This is the discussion topic about commercial real estate.

Commercial real estate is in a difficult situation, especially in the United States, and is one of the risk factors for a systemic credit event.

We currently assess the probability of an event like that as low, given the strong balance sheets of larger banks which might buy smaller banks if they get into trouble.

WeWork is currently trading at levels that are indicating a complete wipeout of equity holders is likely.

This does not automatically mean the company will collapse as it could be restructured in bankruptcy but continued losses make downsizing or a collapse more likely. (700million losses in Q2 and a warning about client cancellations)

In the meantime, its CEO and CFO left the company.

WeWork rents in total 20 million office sqft, more than any other company in the United States according to Stijn Van Nieuwerburgh, a Columbia Business School professor who specializes in real estate.

He notes:

A collapse of WeWork could be a “systematic shock” to the weak commercial real estate sector in New York, San Francisco and other cities.

It would pour more cold water on the office market, which is struggling direly,”

My Assessment:

I lack experience with those numbers, therefore it is hard for me to visualize them, put them into perspective or assess them. Compared to information in the Wiki that predicts 1.1 billion sqft of office space being vacant at the end of the decade in the United States the number looks manageable.

Additionally, WeWork is at 70% occupancy rate and what ultimately interests us is how banks manage commercial real estate stress and they might hold up irrespective of developments in local markets. So chances of any impact are low in my opinion.

It would be interesting though to get a better sense of numbers and understand e.g. how large the office sector in cities like new york or san Fransico is, how much of it is vacant already and how much additional supply could come to the market from a company like WeWork, just to get a better feeling of the overall picture of what is happening.

For reference: Meta agreed to rent 1.5million sqft at three towers in NY in 2019 and returned 250,000 sqft of them in 2022. The empire state building has an total floor area of 2.77 million and it’s usable floor area is 2.25 million.

To be honest Wework as an isolated event, don’t think will have a significant impact. Since there is already 1B sqf vacant, just an approx. 2% increase. For me is just more of an additional sign of the current stress.

Concern for me comes from the fact the Wework buildings are obviously not the only ones being vacant. And the fact, that the maturity wall is relatively soon.

The only systemic risks coming from CRE I could see are enough smaller banks failing at the same time, that big banks are unable to absorb them all on time. Which imo probably a low probability.

Other than that, the credit risks will mostly just materialize in more tightening of credit conditions. However, I am still unsure due to lack of knowledge if this tightening in credit could have a systemic event in any other market.

Here (pg. 14) are the statistics by city in Q1, these are the 1rs 10 by vacancy sqf:

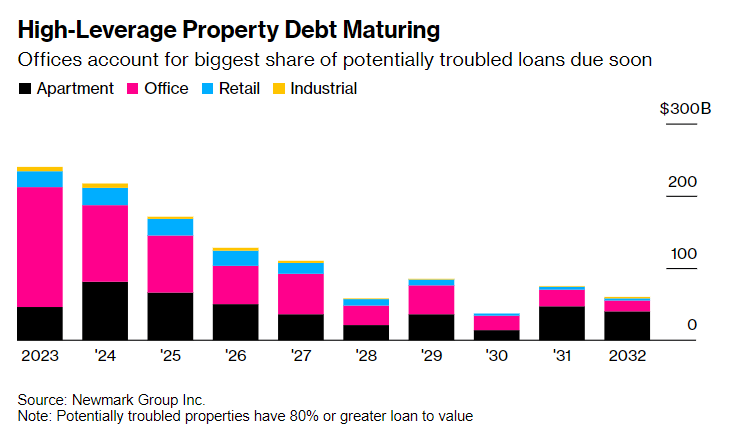

About $1.2 trillion of debt on US commercial real estate is “potentially troubled” because it’s highly leveraged and property values are falling, according to Newmark Group Inc.

Banks, which have tightened lending since this year’s collapse of Silicon Valley Bank, carry the biggest share of at-risk debt, with $303 billion of potentially troubled loans maturing through 2025, according to Newmark.

I sometimes wonder if we and markets are being complacent with CRE, and not putting enough attention to it. Much as they were doing in 2008 with the very obvious crisis in housing.

If not a systemic event, maybe it could trigger a hard stop in lending, making any economic slowdown worse.

Interesting article by WSJ, is a good read if it can be done

Banks’ exposure is even bigger than commonly reported. The banks are in danger of setting off a doom-loop scenario where losses on the loans trigger banks to cut lending, which leads to further drops in property prices and yet more losses.

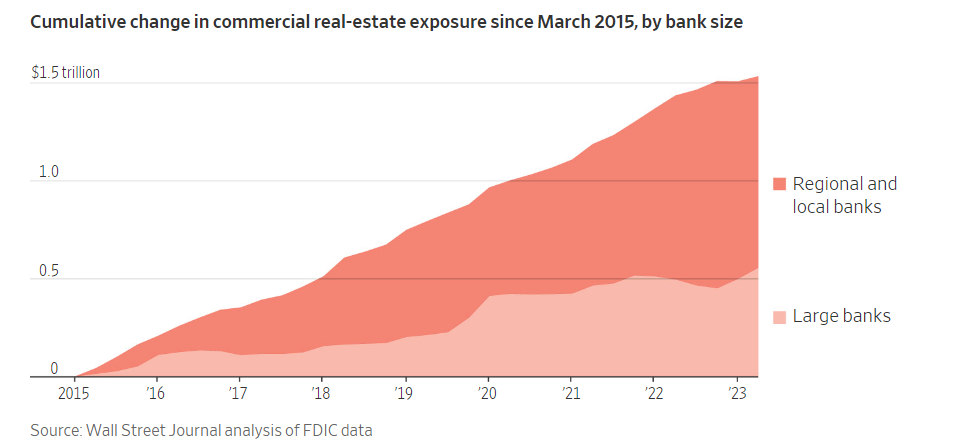

Banks roughly doubled their lending to landlords from 2015 to 2022, to $2.2 trillion.

Banks with less than $250 billion in assets held about three-quarters of all commercial real-estate loans as of the second quarter of 2023. They accounted for nearly $758 billion of commercial real-estate lending since 2015, or about 74% of the total increase during that period.

The volume of commercial property sales in July was down 74% from a year earlier, and sales of downtown office buildings hit the lowest level in at least two decades. When deals begin again, they will be at far lower prices

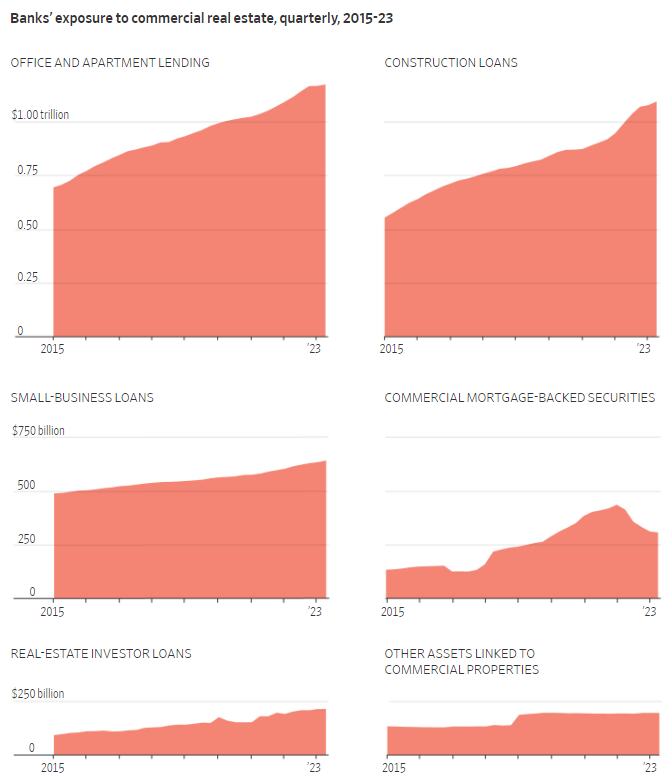

Over the past decade, banks also increased their exposure to commercial real estate in ways that aren’t usually counted in their tallies. Indirect lending brings banks’ total exposure to commercial real estate to $3.6 trillion. That’s equivalent to about 20% of their deposits.

Between 2015 and 2022, banks more than doubled their indirect real-estate exposure. That included loans to nonbank mortgage companies and to real-estate investment trusts that own and operate buildings and lend to landlords. It also included investments in bonds known as CMBS. Banks boosted lending to small businesses that used property as collateral as well. Holdings of CMBS and loans to mortgage REITs and other nonbank lenders accounted for about 18% of the nearly $3.6 trillion in commercial real-estate exposure in 2022

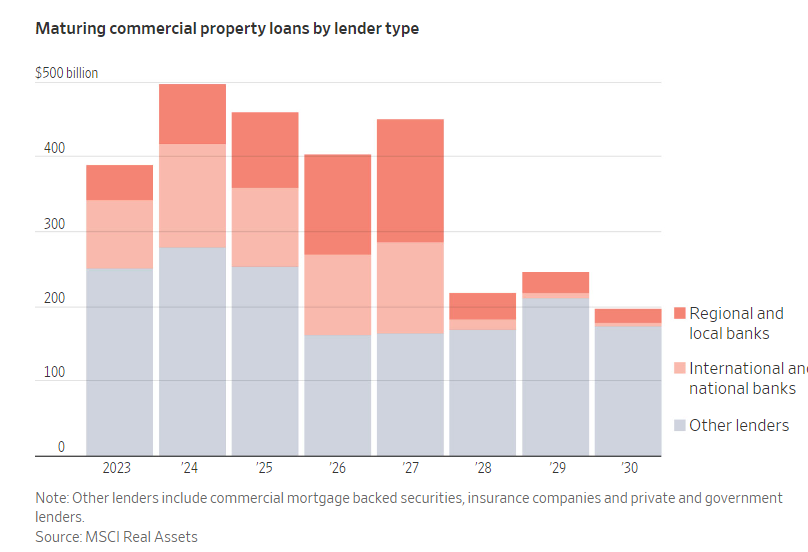

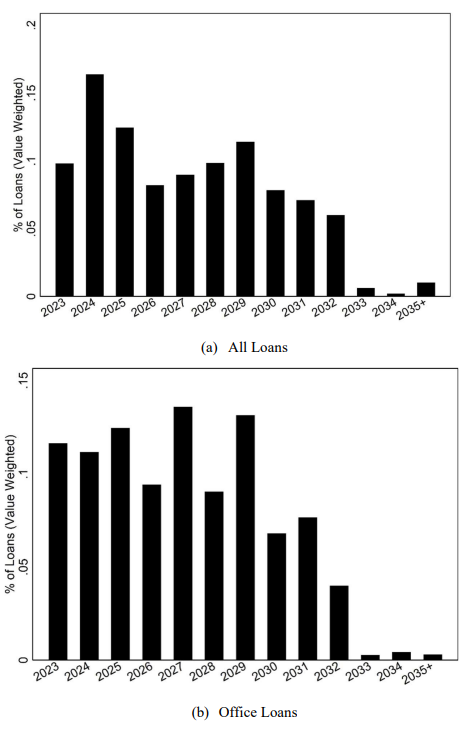

Roughly $900 billion worth of real-estate loans and securities, most with rates far lower than today’s, need to be paid off or refinanced by the end of 2024.

Example of type of discounts happening:

In early 2021, an affiliate of Brookfield Asset Management borrowed $465 million in CMBS and other debt against the Gas Company Tower, a 52-story office building in downtown Los Angeles.

At the time, appraisers valued the property at $632 million, according to Trepp, up from a valuation of $517 million when Brookfield bought the building in 2013. When the loans came due this February, the owner defaulted. An appraiser earlier this year cut the building’s estimated value to $270 million.

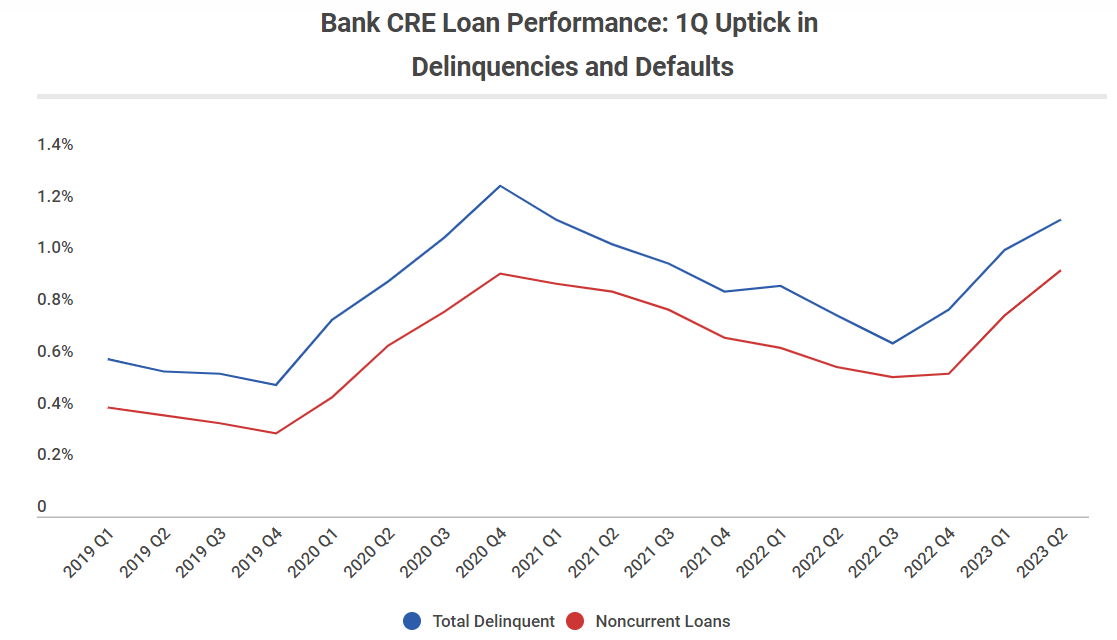

Net charge-offs and delinquency rates for bank-held commercial real estate (CRE) loans increased in the second quarter, with all major property types showing greater distress. Lender concern about risk, indicated by criticized loan rates, increased across multiple regions for most property sectors.

The pace of origination volume has slowed dramatically, with Q2 2023 commercial mortgage origination volume at only about 60% of the pre-Covid average quarterly origination volume in 2019.

The total delinquency rate rose 12 basis points from 1.03% in the first quarter to 1.15% in the second quarter of 2023. The serious delinquency rate, or the non-current loan rate, experienced an uptick of 17 basis points, increasing from 0.78% in Q1 to 0.95% in Q2.

The office sector saw a dramatic rise in its delinquency rate in the second quarter, increasing from 2.7% in Q1 to 4.9% in Q2 2023, after seeing steady increases in the delinquency rate in recent years.

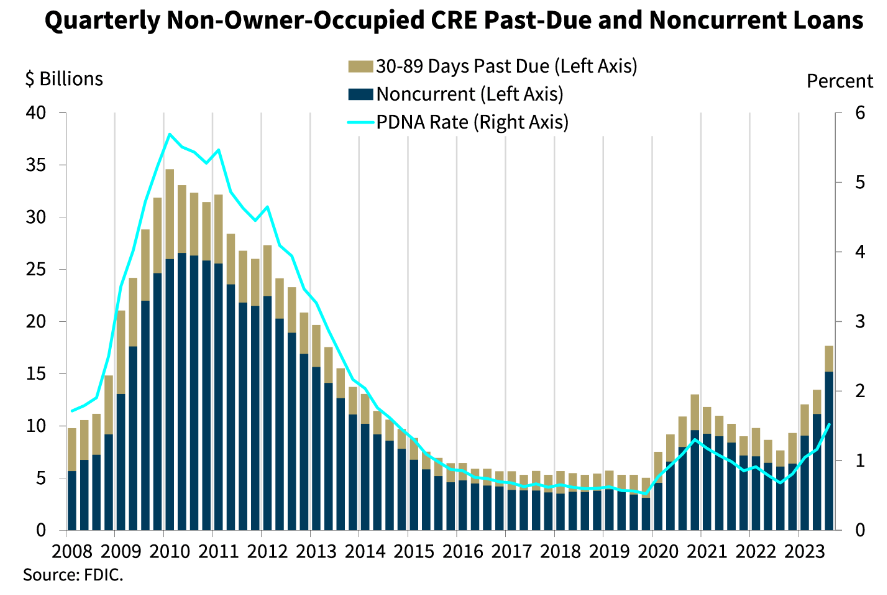

Looking more closely at commercial real estate portfolios, we are beginning to see concerning trends in non–owner–occupied property loans. The volume of noncurrent non–owner occupied CRE loans increased by $4.1 billion, or 36.4 percent, quarter over quarter. In addition, these loans had a noncurrent rate of 1.31 percent in the third quarter, up from 0.96 percent last quarter and 0.54 percent a year ago. This is the highest noncurrent rate reported for this loan portfolio since third quarter 2014.

These trends are being driven primarily by deterioration in office loans.

Research from NBER (Institution responsible for declaring recessions)

Analysis demonstrates that distress in the commercial real estate sector could lead to the

inclusion of dozens to over three hundred predominantly smaller regional banks within the cohort

of institutions vulnerable to insolvency arising from the uninsured depositor runs.

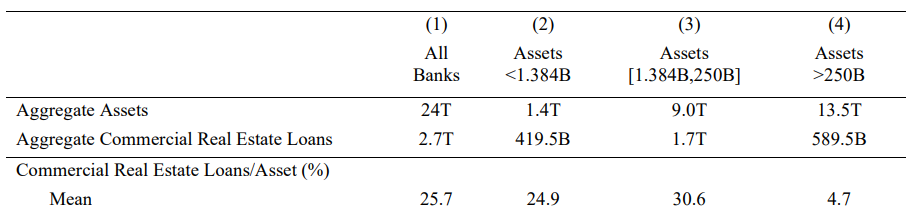

CRE loans represent on average about a quarter of total assets

By the end of November 2023, the equity value of real estate holding companies (REITs) specializing in the office sector had plummeted by nearly 55% since the onset of the pandemic. A straightforward calculation suggests that these declines imply a 33% reduction in the value of office buildings held by these companies

The commercial property price indices from Green Street Advisors reveal that, across metropolitan

areas, the value of office buildings may have, on average, decreased by approximately half from their pre-2020 values.

By December 2023, the LTV has risen to 66.2% due to the recent decline in property values. Notably, this increase is much more significant for office loans, which constitute about 19.2% of all loans in our sample. Their LTV experiences a pronounced surge from 54.4% to around 86% As we observe 14.3% of all loans and 44.6% of office loans are in negative equity.

Data reveals that currently, 6.4% of all loans and 6.6% of office loans have a DSCR less than 1, indicating that the net property cash flow is insufficient to cover loan debt service. This would be worse if they need to refinance at the current rates.

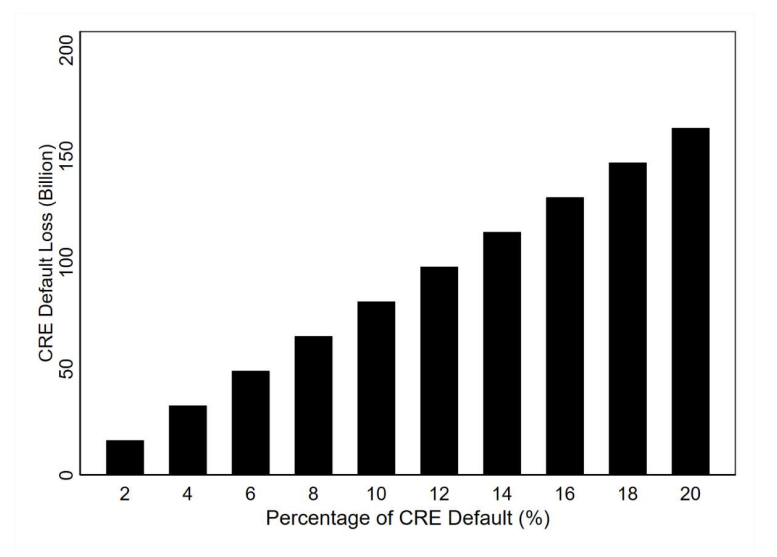

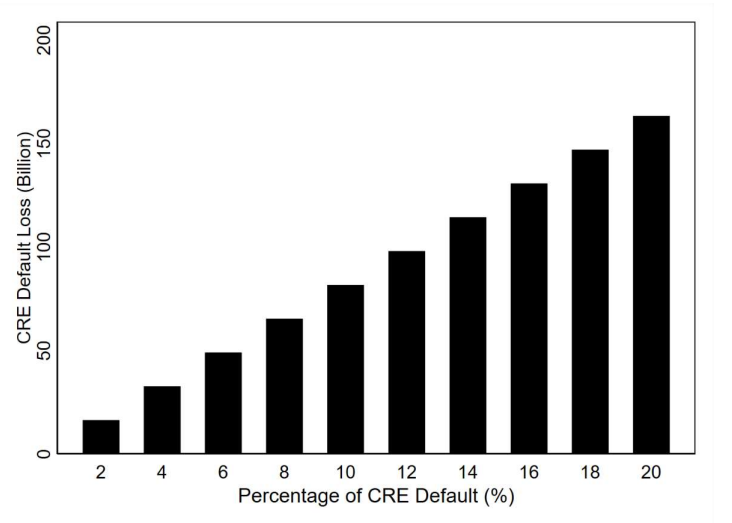

A a 10% (20%) default rate on CRE loans – a range close to what one saw in the Great Recession on the lower end – would result in about $80 ($160) billion of additional bank losses.

Researchers estimated that in a scenario where half of uninsured depositors empty their accounts, losses related to commercial real estate could result in 31 to 67 smaller regional banks becoming insolvent. Another 340 banks could face insolvency due to losses stemming from higher interest rates.

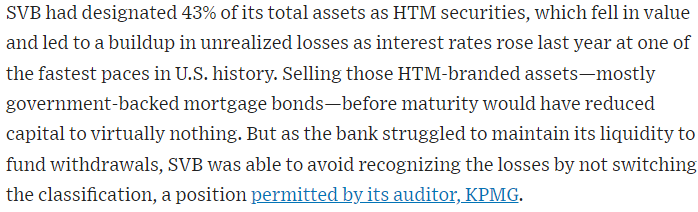

Very interesting. Do you know if banks need to charge off their CRE loans in real-time(quarterly) when asset prices are falling, or are there ways to “hide” bad risks and carry them forward?

@Aron is tracking (CRE) Charge-Offs, Credit Loss Provisions, Non-Performing Loans, but all seem to be in reasonably low territory (?)

If reduced asset prices are already reflected in books, there should be no problem at all, but if they are not, there could be a serious issue (?)

Edit: I just realized that my description of “falling asset prices” has been very indefinite. I was talking about falling prices of the underlying commercial real estate not about falling prices of CRE securities like CRE loans or CMBS.

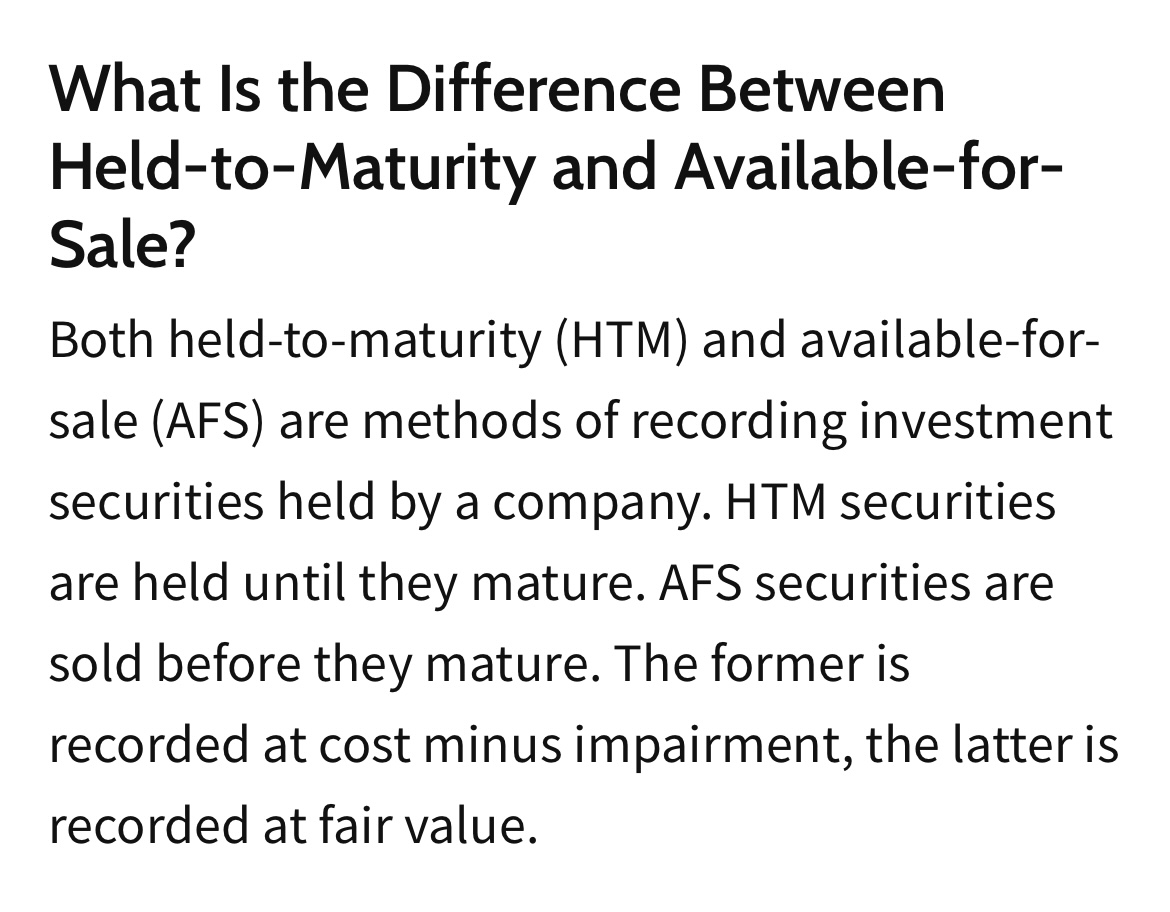

No, banks or other institutions do not have to mark to market all of their assets or recognize losses/gains on them quarterly.

They only have to do it on the assets that they mark as “available for sale”, and not the “hold to maturity” [assets](Available-for-Sale Securities: Definition, vs. Held-for-Trading

This is similar to treasury holdings, currently, they have huge unrecognized losses but are not on their balance sheet or income statement either.

The difference is that while treasuries can be held until maturity without much risk, the same can not be said for other types of assets.

If losses were recognized as the research paper says they would be already a significant amount of banks insolvent. But I would be seeing serious issues at some point if there is huge panic and contagion from credit losses that a wave of small banks start failing, because even if big banks have the capital to buy them, if it’s a large enough number it could become unmanageable.

If it’s like a “control” demolition, there will be banks in trouble and probably economic pain due to more lending restrictions, but the financial system will be most likely able to absorb the losses.

Also have to consider that credit risks are not only in the banks directly, and they have also indirect exposure which is significant.

I am guessing this is why everyone is hoping and begging for huge interest rate cuts, even if it doesn’t make sense, because the longer rates remain at this level more and more refinancing will need to happen in all sectors.

Unfortunately I cannot access the FT article as of now.

Are you sure that there are no regularly impairment tests for held to maturity assets?

Allowing banks to hold treasuries to maturity without reflecting short term price changes is reasonable to some degree as underlying assets are not impaired.

Allowing them to hold assets to maturity which are clearly impaired without any obligation to reflect that in their balance sheet is crazy.

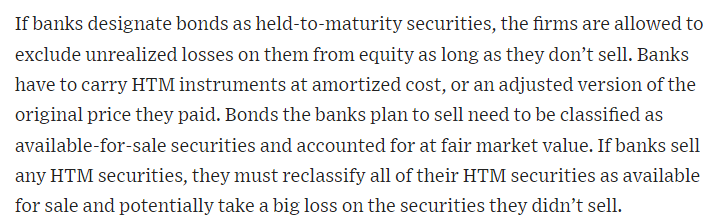

No they don’t, they have to disclose their unrealized losses on HTM instruments, but this is in a separate part of the report, and they don’t have to include any of it on their income statement or balance sheet before they switch them to AFS, which they are not forced to do.

I just looked into the accounting standards and it looks like banks need to reflect expected impairment losses immediately even if assets are held to maturity.

Full guide on current expected credit loss (CECL) models.

That means if there are not any significant loopholes in those rules all expected credit losses that banks are expecting from uncollectibility of CRE loans should be already reflected under credit loss allowances and also be part of both income and balance sheets?

That those CRE loans could currently not be sold at current face value, similar to all other assets that are HTM is another topic but at least banks are forced to adjust their balances to their current repayment expectations.

Yes, but that’s different, thats only about the credit losses. (Which is not the only type of losses/risk banks face)

If they are delinquencies or defaults or any credit losses, those will need to be reported as soon as they happen. And those for CRE have been already increasing.

I was talking about the asset value losses regulation, which is the issue currently with banks, as borrowers start to be on negative equity, and with motivation to default when refinancing. But that will not be reflected until they happen as it is not a default or delinquency currently.

The paper that I shared from NBER is focused on the liquidity risks banks face, which I should have mentioned in the post.

As for your question, credit allowances are set according to what they expect or their model forecast, and they change from quarter to quarter. Banks could very well overestimate or underestimate these provisions. It is not as it is the exact amount of losses that will happen.

It is obviously in the best interest of banks to try to be as exact as they possibly can, but I am guessing their models are also not perfect.

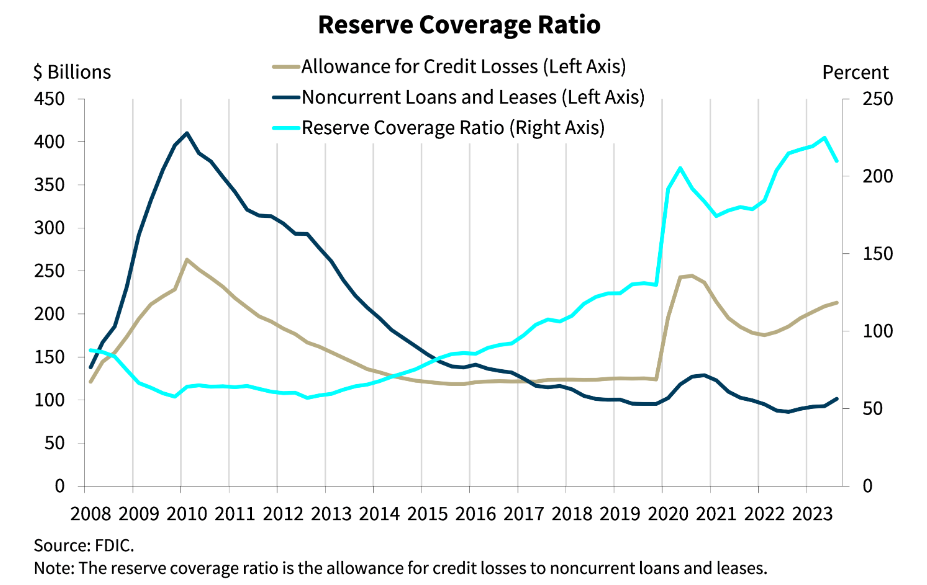

In 2008, the coverage ratio (allowances vs noncurrent loans) was low. This time banks seem to be preparing well in this regard, but still uncertain if it’s going to be enough, at least it looks much better than in 2008.

So, credit risks seem manageable. I am still unsure how to really asses the liquidity risks, which are the ones that could create the trouble.

I must admit that the data looks confusing to me, most likely as i am missing knowledge on multiple fronts.

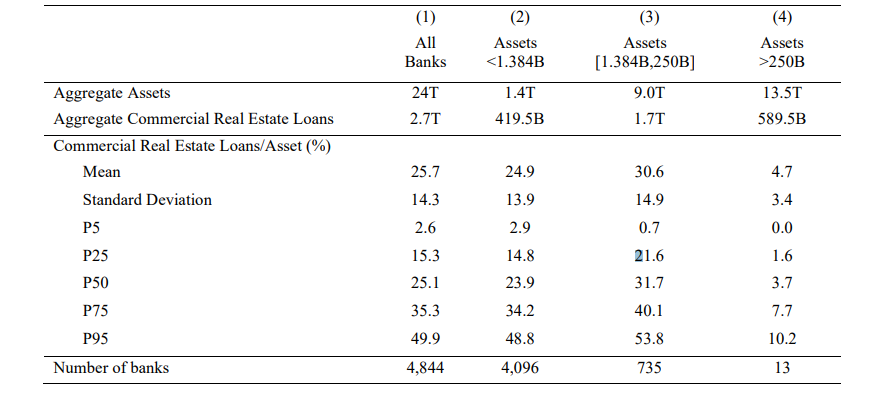

First, the NBER report highlights 24T in Bank assets and 2.7T in CRE Loans. How do we arrive at Commercial Real Estate Loans/Assets 25.7% with those numbers?

Why are allowances for credit losses still so low? As an example, let’s say the 2.7T number is correct. Shouldn’t allowances for credit losses be higher by now than around 125 billion, considering how much the underlying commercial real estate value dropped and could continue to drop as people run into refinancing problems? This 125 billion number is allowances for credit losses of all types of loans, not just CRE, correct?

Example: Calculating with random numbers and assuming that 20% of CRE ends up being repossessed and assuming banks lose 20% on average on those repossessed loans, we already end up with 0.2 * 2.7t * 0.2 = 108billion in CRE losses alone.

I am not sure if small banks have an incentive to be realistic with their models, esp. since they have to fear that there would be a bank run if they report bad numbers and they know that they had to sell their HTM assets at a large loss.

Regarding liquidity risks for small banks, I always assumed that those risks would simply be opportunities for larger banks to buy them as long as the assets those smaller banks hold are good. If it turns out that banks did not properly assess credit risks, we could have a larger problem.

I did not arrive at 25%. This is the mean that they calculated, which is more influence by the amount of small banks on it, which in aggregate have an exposure of 30%. (Table is divided by bank size too)

Yes, this is the aggregated industry credit allowances at the end of Q3 2023 by the FDIC.

Why they are so low still, would be an interesting question for banks regulators or authorities.

It could be because their coverage ratio is 2x already, but this is because noncurrent loans are still low. So, under current circumstances, they are well protected and looking better than 2008, and it could just mean that later on they will need to start to increase provisions are more deterioration starts to happen to maintain the ratio.

As you mentioned, maybe they don’t want to post bad results and only start doing it at the very last minute when it is inevitable.

This is what the paper calculated in losses depending on different default scenarios

Got it. The concentration of CRE loans in smaller banks looks a bit scary.

Is there any breakdown of credit allowances to see which categories they come from? As the focus of this topic is CRE, it would be interesting to put CRE allowances in perspective with CRE risks to understand how conservatively banks created these allowances.

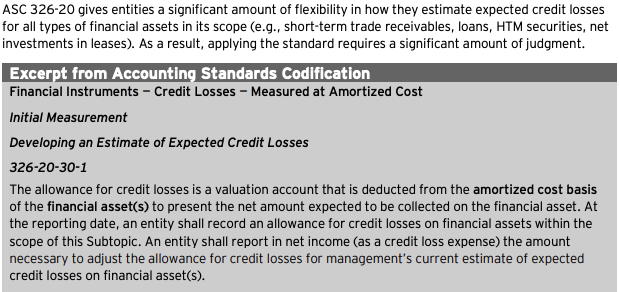

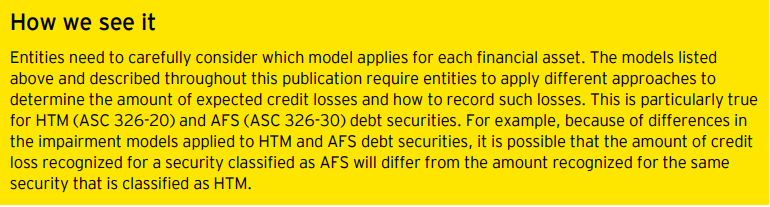

Additionally, it would be interesting to take a deeper look into the ASC 326-20 accounting guidance since it describes that there is a significant amount of flexibility in how banks can estimate expected credit losses. I’d be interested in confirmation of that and examples of how this can be done.

Lastly, finding expert opinions on the same topic would be cool.

All this could strengthen our understanding of how risks are accounted for and how much we can rely on metrics like credit allowances.

The coverage ratio chart you just posted is quite chilling as it shows how badly allowances can fail.

I would not want to take too much comfort in the fact that allowances currently stand approx. 65 billion higher than noncurrent loans since defaults have not started yet, and balance sheets in 2024 should be way larger than in 2008.

I will look into the credit allowances breakdown and accounting in more detail and will post the results here as I have something of substance to post.

And Yes, completely, I am with you that credit provisions can fail very badly. I am just saying is better than 2008 because even though noncurrent loans are still low, they are taking the steps to better protect themselves, which they failed to do at all at the start of 2008, with a coverage ratio below 1. But if they don’t adjust provisions later on as risks start to be more apparent, I also don’t think it will be enough this time either in a wave of defaults.

As CRE is not the only issue, corporate loans maturities are also approaching, and auto loans and other consumer credit are already starting to get weak too. This without adding a recession and unemployment increasing.

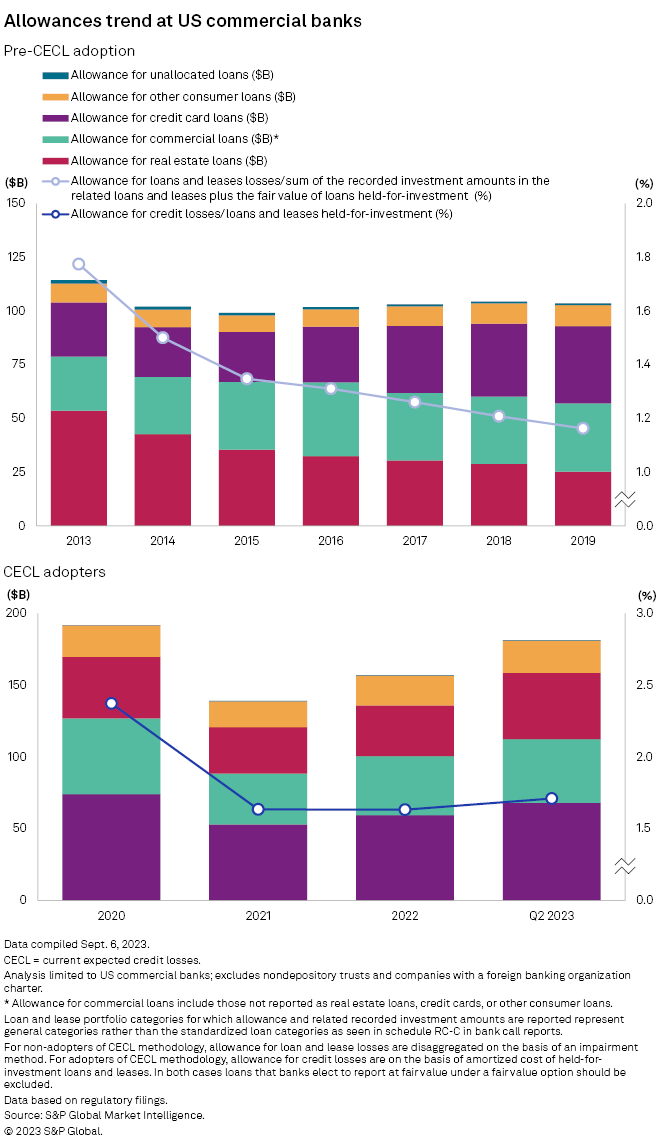

This is the only breakdown of credit alloancews I found, it aggregates all real estate, but still is only a fraction of the total, is as of Q2 2023:

I also noticed that you misread the previous chart and allowances are not 125B, they are close to 200B, but the point is still the same. H8 also gives a weekly update of the number, which currently stands at 198.4B.

I also reviewed ASC 326-20 accounting guidance from EY explanation to its clients on how to apply it: Its very long and I will only post what is most relevant

The regulation indeed allows great subjectivity when calculating expected credit losses:

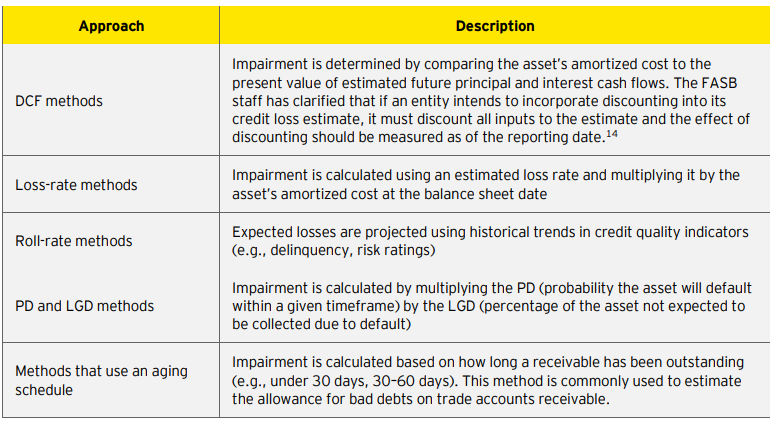

They can choose the method (p.31):

326-20-30-3

The allowance for credit losses may be determined using various methods. For example, an entity may use discounted cash flow methods, loss-rate methods, roll-rate methods, probability-of-default methods, or methods that utilize an aging schedule. An entity is not required to utilize a discounted cash flow method to estimate expected credit losses. Similarly, an entity is not required to reconcile the estimation technique it uses with a discounted cash flow method.

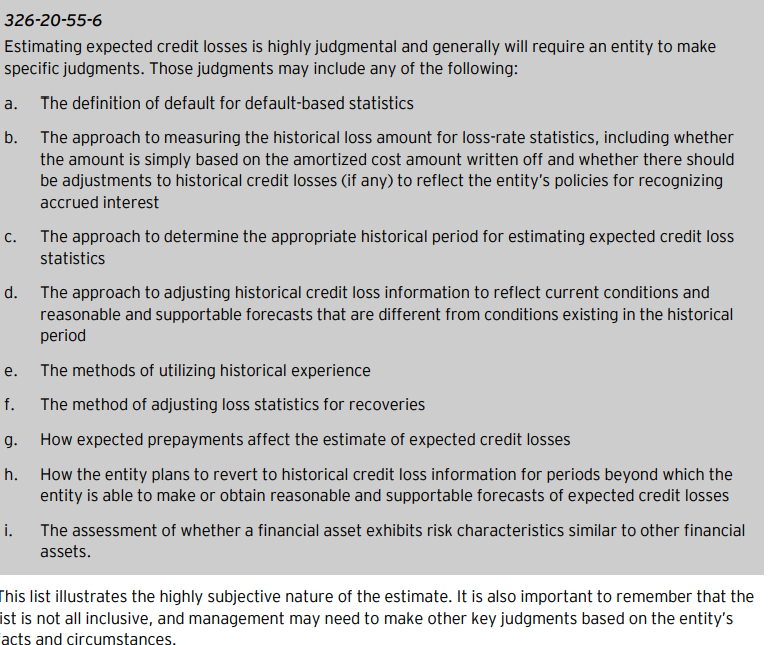

326-20-55-7

Because of the subjective nature of the estimate, this Subtopic does not require specific approaches

when developing the estimate of expected credit losses. Rather, an entity should use judgment to

develop estimation techniques that are applied consistently over time and should faithfully estimate

the collectibility of the financial assets by applying the principles in this Subtopic. An entity should

utilize estimation techniques that are practical and relevant to the circumstance. The method(s) used

to estimate expected credit losses may vary on the basis of the type of financial asset, the entity’s

ability to predict the timing of cash flows, and the information available to the entity.

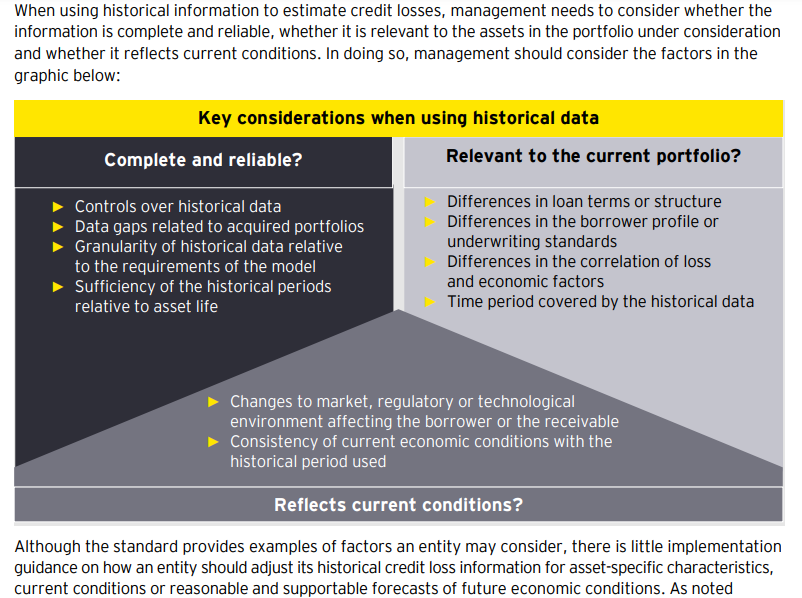

The banks should adjust historical data to reflect current circumstances accurately, but the adjustments are also subjective to them, and no much guidance is given either. This is the more challenging part, and where different views or forecasts of the future lead to different estimates from institutions(p.68)