This topic will be centered around the automotive industry developments

US article: Automotive Industry:United States - InvestmentWiki

Europe Article: Automotive Industry:Europe - InvestmentWiki

This topic will be centered around the automotive industry developments

US article: Automotive Industry:United States - InvestmentWiki

Europe Article: Automotive Industry:Europe - InvestmentWiki

Ford cutting prices significantly on EV. In line with articles about the demand for EVs decreasing.

Ford Motor is slashing prices on the electric version of its best-selling F-150 pickup by as much as 17%, as it moves to fend off new competition coming from Tesla and General Motors.

@moritz My assessment currently:

Data mainly for the US. I have tried to find data on global prices, and no luck for now.

Currently new vehicle market seems stable, and it does not look that the weakness in the used car market has been transmitted to new cars for now. But looking ahead there are some concerning signs already, especially in credit conditions, that could point to additional reduced demand going forward.

Some Insights:

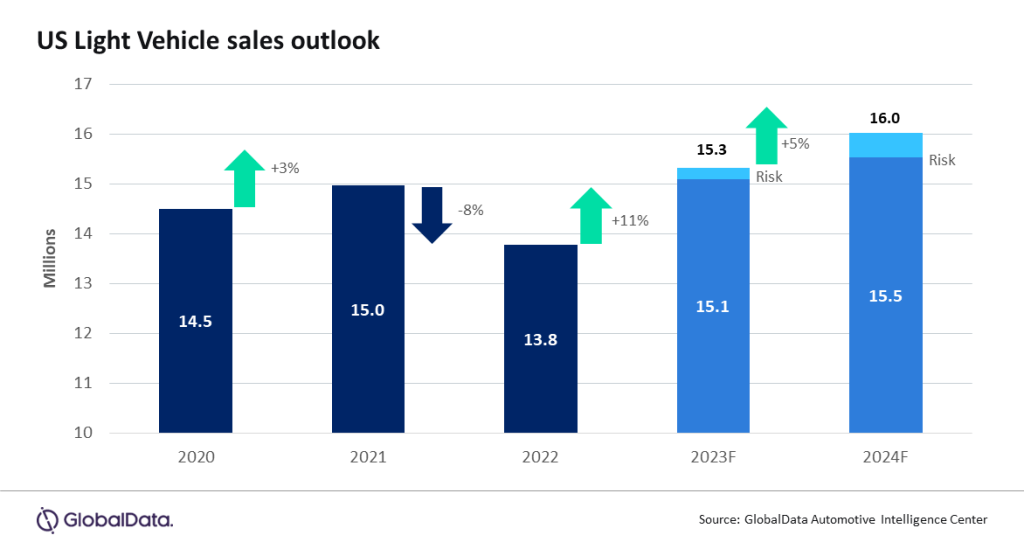

New car sales have increased significantly during the quarter coming from a low base in 2022. This a mostly due to inventory increasing. This is the same for US and Europe.

Total Vehicle Sales (TOTALSA) | FRED | St. Louis Fed

New car prices have come down 1.7% since January 2023, but still 1.6% up Y/Y, they are still high compared to history (not sure they will ever come back to the level as before). However, days of supply are increasing, which could put additional pressure on prices going forward.

New Car Prices Fall as Inventory, Dealer Incentives Rise | Money

Delinquency though they appear low, they are higher than even what we saw in 2008. But this is mostly from subprime borrowers. This could translate into more defaults coming months, and result in additional tighter credit conditions.

Auto Market Weekly Summary: July 17 - Cox Automotive Inc.

Special report from S&P Global Mobility: Auto-finance delinquencies rise past Great Recession peak, but….

Auto credit rejection has reached new series high in the NY fed survey at 14.2 percent from 9.1 percent in February. The probability that a loan application will be rejected rose to 30.7 percent for auto loans.

SCE Credit Access Survey - FEDERAL RESERVE BANK of NEW YORK

https://twitter.com/LizAnnSonders/status/1681262926504640512/photo/1

Credit availability is almost as low as 2020, and affordability is still very bad compare to history while rates remain high.

New-Vehicle Affordability Stable in June - Cox Automotive Inc.

Auto Credit Availability Improved in June - Cox Automotive Inc.

Cox mid-year review: https://www.coxautoinc.com/wp-content/uploads/2023/06/2023-Cox-Automotive-Mid-Year-Review-Presentation.pdf

5 posts were merged into an existing topic: Automotive Industry: China

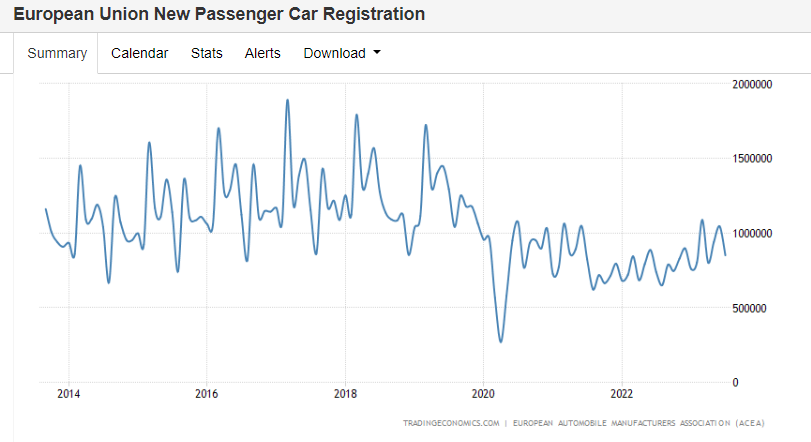

In July 2023, the EU car market continued its growth trajectory, expanding by 15.2% the twelfth consecutive month of growth. New car registrations reached 851,156 units as the bloc recovers from last year’s component shortages. Most markets posted solid growth, including the four largest: France (+19.9%), Germany (+18.1%), Spain (+10.7%) and Italy (+8.7%).

From January to July 2023, new EU car registrations grew significantly (+17.6%), totalling 6.3 million units. Despite indications of the European automotive industry’s recovery from pandemic-related supply disruptions, year-to-date volumes are still 22% lower than in 2019.

Automotive Industry:Europe - InvestmentWiki

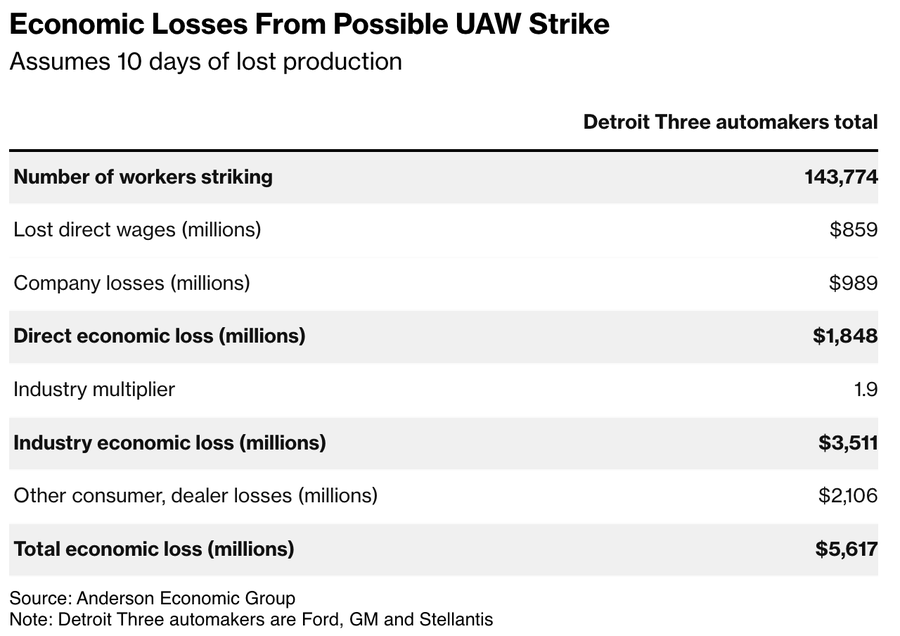

The United Auto Workers began a strike Friday against all three of the legacy Detroit carmakers, an unprecedented move that could launch a costly and protracted showdown over wages and job security.

The strategy of targeting individual plants is designed to methodically cut production of profitable vehicles while minimizing the impact on the UAW’s strike fund. The union said it will add strike locations depending on how bargaining progresses.

https://www.bloomberg.com/news/articles/2023-09-15/uaw-strike-2023-auto-workers-eye-walkout-at-gm-ford-stellantis-plants

46% of US auto production is set to go offline as a result of the UAW strike.

According to Bloomberg, a 10-day UAW strike would reduce US GDP by $5.6 billion.

The auto industry accounts for 3% of US GDP.

A strike longer than a few days would send many midwest states into a recession.

What is our current assessment of the automotive industry @Magaly?

All geographies appear to perform well at the moment?

What is our outlook how those geographies are going to perform in 2024 and beyond?

I consider the outlook to be the same, sales are still strong due to pent-up demand, but credit continues to deteriorate, at least in the US, no data yet found for other regions.

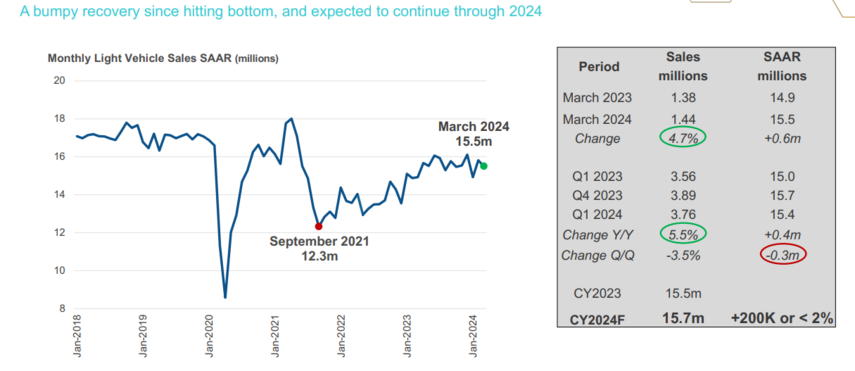

US sales as of September were 15.4 SAAR, 3.91 million in Q3, 11.56m YTD. Meaning -4.4% Q/Q, 13.7% y/y.

Europe YTD registrations 9.6 millions, 17% y/y

The Global Light Vehicle (LV) selling rate ended its 6-month rising streak by falling to 93 million units/year in September, from a revised figure of 100 million units in August.

US new car prices are -0.7% y/y, and -3.4% YTD, still very high.

US used car prices -3.9 y/y, and Europe -12 y/y and -0.9% YTD.

US delinquencies are at a level not seen since 2006, and it continued to increase during the quarter.

Affordability is the US is still really bad compared to pre pandemic, while prices have declined a bit, rates continue to increase. Credit availability is still tight.

1H2023 EV global sales 6 million, 40% y/y (includes BEV and PHEV) .China EV sales increased by +37 % in 2023 H1 y/y, Western and Central Europe were up +28 % in H1, USA and Canada are +50 % higher YTD to June than last year. EV sales outside the aforementioned markets increased by 102 %, albeit from a low base.

Forecast:

Global:

US:

Have not found any reliable source for a more long term forecast, but what I have seen up to 2030 is expected to have a 3-5% GAGC range.

According to Lucky Lopez (Car Dealer), repos were up to 20,000/day in July, up from 17,000/day at the start of 2023. He talks about how loosened credit requirements in the 2021 stimulus era, and the fact people overpaid for cars, having now huge negative equity in their used cars is what is causing this spike.

This could mean 4-5m repos annually, only including business days.

He says this repo data comes from what financial institutions disclosed them, but there are other smaller lenders that don’t do it, and repos could be even higher.

Other dealers have stated similar experiences in their auctions

Cox is also predicting a similar 25% increase in repos but for a smaller volume 1.5m (As reference, 1.75m was the high in 2009, according to them)

However, I have difficulty trusting Cox data because I have seen a lot of criticism about their transparency of the true state of the market because of their interests. So If I have to chose who to follow more, I choose the car dealers showing the reality in the auctions

I have not watched the dealer videos yet, but my first instinct is that it is likely anecdotal evidence or do they have/use any good data sources?

YouTubers often have other strong reasons to flaw data, like simply the fact that their videos are likely going to be clicked more if they exaggerate or that they target a less professional audience that would not even realize in most cases if their data, research, methodology, etc. is not strong.

Conversely, Cox is certainly more professional and has other kinds of capabilities to aggregate and present data. I am not sure how easy it would be for them to manipulate without someone recognizing and if there could be consequences (like reputation loss or worse) or fines if they were caught.

Ultimately what would be interesting are longer repo time series so that we could understand repo averages and additional supply (beyond those averages) that is coming to the market most recently.

1.5m would certainly be way more digestible in relation to 16 Million annual car sales than 4-5m.

I guess is preference.

I have been listening to Lucky since start of 2022, and he has been pretty stop on in his assessments of the developments of the market, especially the credit parts, and has usually pretty good insights and analysis because he works analysing auto loans data.

On the other hand Cox has been downplaying everything.

For me personally, I will keep listening to him, and others alike.

But is totally ok, if you prefer to follow Cox assessments, that’s why I put both, so everyone can decide what they prefer to believe in.

For me what is more important all of it, is that we are reaching credit distress in the auto market even greater than the 2008 crisis, even before we are experiencing an actual recession/job losses. So my question is always, how is going to look like in it?

I don’t think it’s a question of choosing between Lucky vs. Cox but of analyzing their methodologies and how they reach their conclusions, weighing the data and insights we find, and building them into a consistent model.

I downloaded one of the reports of the source that Lucky Lopez linked below the video, and it looks to have interesting data on things like turnover. Maybe you can find his source on repos so we can assess it ourselves?

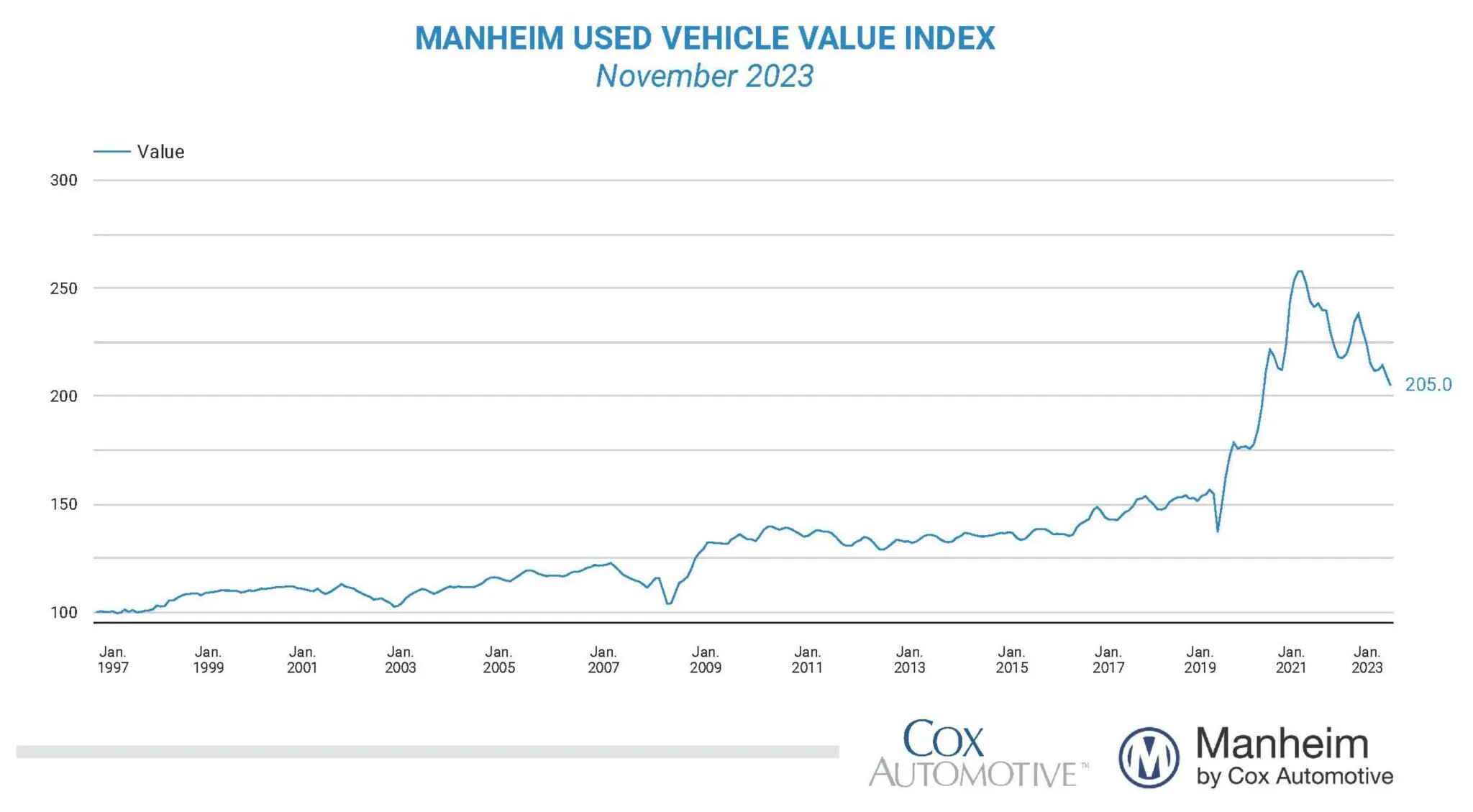

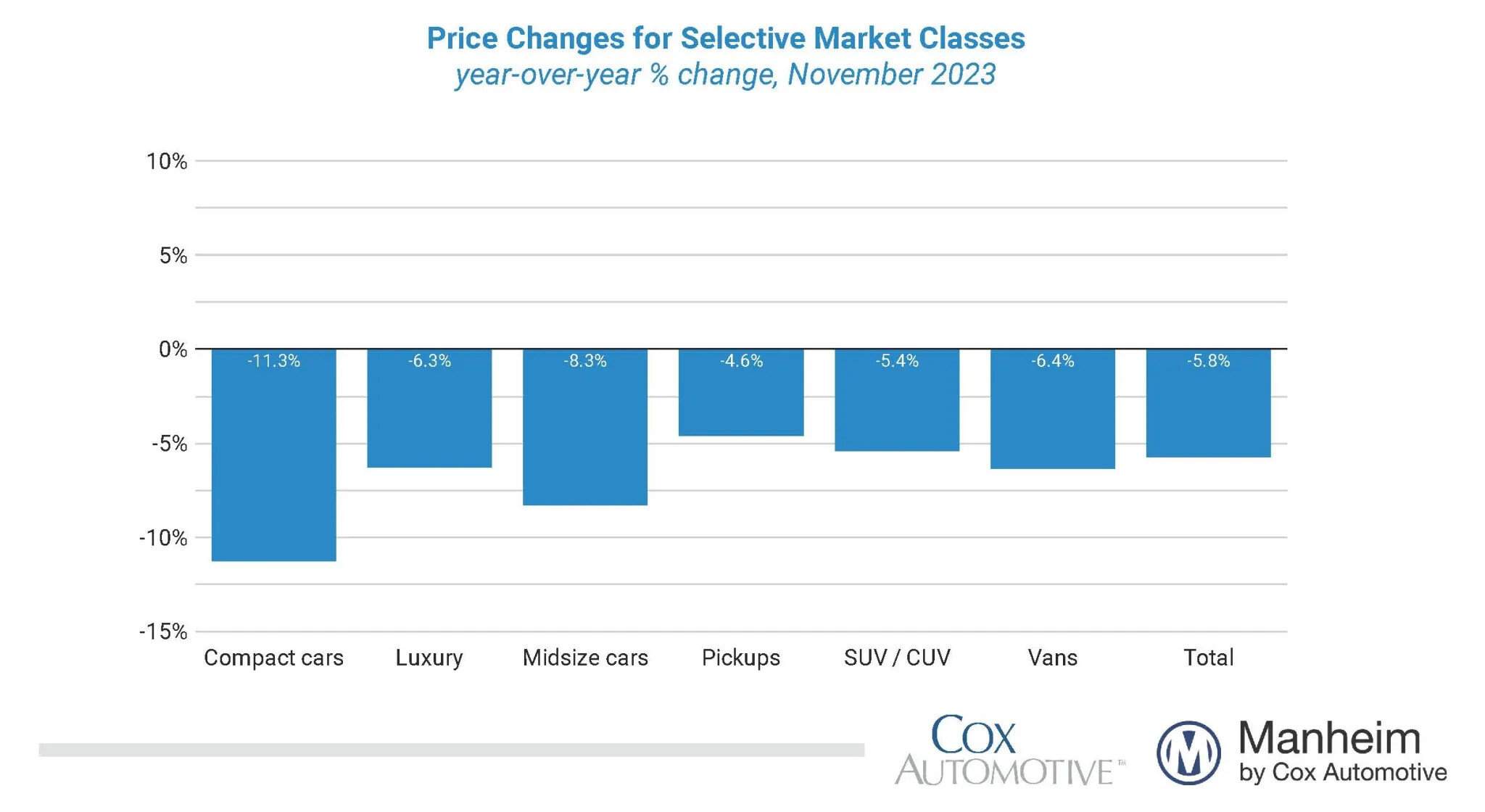

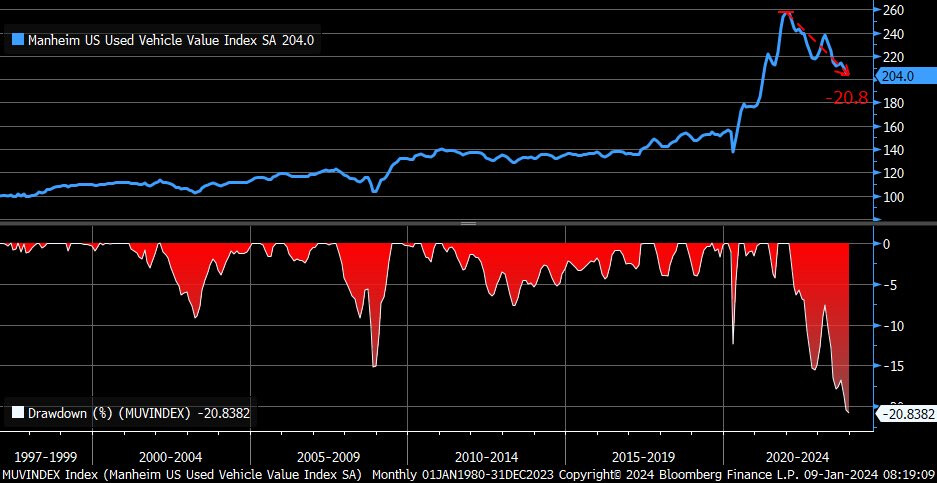

US wholesale used car prices declined -2.1% m/m in November and -5.8% y/y.

They have declined 20.46% from the peak, but are still way above pre-pandemic prices, which could leave room for additional declines.

There is a huge decline in Used car prices of almost 21% from the peak, and yet still too high compared to the historical trendline.

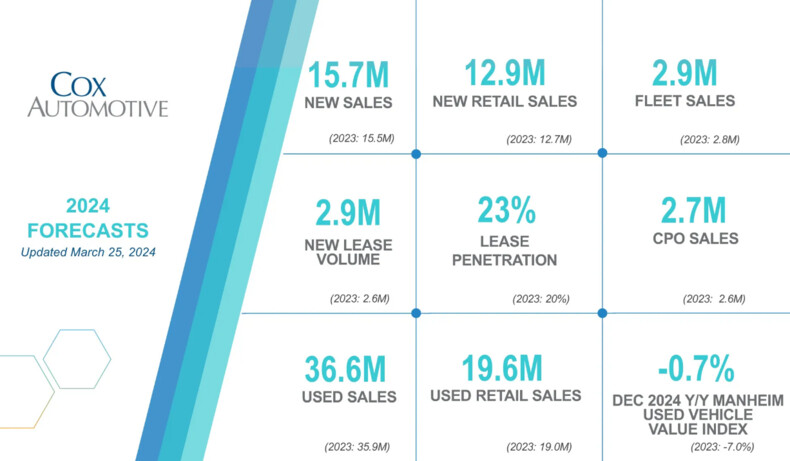

These are Cox Automotive 2024 forecasts:

As a reference, their initial 2023 forecasts were so-so.

New vehicle sales: 15.46 M vs 14.1M forecasted

Used vehicle sales: 35.9 M vs 35.6M forecasted

Used Value Index: -7% vs -4.3% forecasted

I think this pressure on new car prices will continue even if no recession materializes, and not sure any brand will be able to avoid it.

Especially since prices are still way higher than in 2019, supply is increasing significantly, and demand is not as abundant as before with these prices and rates high.

And also the fact that used car prices have declined even more, making them more attractive currently.

New car prices are declining at an astounding pace:

• Ford just reduced prices on its Lightning and Mustang Mach-E (EVs)

• Mazda just reduced up to $4000 on its CX90

• Hyundai just marked down every IONIQ and Tucson

EV-centric brands are at the forefront of the declines — but with supply levels rising, nearly every brand is feeling some level of pressure.

https://twitter.com/GuyDealership/status/1760732009545003148

This is what Cox reported in January:

@Magaly, what’s your assessment on these estimates, particularly prices of used cars? Do you think, used car prices would indeed be better in 2024?

Does it provide forecasts for prices of used EVs?

I read that it expects more discounting and incentives in the EVs market. That means EV prices would likely stay low?

https://athensceo.com/news/2024/01/cox-automotives-forecast-2024-return-normalcy-us-auto-market/

I dont really have a method at the moment to predict car prices.

I could only make the argument that based on higher rates, still low affordability, credit conditions continuing to deteriorate in auto loans, I would not really expect the prices to have positive growth for used cars.

And as of the middle of February, they have continued to decline.

Wholesale Used-Vehicle Prices Decrease in First Half of February - Cox Automotive Inc.

But if the economy indeed continues to be relatively good, it could be this year will be more stable, or at least not as bad as 2023. It does not mean I think price declines are over, but we could have stable and other not-so-stable years, as most everything don’t go down or up in a straight line.

Cox Forecasts as I mentioned are also not perfect, at least their initial one.

Last year they forecasted a -4% decline in January, and it ended up being more than 7%.

And they do not give forecasts for EVs, or New cars.

But yes, EVs are the ones struggling the most in terms of prices. Tesla has a lot of impact on what they have done, and I think continues to do.

This is how used car prices have done in history.

While there are greater declines during a recession, there is a lot of volatility always in prices.

Currently, we have already experienced a bigger decline than in any other period, but rate of change is getting better for now.

Y/Y

New car prices declined 0.1% during February

Used car prices also declined by 0.1% m/m in February.

A cautious outlook for the US industry, with sales growth decelerating, prices declining, inventory increasing back to normal levels of days of supply already, delinquencies and defaults still highest since the 2008 crisis, and rates still high and not expected to be cut relatively soon.

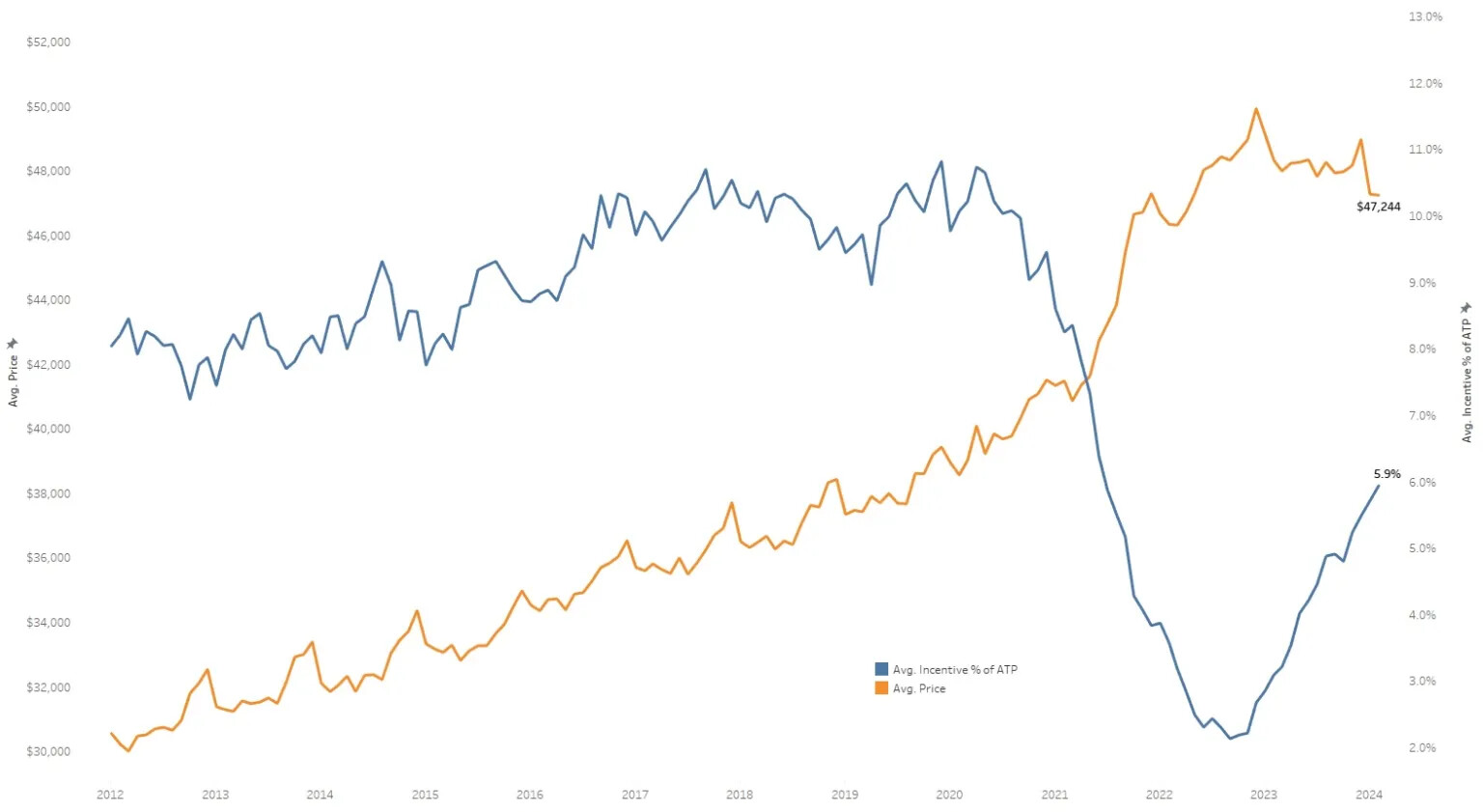

According to COX Automotive, the biggest risk for the industry right now is rates staying high for longer, because rational consumers will postpone buying until rates are lower, and dealers would need to work harder (higher incentives) for them to buy now.

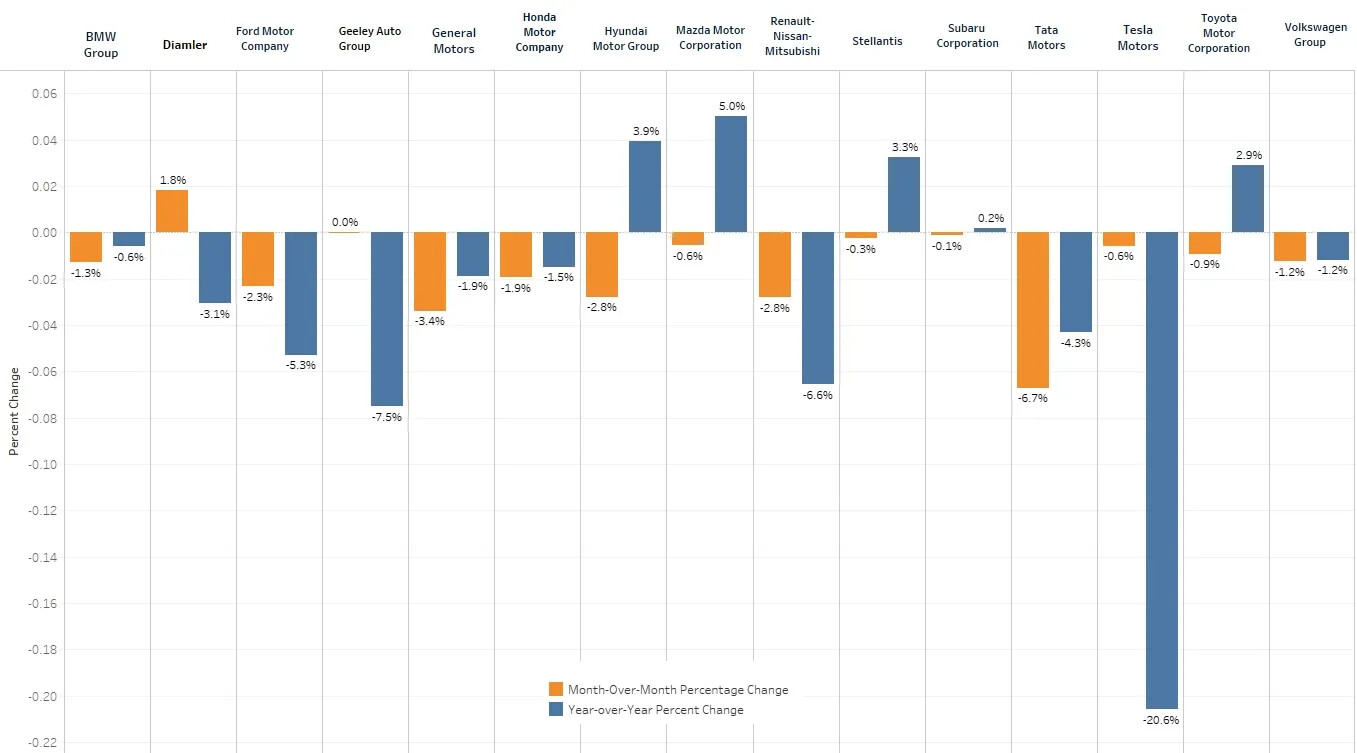

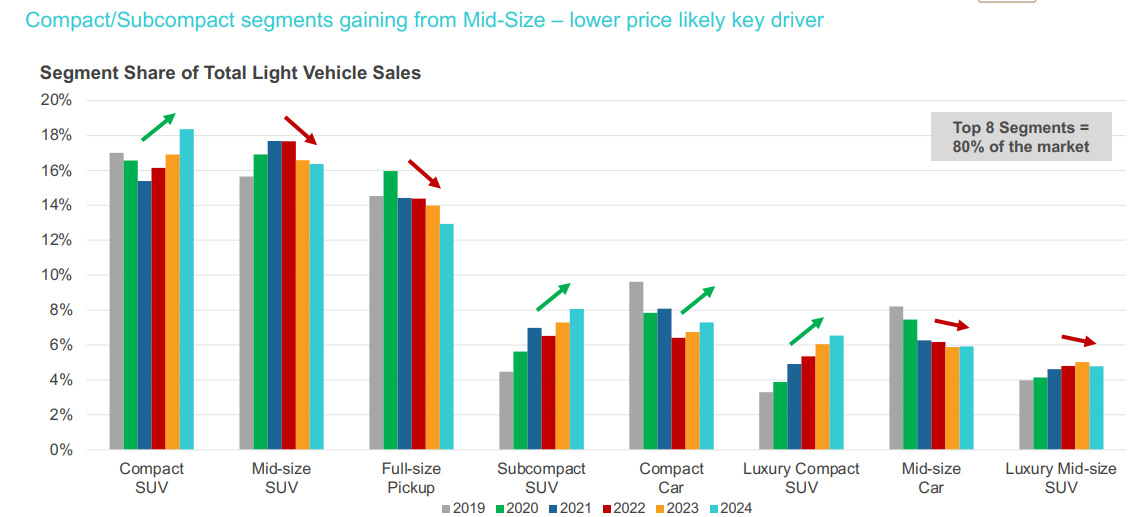

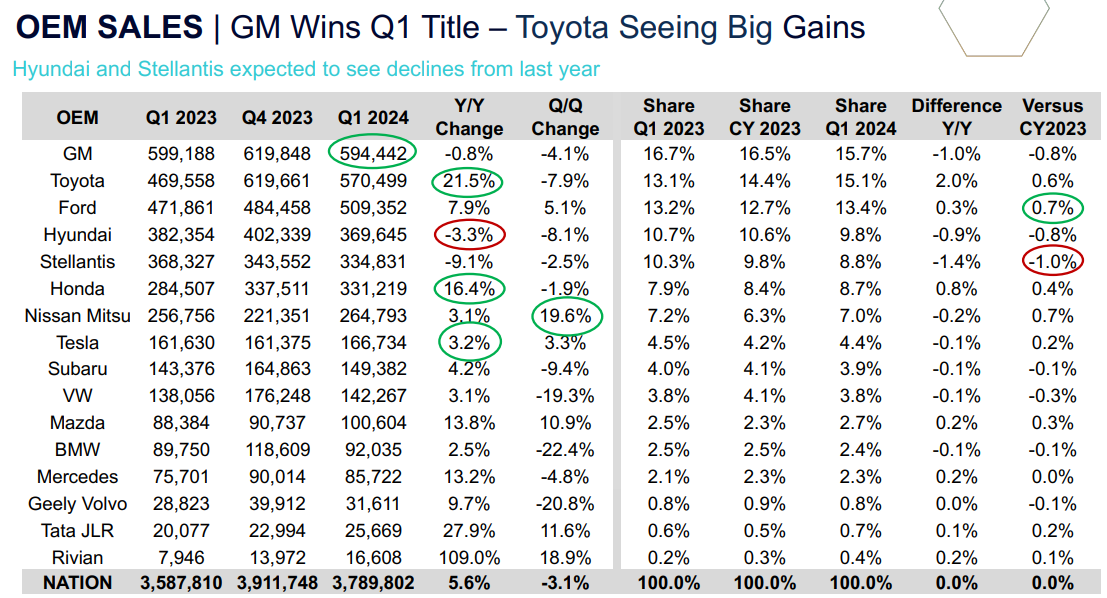

Sales By OEM (include some big trucks)

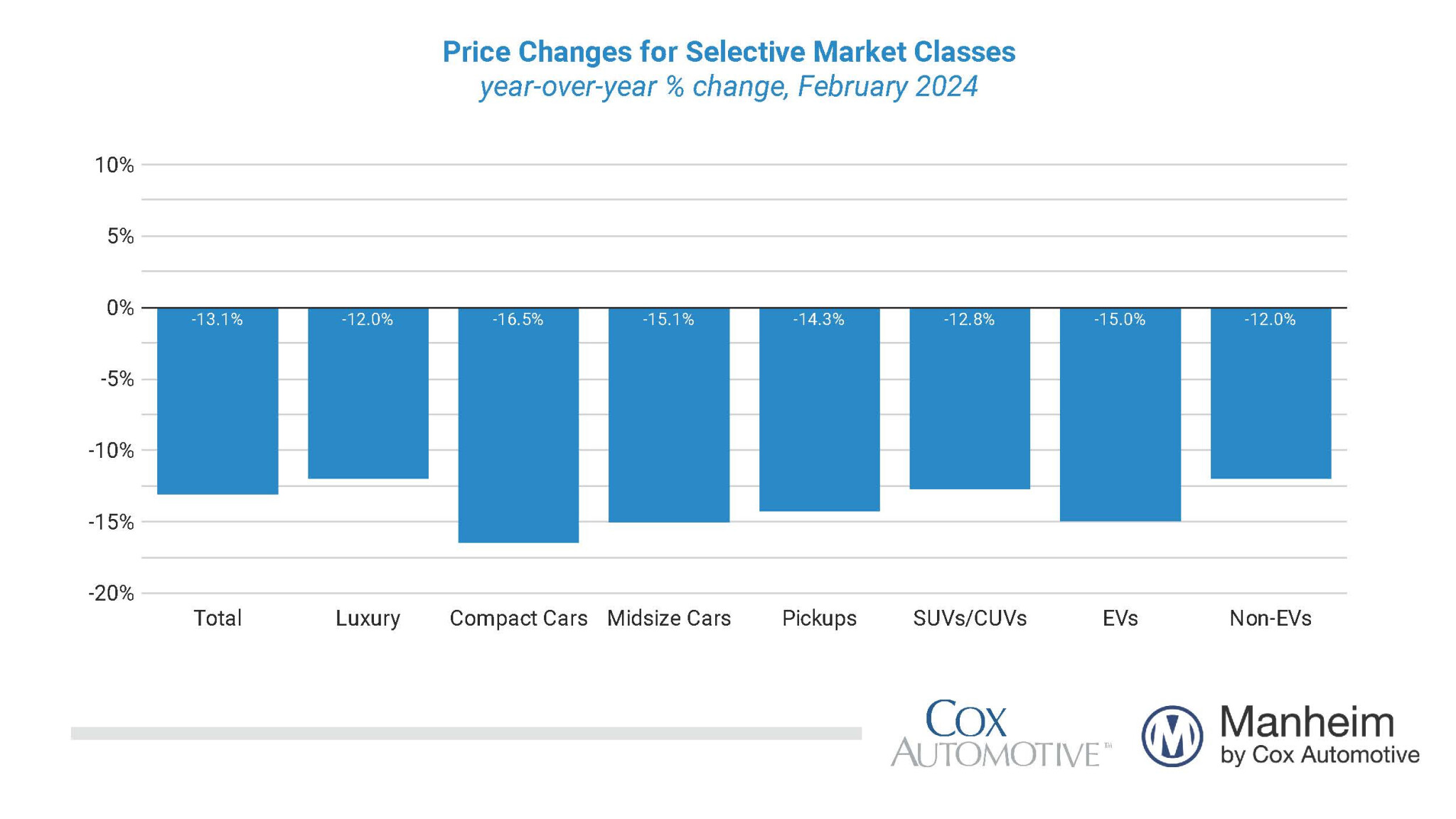

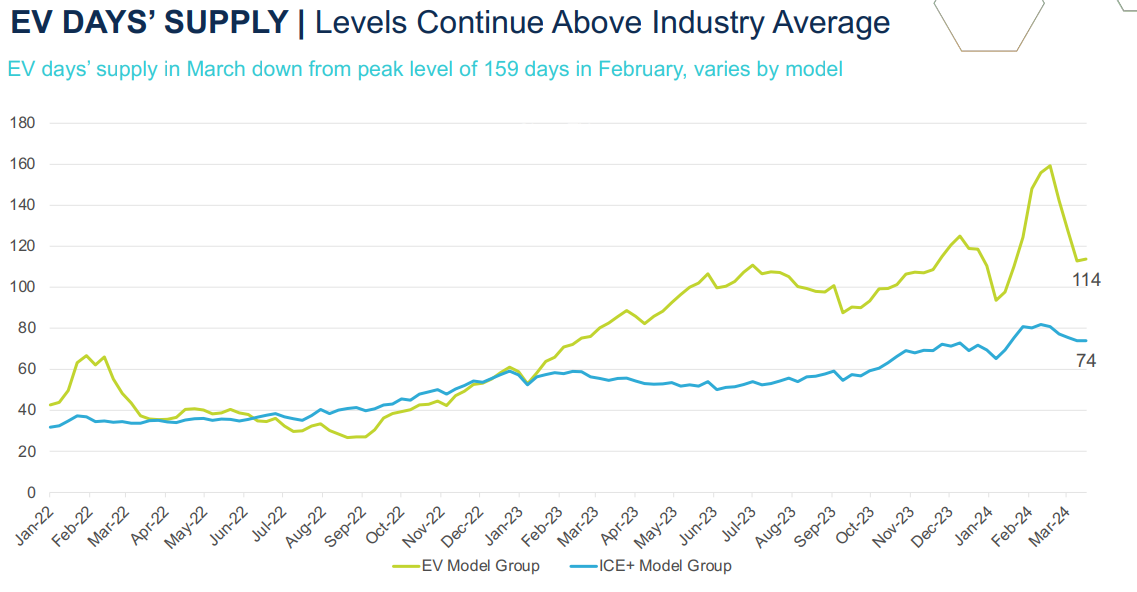

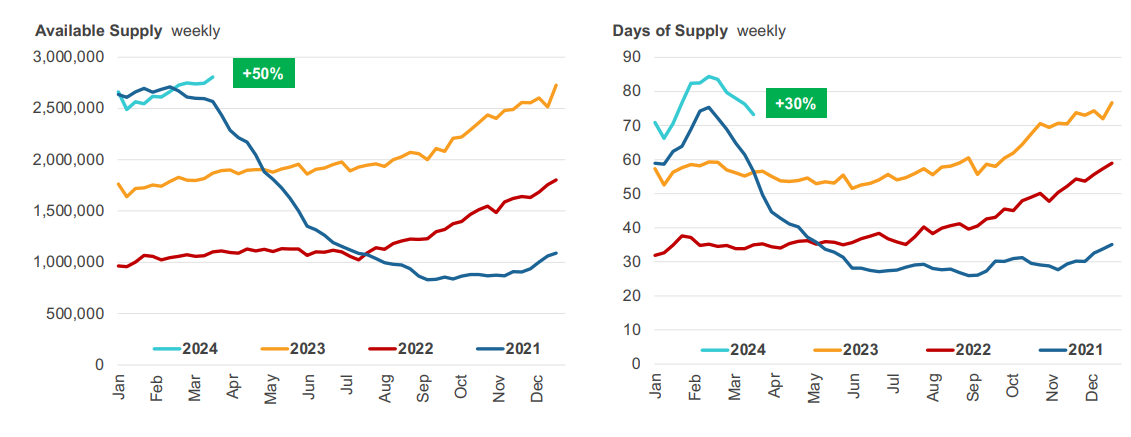

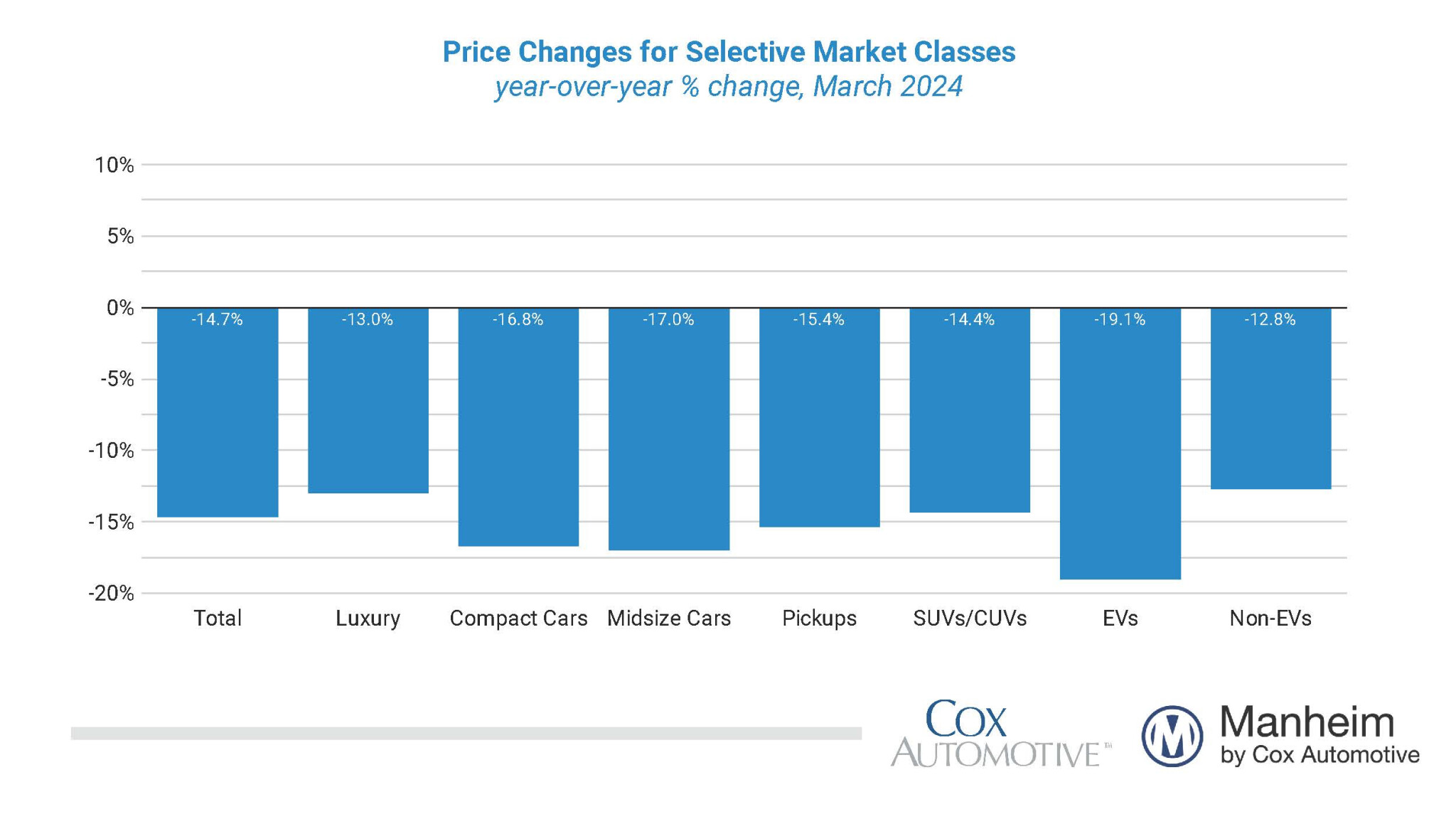

Used Vehicle Value Index (MUVVI) fell to 203.1 in March 2024, a decline of 14.7% from a year ago. Down 21% from the peak.

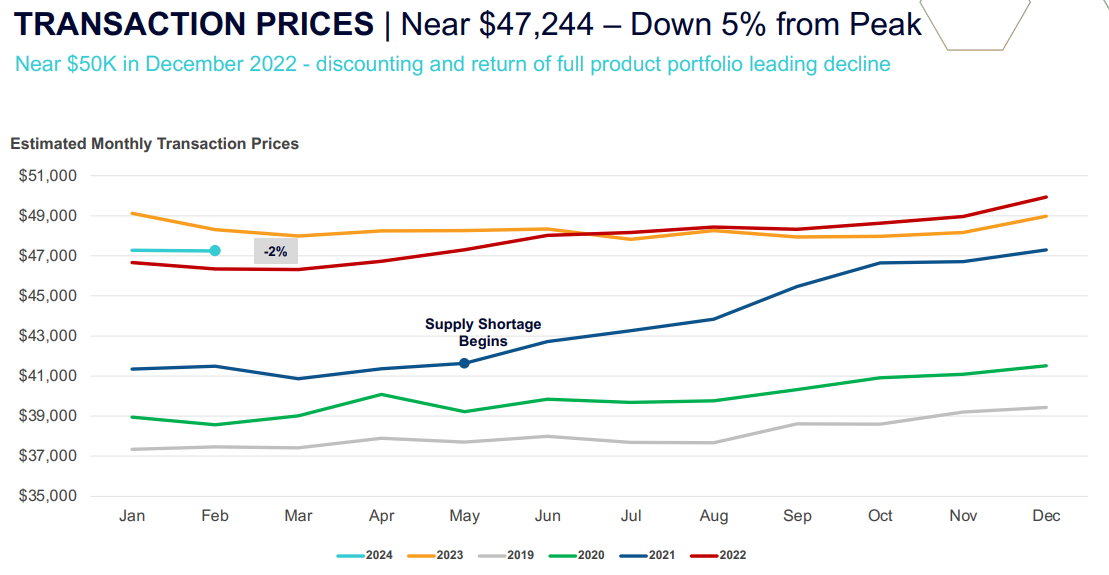

The average price for new vehicles was down 2.6% year over year. And are ~5% down from the peak.

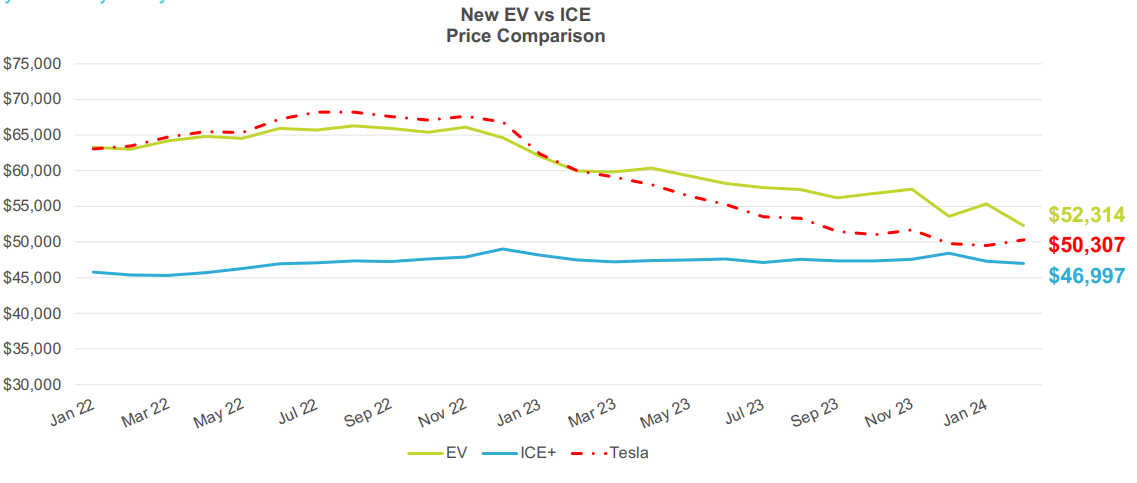

The average transaction price for a new EV in Q1 was $55,167, a 9.0% decrease compared to Q1 2023 and down 3.8% quarter over quarter

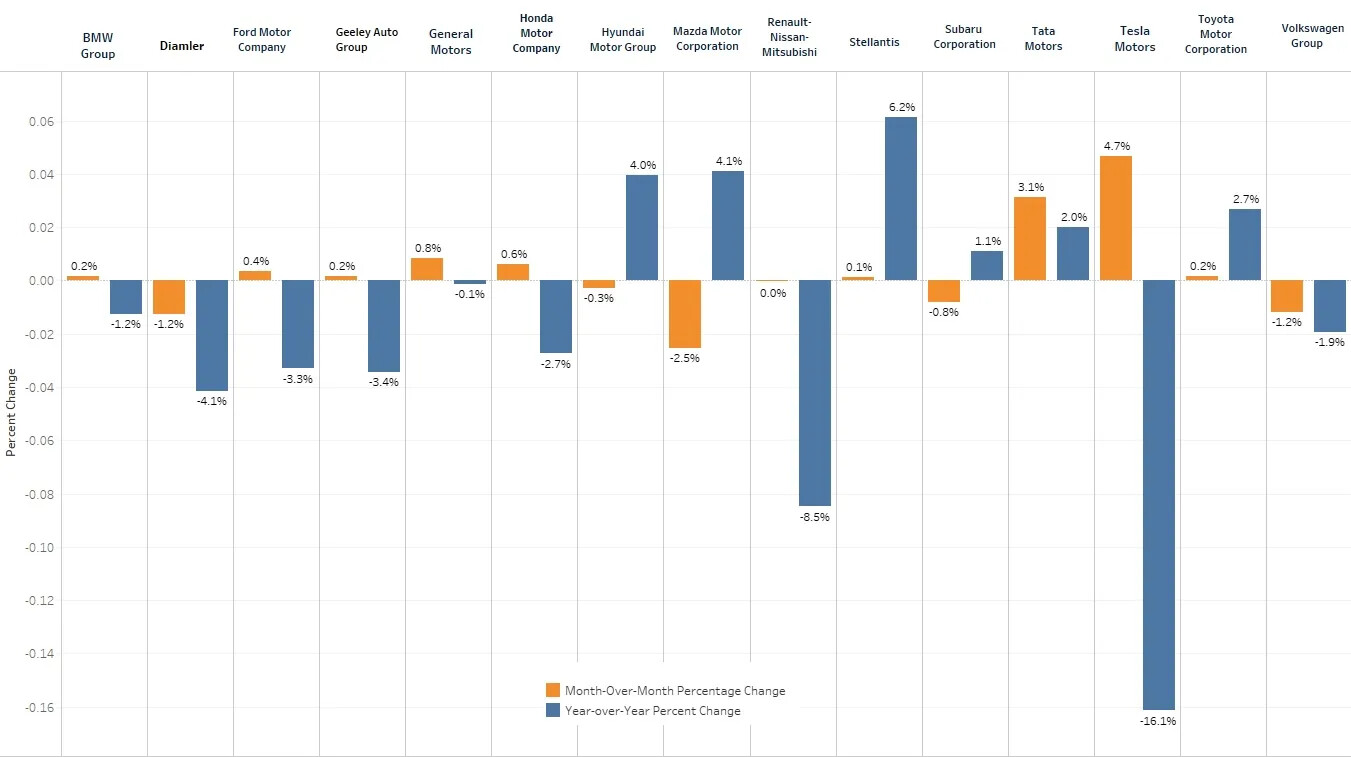

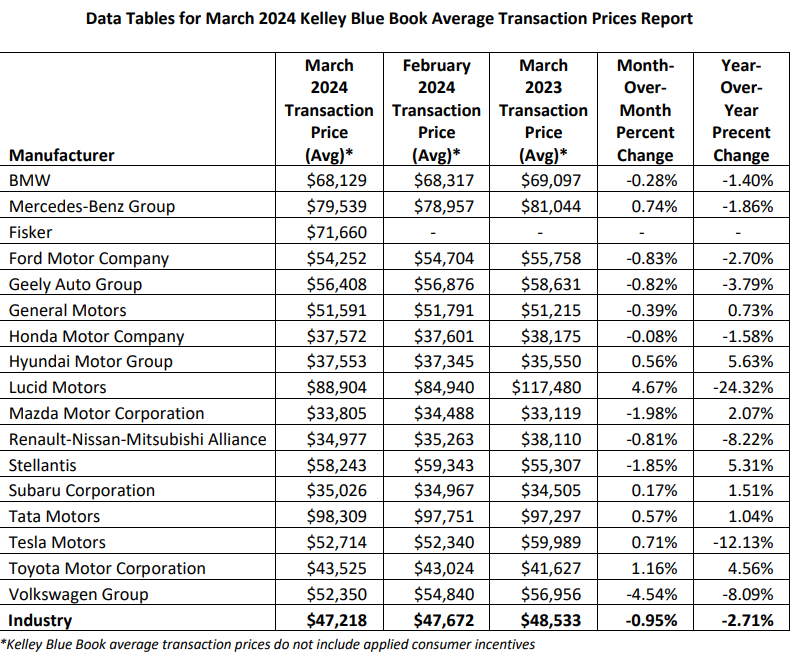

Average transaction prices by Manufacturer

Cox updated its 2024 Forecast

COX Automative Q1 2024 presentation: https://www.coxautoinc.com/wp-content/uploads/2024/03/Q1-2024-Cox-Automotive-Industry-Insights-and-Forecast-Call-Presentation.pdf

Q1 2024 Cox Automotive Industry Insights Webcast Replay Available - Cox Automotive Inc.