November 2024 CPI Assessment

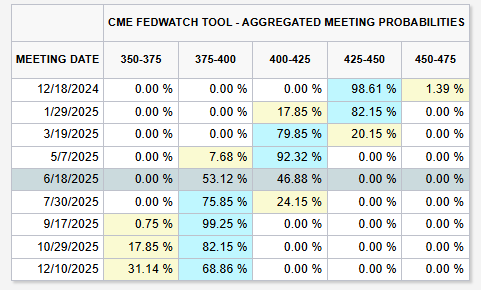

Despite recent stagnation in inflation progress, the market has grown more confident in the likelihood of a December rate cut after today’s report, while expectations for 2025 cuts remain unchanged.

Following Trump’s election, potential inflation risks could emerge. In such a scenario, I do agree it would be prudent for the Federal Reserve to adopt a more cautious approach until there is greater clarity on the trajectory of CPI, labor dynamics, and the specifics of forthcoming policy changes.

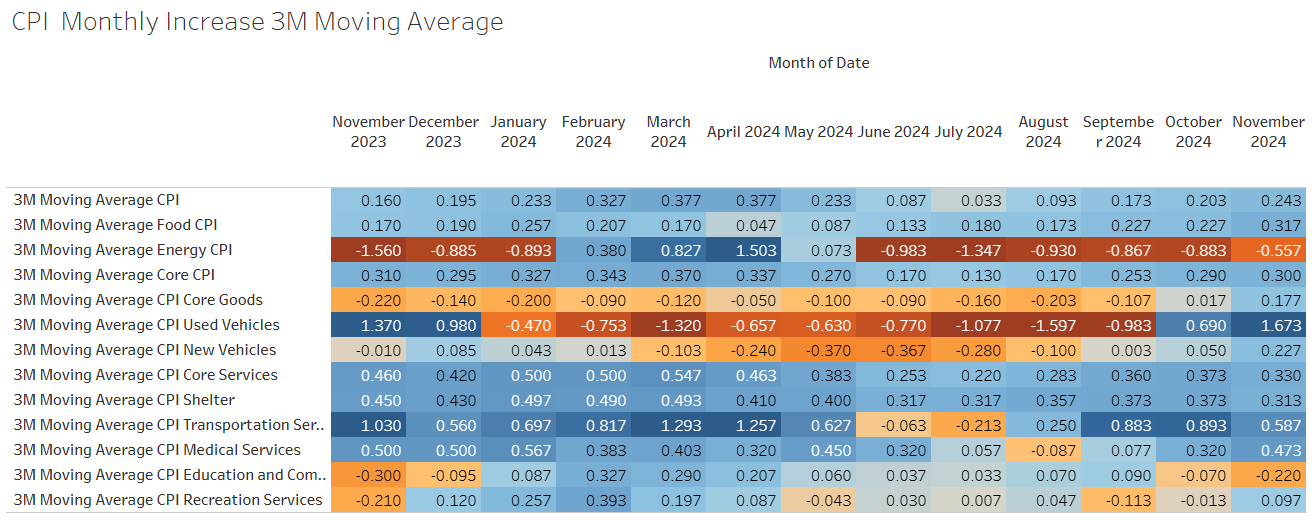

Monthly Increases for most components have been increasing in recent months

Shelter as usual made up the main portion of the rise in CPI, at almost 40%, although they did slow from the previous month.

- Owners’ equivalent rent component rose 0.23% on the month, which marked the smallest rise since the start of 2021.

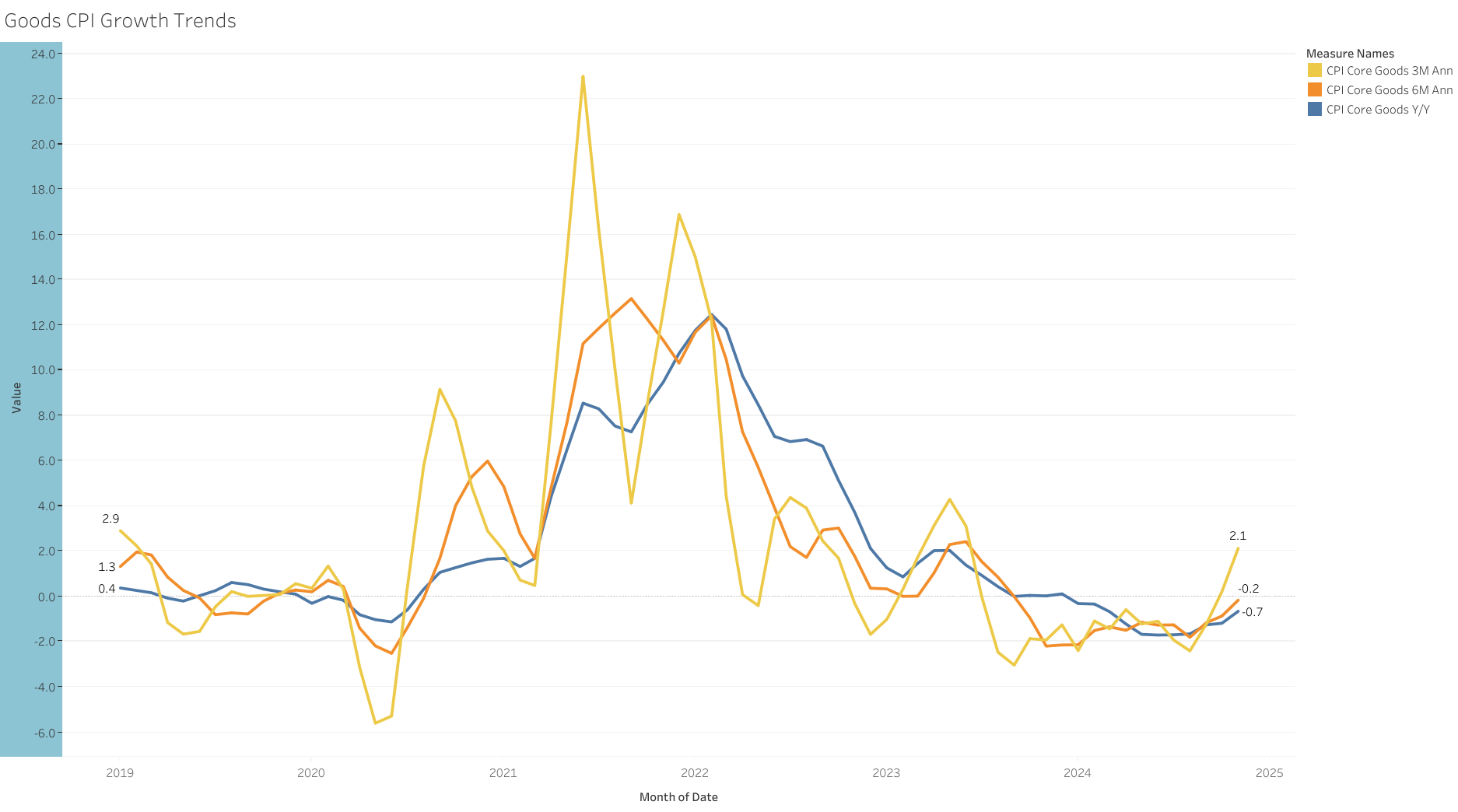

Used and New Car prices as mentioned above put upward pressure on goods CPI this month

Goods prices have played a key role in driving disinflation thus far, making it important to monitor any pressures in this area closely. While I do not anticipate a resurgence of inflation in car prices given the current industry dynamics, potential policy shifts related to tariffs under a Trump administration could temporarily alter this trajectory.

- Core Good increased 0.31% m/m, the highest since May 2023. The 3M annualized trend back into positive territory.

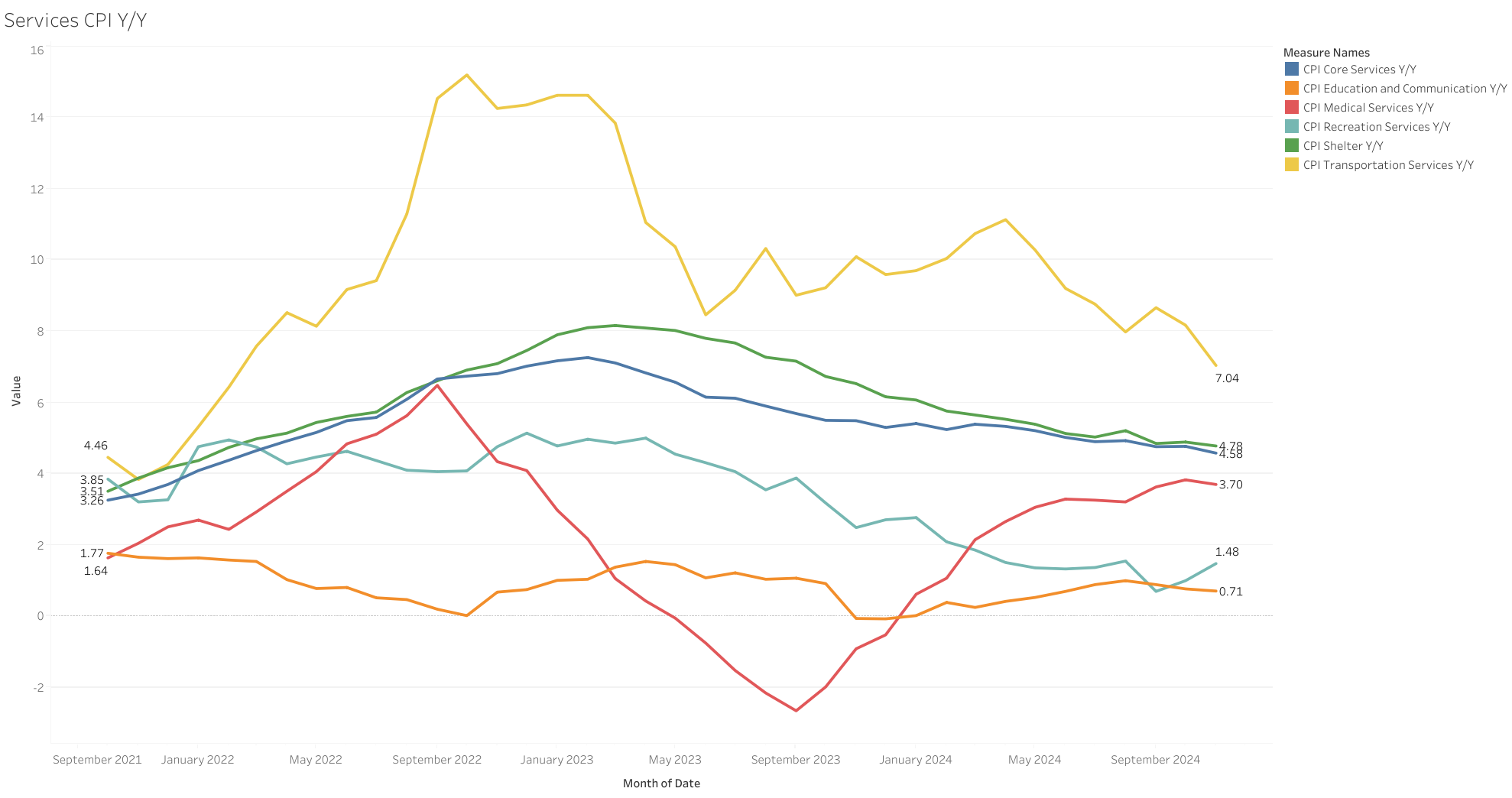

Transportation Services inflation continues to moderate, while medical services remain on an upward trajectory but stable this monte

Sources:

Data

Tableau Workbook