Todays conference gave me the feeling that the December rate cut is not assured at this point. And if the economy maintains its resilient performance, the pace of rate cuts in 2025 may slow accordingly.

This outlook arises from the ongoing uncertainty around the neutral rate level, with the possibility that it may be higher than previously estimated. However, Powell emphasized that the risks of overtightening versus under-tightening are currently balanced.

The market appears to have interpreted the message similarly, as the odds of a December cut and additional rate cuts in 2025 have slightly decreased

Powell clarified that the Fed does not expect immediate policy effects from the incoming administration. While fiscal policy changes, can influence economic outcomes, the Fed will consider these impacts once the specifics become available.

Powell emphasized that, legally, the President does not have the authority to remove the Fed Chair.

Inflation

Recent inflation data came in slightly higher than anticipated. Anticipate some bumps in inflation ahead, though the trend remains downward.

This is not an overheated economy. Much of the inflation observed this year represents “catch-up” inflation in housing rather than ongoing pressures.

Current renter inflation data reflects a lag from prior conditions. Newly signed leases are showing low inflation, which will gradually appear in broader measures.

Despite increases in break-even inflation rates, Powell did not observe significant de-anchoring of long-term inflation expectations, indicating continued confidence in inflation moving toward the 2% target.

Labor Market

Average monthly job gains over the past three months stand at 104,000, a marked slowdown from earlier in the year. The labor market is currently slightly weaker than pre-pandemic.

Powell indicated that the Fed is keen on maintaining a strong labor market while avoiding unnecessary cooling that could weaken economic activity.

Current wage increases are now roughly in line with inflation at 2%, assuming productivity gains remain strong.

Long-term yields and rates

Powell attributes higher Treasury yields since September to stronger growth expectations and reduced recession risks, rather than heightened inflation expectations.

As the Fed approaches neutral territory, the pace of rate cuts could slow, a consideration that is only now starting to take shape.

The Fed remains flexible and will adjust its view on the pace and endpoint for rate changes as the economic outlook evolves.

Fiscal Deficits

Powell acknowledged the unsustainable path of U.S. fiscal policy, with deficits increasing despite full employment.

Fed views high and rising debt levels as ultimately a longer-term threat to economic stability. However, he reiterated that fiscal policy is beyond the Fed’s direct control and urged responsible management.

I=7 Powell said they don’t have to be in a hurry to cut interest rates further

Powell said the performance of the economy means that they don’t have to be in an hurry to cut interest rates.

“The economy is not sending any signals that we need to be in a hurry to lower rates,” said in a speech to business leaders in Dallas. “The strength we are currently seeing in the economy gives us the ability to approach our decisions carefully.”

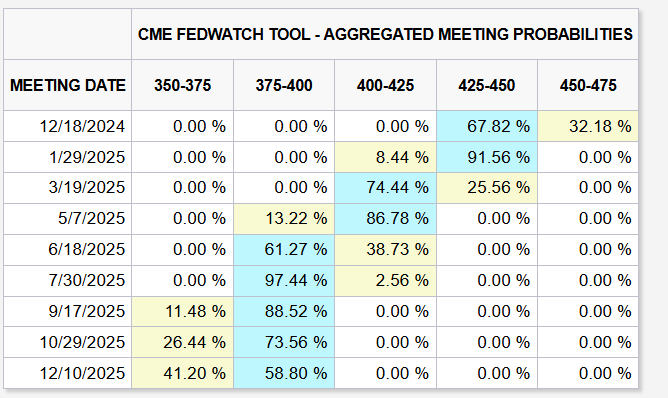

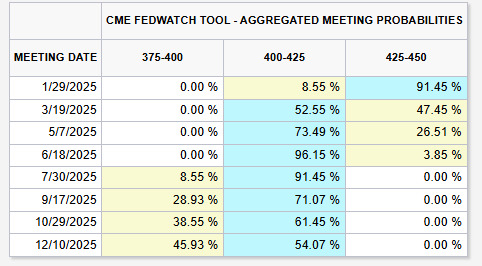

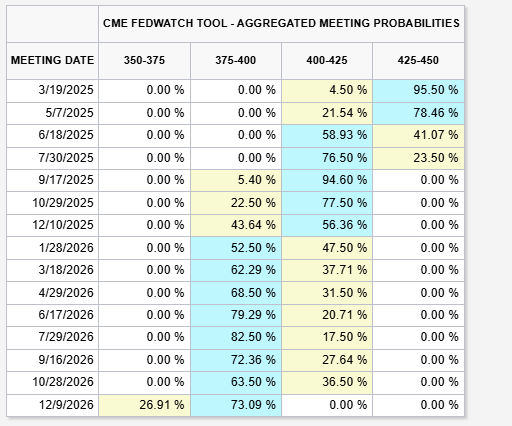

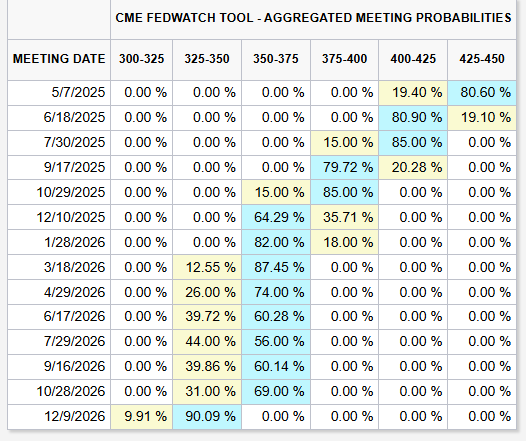

The probability of a 25 basis points rate cut in December were lowered to 58.7% from 67.82%.

The Federal Reserve is not at risk of losing its independence. Its self-funding structure ensures autonomy from government interference in spending and hiring decisions.

Declining response rates in surveys have increased data volatility, making revisions more common and potentially less predictable.

The Fed does not create policies based on still uncertain assumptions of future fiscal policies.

The Fed has no role in immigration policymaking, even though immigration has positively contributed to the economy thus far

The Fed does not consider national debt levels when setting interest rates. Its mandate is focused on price stability and maximum employment.

Aggregate economic data remains strong, with the economy performing better than anticipated in September. However, pressures are evident among lower-income consumers, a trend that wasn’t as evident two years ago.

Bitcoin is viewed as a speculative asset and a competitor to gold, not as a rival to the U.S. dollar.

The market has decreased the amount of cuts expected significantly, the December cut is still not that clear

I=10 Fed cuts interest rates by 25 basis points as expected, turns more hawkish regarding next year rate cuts

The Fed cut its key interest rate by 25 basis points to a target range of 4.25%-4.5% as was widely expected by the market.

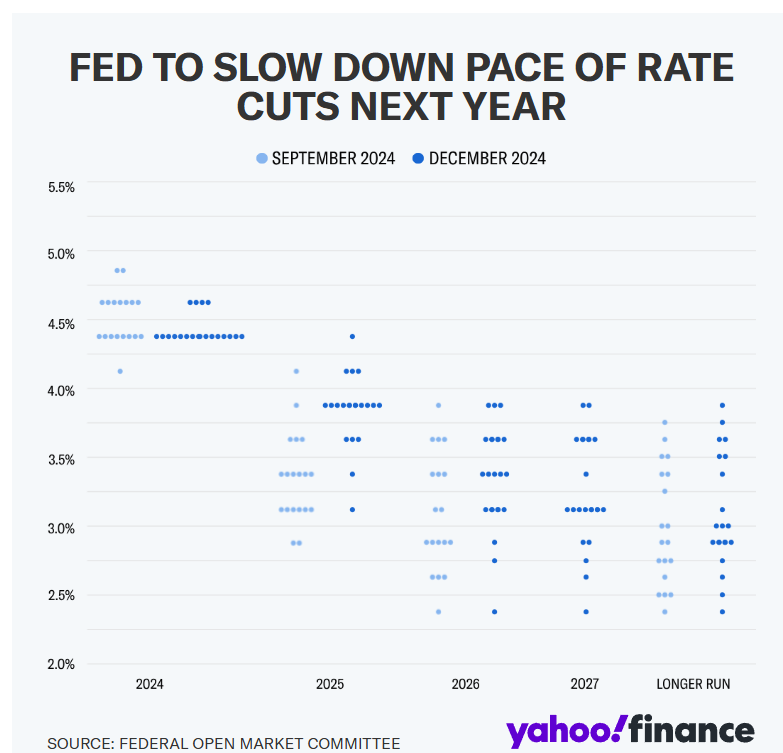

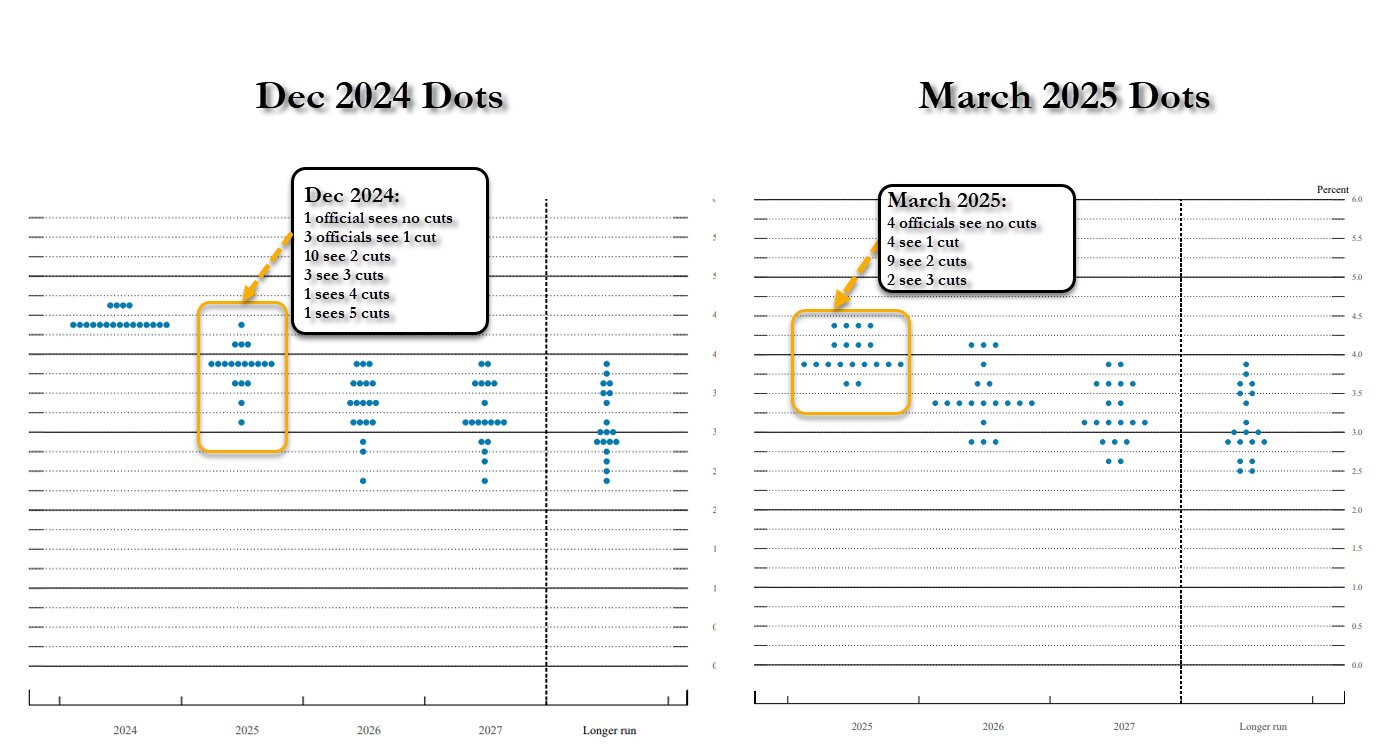

However, its “dot plot” indicated that it would probably cut it two times next year, down from four that the matrix indicated in September.

In a post-meeting call, Jerome Powell pointed out that the policy is now significantly less restrictive.

“With today’s action, we have lowered our policy rate by a full percentage point from its peak, and our policy stance is now significantly less restrictive,” he said. “We can therefore be more cautious as we consider further adjustments to our policy rate.”

Powell added that going forward they will move much slower with regards to rate cuts.

“We moved pretty quickly to get to here, and I think going forward obviously we’re moving slower,” Powell said.

Powell signaled that the Tariffs brings some uncertainty next year.

“It’s very premature to try to make any kind of conclusion. We don’t know what will be tariffed, from what countries, for how long and what size. We don’t know whether there will be retaliatory tariffs,” Powell said. “What the Committee is doing now is discussing pathways and understanding the ways in which tariffs can affect inflation.”

He pointed out that the Fed is not looking to add Bitcoin.

“We’re not allowed to own bitcoin. The Federal Reserve Act says what we can own, and we’re not looking for a law change. That’s the kind of thing of thing for Congress to consider, but we are not looking for a law change at the Fed,” Powell said.

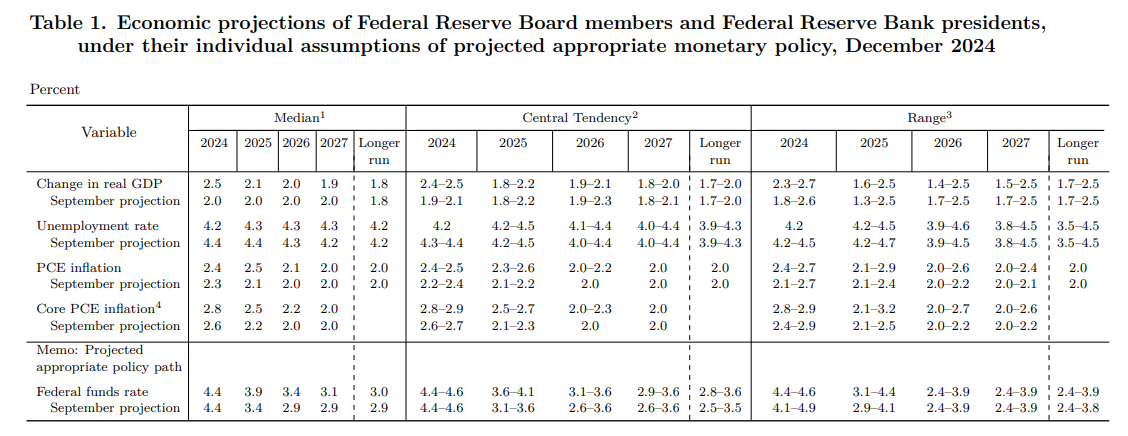

The committee raised its projections for PCE inflation in 2024, 2025 and 2026 to 2.4%, 2.5% and 2.1% from 2.3%, 2.1% and 2.0% respectively.

The Federal Reserve delivered a hawkish message in its latest meeting, signaling not only a reduction in the anticipated number of rate cuts but also a significant upward revision to inflation forecasts, along with an acknowledgment of upside risks to inflation.

The FED is once again shifting its focus to inflation from unemployment.

While I remain skeptical about the accuracy of the Fed’s projections (given their poor track record), my concerns are around:

The Fed’s credibility is once again under pressure. The rapid flip-flopping in policy signals and focus over just a few meetings has eroded confidence. The reliance on a highly data-dependent approach, without a clear proactive plan, underscores the lack of forward-thinking in their planning.

The Fed’s inconsistent signaling is only amplifying uncertainty and volatility in financial markets. Currently, there is not a clear trajectory, and each pivot by the Fed now triggers overreactions in either direction.

The decision to aggressively cut rates in September may have been a mistake. They conditioned themselves to further easing when the economy maybe did not need it yet. A more measured approach waiting to thoroughly assess whether unemployment was genuinely set to rise might have avoided it.

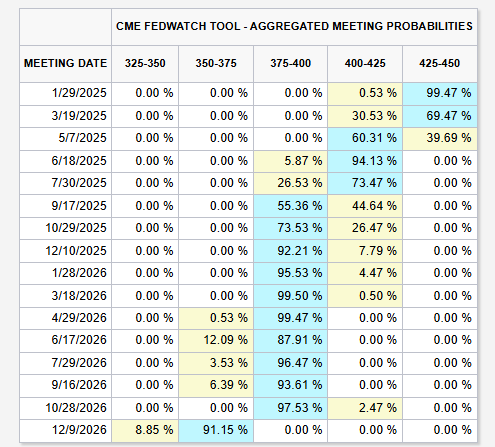

Currently, markets are pricing in only one rate cut for 2025. The positive takeaway here is that expectations are already set at a very low bar for rate cut surprises, should economic data fail to come in as hot as anticipated.

This doesn’t necessarily require a recession, just a modest economic slowdown or softer data in what many are expecting to be a very strong 2025 could be enough to shift expectations toward additional easing. This would be bullish for the markets.

In my view, the Federal Reserve appears to be positioning for an extended pause. If we do see a rate cut, it is unlikely before May or June, given inflation’s historical pattern to run hotter during the first half of the year.

While I have previously noted the increased inflationary risks following the Trump election, it is still too early to have definitive conclusions about the impact of his policies.

While the potential for upward inflationary pressure exists, there is insufficient evidence at this stage to assert that inflation will accelerate meaningfully in the near term, but is in my view that we will continue to see stickiness in its developments.

The FED cut 25bps in the December meeting. But there was 1 dissent, and 3 other non members also dissented. Indicating further rate cuts will ve more difficult to get.

Only 2 more cuts are projected for 2025. They removed 2 from the forecasts, which was in line with expectations.

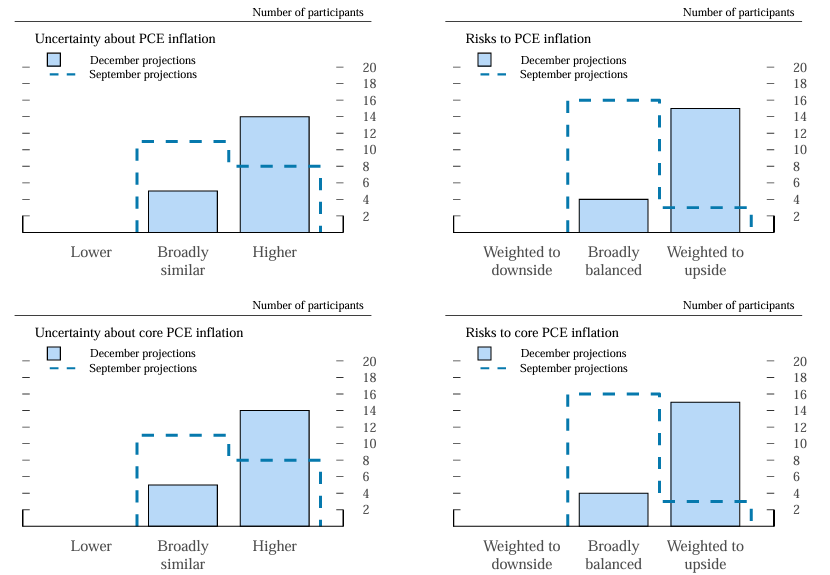

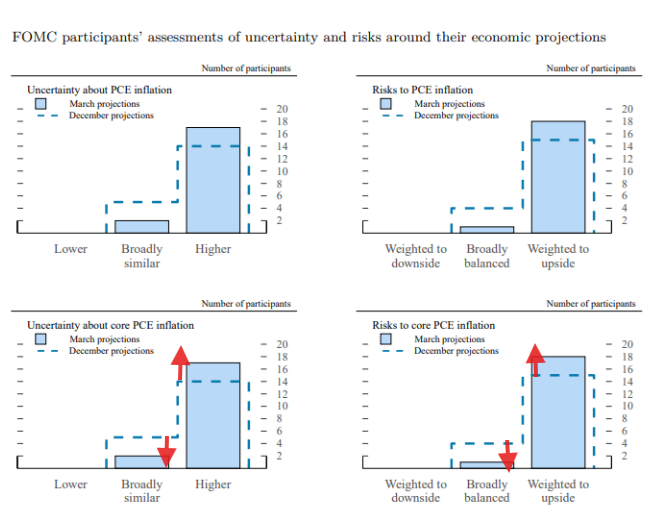

15 or 19 judged the risks around the inflation forecast (which were raised) were weighted to the upside. (only 3 in September). The Fed is now sifthing its focus to inflation risks.

The decision to cut rates was appropriate, they need to balance risk on both sides.

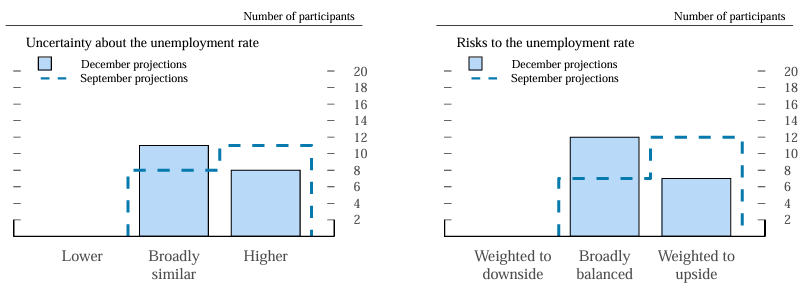

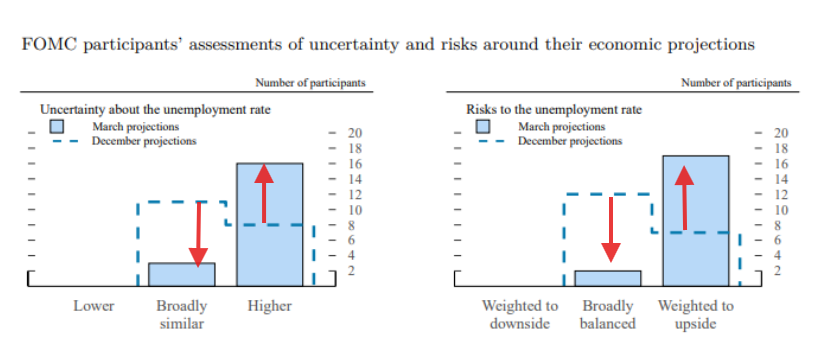

Labor market risks have diminished, but the market has loosened. Further loosening is not needed to achieve the inflation target.

Some Fed members factored fiscal policy uncertainty into their outlook, raising concerns about upside inflation risks in 2024.

Today’s decision was a closer call. Further cuts will depend on notable progress in reducing inflation or additional labor market loosening.

The decision for fewer cuts due to stronger growth, fewer unemployment

risks, closer alignment with the neutral rate, and greater uncertainty around inflation.

A more cautious approach is now deemed appropriate, monetary policy still remains restrictive, but they are now closer to neutral rate.

Chair Powell sees Core PCE inflation at 2.5% by 2025 as significant progress. Inflation is not expected to reach the 2% target until 2027.

The FED will not settle for inflation above 2%.

Inflation is moderating more slowly than anticipated, largely due to the slow adjustment in housing prices.

Long-term rates are responding to a robust U.S. economy compared to global peers.

A rate hike is unlikely but cannot be ruled out in today’s uncertain environment.

Key Points from the December 17-18 2024 FOMC Minutes

Inflation:

Inflation eased from its 2022 peak but remained somewhat elevated.

Core Personal Consumption Expenditures (PCE) inflation was 2.8% as of October, down from 3.4% a year earlier.

Some progress was noted, especially in core goods and market-based core services, with firms reluctant to increase prices due to consumer price sensitivity.

However, housing services inflation remained elevated, although slowing.

Risks to inflation were tilted to the upside due to:

Stronger-than-expected recent readings.

Potential changes in trade and immigration policies.

Persistent service sector inflation pressures.

Labor Market:

The labor market showed signs of gradual easing but remained solid overall.

Key indicators:

Unemployment rate increased to 4.2% as of November.

Nonfarm payroll growth slowed slightly, partially due to strikes and weather events.

Wage growth was 4% year-over-year in November.

Labor supply and demand appeared to be reaching better balance, with some indicators (like job openings and quits) moderating.

Risks were seen as balanced, but concerns remained that slowing payroll growth might eventually soften the labor market further.

Rate Decisions and Monetary Policy:

The Committee lowered the federal funds rate by 25 basis points to a target range of 4.25% - 4.5%.

Continued solid economic activity and labor market strength.

Some participants expressed concerns about persistently high inflation and argued for keeping rates unchanged.

The decision was accompanied by continued balance sheet reduction, with the Fed maintaining its commitment to reducing Treasury and mortgage-backed securities holdings.

The Committee emphasized data dependence, indicating that future adjustments will be based on evolving economic conditions.

Forward Guidance:

The Fed noted that while inflation was moderating, the process might take longer than previously expected.

If inflation persists, the Fed might hold rates at restrictive levels longer or slow the pace of easing.

Conversely, policy could ease faster if labor market conditions deteriorate or inflation moves sustainably toward the 2% target sooner

End of Balance Sheet Runoff:

Market participants’ expectations for the end of balance sheet reduction shifted slightly to June 2025.

This delay was mainly due to revised expectations among those previously forecasting an earlier end to the runoff.

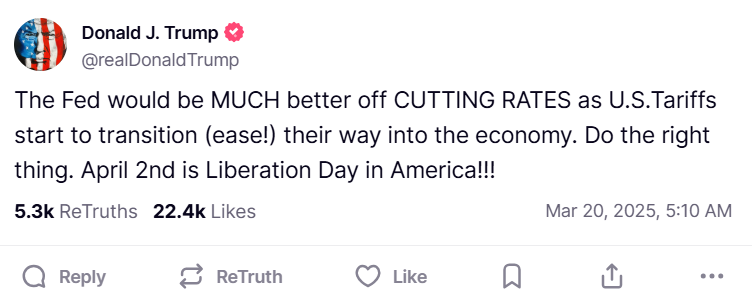

Trump said he will demand for interest rate cuts due to oil prices going down because of his new policies.

Assessment: I am currently giving the possibility of Trump influencing interest rates in the short term as low (below 15%), this assessment could change next year when a new chairman is appointed.

Trump’s options to directly interfere with the FED decisions are very low (Powell is not on good terms with him), and the ones he will most likely try are more indirect ways to try to influence the FED.

Trump options (with probability success on parenthesis):

Public or private pressure (medium): Trump is a good negotiator, we don’t know what original tactics he could use for this. But currently, he is not liked at all by Powell.

Appointing Dove-leaning Governors or followers of him (medium): requires senate approval, and this would be until next year. He can’t appoint new regional FED presidents though, lowering his success

Removing Powell (low): he can try to fire him, but the only way to succeed is if there is a justified cause or misconduct.

Legislative Push to change Law (low): very high impact, this could change the FED completely, but would need Congress approval, and probably a very slow process to complete

Devalue US Dollar (low): The treasury can exert control over the dollar, forcing lower rates for stability, but it is a very controversial policy overall due to the global implications, and don’t think it is likely

Use rhetoric or policy to create uncertainty in financial markets (low): he could create fear that could push the FED to act, but he is instead opting for policies that will stimulate the economy

Invoke emergency powers in extraordinary circumstances (low): The economy is currently performing okay

FED January Meeting Expectations: FED is expected to keep the federal funds rate steady at the current range of 4.25% to 4.5%

This pause is seen as a part of a cautious approach by the Fed, waiting for clearer signs of economic weakening or further progress on inflation before considering additional rate cuts

99% probability priced in for a hold in tomorrow’s meeting

Some of the analyst expectations or commented for the expected FED pause:

The economy is still running a bit hotter than expected. With GDP for Q4 expected to come in at ~3.2

Inflation progress has stalled out since the second half of 2024

All the fiscal policies proposed (tariffs, deregulation, taxes, immigration, oil drilling) create a lot of uncertainty, which is another reason to pause currently

Powell should signal a pause but without committing to a specific date because of all the uncertainty currently

Fed kept its key interest rate unchanged at a range of between 4.25%-4.5%, as was widely anticipated.

However, the post-statement said “inflation remains somewhat elevated” versus their previous statement which said inflation had made progress towards their 2% goal.

The committee now says unemployment rate has stabilized at a low level versus their previous statement which had noted an increase in the unemployment rate and easing of labor market conditions.

S&P 500 futures shed 0.8%, Nasdaq composite lost 1.1% while Dow Jones futures declined 0.4% briefly following the report.

Very inconsequential meeting to be honest (which seems it was his goal to not say anything important today), the only signal that was slightly hawkish in the report this time was completely dismissed by Powell in the press conference, and his tone this time instead sounded more dovish.

The FED still sounds without any clear direction and is extremely data-dependent, which I still think is adding to the huge uncertainty everyone is currently feeling.

Rates Expectations did not have any meaningful move after the meeting

The Fed is not in a hurry to make any adjustment to rates

Powell says he’s had no contact with President Trump and when asked to comment on his reaction to what Trump says, Powell’s response was, “it’s not appropriate to do so.” He says the public should be confident they will continue to do their job as always

On crypto, he thinks banks are able to serve customers as long as they manage risk.

Powell says removal of “inflation” line is just clean up to shorten sentence, not determination that inflation is rising again

Two last inflation readings have been positive, but they don’t want to overinterpret only 2 good readings, and want to see serial good readings for further cuts

The range of possibilities is very wide for fiscal policies, especially tariffs, and can’t really speculate on those yet to make policy

Reserves are still abundant, no date determined yet to end QT

He thinks still meaningful above the neutral rate (still restrictive), but that financial conditions are somewhat accommodative → IMO these don’t make sense together, one or the other. It seems the FED is really lost about the neutral rate.

I=5 Powell reiterates that they are in no hurry to cut interest rates

In remarks before the Senate Banking Committee, Powell reiterated that they don’t need to in a hurry to change interest rates and that the economy remains strong.

“With our policy stance now significantly less restrictive than it had been and the economy remaining strong, we do not need to be in a hurry to adjust our policy stance,” Powell said. “We know that reducing policy restraint too fast or too much could hinder progress on inflation. At the same time, reducing policy restraint too slowly or too little could unduly weaken economic activity and employment.”

He pointed out that current stance provides flexibility to deal with uncertainties.

“We are attentive to the risks to both sides of our dual mandate, and policy is well positioned to deal with the risks and uncertainties that we face,” he said.

Other comments from Powell February 11 2025 Speach

Overall hawkish tone from Powell again, it does seems they are very confortable with a pause until a significant scare on growth.

Bank reserves remain abundant, they are a long way away from ending QT

He believes neutral rate is meaningfully higher

They would only use QE again when rates are at zero

Powell says the Federal Reserve will never create a central bank digital currency (CBDC).

Powell says he is “struck” at the growing number of cases of Bitcoin and crypto firms that were debanked and he is “determined to take a fresh look at that.”

Powell stated they support establishing a regulatory framework for stablecoins to ensure consumer protection

Powell stated that there is *no time like the present" to put the U.S. budget on a sustainable path, subtly supporting fiscal hawks.

He emphasized that the Fed will follow the data rather than make premature judgments on trade policies.

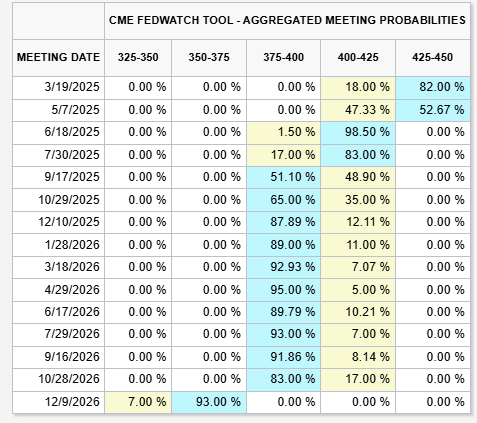

The market has now pushed a second rate cut in 2025 to December o even January 2026

Powell downplayed a bit the hot CPI reading from January 2025

This is the same FED that said 2021 was transitory, so I do have a hard time trusting anything they say after it.

Still he says the most likely outcome is to remain on pause.

Some of Powell’s quotes:

“I would say we’re close, but not there on inflation"

“Last year, inflation was 2.6% — so great progress — but we’re not quite there yet,” Powell said, referencing tp PCE

“So we want to keep policy restrictive for now,”

“We don’t get excited about one or two good readings, and we don’t get excited about one or two bad readings,”

“The underlying economy is very strong, but there’s some uncertainty out there about new policies,”

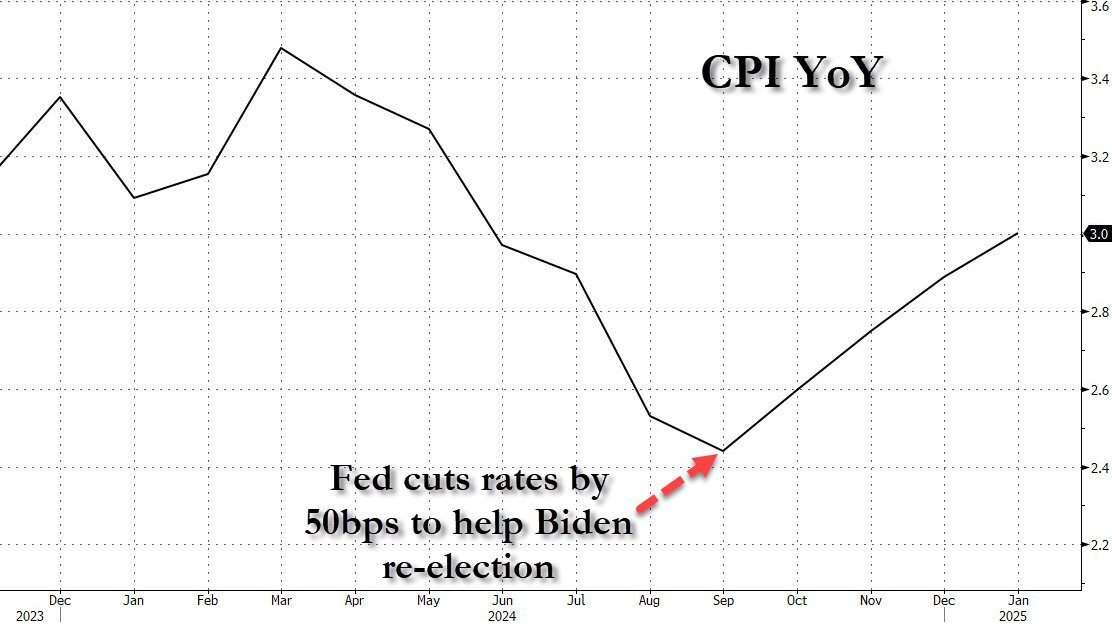

I dont think this was politically motivated as the image suggest by is interesting to realized that maybe that 50 bps cut in sep was not a good idea

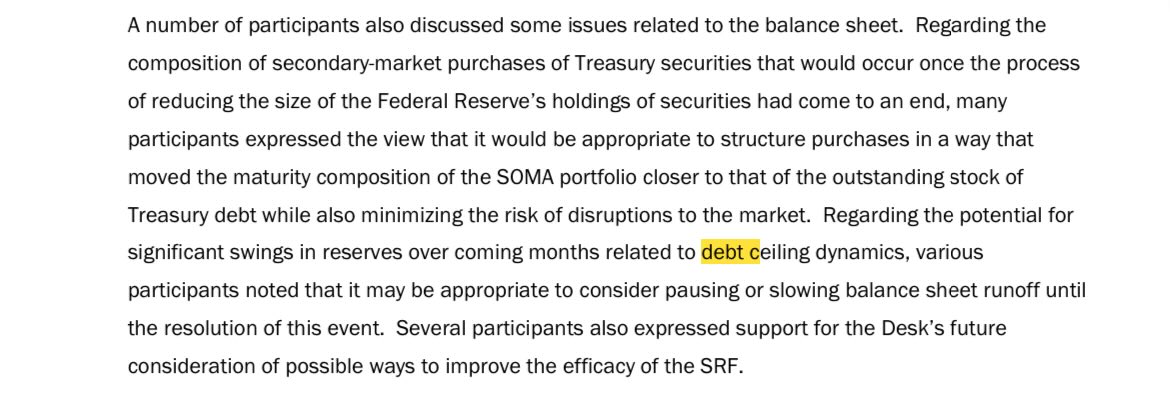

Some FED members discussed whether it would be appropriate to pause or slow QT temporarily due to potential swings in reserves linked to debt ceiling dynamics

Market expectations for the end of QT have shifted slightly later, to mid-2025, compared to prior expectations.

The Fed is considering potential changes to the maturity composition of its balance sheet once QT ends, aiming to bring it closer in line with the maturity structure of outstanding Treasury debt.

Fed noted that reserves remain abundant, but they could decline more rapidly than expected, requiring careful monitoring.

Reserves might decline quickly upon resolution of the debt limit and, at the current pace of balance sheet runoff, might potentially reach levels below those viewed by the Committee as appropriate

FED is expected to keep interest rates unchanged with a 99% probability according to market pricing

The first 2025 cut in June and the second one in September

FED expected to continue QT without changes at the March meeting, with expectations it might end around mid-2025, but there’s uncertainty due to debt-ceiling concerns.

Reserves are expected to be at $3.125 trillion by the end of the QT process, compared with $3.3 trillion now, while the level of the Fed’s reverse repo facility, a proxy of excess liquidity, is estimated to be $125 billion.

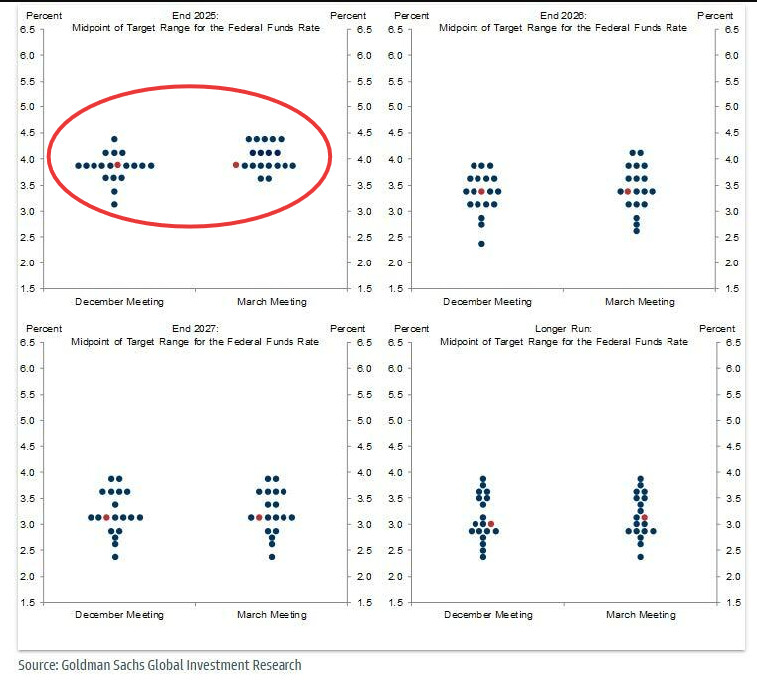

Tomorrow we also get new FED projections, there are expectations for the FED to most likely keep cuts at only 2 in 2025 despite recent growth concerns due to the equal upside risks to inflation due to Trump tariffs.

Analysts expect a mild economic downgrade, with GDP forecasts reduced and inflation estimates revised upward.

It seems likely to me we will these revisions on their economic projections since this is also the current trend most economists are reporting on their forecasts.

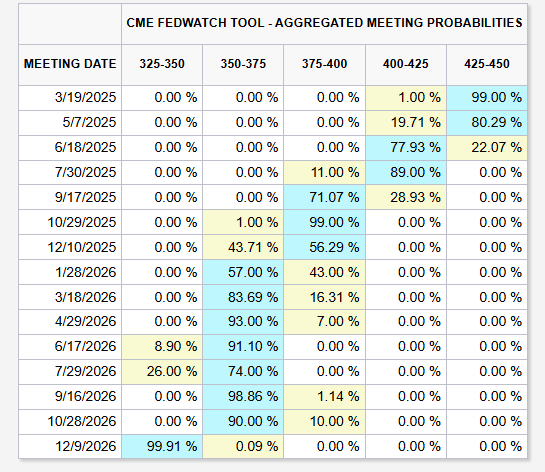

As a reminder the FED projected two cuts in 2025 to get to 3.9%, and 2 more in 2026 to 3.4%.

Any up or down revision will most likely mean a market reaction since the market’s current pricing is more o less in line with December projections.

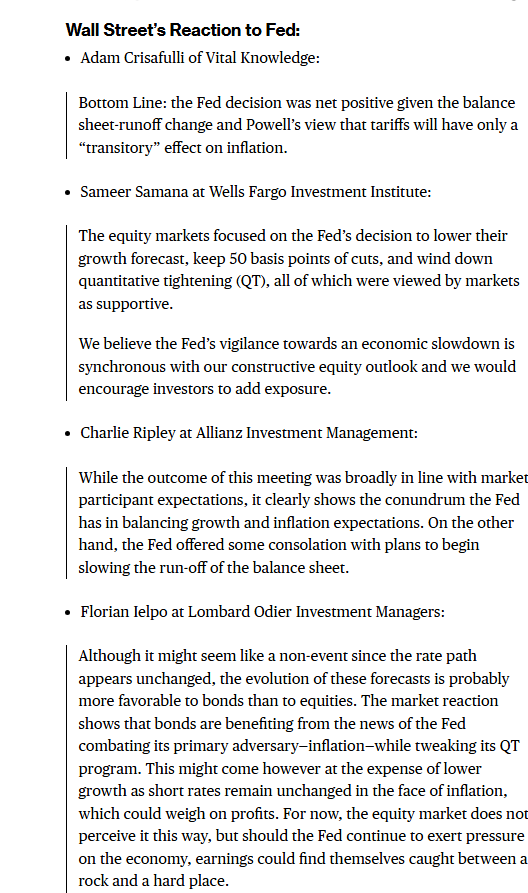

I=6 Fed kept interest rate steady as expected, still expects two rate cuts in 2025

Fed kept interest rate unchanged in the range of 4.25%-4.5%, as was widely expected.

The officials said they still see another half percentage of rate cuts in 2025, implying just two quarter-point cuts this year, unchanged from December.

The “dot plot” of officials’ rate expectations is now turning hawkish, with four officials now seeing no changes to rate cuts compared to just one in December.

The fed scaled back its “quantitative tightening” program, now allowing just $5 billion in maturing proceeds from Treasuries to roll off each month, down from $25 billion, though it left $35 billion cap on mortgage-backed securities unchanged.

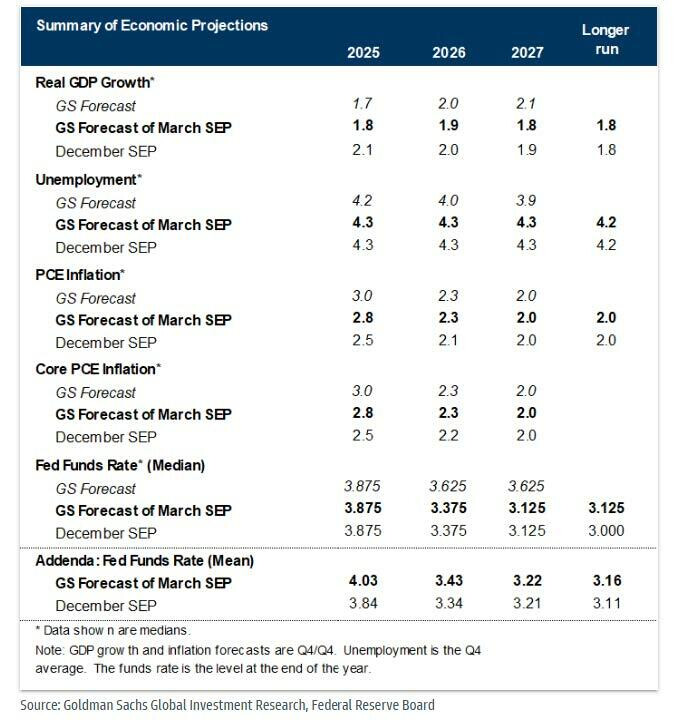

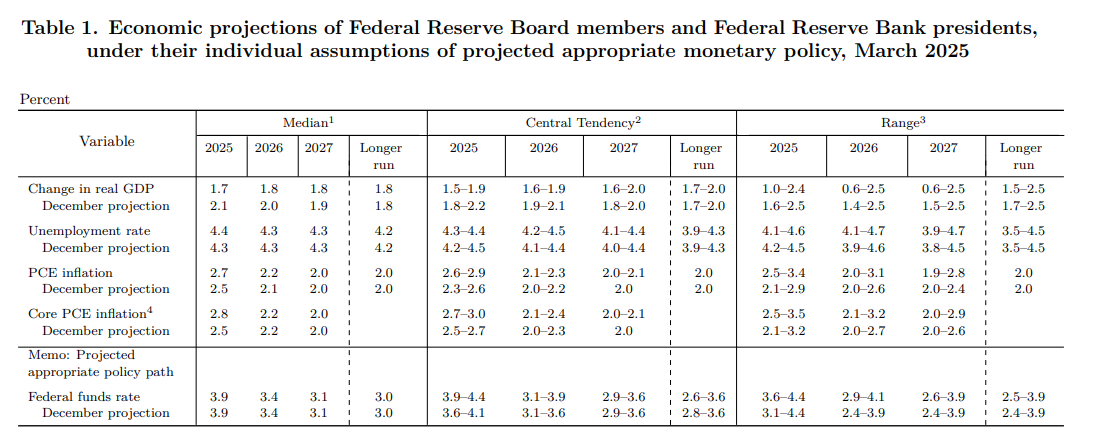

The officials lowered their projections for 2025 GDP growth rate to 1.7% from 2.1% and increased core PCE projection to 2.8% from 2.5%.

FOMC said “uncertainty around the economic outlook has increased.”

S&P 500 futures gained 0.8% while Nasdaq composite rose 1.2% following the report.

Despite some mixed signals, the market is mostly taking this as a positive/dovish meeting:

Despite the stagflationary feel in the new forecasts, the FED is still signaling 2 cuts in 2025 and the 2026, easing bias is still the base case.

The balance sheet run off of the US treasuries has almost been paused (only $5 billion a month), which was mostly unexpected and will help with some of the liquidity concerns that were present

Powell says tariff inflation could be transitory (being the FED I would have never said this after 2021 mistake, even if the logic/theory says tariffs create only a 1 time effect)

Particularly it seemed to me that the FED doesn’t really know what to do yet and what the economic impacts will be, especially clear after Powell said in similar words that “They have time to wait for more clarity because the uncertainty in forecasts is very high inside the FED”

The FED is really also at the expense of the fiscal policies, which are currently the primary driver of the economic outlook, and this is something where the FED can not do anything about it, and can only react to the consequences.

FED signals:

Economic projections: mixed (stagflationary)

Dots: hawkish

QT taper: dovish

FED Conference: Dovish

Cut Expectations did not change and the 10-year yield declined only 10 bps after the decision.

Fed Forecast assumes full tariffs retaliation, meaning worse case for now forecasted

Some of the rise in inflation, especially on goods, has been partly due to tariff, but separating the effects is pretty difficult.

Still early to have seen the full effect of tariffs on economic data

He thinks they are in a good place currently, and allows them to wait for more clarity on the outlook due to all the uncertainty currently

Powell thinks U Michigan’s inflation expectation going up significantly is an outlier for now, with other surveys and market base data not showing the same

Powell highlighted that the relationship between survey data and actual economic activity hasn’t been very tight recently

He thinks the FED’s tariff inflation base case is transitory, and they sometimes can look through this kind of inflation. Depending on the pass-through being fairly quick, and inflation expectations remain anchored.

Recession probability has increased in recent months, but still no super high