This topic covers Sixt’s Q2 2025 earnings. A preview of the results will be posted here ahead of the earnings release. A full summary of the preview is available in the Wiki:

Earnings date: August 13, 2025

Time of Earnings release: 7:30 CET

Time of Analysts Call: Unknown

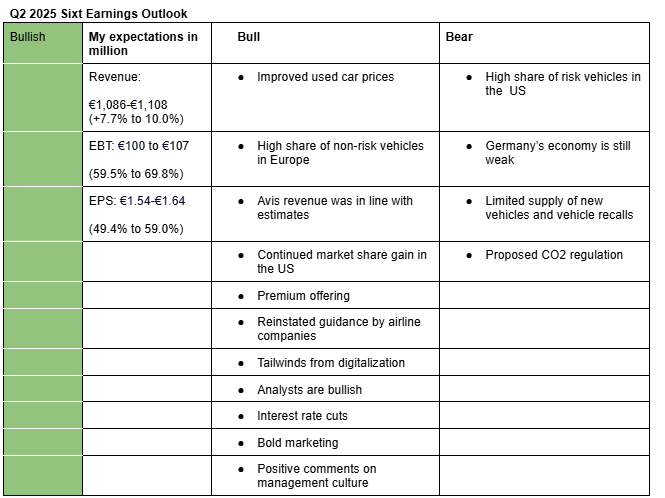

I am bullish on Sixt’s Q2 2025 earnings. My estimates (valuation model) take into account improved used car prices, positive commentary from Avis and other industry players, continued U.S. expansion, the premium nature of Sixt’s offerings, its fleet composition, tailwinds from digitalization, bold marketing, favorable remarks on management culture, and a potential revenue headwind from the macro slowdown in Germany. Here is a description of my bullish and bearish points.

Bullish factors

Improved used car prices: Auto1 Group data indicates that used car prices in Europe rose about 3% year over year during the quarter. This marks the first increase in two years. Likewise, Manheim data indicates that used car prices in the U.S. increased by approximately 5% year over year during the quarter. A decline in residual values has been one of the main factors behind the drop in Sixt’s earnings over the past two years.

Avis revenue was in line with estimates: Avis’s Q2 2025 revenue was flat y/y at $3.039 billion, in line with analysts estimate of $3.022 billion. In the earnings call, management said demand for car rentals is strong, especially in the leisure segment ( Business to Business (B2B) and Business to Partner (B2P) sales channels account for 72% of Sixt’s revenue-page 17). It also pointed out that pricing is stabilizing. Its International Revenue per Day (RPD) rose 7% y/y while Americas Revenue per Day (RPD) was down 2% y/y. Commentary from the Sunny Cars CEO on pricing and demand during the quarter was also positive.

High share of non-risk vehicles in Europe: Sixt’s share of non-risk vehicles in Europe is now almost 100% compared to at the end of 2023 when it was 87%. This means that Sixt is now in a better position to dispose off its used vehicles in Europe than in Q2 2024.

Continued market share gain in the US: Sixt continues to make strides in the US. For instance, the new Delta Air Lines SkyMiles partnership, the first of its kind in United States keeps the U.S. growth story in focus. Also, Avis flagged Sixt during its Q2 2025 earnings call, saying it stepped up competition this year.

Premium offering: Around 50% of Sixt’s fleet are composed of premium vehicles. Sixt’s premium positioning commands 30%-40% higher average revenue per unit compared to Avis and Hertz, according to S&P Global. This premium focus provides resilience during periods of macro slowdown.

Reinstated guidance by airline companies: Both Delta Air Lines and United Airlines see upside to their 2025 earnings due to stabilizing demand.

Tailwinds from digitalization: Sixt’s digitalization efforts are expected to enhance operational efficiency, resulting in cost savings for the company and time savings for customers. For example, its Car Gate inspection technology is designed to materially reduce repair costs. Data from Hertz indicate that similar AI-based inspection systems lead to three times more billable damage than the industry average. Similarly, Sixt’s in-house tech division, which consists of 731 employees and has deployed over 100,000 software updates in the past year, gives it a competitive edge in the AI era. This technological capability could prove especially valuable in dynamic pricing, where personalized price offerings are emerging. Notably, there are reports that airline companies are testing AI-powered dynamic pricing models.

Analysts are bullish: Jefferies, DZ Bank, Deutsche Bank and Warburg Research analysts expect Sixt to post solid results for Q2 2025.

Interest rate cuts: The ECB’s key interest rate now stands at 2%, down from 3.75% in June 2025. This reduction should lower Sixt’s interest expenses over time, supporting earnings and freeing up capital for investment.

Bold marketing: Sixt’s provocative political-themed advertising has long been central to its marketing success. While some feared this strategy might fade after Erich Sixt stepped down as CEO, the company has continued to launch bold campaigns that consistently draw public attention. Former CMO Tobias Seitz is said to have left the company after his creative freedom was curtailed. However, the continued strong performance of part of the marketing division helps ease concerns about Sixt’s management culture.

Positive comments on management culture: Moritz interaction with a former Sixt employee who reported directly to Alexander Sixt was positive. In addition the CEO of a direct competitor to Sixt told

Moritz that Sixt is performing well when it comes to Software and has a good performance culture.

Bearish factors

High share of risk vehicles in the US: At the end of 2024, Sixt’s share of vehicles not covered by repurchase agreements stood at 87%, up from 75% in 2023. This means that its depreciation of rental vehicles in North America may not fall significantly in 2025.

Germany’s economy is still weak: Germany’s GDP shrank by 0.1% in Q2 2025, signaling continued weakness in one of Sixt’s largest markets.

Limited supply of new vehicles: Avis stated in its Q2 2025 earnings call that tariffs are causing OEMs to delay vehicle production and deliveries, leading to postponements in its in-fleet schedule. Most vehicles in Sixt US fleet are imported. This may lead to higher maintenance costs, residual value risk, and margin pressure. Avis also flagged vehicle recalls during the quarter, which affects 4% of its US fleet and could affect vehicle supply in summer and 2026. It said that vehicles recalled cannot be sold.

Proposed CO2 regulation: The EU Commission is drafting a regulation that would ban rental companies from purchasing internal combustion engine (ICE) vehicles starting in 2030. Although the likelihood of it passing is low, the surrounding uncertainty could weigh on the share price in the short term.

Here are analysts estimates for Q2 2025 and FY2025:

Q2 2025 analysts estimate for EBT: €107.8 million (+71.5%)

Q2 2025 analysts estimate for EPS: €1.63 (+58.14%)

Q2 2025 analysts estimate for revenue: €1,070 million (+6.2%)

2025 analysts estimate for EBT: €440.3 (+31.4%)

2025 analysts estimate for EPS: €6.74 (+30.23%)

2025 analysts estimate for revenue: €4,269 million(+6.7%)

Management guidance for 2025:

2025 revenue guidance: €4,202 to €4,402 (+5% to +10%)

2025 EBT guidance: €420.2 to €440.2 (+25.8% to 31.8%)

Hertz’s Q2 2025 revenue was in line with estimates, while EPS beat expectations; management flagged vehicle recalls as a headwind

Hertz Q2 2025 revenue fell 7.1% y/y to $2.19 billion, in line with analysts estimate of $2.17 billion while EPS came in at -$0.34, above analysts estimate of -$0.45.

Hertz said in the earnings call that pricing remained challenged during the quarter but is starting to improve.

Hertz also said demand continues to improve.

Like Avis Budget Group, Hertz is also affected by vehicle recalls, which impact about 2% of its fleet.

Depreciation Per Unit Per Month (in whole dollars) fell 58% y/y to $251 million due to strong residual values achieved through fleet rotation.

Assessment

Hertz confirmed that vehicle recalls are a common problem and could affect Sixt’s infleeting for this summer and next year, especially if tariffs impact the supply of parts. This topic may be worth investigating further.

Sixt Q2 2025 revenue and earnings met expectations, management reiterate its guidance for 2025

Sixt Q2 2025 revenue rose 7.4% y/y to EUR 1.08 billion while EBT rose 70.8% y/y to EUR 107.3 million, both in line with analysts expectations of EUR 1.07 billion and EUR 107.8 million respectively.

Diluted EPS rose 62.2% y/y to EUR 1.67, above analysts estimate of EUR 1.63.

Sixt maintained its 2025 guidance which includes revenue revenue in the range of EUR 4.2 billion to EUR 4.4 billion (+5% to 10% y/y) and EBT in the range of EUR 420 million to EUR 440 million (EBT margin of 10%).

Sixt revenue from Germany rose 1.5% y/y to EUR 292 million (my estimate: +0.43% y/y), revenue from Europe rose 14% y/y to EUR 456 million (my estimate: +9% y/y), revenue from North America rose 5% y/y to EUR 335 million (my estimate: +17% y/y).

Depreciation of rental vehicles fell 35% y/y to EUR 147 million, below my estimate of EUR 171 million.

Assessment

Overall, results were in line with estimates but some reports indicate the print was not as significant as expected. This likely explains why shares were down 6% pre-market and are down 3.4% at open market.

North America revenue showed significant weakness in Q2. This was offset by strong performance in Europe, but if the current trend persists, Europe may no longer be able to compensate, leading to potential revenue pressure at the Group level. Current trends, however, indicate that demand is improving as uncertainty around tariffs diminishes.

Analysts said Q2 results were solid, maintain positive ratings on strong pricing and utilization

Buy, €105: Jefferies said Sixt Q2 2025 results were solid and in line with expectations. It expects good profitability in the coming quarters driven by solid pricing discipline and stronger than expected pricing demand. Jefferies pointed out that Average selling prices (ASPs) was up 1.7% y/y, supported by robust pricing environment and solid vehicle utilization.

Buy, €125: Warburg research said Sixt met expectations in Q2 2025.

Metzler analyst Stephan Bauer said Sixt’s Q2 EBT was somewhat weaker than he and the market expected.

Buy, €110: Baader Bank said Sixt’s Q2 2025 results were solid, even though it slightly fell short of expectations.

Outperform, €106: Oddo BHF pointed out that Q2 results were in line with expectations. It expects the summer season to be supported by robust pricing environment and high vehicle utilization rates.

What exactly caused the America business to be so weak? Could we have predicted that before the results have been released? Are there learnings we can draw to get more precise in our models over time? (E.g. including other sources that we did not incorporate or weigh insights differently)

Same question for Europe which was surprisingly strong.

Overall I would always also note how results came in compared to our expectations. Given that you had been a bit more positive compared to analysts expectations I think it missed your expectations by some small margin?

CFO Weinberger told the German Press Agency that revenue in US was weak since they kept their fleet there somewhat smaller due to the current uncertainty. Weak US dollar also contributed to the weakness in North America.

Sixt said Europe revenue was strong, boosted by travel demand to popular holiday destinations in the Mediterranean region, such as Spain and Italy and expansion of branches (6 new airport branches and 27 new downtown branches).

I am not sure if we would have predicted that by relying on the same data. Maybe we need to expand our data footprint and change our we model them.

Yeah, revenue missed my midpoint estimate by EUR 14 million but EBT was above my midpoint estimate of EUR 104 million.

Can you remind me to which degree they hedge their currency exposure? Do we have a Notion page dedicated to the currency topic for Sixt yet?

I ran a couple of GPT prompts and found the following insights very interesting. I did not investigate further but in case you find them to be true we could just have gained a few additional sources for insights. I by now think it is imperative that we always investigate with GPT before all earnings to see if we miss anything or if it has additional arguments and also look for other peoples opinions e.g. on Seeking Alpha. Ideally this workflow should lead to improved sources and predictions on our side as well. (I think we should have certainly highlighted the U.S. pricing and demand problems before the earnings call in more detail/as a focus area.)

(Note: Not sure if reposting parts from GPT here is a good workflow. The upside is that it is fast but if segments repeat themselves too much it’s certainly not good. I just wanted to share different levels of details as those replies have slightly different angles, while i am short on time. If the time is there to create a better more comprehensive overview that’s certainly better. - We could for example store the outputs of GPT in Notion as always, create a short overview here + link to the full Notion outputs for everyone wanting the full details)

GPT: So…what’s the problem in the U.S. rental market right now?

Recent prints from U.S. peers and market trackers point to a common set of headwinds:

Pricing has softened.

Hertz said the market pricing declined mid- to high-single digits in Q2.

Avis reported revenue per day down ~1% YoY with rental days flat in Q2.

CarTrawler’s Q2 2025 Market Monitor shows a typical U.S. 5-day rental for July (booked Jan–Jun) at $531, ~8% below last year.

Demand mix & travel flows are less helpful.

Phocuswright notes the U.S. car-rental market cooled in 2024 and is in a “more measured phase” for 2025; inbound travel to the U.S. is forecast to fall ~9–10% in 2025, pressuring peak-season pricing power in gateway markets.

Residual values & fleet economics are still normalizing.

2024 saw falling used-car residuals hit earnings (Sixt highlighted this, especially in North America). Depreciation metrics are improving in 2025 (e.g., Hertz DPU down to $251), but the pricing softness offsets some of that relief.

Operational friction.

Recalls and new-vehicle delivery timing have been called out by peers as near-term headwinds, creating utilization and cost noise even as fleets get tighter/more efficient.

Details

What’s pressuring the U.S. market (2025)

Inbound international demand is weak.

Multiple data points show 2025 inbound to the U.S. running below 2024. Tourism Economics (Oxford Economics) now projects ~8% fewer international overnight arrivals in 2025 vs. 2024, and says June data confirm the slide. U.S. Travel’s dashboard also flagged a YoY decline in total travel spending in June—the first since 2021.

Pricing (rate) softness.

CarTrawler’s industry monitor highlights softening retail rates in major rental markets through Q2 2025, reflecting pushback from price-sensitive leisure travelers and less buoyant inbound demand. (CarTrawler’s Q2 2025 Market Monitor).

Costs are still elevated ex-depreciation.

Vehicle upkeep and branch operating costs haven’t deflated: BLS shows motor-vehicle maintenance & repair up ~6.5% YoY in July and auto insurance up ~5.3% YoY—both key line items for rental fleets.

Residual-value volatility.

After big swings in 2023–24, used-car prices have been choppy in 2025 (e.g., a June jump—the biggest monthly rise in a year), complicating timing of de-fleeting and resale proceeds.

Policy & tariff risk.

New/anticipated tariffs on China-sourced vehicles/parts are a direct cost overhang; Hertz explicitly warned that such tariffs could raise fleet costs.

Peer-to-peer competition isn’t gone—but it’s wobblier.

Turo withdrew its IPO and cut ~15% of staff in April; that eases competitive heat somewhat at the margin versus 2022–23, especially for price-led leisure.

Macro travel tone cooled into summer.

Overall U.S. travel spending fell 0.4% YoY in June, hinting at softer domestic momentum right when rates usually peak (airport-heavy rental mixes feel this quickly).

Avis Budget Group (CAR, US) — revenue steady, profit thin.

• Revenue $3.0bn (flat YoY).

• Net income $5m; Adj. EBITDA $277m. (Release Jul 29, 2025.) ir.avisbudgetgroup.com

Hertz (HTZ, US) — best quarter in ~2 years, still GAAP-loss but big improvement.

• Revenue $2.185bn (–7% YoY).

• Net loss –$294m (vs –$865m LY).

• Adj. net loss –$104m; Adj. Corporate EBITDA ≈ $1m (vs –$460m LY).

• Ops: utilization 83% (+300 bps), DPU $251 (down from $595 LY). (Release Aug 7, 2025.) ir.hertz.com

Europcar Mobility Group (EU) — H1 shows pressure.

• H1 revenue €1,528.7m (–2.0% YoY).

• Adj. Corporate EBITDA –€52.2m; Net loss –€268.8m. (Report Jul 29, 2025.)

Why U.S. rental feels worse than Europe right now

Heavier exposure to airport & inbound leisure (still soft),

Rate resistance from domestic leisure after two expensive summers,

Higher ongoing operating costs (repairs, insurance), and

Policy uncertainty hitting vehicle cost planning (tariffs, EV residuals).

(See sources above.)

Outlook (next 6–12 months)

Demand: Domestic should be flat to slightly down into late 2025; inbound likely remains down mid- to high-single digits for full-year 2025 per Tourism Economics, with any rebound more a 2026 story.

Rates: Expect low- to mid-single-digit YoY declines on average vs. 2024 through Q3/Q4 as operators trade price for utilization; shoulder periods could be weaker where inbound typically fills gaps. (CarTrawler monitor).

Residuals: Volatility persists; companies that de-fleet tactically and lean into better-selling trims should do relatively better if used prices roll over again after the mid-year bounce.

Policy risk: Tariff path is a wild card; any broadening to parts or non-China sources would pressure fleet capex and elevate break-even RPDs.

What to watch (practical signals)

NTTO monthly arrivals and U.S. Travel’s spending dashboard for signs the inbound/domestic drag is abating.

CarTrawler/OTA rate trackers for pricing inflection into holiday periods.

Used-car indices (Manheim/Cox) for residuals direction.

Peer commentary (Avis/Hertz) on RPD & utilization each quarter to confirm stabilization.

If you want, I can turn this into a one-pager (problems → KPIs → base/ bear/bull scenarios) you can drop into your InvestmentWiki brief.

Can you give me some more insights what peers have been saying? What do you expect for 2026 and beyond? Any predictions how this market should develop over the long run?

Absolutely—here’s what peers are saying right now, and a grounded 2026+ outlook for the U.S./North America rental market.

What peers are saying (Q2-2025)

Avis Budget (CAR)

• Q2 revenue $3.0bn, Adj. EBITDA $277m. Ops lens: rental days ~flat YoY and RPD down ~1%, but utilization up and fleet costs lower, so Americas EBITDA rose; also launching premium product “Avis First.”

• Strategy: leaning into premium + ops partnerships — multi-year Waymo deal (Avis to run fleet ops for Waymo’s Dallas robotaxi launch). That’s a tell on “beyond daily rental” positioning.

Hertz (HTZ)

• Best print in ~2 years on cost discipline: DPU $251 (below sub-$300 goal), utilization 83% (+300 bps YoY), and MY2025 fleet locked at pre-tariff pricing; also pushing retail car sales to maximize residuals.

• Big context: 2024’s EV overhang is still the cautionary tale (large EV sell-down/write-downs) — hence today’s focus on “buy/hold/sell right.”

SIXT (North America)

• Q2 North America revenue €334.6m (+4.8% YoY) with a sharp EBITDA swing back to positive; but mgmt flags a “politically challenging and highly volatile” U.S. backdrop and a very competitive market. (NA trails Europe on growth.)

Distribution & demand color (not fleet-owners but crucial signals)

• CarTrawler sees U.S. prices softer: a 5-day July rental averaged $531, ~8% lower YoY; EV rentals are still a niche (~6% of NA rentals).

• U.S. Travel Association: June travel spend −0.4% YoY, first YoY dip since 2021; inbound & air metrics softer.

• Booking Holdings’ CEO warns U.S. inbound is weakening due to harder border/visa experience (and fees).

Residuals / used-car backdrop

• Manheim: wholesale used prices have stabilized with modest YoY gains; monthly moves remain choppy (June up; July eased slightly). That’s better for depreciation planning than 2024’s whipsaw.

What this means for 2025 H2 (synthesizing peers + data)

Rates (RPD): gentle downward pressure (Avis: −1%; CarTrawler: −8% on a 5-day basket) as leisure demand normalizes and inbound softens. Operators are defending margins via utilization, mix, and fleet costs instead of price.

Costs: insurance/repair inflation still a grind (BLS has motor-vehicle insurance +~5% YoY as of June), so the peers’ emphasis on depreciation control and younger fleets continues.

Demand: domestic steady to mixed; inbound is the drag right now.

2026 outlook (base / bull / bear)

Base case (most likely):

Inbound recovery off a weak 2025 aided by mega-events (World Cup ’26), but constrained by visa/airport throughput unless fixes land. Expect mid-single-digit volume growth, RPD flat to +2%, and margins supported by normalized depreciation.

Bull case:

Policy fixes + mega-event tailwinds → strong inbound bounce, airlines add lift, OTAs + direct push demand; RPD +3–5%, high 70s–80s utilization across majors; residuals benign.

Bear case:

Visa bottlenecks/tariffs persist; used-car prices wobble; travel demand softens with macro → flat/negative RPD, utilization slips, margin gains limited to operators with best cost control and retail disposal channels.

2027–2030 (structural trajectory & where the profit pools shift)

Distribution mix keeps tilting direct/loyalty. Phocuswright pegs supplier-direct at 44% now, ~47% by 2028 → brands with sticky apps/loyalty and premium tiers (e.g., Avis First) gain yield and lower CAC.

EVs: slow, pragmatic ramp. Rentals remain single-digit share in NA near-term; expect low-teens by late decade as model variety improves and operators price for residual risk. (Hertz’s 2024–25 reset is the caution flag; CarTrawler shows ~6% share now.)

Autonomy: ops revenue adjacency emerges. Fleet-ops/maintenance for AV networks creates a new B2B revenue line (Avis-Waymo Dallas is the template; more cities possible 2026–28).

Residuals normalize. With Manheim near-flat to modestly rising YoY, depreciation should be far more predictable than 2023–24, rewarding “newer fleet + retail disposal” strategies.

Cost inflation stays above CPI in insurance/repair. Even if headline CPI cools, these categories tend to lag; operators will keep pushing younger fleets, telematics-driven claims, and airport mix optimization.

Peer-to-peer: still a factor, but 2025 retrenchment (IPO pulled, ~15% layoffs at Turo) suggests less pricing pressure than 2022–23.

My call (actionable takeaways)

2025: Pricing is the weak link; winners are the ones nailing utilization + cost per day + disposal (Hertz’s DPU/utilization step-ups are the blueprint; Avis’ premium push pads mix).

2026: If visa/airport fixes materialize, expect rate stabilization and volume support from events; otherwise, growth skews to Europe/LatAm outbound rather than U.S. inbound.

Long run: Margin expansion is less about RPD and more about ops (depreciation discipline, retail sales channels, loyalty/direct, AV fleet-ops contracts). The market should grow at low- to mid-single digits through the cycle, with peaky summers moderated by smarter revenue management and a steadier residuals backdrop. (Synthesis of sources above.)

If you want, I can also map this into a base/bull/bear model (RPD, days, utilization, DPU) you can drop into your InvestmentWiki piece, with footnoted sources.

Sixt does not hedge the currency impact on its U.S. revenue. Its currency derivatives are used to manage FX risk from euro-denominated funding of non-euro subsidiaries (covering both principal and interest), not to protect reported revenue ( Sixt’s Fx impact). According to GPT 5 (Notion), the euro strengthened against the dollar by roughly 4.7% in Q2 2025 compared to Q2 2024. That’s around 2% more than in Q1.

Those are interesting insights but I think Sixt reported weaker North America revenue because it tightened fleet in expectations of weaker quarter not because demand or pricing weakened significantly. Both Hertz and Avis said in their earnings calls that demand and pricing continue to improve.

Avis’s US revenue per day (RPD) fell 2% y/y to $70.06. That was an improvement from Q1’s RPD of $64.78 or -3% y/y.

Hertz revenue per day (RPD) fell 6% y/y to $56.08, a sequential improvement from Q1’s RPD of $53.68 or -5% y/y.

CFO Franz Weinberger stated in the earnings call that business in July was according to the plan, Berenberg analyst said

Hold, €90: Berenberg analyst Yasmin Steilen said CFO Franz Weinberger stated in the earnings call that business in July was according to the plan but predictability of developments for the rest of the year is low.

Buy, €105 to €110: Jefferies analyst Constantin Hesse expects a solid third quarter for Sixt as travel activity is likely to be strong in the summer months.

Buy, €105->€103: DZ Bank analyst Dirk Schlamp said Q2 results were in line with expectations but he reduced his revenue and earnings estimates for 2025 and 2027.

North America revenue grew 11% y/y FX-neutral versus 4.8% in euros

Sixt said in its Q2 2025 analyst presentation that North America revenue grew by 11% year-over-year on a constant currency basis, compared to 4.8% growth in euros.

Sixt changed the definition of its premium vehicles to include models from Porsche, Volvo, and Maserati, taking the share of premium vehicles to 57% compared to 49% last year.