This topic discusses the upcoming Q1 2026 Meta Platforms earnings. It will include our final assessment and decision before the earnings release. We will also summarize the results here. You can find our earnings preparation and full summary of the results in the Notion:

Earnings date: April 29, 2026

Time of Earnings release: 4:00 PM ET

Time of Analysts Call: 5:30 p.m. ET

I=8 Tinuiti Ads Benchmark report imply Meta Q1 2026 revenue growth of 30%-32%

Ad spent growth on Meta Platforms by Tinuiti advertisers accelerated to 13% y/y in Q1 2026 from 9% in Q4 2025, CPM fell 3% in Q1 versus a decline of 7% in Q4 while ad impressions rose 17% y/y for the second straight quarter.

Ad spend growth on Facebook rose 4% y/y (Q4 2025: +3%), ad impression growth decelerated to 8% from 19% in Q4 while CPM growth decelerated from -13% y/y to -4% y/y as Reels impression stalls.

Ad spend growth on Instagram rose 28% y/y the fastest growth since Q1 2024, CPM fell 3% y/y the first decline since Q3 2023 while ad impressions rose 31% y/y versus growth of 7% in Q4 2025 as share of Reels ads continue to grow.

Ad spend growth on TikTok rose 14% y/y (Q4 2025; +1%), ad impressions rose 2% (Q4 2025: +8%) while CPM grew 11% versus a decline of 6% in Q4 2025.

Ad spend growth on Google search grew 14% y/y (Q4 2025: +13%), click through rate (CTR) rose 14% (Q4 2025:+13%) cost per click (CPC) was flat y/y (Q4 2025: -1%).

Assessment

Tinuiti Ads Benchmark report has historically been reliable in predicting Meta’s revenue growth.

In Q4, Q3, and Q2 2025, Meta’s reported revenue growth outpaced Tinuiti spend growth on the platform by 15, 12, and 10 percentage points, respectively. Extrapolating this trend, with the outperformance gap widening by a further 2-4%, implies Q1 2026 Meta revenue growth of approximately 30-32%, within the upper half of management’s guidance range of 26–33.5% (Q4 2025 Meta Platforms (Notion)).

It’s good to see that despite the rebound in ad spend on TikTok, ad spend on Meta Platforms remains strong.

While Tinuiti has been indicating declining Meta CPM, Meta 10-Q reports have been showing CPM is stable (Meta Platforms Tinuiti Report Analysis (Google Sheets)). Therefore, I will take Tinuiti CPM numbers with a grain of salt.

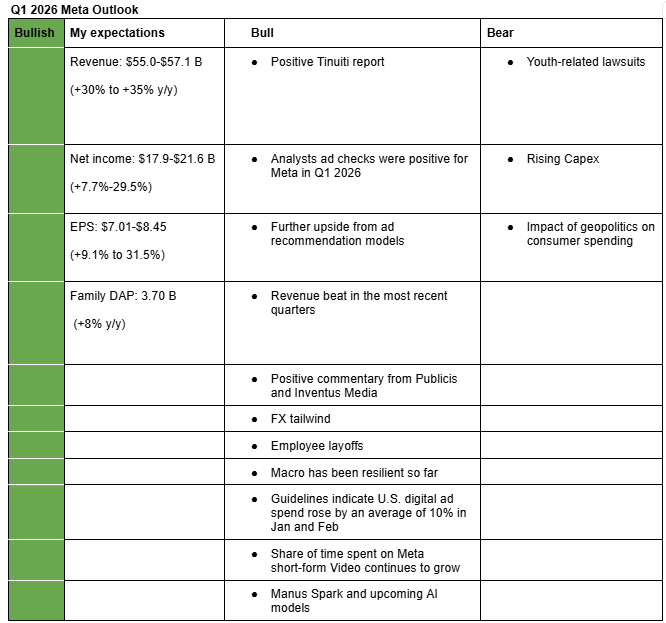

I am bullish on Meta’s Q1 2026 earnings and the company overall. My estimates (Meta Valuation Model (Google Sheets)) are based on positive Tinuiti report, positive ad spend checks, continued gains from Meta’s Ai-driven ad models, expected cost-savings from layoffs, assumption that capex will remain elavated, FX tailwind, and Meta’s consistent guidance beats over the most recent eight quarters. Let’s dive in into my bullish and bearish arguments.

Bullish arguments

Positive Tinuiti report: According to Tinuiti Ads Benchmark report (forum post), which has been consistently reliable in predicting Meta’s revenue growth, ad spend on Meta Platforms by Tinuiti advertisers rose 13% y/y in Q1 2026. Extrapolating from this report a lone, Meta’s Q1 2026 revenue could grow by approximately 30-32%.

Analysts ad checks were positive for Meta in Q1 2026: Bofa, Piper Sandler and KeyBanc analysts pointed out (Q1 2026 Meta Platforms Earnings (Notion)) that their ad checks were positive for Meta Platforms in Q1 2026.

Further upside from ad recommendation models: I expect further efficiency gains from Meta’s ad recommendation models such as Andromeda, GEM and Lattice. Meta’s CFO Susan Li pointed out during the last earnings call that algorithm performance gains continue as they scale the models (Q4 2025 Meta Platforms Earnings Call (Notion)).

Revenue beat in the most recent quarters: Meta Platforms has beaten management’s mid-point revenue guidance by an average of 4% in the most recent eight quarters (Meta Platforms Google Sheets).

Positive commentary from Publicis and Inventus Media: Publicis (Notion) and Inventus Media (Notion) (advertising agencies that supply the likes of Meta with customers) reported revenue that were in line with estimates, with Publicis CEO saying he hasn’t seen any slowdown in marketing spend. S4 CEO Martin Sorrell also said (Notion) there are signs marketing spending is beginning to stabilize and improve. Similarly, Guidelines indicate U.S. digital ad spending rose by an average of 10.3% in January and February versus 10.7% in Q4 2025 (Google Sheets).

FX tailwind: Meta will again benefit from the strengthening of the foreign currencies against the U.S. dollar in Q1 2026. While management is guiding FX tailwind of 4%, I expect it to be around 2.8% due to the pullback associated with the Iran conflict (Notion).

Employee layoffs: There are reports that Meta plans to lay off 20% of its employees in 2026 due to efficiency from AI. Analysts estimate that such a magnitude could save Meta between $5 and $8 billion annually (Q1 2026 Meta Platforms Earnings (Notion)). In my opinion, this cost-savings will offset some further increases in Capex.

Macro has been resilient so far: According to macro analysts, macroeconomic conditions in the USA have been resilient so far though the ongoing Iran conflict is threatening consumer spending (forum post).

Share of time spent on Instagram and Facebook short-form video continues to grow: According to Sensor Tower, time spent on Instagram and Facebook short-form video rose further in 2025, that of YouTube Shorts was flat while that of TikTok was down (forum post). As such, the rising ad load in Facebook and Instagram may not be necessarily impacting user engagement.

Manus Spark and upcoming models: The underperformance of Meta’s LLMs models coupled with rising Capex created an overhang on Meta’s shares. However, the recently released Manus Spark is competitive and signals that the upcoming models will be more competitive (forum post). As a result, if Q1 2025 earnings will be solid, Meta shares could rise sharply.

Bearish arguments

Youth-related lawsuits: This is currently the major overhang on Meta shares. Some analysts have drawn parallels to the “Big Tobacco” moment. However, I view this comparison as overstated given social media companies are beneficial to the economy and also the fact that users age 16 and below account for roughly 5% of Meta’s users. I estimate that the lawsuits could lead to $5 billion in fine and $8 billion headwind from structural changes. This is not material for Meta given that it generates around $60 billion in profit annually. These cases are still evolving though and the possibility of a larger headwind remains a risk (Notion).

Rising Capex: Based on commentaries and the compute deals that Meta is signing (forum post), it remains a possibility that its Capex could rise further. Management guided Capex in the range of $115 to $135 billion in 2026 and analysts already see Capex rising further in 2027 (Q1 2026 Meta Platforms Earnings (Notion)) .

Impact of geopolitics on consumer spending: If the Iran conflict lasts for several days, consumer spending in the U.S. could deteriorate and inflation could start rising again. This may force businesses to reduce their ad spend. However, given Meta leans more into direct response advertising, the impact may be small (Notion).

Management guidance and analysts' estimates:

Management Guidance for Q1 (Revenue): $53.5-$56.5 billion (+26.4% to +33.5%)

Analysts’ Estimate for Q1 (Revenue): $55.5 billion (+31.3%) Analysts’ Estimate for Q1 (EPS): $6.64 (+3.0%)

Recommendation

At its current P/E of around 22x, which I view as fair, combined with improving AI execution, potential for further AI-driven cost efficiencies, solid advertising revenue growth and other opportunities outlined in our broader thesis (Meta Platforms – Notion), I raise my rating from Hold to Buy. Should the shares decline further, the risk/reward would become increasingly attractive.

I=10 Meta beats Q1 2026 revenue and EPS estimates, raises 2026 Capex guidance by $10B, and issues Q2 guidance suggesting strong revenue growth may be losing steam

Meta’s Q1 2026 revenue rose 33.1% y/y to $56.3 B, in line with management’s upper point guidance and above analysts’ consensus estimate of $55.5 B, while operating margin was 40.6% versus analysts’ estimate of 35%.

EPS (excluding tax benefit of $3.13 per share) was $7.31 versus analysts’ consensus estimate of $6.74.

Meta guided Q2 2026 revenue in the range of $58-61 billion (+22.1% to +28.4%) versus analysts estimate of $59.6 B (+25.4% y/y), 2026 Capex in the range of $125-$145 B (up $10 B from previous guidance and compared to consensus estimate of $125 B), and 2026 total expenses in the range of $162-169 B (unchanged from prior guidance).

Family daily active people (DAP) rose 4% y/y to $3.56 B (but down 0.6% QoQ) due to internet disruption from Iran conflict and WhatsApp ban in Russia, ad impressions grew 19% y/y (Q4 2025: +18% y/y) while average price per ad increased 12% y/y (Q4 2025: +6% y/y).

Meta shares down 5% at the time of writing this post, with Bloomberg citing the increased Capex guidance and revenue guidance that fails to blow analysts’ minds as usual.

Assessment

Meta’s Q1 2026 earnings were solid. Revenue and EPS beat estimates while ad pricing and impressions continue to grow. While the market reacted negatively to the increased Capex guidance, it didn’t come as a surprise to me. While analysts’ consensus for Capex was around $125 B, my estimate was $135 B (upper point of management prior guidance) and I expected further increase due to the compute deals that Meta is making.

While Q2 revenue guidance is somewhow weak, it could be that Meta is being conservative given the ongoing Iran conflict.

Overall, the earnings call didn’t have a lot of new insights, particularly on the new LLMs. However, their vision for personal superintelligence appears intact.