This topic discusses the upcoming Q2 2025 Meta Platforms earnings. It will include our final assessment and decision before the earnings release. We will also summarize the results here. You can find our earnings preparation and full summary of the results in the Wiki:

Earnings date: July 30, 2025

Time of Earnings release: 4:00 PM ET

Time of Analysts Call: 5:00 p.m. ET

Tinuti Digital Ads Benchmark report signals Meta’s Q2 2025 revenue could grow at 15%-17%

Ad spent growth on Meta Platforms by Tinuiti advertisers accelerated to 12% y/y in Q2 2025 from 11% in Q1, impressions rose 13% y/y, the fastest growth since Q1 2024 while CPM fell 0.5% y/y- unchanged from last year.

Ad spend on Facebook rose 12% y/y (Q1 2025: +11% y/y), impressions grew 18% y/y, the biggest increase since Q3 2024 while CPM fell 0.5% (Q1 2025: +1% y/y) due to growth in newer inventories like Reels.

Spend on Instagram ads grew 11% y/y in Q2 (Q1 2025: +7% y/y), impressions declined 1% (Q1 2025: -6% y/y) while CPM increased 12% y/y (Q1 2025: +14% y/y)- the slowest growth since Q1 2024.

The share of Advantage+ shopping campaigns’ (ASCs) slipped to 35% from 38% in Q1 2025.

Ad spend growth on TikTok fell 20% y/y in Q2 (Q1 2025: -11% y/y) due to uncertainty over the app’s future, impressions rose 3% y/y (Q1 2025: +27% y/y) while CPM fell 22% y/y (Q1 2025: -30% y/y).

Ad spend on Google search rose 11% y/y in Q2 (Q1 2025: +9% y/y), click through rate (CTR) accelerated to 7% y/y from 4% in Q1 2025 while cost per click (CPC) slowed to 3% y/y from 5% in Q1 2025.

Assessment

Over the most recent six quarters, Meta’s reported revenue growth has outperformed Tinuiti’s Meta ad spend growth by an average of 9.25%. However, from Q4 2024, the deviation narrowed significantly to 6%. The average deviation for revenue growth in Q4 2024 and Q1 2025 was 5%. Based on the Tinuiti report, which has historically been a reliable indicator of Meta’s revenue growth, Meta’s Q2 2025 revenue could grow at 15%-17% .

It’s not good to see Meta’s CPM starting to weaken. Maybe this is driven by the uncertainty caused by the tariffs. Over the past six quarters, Meta’s reported average price per ad has exceeded CPM reported by Tinuiti by an average of 7.5%. Therefore, Meta’s Q2 2025 average price per ad could grow 6%-7% y/y, a deceleration from 10% in Q1.

The share of spend on Advantage+ Shopping (ASC) decelerated during the quarter, raising concerns that advertiser complaints over the past year may now be impacting its utilization. Insights shared during the earnings call regarding ASC performance will help clarify whether advertiser concerns are affecting its momentum.

Meta Platforms continues to benefit from TikTok’s shrinking share of digital ad spend.

Based on Tinuiti report, I expect Alphabet’s Q2 2025 advertising revenue to grow 8%-9.5%, topping analysts estimate of 7.7% or $69.6 billion. Over the most recent five quarters, Alphabet’s advertising revenue has underperformed Tinuiti Google search ads spend by 1.5%.

My bullish stance is also supported by other positive developments during the quarter; including resilient ad spend despite tariff uncertainty, as evidenced by Omnicom Group and Publicis reporting revenue above estimates; Magna upgrading its ad spend forecasts; and positive advertising checks by analysts.

Key insights I’m watching in Alphabet’s earnings include:

Trends in advertising spend amid tariff uncertainty: Whether ad budgets remain resilient could offer a read-through for Meta’s ad business as well.

Progress in AI monetization and advertiser adoption: Insights into how advertisers are using Google’s AI tools may help assess Meta’s positioning in AI-driven ad solutions.

Capital expenditure (CapEx) projections: Alphabet has guided for $75 billion in CapEx for 2025. Any upward revision gives Meta a reason to keep investing. A downward revision might raise concerns among Meta investors about broader pullbacks in tech spending.

Commentary on the DOJ antitrust case: A confident or bullish tone from Alphabet may imply optimism for platform companies facing regulatory scrutiny, including Meta’s own FTC case.

I=7 Alphabet reported advertising revenue above analyst expectations and increased its 2025 capital expenditure guidance by $10 billion

Alphabet’s Q2 2025 revenue rose 14% y/y to $96.4 billion, above analysts estimate of $94.0 billion while EPS came in at $2.31, exceeding analysts estimate of $2.17.

Google advertising revenue rose 10.4% y/y to $71.3 billion, exceeding analysts estimate of $69.6 billion.

Alphabet increased its CapEx guidance for 2025 to $85 billion from $75 billion.

Alphabet shares shed 2.8% in late trading (and then bounced back) due to the increased CapEx guidance.

Alphabet expects further growth in CapEx in 2026, doesn’t list tariff as one of the headwinds in H2 2025

Alphabet expects CapEx to increase further in 2026 due to customer demand and opportunities they are seeing across the company.

“Looking out to 2026, we expect a further increase in CapEx due to the demand we’re seeing from customers as well as growth opportunities across the company,” CFO Anat Ashkenazi announced in the earnings call.

Almost the entire CapEx is going to servers and data centres.

“The vast majority of our CapEx was invested in technical infrastructure, with approximately two-thirds of investments in servers and one-third in data centers and networking equipment,” Anat said.

Management didn’t mention the impact of the tariffs, only saying second half of 2025 will be impacted by strong comps.

“Advertising revenues in the second half of 2025 will be affected by the following: the continued lapping of the strength we experienced in financial service verticals throughout 2024, and year-over-year comparisons will be negatively impacted by the strong spend on US elections in the second half of 2024, particularly on YouTube,” Anat said.

Alphabet’s AI ad generation tools continue to see good traction.

“Over two million advertisers now use Google’s AI-powered asset generation tools… a 50% increase on this time last year, " CBO Philipp Schindler said.

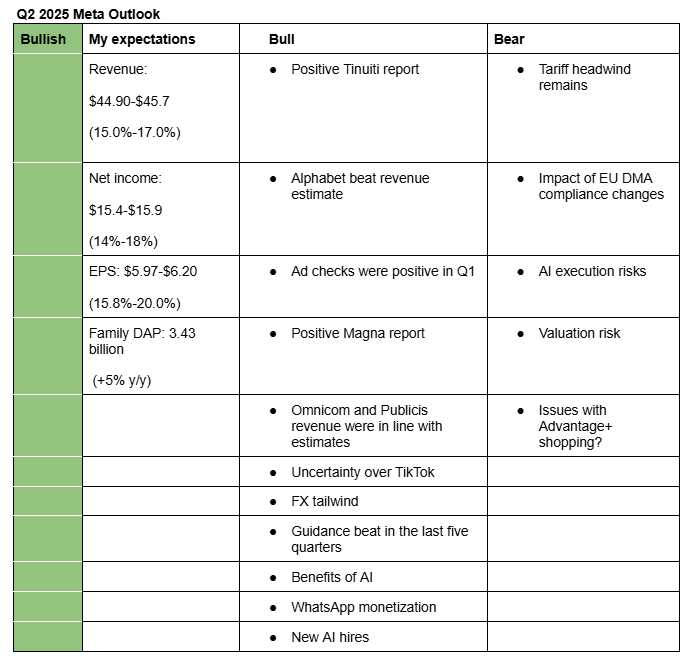

I am bullish on Meta’s Q2 2025 earnings. My estimates reflect resilient ad spending during the quarter, insights from Tinuiti report, FX tailwind, uncertainty around TikTok, revenue beat by competitors, and guidance beat in the last five quarters.

Here is a description of by bullish and bearish sentiments:

Bullish sentiments

Positive Tinuiti report: Tinuiti’s Q2 2025 Digital Advertising Benchmark report shows that ad spend on Meta Platforms grew 12% y/y. Historically, Tinuiti has been a reliable indicator of Meta’s ad revenue. Based on the report, Meta’s Q2 revenue could grow in the 15%–17% range.

Alphabet beat revenue estimate: Alphabet’s advertising revenue rose 10.4% year-over-year to $71.3 billion, beating analysts’ estimate of $69.6 billion. This strong performance sends a positive signal that Meta may also exceed its revenue estimates.

Ad checks were positive in Q1: Several research firms such as Deutsche Bank, TD Cowen, Bofa, JPMorgan, Piper Sandler, Wells Fargo, etc. have indicated that their ad checks were positive during the quarter, implying that Meta is likely to report solid ad revenue in Q2.

Positive Magna report: Magna recently hiked its 2025 US digital ad outlook by 0.5% to 10.1% due to resilience in Q1. In my opinion, if Magna saw weakness in ad spend in Q2, they couldn’t have raised their projections.

Omnicom and Publicis revenue were in line with estimates: Omnicom and Publicis reported revenue in line with estimates, with Publicis slightly raising its full-year guidance. Advertising spend typically flows first through media and advertising agencies. In a macroeconomic slowdown, advertisers often bypass agencies. Therefore, continued strength in agency spend suggests positive momentum for Meta Platforms.

Uncertainty over TikTok: Uncertainty over TikTok’s existence in the US continues to favor ad spend on other platforms such as Meta. According to Tinuiti, ad spend by Tinuiti advertisers on TikTok fell 20% y/y in Q2. An April 2025 report by Sensor Tower indicates that Meta is the primary beneficiary of ad spend shifting away from TikTok.

FX Tailwind: Meta’s Q2 2025 revenue will benefit from the weaker U.S. dollar against major global currencies. Management, which has a strong track record in forecasting FX impacts, expects a 1% tailwind from foreign exchange this quarter. My rough estimate is a tailwind of around 1.4%.

Guidance beat in the last five quarters: Meta Platforms has beaten management’s mid-point revenue guidance by an average of 3.2% in the most recent five quarters.

AI benefits: I expect Meta’s AI tools such as GEM and Andromeda to continue driving ad performance, leading to market share gain. Meta also plans to automate ad creation using AI by 2026. New Street Research estimates that AI ad creation tools could boost Meta’s ad revenue by $28 billion by 2030.

WhatsApp monetization: Meta Platforms announced in June 2025 that it’s introducing ads in WhatsApp. The venture could start being revenue accretive from Q4 2025. Analysts estimate that WhatsApp ads could bring in additional $6 billion to $10 billion in the coming years.

New AI hires: Meta has brought in industry heavyweights, including Shengjia Zhao (co‑creator of ChatGPT, now Chief Scientist of Superintelligence Labs), Alexandr Wang (former Scale AI CEO, serving as Chief AI Officer), and prominent AI researchers from OpenAI, DeepMind, Anthropic, and Apple (such as Ruoming Pang, Mark Lee, and Tom Gunter). I expect these new AI hires to address Meta’s underperformance in large language models (LLMs).

Bearish sentiments

Tariff headwind: The tariff overhang persists as the U.S. has yet to finalize trade agreements with several countries. The 55% tariff deal signed with China is both temporary and unusually high, which could prompt advertisers to remain cautious or delay spending decisions.

Impact of EU DMA compliance changes: In its Q1 2025 earnings, Meta announced that it expects to modify its ad model in Europe to comply with the Digital Markets Act (DMA), which will significantly impact revenue starting in Q3 2025. I estimate a revenue headwind of $3.7 billion in 2025 and $8.3 billion in 2026. EU Commission said at the beginning of this month that Meta’s pay or consent model needs further reworking, signaling that Meta may not avoid the headwind. However, similar to Apple’s ATT rollout, I expect this headwind to be temporary. Meta’s core AI team will likely develop solutions to mitigate the impact over time. Additionally, growing monetization of WhatsApp and revenue from AI-powered ad creation tools should help offset the decline.

AI execution risks: Zuckerberg’s strategy now appears focused on “superintelligence”, an ambitious but unproven technology. This introduces execution risk, which could put pressure on the share price, especially amid rising CapEx. Based on recent comments from both Zuckerberg and Alphabet, I expect Meta’s 2026 CapEx to exceed $80 billion (2025 guidance: $64–$72 billion).

Valuation risk: Trading at a trailing twelve-month (TTM) P/E of around 25, Meta’s share price could face a significant pullback if the company slightly misses expectations or if management delivers negative commentary on AI.

Issues with Advantage+ shopping Campaigns (ASCs): According to Tinuiti, the share of Advantage+ Shopping Campaigns (ASCs) fell to 35% in Q1 2025, down from 38% in the previous quarter. This decline may signal that advertisers are starting to pull back from ASCs, following a series of complaints since last year that the product has been underdelivering on performance.

Here are management’s and analysts’ expectations for Q2 2025;

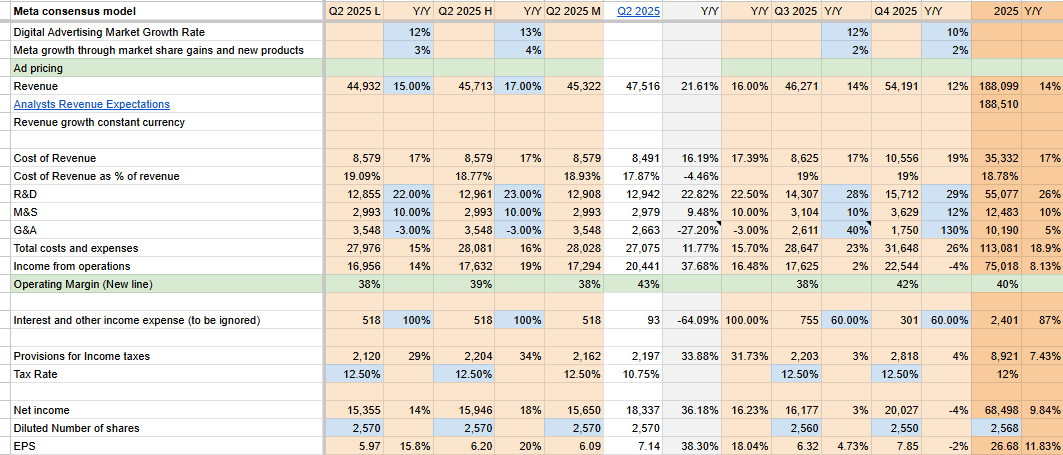

Management Guidance for Q2 (Revenue): $42.5-$45.5 billion (+8.9% to +16.5%) Analysts’ Estimate for Q2 (Revenue): $44.8 billion (+14.7%) Analysts’ Estimate for Q2 (EPS): $5.89 (+14.1%)

Recommendation

Overall, given the resilience of the advertising market, upcoming monetization from WhatsApp and AI-powered ad creation tools, continued market share gains, and offsetting risks from regulatory headwinds and AI execution challenges, combined with a valuation that appears fair at current levels, I reiterate a Hold rating on Meta shares.

Meta’s Q2 surges past estimates; 2026 expenses and CapEx set to stay elevated

Meta Q2 2025 revenue rose 22% y/y to $47.5 billion, above management’s upper guidance of $45.5 billion and analysts estimate of $44.8 billion, EPS came in at $7.14 versus analysts estimate of $5.89 while operating margin of 43% exceeded analysts estimate of 38%.

Family daily active people (DAP) rose 6% y/y to 3.48 billion, versus analysts estimate of 3.45 billion, ad impressions grew 11% y/y (Q1 2025: +5%) while average price per ad increased 9% y/y (Q1 2025: +10%).

Meta is guiding Q3 2025 revenue in the range of $47.5-50.5 billion (analysts estimate: $44.62 billion)- which assumes FX tailwind of 1%, 2025 total expenses in the range of $114-118 billion (increased from $113-118 billion) and CapEx in the range of $66-72 billion (increased from $64-72 billion).

Meta expects 2026 y/y expense growth rate to be higher than the 2025 expense growth rate driven by infrastructure costs and employee compensation.

It expects 2026 to be another year of significant capital expenditure as it continues increasing capacity to support AI and business operations.

Meta continues to flag EU’s DMA, pointing out that it could significantly impact its business as early as Q3.

Assessment

This was another strong quarter for Meta. Q2 2025 revenue grew 22% year-over-year, exceeding my upper estimate of 17%. Cost of revenue, R&D, and Sales & Marketing expenses were in line with expectations, while G&A came in $900 million below my estimate. Q3 2025 revenue guidance also topped my forecast of $46.3 billion.

There were no one-off benefits during the quarter, and FX impact was neutral.

Here are the main takeaways from Meta’s Q2 2025 earnings call as well as my assessment:

CEO Mark Zuckerberg said the strong performance this quarter was mainly due to AI.

“On advertising, the strong performance this quarter is largely thanks to AI unlocking greater efficiency and gains across our ads system,” he said.

CFO Susan Li said they don’t expect WhatsApp to be a meaningful contributor of revenue growth for the next few years due to limited ad tracking data and the fact that WhatsApp usage is skewed towards lower monetizing regions.

Meta continues to make improvements to its AI recommendation tools such as Andromeda, GEM and Lattice, leading to improvement in ad recommendations and conversions.

Analyst Doug Anmuth with JPMorgan said in the call that Susan Li’s comments suggest CapEx of $100 billion in 2026. Li didn’t deny it while Zuckerberg agreed that the investment they are making is massive.

Assessment

Overall, Zuckerberg reiterated recent comments that Meta’s AI strategy is now focused on achieving superintelligence. Management signaled that CapEx and expenses are likely to increase significantly again in 2026, driven by investments in short-lived assets and compensation for new hires made this year. The strong performance of the core business gives Meta the justification to continue investing heavily in its compute infrastructure. However, despite this strength, I expect operating margins to slightly decelerate in 2026.

Analysts say Meta gave CapEx and OpEx outlook for 2026 that is higher than expected, praise returns from AI

Outperform, $775->$900: Bernstein notes that Meta destroyed expectations in Q2 with perhaps one of the biggest prints in history thanks to massive returns from AI in both engagement and ad performance. The analysts add that the 24% y/y growth for Q3 at the top end is "hard to comprehend but shouldn’t be possible at this scale.

Buy, $812->$897: UBS notes that Meta’s ad growth was driven by impression rather than pricing, suggesting the trajectory can be sustained in the midterm.

Overweight, $800->$905: KeyBanc said Meta’s Q2 results reinforced that AI is driving positive impacts on engagement and advertising. They highlighted that tax policy is supportive of AI investments.

Overweight, $783->$811: Wells Fargo said Meta gave CapEx and OpEx outlook for 2026 that is considerably more than expected but the robust growth outlooks offset the investment.

Hold->Buy, $610->$900: HSBC contends that Meta is well position to outpace digital ad market growth. They cited AI benefits as new growth opportunities.

Snap’s Q2 2025 ARPU missed estimate due to platform changes, guided Q3 revenue above estimates

Snap’s Q2 2025 revenue rose 4% y/y to $1.34 billion versus analysts estimate of $1.35 billion.

Global average revenue per user (ARPU) was $2.87 versus $2.90 expected.

Snap blamed the weaker-than-expected ARPU on pricing changes made to its ad platform, timing of Ramadhan and impact of de minimis changes.

Snap guides Q3 2025 revenue in the range of $1.475 billion to $1.505 billion, above analysts estimate of $1.475 billion.

Snap said direct response advertising revenue rose 5% y/y (a deceleration from the prior quarter) while brand advertising revenue was flat y/y (an improvement from the prior quarter).

Direct response represents approximately two-thirds of their ad business.

Snap hinted that most of the headwind came from the ad platform pricing changes.

Pinterest Q2 2025 revenue beats, guides Q3 above estimates; tariff impact smaller but still on advertisers’ radar

Pinterest Q2 2025 revenue rose 17% y/y to $998 million, above analysts estimate of $975 million while EPS came in at $0.33 versus analysts estimate of $0.35.

It guided Q3 2025 revenue in the range of $1.033 billion to $1.053 billion, exceeding analysts estimate of $1.025 billion.

Pinterest said tariff impact in Q2 was smaller than anticipated though tariff concerns continue to linger on advertiser’s minds.

“I’d say, as we talk to advertisers about Q3, we do hear that some of that tariff-related and broader market uncertainty has continued into how they’re thinking about spend for Q3, though this varies by advertiser and again, it’s definitely a relatively more constructive environment than feared,” CFO Donnelly said in the earnings call.

“So while the tariff impact was certainly smaller than we anticipated in Q2, we did still see some impact affecting our UCAN region.”

“For example, Asia-based e-commerce retailers pulled back spend in the U.S. tied to the change in the de minimis exemption. But partially offsetting this headwind, we also continue to see really exciting ongoing geographic diversification from some of these and other retailers to our European and Rest of World regions.”