Mohamed El-Erian is the Allianz chief economic advisor of Allianz and former PIMCO CEO and Co-CIO.

He is a regular guest on Bloomberg and CNBC and is highly knowledgeable.

I liquidated my entire stock portfolio in Feb 2020 shortly before the market crashed, after listening to his urgent warnings about the impending shock and studying the characteristics of the virus.

He stayed cautious while the market has been at its lows. (1,2,3)

His overall stance might be balanced with a bias to be cautious and careful.

Mohamed El-Erian on current conflic and economy, he sounds much more cautious than what he did before:

Markets currently trading as if Israel’s conflict is contained, but if not the case, the outlook will be for a weaker economy along with inflationary pressures. This needs to be a constant question for investors and not something given

He is mostly worried if there is scalation and more parties start to get involved

Current uncertainties are a combination of geopolitical risks, policy mistakes, and insufficient growth

We currently have a significant move higher in yields, a significant rise in oil prices, and a significant rise in the dollar. Those 3 factors combined usually break something in the financial system according to him

We seem to not be done with interest rate risks yet, and we still have credit and liquidity risks in the background.

He thinks currently we are living in a world of inflexible supply, and the FED needs to acknowledge 2% target could not be realistic to get as quickly as they desire, before making another mistake.

Hmm the latest point about inflexible supply is pretty good. @Magaly can you open a new topic for USD strength? I think we could either look at DXY, EUR/USD, other indices like e.g. Bloomberg Dollar Spot Index or eventually create a basket our own to measure global Dollar strength and discuss developments and reasons for those developments.

Mohamed El-Erian: Most people entered 2023 very pessimistic, and the upside surpise until now in 2023 has instead made the market overly optimistic about 2024, he thinks consensus forecast about 2024 are too optimistic about the global economy, but the baseline isn’t either a finantial accident

November has been great because of 4 factors aligning:

Goldilocks data for the economy

Lower oil prices

Lower yields

Lots of money to be put to work after the correction

However, 3 of these factors are facing headwinds that question the sustainability of the movement. Not forecasting a major sell-off, just a consolidation until there is more clarity on these factors.

Goldilocks data is unlikely to persist

Yields are going to face significant debt auctions where the buyers are in question

OPEC+ probably going to react to the significant decline in oil prices

Currently, he thinks, there are a lot of structural changes going on, and no one should be held hostage by any certain view. The world is currently very fluid which doesn’t allow for high conviction for any event, and being open to changing views quickly will be key.

The world thinks always of normal distributions for events, where there is a predominant event and tail events with much less probability. He thinks we don’t live in that world anymore, currently is a multimodal world, where very different outcomes could have equal probabilities because there is not enough information/foundation before the events, and therefore analysts need to be open to all possibilities. (5:00)

What can we do to manage the current high uncertainty (29:00)

Resilience: In a world that is highly fluid investment mistakes will be more common, the important step is to have a resilient business that can afford mistakes and be able to respond to the new reality.

Agility: Be able to move quickly enough when things start to become more clear one way or the other

Optionality: Build enough intellectual optionality and portfolio optionality to be able to change our minds.

His current scenarios (12:00):

US growth slows down, but no recession, with inflation stuck at 2.5-3%. The FED will let inflation run slightly higher, and no issues in the financial markets → Highest probability but no highly dominant (60%)

FED makes another policy mistake because it does not realize we are entering an insufficient supply world, and overtigh due to this, not cutting rates when needed. (30%)

Financial system can’t handle the amount of refinancing thats is coming at higher interest rates in all sectors of the economy. (10%)

Why he thinks the FED makes mistakes (16:00):

They get stuck in their analysis, not using real-time evidence to change its views, and end up reacting when is already to late Eg. Inflation transitory in 2021

Communication is not consistent, the markets is always misinterpreting their intentions.

Forecasts have been consistently wrong in the same direction, no much learning from past mistakes

The FED has no accountability. It’s still the 1 only big central bank to not give answers as to why it got its inflation call wrong in 2021

The fact that Powell is not an economist makes him extra dependent on data to make decisions, they need cognitive diversity in the FED to have different views of the same problem. The FED can not be extra excessive data dependent because the data is already backward-looking, and the tools on top of that act with a lag.

Current challenges in the economy (27:00)

Have lost the ability to grow in a balanced and inclusive manner for everyone and the planet

Current policy mistakes. Policymakers get stuck in the past, without realizing when there are significant structural changes in the economy. There is a behavioral problem of accepting new changes because of the challenges it could bring.

The Fed is overlooking the greater risk of acting too late, which could lead to a more pronounced economic slowdown (35% probability that the Fed will act too late).

Rate cuts starting in December 2024 will already be too late, the lagged effects will be biting even more.

The financial cushions of small businesses and households have eroded—pandemic savings are depleted, debt levels are high, and delinquencies are rising.

Households and small businesses are now entirely dependent on income, with no savings buffer or access to debt as before. Any disruption in the labor market could cause exponential, rather than linear, economic deterioration.

The Fed was shaken by the “inflation is transitory” mistake, which has led to excessive caution, becoming excessively data-dependent. They need the courage to adopt a more forward-looking approach.

The 1995 soft landing succeeded because the Fed cut rates pretty early. All other hiking cycles ended in recession because the Fed tended to be late. The current Fed being so reactive, and overly data-dependent is risking being very late.

Thank you for those insights. It’s quite important to see as a reference what great economists are thinking.

I think it would be pretty cool to establish greater links between his insights and our research. As an example, he speaks about depleted savings & high debt levels.

It would be interesting to link those statements to our own research on the topics to see what exactly the data shows and how much we are agreeing with his statements.

Yes, I agree that it would be beneficial to contrast their opinions with our research.

In this case, I mostly agree with his perspective, and I value that he always discusses topics in terms of probabilities.

I also fear the FED will be too late because of the concern about inflation because I have been noticing a deceleration in consumer spending growth as of late.

So, in terms of data:

Consumer:

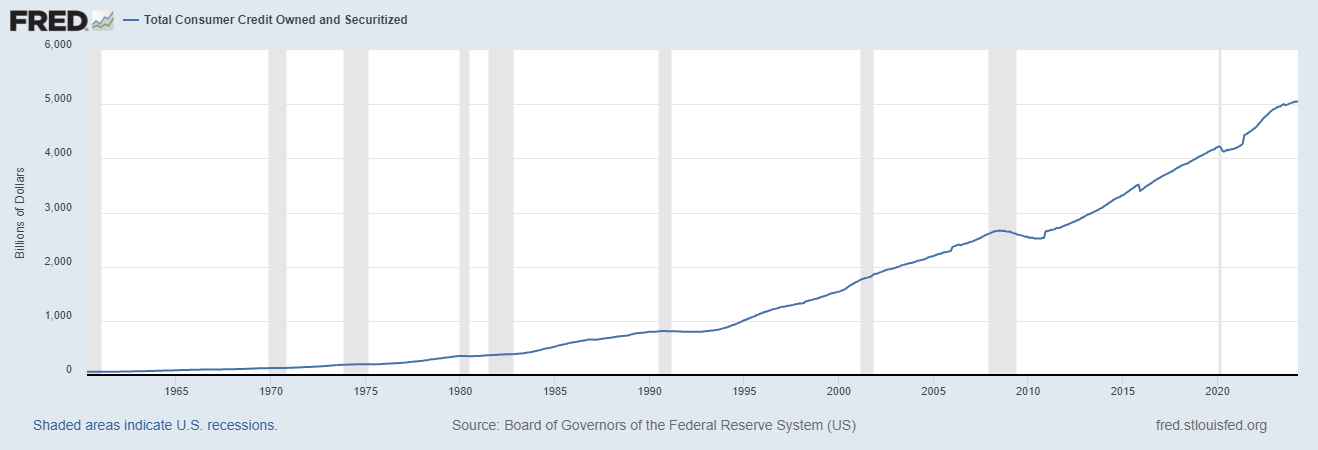

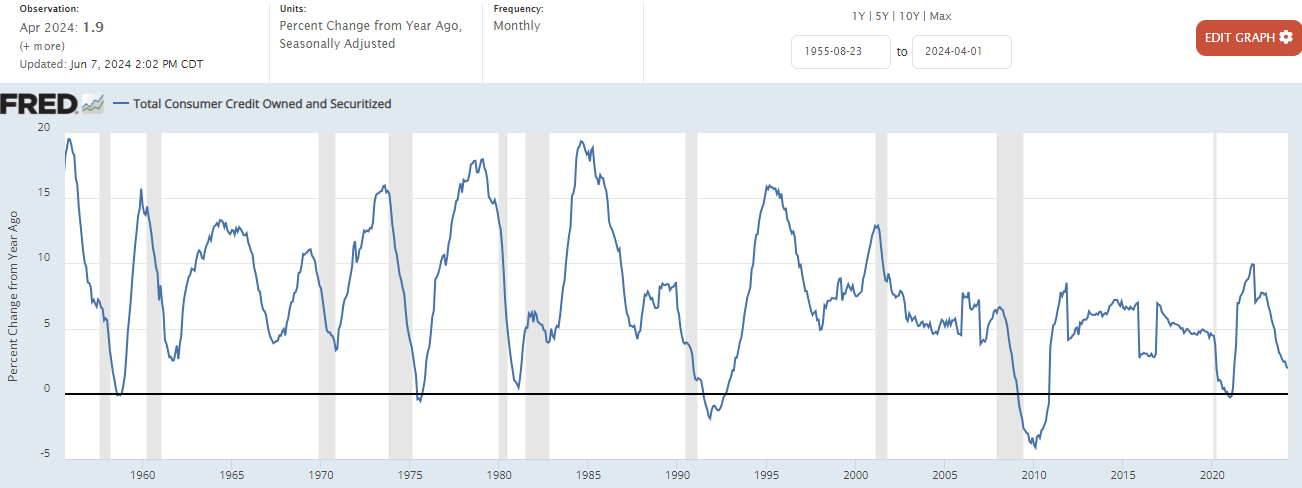

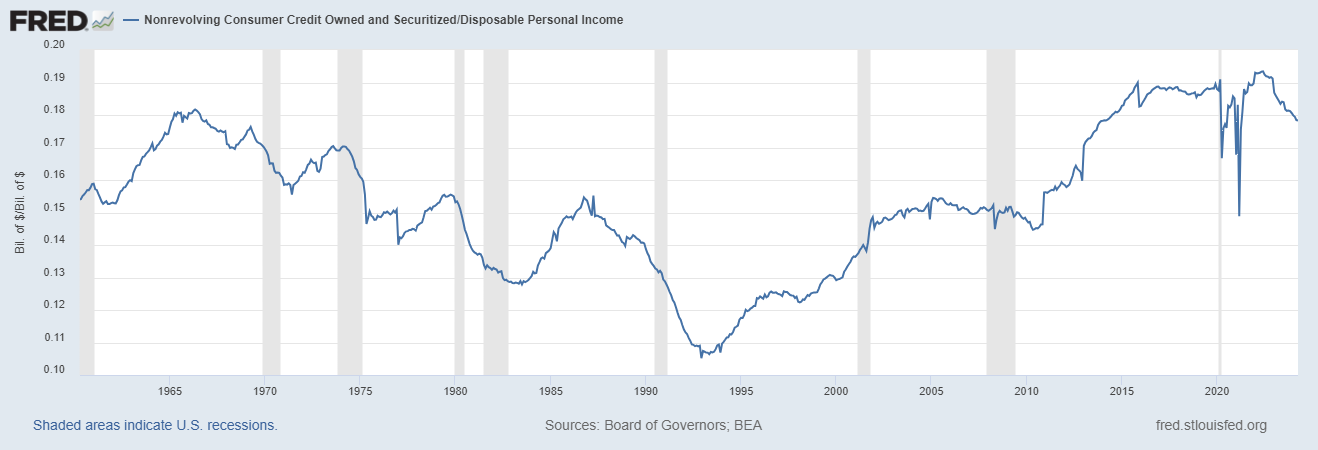

I previously mentioned, the primary source of consumer spending is currently income. This is because the growth rate of consumer credit is very low and continues to decline.

I have been reporting the concerning sharp increase in delinquencies for credit cards and auto loans, and they are expected to continue increasing since the share of consumers that are maxed out is expected to rise.

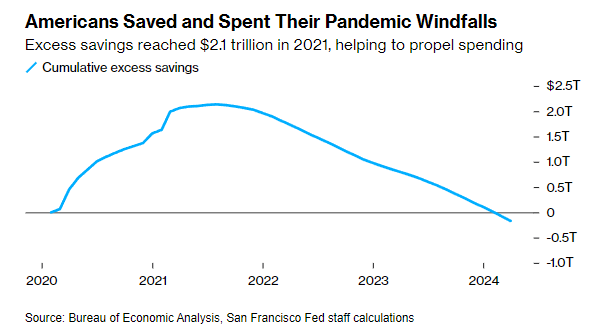

I have also been noting the very low savings rate in the US consumer, with limited potential for further decrease. And according to the SF Fed, excess savings have already been depleted since March 2024.

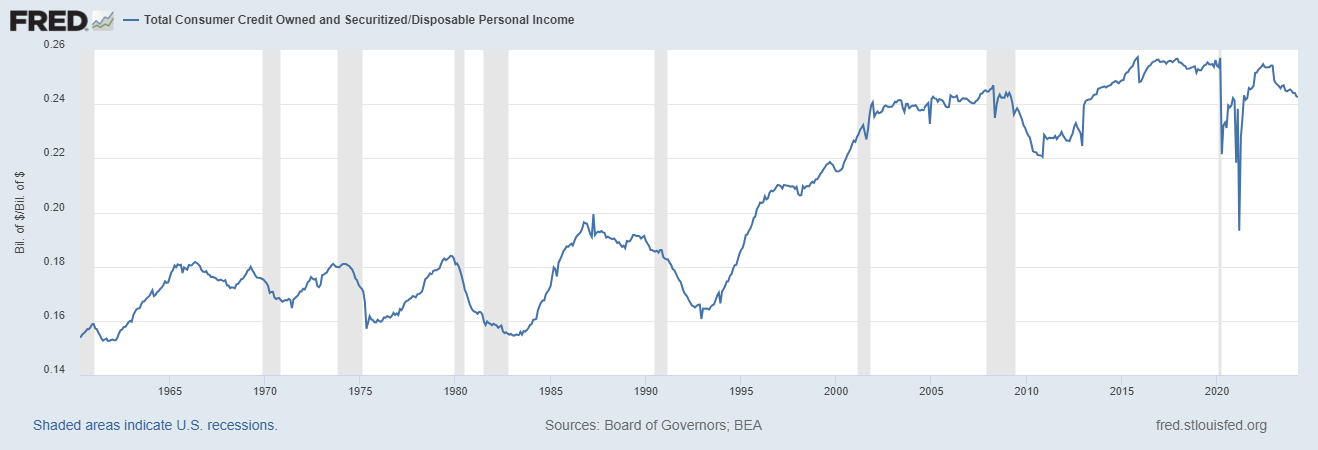

While debt-to-income levels are better than in 2008, they remain high. And this does not stop short-term issues related to credit accessibility and tough bank standards to effect the economy, especially with delinquency increases.

Also, what got better after 2008, was mostly mortgage debt (and revolving too), because consumer credit to income remains at similar levels, more especially due to the increase in non revolving debt (auto loans mostly) increases.

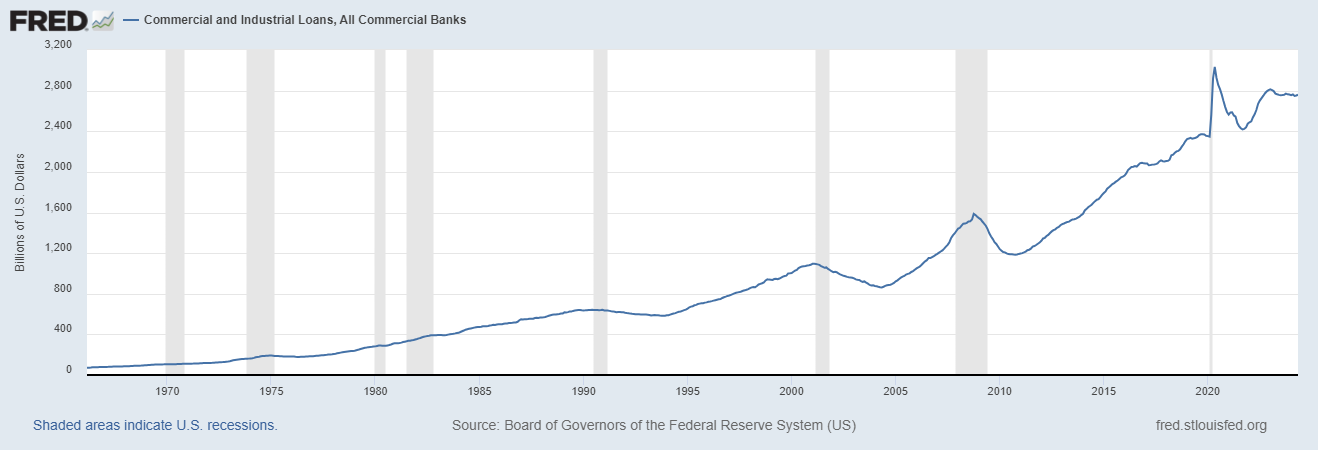

Small businesses have been struggling for a long time and have not shown any significant improvement since then.

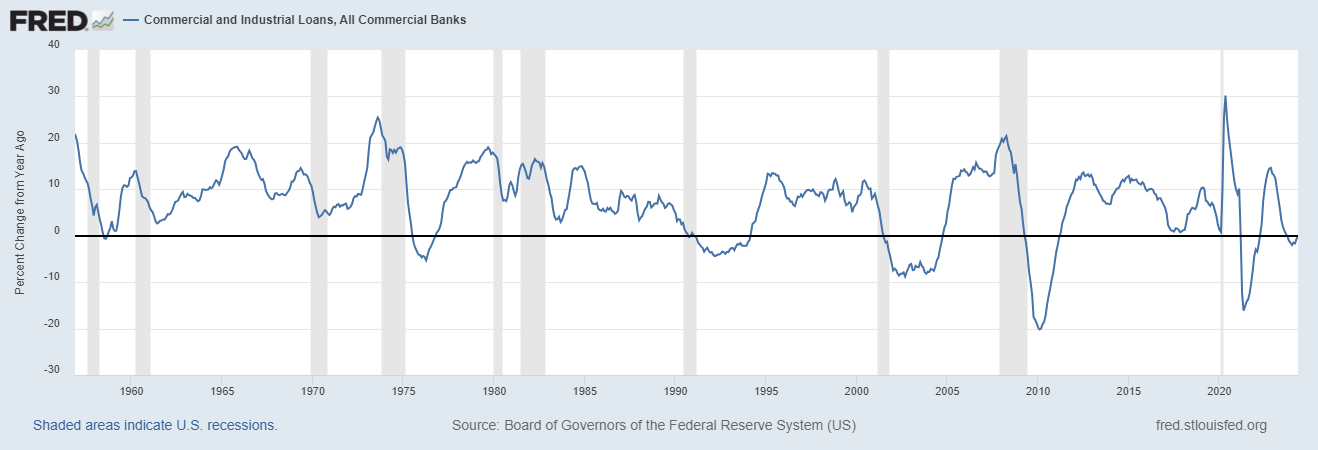

Business loans are currently experiencing negative growth but stabilizing recenty. There is little incentive and accessibility to borrow and invest at current rates.

Bankruptcies have been increasing significantly over the past year, recognizing they are starting for a very low level, but growth rate is significant.

The maturity wall is approaching, especially for small businesses, with interest rates remaining high.

I agree that the current economic tcycle still positive growth is primarily driven by income, but this is the goal of monetary policy to slow the growth of money and credit creation.

Continued weakening in the labor market will likely cause further slowdown, and this deterioration is unlikely to be linear. Because economic problems are never linear, they often intensify rapidly once they begin to be more evident

Mohamed Increased Recession Probability, see 2025 growth at 1.5% - 2%

Recession probability has risen from 10% to 25-30%, with a “growth scare” likely despite the economy’s structural strength.

The 2025 outlook has weakened as consumer and business confidence declines, raising concerns about a potential economic slowdown into 2026.

Tariffs and policy uncertainty are not temporarily, adding persistent risks to markets and business investment.

The market initially underestimated the short-term negative effects of tariffs, assuming quick benefits from deregulation and tax cuts, but the negative impacts are being felt first.

Investors should focus on risk management, with small investors avoiding forced exits due to volatility and institutions using a barbell strategy—balancing high-quality yields with selective opportunities.

The Federal Reserve may need to reconsider its 2% inflation target as the economic landscape undergoes structural changes.

Economic growth could slow below 2%, approaching “stall speed,” where administration goals become more challenging

Market expectations for Fed rate cuts have shifted from one to at least three, reflecting rising concerns about employment and economic stability.