of €39 to €40 billion.

Analysts opinions and expectations: Analysts expect Volkswagen to beat its guidance for 2024.

Pre-close call with analysts: During the recent pre-close call with analysts (page 8), Volkswagen reiterated its outlook for 2024, signaling that the downside risk is low.

Improved pricing: There is a possibility that pricing at individual brands such as Porsche and Audi improved further in Q4 due to pricing tailwinds from new models such as Audi A6 e-tron, Audi Q6 e-tron and refreshed models such as Audi A6, Audi Q5, Tiguan, etc. Similarly, new vehicle pricing was stable in the US during the quarter.

Ford and General Motors revenue beat: Both General Motors and Ford reported revenue for Q4 that topped analysts estimates, suggesting that the US market could have performed better than expected. General Motors specifically stated that demand and pricing were strong during the quarter.

Bearish sentiments;

Problems at Porsche: Porsche is facing challenges such as reduced demand for EVs, especially in China, supply chain issues and high costs. As a result, it now targets 2024 operating return on sales to come in at the lower range of its previous guidance which stands at 14% to 15%.

Used car prices: While used car prices have stabilized in the US, they are still down year over year in Europe.

High interest rate: While the ECB has lowered key interest rates to 2.75%, it will probably take some time for the changes to be reflected in Volkswagen Financial Services’s (VFS) books. High interest rate expenses coupled with unfavorable used car market will reduce VFS’s operating profit. As such, it’s unlikely that VFS will achieve its operating profit, which it had guided to come in at 3.2 billion euros in 2024.

Limited improvement at the Volkswagen brand: Reports indicate that Volkswagen brand’s operating return on sales will take a while to improve despite the initiated cost measures. As such, I expect limited improvement in its operating return on sales in Q4 compared to Q3.

N/B: Here are the analysts estimates and management guidance for Q4 2024 and 2025:

Mercedes Q4 2024 revenue and operating profit slightly missed analysts estimates, 2025 revenue and vehicle sales expected to be slightly weaker

Mercedes-Benz Q4 2024 revenue fell 3.8% to 38.45 billion euros, slightly below analysts estimate of 38.12 billion euros while net profit declined 20.5% to 2.48 billion versus analysts estimate of 2.42 billion euros.

The company said it expects to sell slightly fewer cars and vans this year compared to 2024 and is guiding 2025 adjusted return on sales margin in the car division of 6%-8% compared with 8.1% in 2024.

It expects 2025 group revenue to be slightly below the prior-year level.

Renault beats revenue and operating margin forecast, said it expects an headwind of 1% or €500 million on operating margin from the CO2 regulation

Renault 2024 revenue rose 7.4% to 56.2 billion euros, exceeding management guidance of 54.5 billion euros, driven by product launches such as the popular R5 and new hybrids while operating return on sales of 7.6%, met their target of 7.5%.

For 2025, Renault expect operating return on sales to drop to 7%, noting that the CO2 regulation would have a 1% headwind on its margin, equivalent to around 500 million euros of operating profit.

Renault remains “hopeful” that the CO2 rules will be relaxed but ruled out pooling with other car makers, nothing that it expects to sale EVs on discounts while raising prices for combustion engine vehicles.

I=6 Traton’s Q4 2024 operating return on sales beats estimate while revenue slightly misses estimate, the company sees gloomy 2025

Traton Q4 2024 revenue fell 3.8% to €12.22 billion, almost in line with analysts estimate of €12.35 billion while operating return on sales was 9.2%, above analysts estimate of 8.5%.

Traton is guiding 2025 sales growth in the range of -5% to +5% and operating return on sales in the range of 7.5% and 8.5%, lower than 9.0% forecasted by analysts.

“We anticipate that global economic momentum will be slightly weaker in 2025, compared to the previous year. Overall, therefore, we expect demand for trucks to decline in TRATON’s core markets,” Traton said.

Assessment

Traton’s Q4 2024 revenue was below my estimate by 128.5 million euros while operating return on sales topped my average estimate of 8.8%. The 2025 revenue growth estimate and operating return on sales are in line with my estimates. Given the deviation in Q4 2024 revenue and operating return on sales was small, I will reiterate my Volkswagen Q4 2024 outlook.

Volkswagen’s Q4 2024 results top analysts estimates, company forecasts a stable 2025

Volkswagen Q4 2024 revenue rose 0.2% to €87.38 billion, significantly above analysts estimate of €83.9 billion (boosted by strong development in Financial Services) while operating return on sales came in at 7.0%, above analysts estimate of 6.4%.

Net cash flow in the automotive division was down 70% to €1.74 billion in Q4 due to continued high investments and decline in operating profit but supported by reduction in net working capital while net liquidity at the end of the year stood at €36.1 billion (-10.5% y/y).

For 2025, Volkswagen is guiding revenue to grow by up to 5% (analysts estimate: +1.5%), operating return on sales of between 5.5-6.5% (analysts estimate: 6.2%) and net liquidity in the range of €34-€37 billion.

Volkswagen brand’s operating return on sales rose to 6.4% in Q4 from 3.17% in Q3.

Assessment

Volkswagen reported a solid quarter and is guiding for a stable 2025 despite the geopolitical headwinds such as the Trump’s tariff. It’s impressive to see Volkswagen’s brand operating return on sales improving, suggesting that costs measures are having a positive impact. However, it’s not good to see pricing starting to decelerate quarter over quarter at Audi, Porsche and Traton.

What is the reason why the operating margin („return on sales“) was so high this quarter? Maybe there have been special factors?

Are there more details on the 5.5-6.5% operating margin target for 2025? The lower end is quite low. Are there special factors like restructuring costs in there? (The underlying adjusted operating margin in 2024 was 6.7%)

Net cash flows of 2-5 billion in the automotive division also looks quite low. What are the reasons for that?

I read that rescaling for Cariad is planned. What is exactly is meant by this? Are there more details like how much they want to invest?

They didn’t give reasons why operating margin in Q4 was that high. They only said Q4 was a strong quarter. But I think it was mainly due to the outperformance at the Volkswagen brand. There was special item of €409 million, but that could have taken the underlying margin to 7.5%.

The operating margin in 2025 is expected to be that low mainly due to the ramp-up of BEVs, which are margin dilutive. Arno said they expect to grow the BEV share in Europe towards 20% from the current 13%. As a matter of fact Q1 is expected to be significantly lower when it comes to margin. The ramp-up in investments is also expected to contribute to this result.

Net cash flow in the automotive division is expected to be that low due to €2 billion euros cash outflow associated with the implementation of restructuring measures launched in 2024. They also expects dividend contribution from China joint ventures to be lower by €1 billion euros in 2025. They are also making investments for the future but expect cash flow to improve towards 2027.

Yes, Blume said Cariad will continue playing an important role in the group into the future since it will be producing the 1.1 and 1.2 software. However, he added that they will scale cariad according to the needs of the Group.

On a side note, Arno said the 2025 guidance doesn’t include the impact of Trump Tariff, CO2 penalty relaxation in Europe and potential further restructuring expenses.

Arno also pointed out that they are seeing better momentum in BEV intake and that will allow them to lower the €1.5 billion euros headwind in 2025 though they still don’t expect to beat the CO2 target in 2025. They expect to be CO2 neutral in 2026 and to turn positive in 2027.

Unit sales this year are expected to be flat.

Arno confirmed that Volkswagen Group will reduce the investments in 2025 to 2029 to €165 billion from €180 billion that had been planned for 2024-2028

Neutral, €101: Analyst George Galliers of Goldman Sachs said Volkswagen clearly exceeded expectations in terms of profits and cash, adding that the outlook is conservative.

Market perform, €102: Analyst Stephen Reitman of Bernstein said Volkswagen’s results and 2025 guidance exceeded consensus, but the decisive factor remains with Volkswagen to curb investments and implement its strategy.

Sector perform, €116: Analyst Tom Narayan of RBC said Q4 results and guidance for 2025 exceeded consensus estimates.

Buy, €131: Analyst Fabio Hölscher of Warburg Research said Q4 results and 2025 guidance slightly exceeded consensus.

Sell, €75: Analyst Patrick Hummel of UBS said only the cash flow target for 2025 is somewhat mild compared to the consensus but the reduction in investments should be well received.

Neutral, €110: Analyst Jose Asumendi regarded the 2025 outlook as conservative but said the development of net cash was strong towards the end of the year.

Alright thanks for the summary. Some important points in there. Volkswagen also released its annual report. I assume that you will be able to find more details in it. (At least what happened in Q4, maybe even more details regarding the outlook)

It looks like it was due to volume and mix effects.

"The operating result amounted to €19.1 billion, a slight increase on the guidance provided in our adjusted forecast, due mainly to positive volume and mix effects in the fourth quarter. " Page 136.

“In terms of pricing, there are really several effects. First and foremost, we see now the positive list price increases from the past months coming through in Q4. Second, you mentioned already have great new models, specifically also in the volume brand, but also the premium Passat, Tiguan, Golf. So, these new models have better margins, but obviously, and it’s not a secret, if you look into the market, there’s a negative effect on the BEV side. So, we had to increase our BEV incentives in order to get to a better order intake. But still, if you take these three elements together, we were still positive in Q4, and as I said before, we are confident that overall price-volume mix we can keep stable in 2025, although we doubled the share of BEVs in Europe, which will be a challenge.” Arno said in the earnings call.

I=8 Porsche cuts its midterm target to a range of 15%-17% from 17%-19%, sees selling 300,000 units in the long-term

Porsche lowered its midterm operating return on sales target to a range of 15%-17% from 17%-19%, saying they don’t expect the situation in China to recover in the near future and that they expect supply chain issues to continue in the midterm.

Outgoing CFO Johan said they will rely on further price increase this year, especially on the 911 to meet their 10%-12% operating return on sales guidance.

They said that if tariffs were to be imposed, their first reaction will be to increase prices on the sporty vehicles such as the 911 and seek further cost-cuts.

Porsche downplayed competition in China, saying the slow demand they are facing is due to economic headwinds.

“Talking about other car manufacturers, there’s no Chinese, Chinese competitor. There are some where customers move in in the SUV segment to Li Auto, but there that’s expectation in terms of roominess in the car and screens for watching videos. And that’s a completely different use when you compare it, for example, with the Cayenne. The customers who love the sportiness, the driving dynamics of Porsche stick to the brand, and we still have some. Our market development is more driven by the financial crisis, real estate crisis we do have, and many of our customers are affected.”

Blume said he sees the company selling 300,000 vehicles in the long-term.

“We will make, a adaption of our company structure to a 250,000. This does not mean that this is our volume target. I expect more a volume around 300,000, but always, well balanced in between, the value drivers.”

Assessment

The midterm targets are significantly lower than my estimates. I will consider the changes in my next valuation model estimate. I think if they can keep prices high and reign on costs, selling 300,000 units per annum would still result in good profits for the Group.

I=5 Volkswagen brand confirms that it’s postponing the 6.5% operating return on sales target by 3 years

Volkswagen brand confirmed Handelsblatt report that it was postponing the operating return on sales target of 6.5% to 2029 from 2026.

Powel said achieving margin positive with the small cars will be hard but they are confident that they will (min 49:30).

“With small cars, the 6.5% margin expectation is a big one,” Chief Financial Officer David Powels said. “And we are confident that we can meet this forecast.”

CEO Thomas Schafer said by 2027 they aim to have lowered battery cost by 50% compared to 2023 (min 5).

Powels said they have already reduced factory costs by 3% y/y partly by eliminating night shifts at selected plants (min 26:25), reduced overhead costs to 9.2% from 9.4% in 2023, reduced the number of positions globally by 4,200 (40% in production, 30% in administration, and 20% in overseas regions)

Assessment

If they manage to reduce costs by 50%, then their EVs will be very competitive since batteries account for about 40% of an EV cost. It’s good to see that they have already implemented performance program measures. However, the benefits look muted considering that they now expect to achieve their 6.5% return on sales target in 2029 instead of 2026. They must be expecting significant margin dilution from the upcoming BEVs.