I understand the argument, but one thing that seems clear is that everyone underestimated how far Trump was going to go with these tariff threats. Even with the ones put in place before yesterday (removing extensions), the effective rate had already gone up about 4%, from 4% to 7%.

And what Bessent, Trump, and some around him have said about them being somewhat comfortable with short-term pain for long-term gains, makes me think they are still willing to go as far as they can without causing major issues.

Car and auto parts may seem like a significant % of imports, but at the end of the day is only like ~1.6% of GDP (because imports are only like 11% of GDP) So, I think currently there could be negotiations, probably to companies with clear plans to invest on the US, but don’t think he will back away until he sees real ugly damage on the economy or auto industry.

Because while direct impact is low, probably the secondary effects and uncertainty here is what will matter.

I will investigate this more, and share my thoughts on another topic when done.

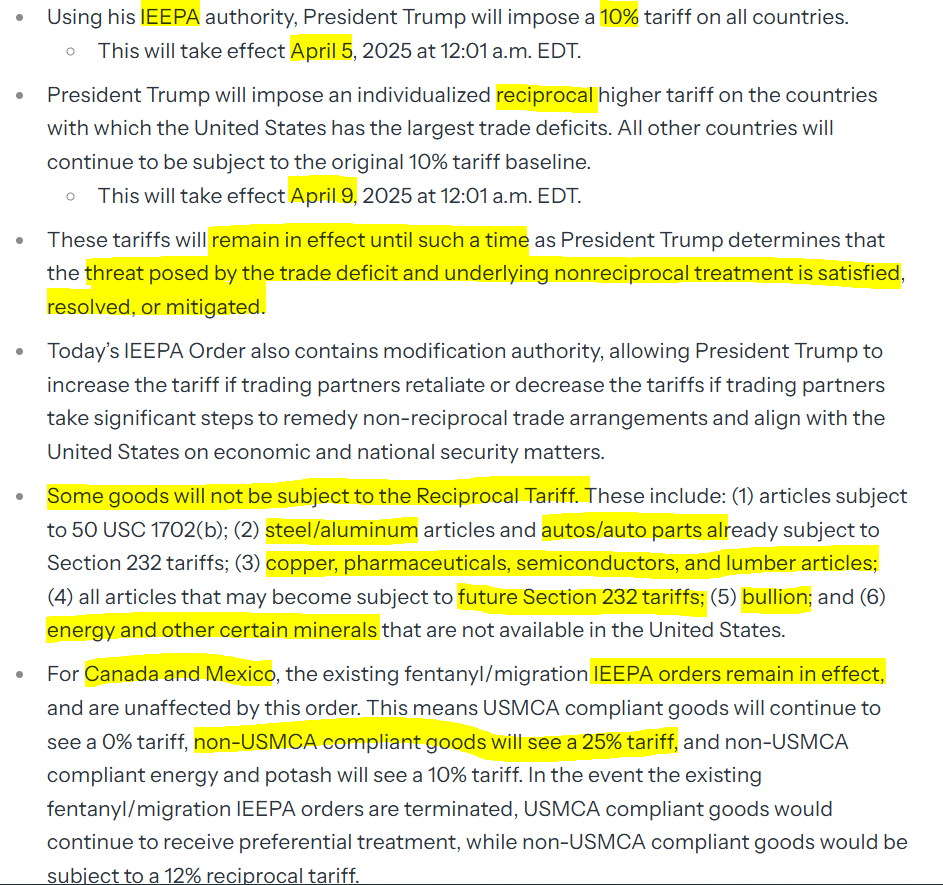

Auto part tariffs will come until May 3, and only non-US parts of imports will be tariffed from the ones coming from Canada and Mexico

This sounds terribly complicated to implement, I have read auto parts could pass the border between 6-8 times before the completed car is finally assembled, so it will not be a straightforward 25% for all cars and auto parts, and will be very dependent on the specific cars components supply chains

This unfortunately adds another layer of uncertainty that will not allow to model clear impacts.

A Senior White House Official says cars coming from Canada and Mexico will only be tariffed on their foreign parts. So if the car has 50% American parts it will see a tariff that is 50% of 25% so 12.5%.

The 25% tariffs apply on April 3 to imported vehicles, but auto parts don’t get the tariff until a "date no later than May 3, when the Commerce Secretary figures out a process to apply the tariffs exclusively to the value of non-US content

I think direct impact will be high esp. psychologically when car prices all the sudden skyrocket and car sales slump.

This could have a lot of ripple effects like inflation expectations unanchoring or consumers pulling certain demand forward because of fears that other items will also get more expensive.

So even though it’s just a small % of GDP and GDP might even temporarily rise due to this it could cause a lot of havoc in the economy.

In addition I would say that even smaller changes in the budget of consumers can hurt. Let’s say someone has fix costs of 1000$ and a more variable budget of 100$ than it can hurt quite a lot if prices overall rise by let’s say 5%.

By this I want to say that it can feel drastic if car prices rise (everything else being stable) Even if it is only a smaller part of GDP and overall costs for consumers it feels like a lot.

In my opinion Trump was always to be taken seriously because he is not afraid to cut ties but on the other side he might still do all of this as part of a negotiation strategy. (Or a strategy in which he either wins in negotiation or gets his tariffs - both outcomes he likes)

Note: Those are just a few theories off the top of my head. I did not previously research them. Maybe you have or find strong indications why I am completely wrong with them and things will play out most likely completely differently

No, I mostly agree with your theories. But I think auto tariffs alone are not enough to cause sufficient damage. For me, are all of these tariffs, policies, and uncertainty combine.

While Auto tariff’s impact on consumer spending is honestly very low (PCE is ~20 Trillion, durable goods spending ~2.2 Trillion), I agree the uncertainty and psychological effects are what will dictate the full impact eventually. But I think it really depends if its sustained or not.

We also have to take into account that the majority of consumer spending (>50%) is coming from the very high earners, who things like this will have a very limited impact.

I did ask deep research about this psychological effect impact on the economy, and while it did not provide a concrete quantifiable impact, it still gave a very good overview of how every downturn or recession is accompanied by high and sustained levels of uncertainty, and the mechanics why is this the case. I am linking it here for everyone who wants to read it.

So, I do also think that the longer the current volatility and uncertainty remains, the very bad negative soft data we are getting, we will need to start to incorporate it more on expectations in hard data also.

I will continue to research for information, and listen to analysts to give a more concrete assessment, but the feeling I am overall getting is that yes this will be very disruptive in a lot of ways, hence it can’t be permanent, and only to negotiate. I just want to make sure people are not just underestimating Trump’s willingness to inflict pain on the economy.

The article on spending is indeed interesting. 10% of consumers account for 49.7% of spending.

(Note: Always good to post a few key insights in the Forum for anyone to get a quick impression esp. those that cannot access the source which is behind a paywall)

I cannot access the results of the GPT query as it is not showing up correctly. I think the better workflow is to likely post the answers in Notion and then publish and link this specific Notion page.

Yes I think you are right and Trump might be willing to inflict serious short term pain to the economy in order to achieve the changes he thinks are right. I think it might even be permanent and we should not rule out this possibility.

According to WSJ and Washington Post, White House aides have drafted a proposal to impose tariffs of around 20 percent on most imports to the United States

First scenario: 20% universal tariff on virtually all imports

Second Scenario: an across-the-board tariff on a subset of nations that likely would not be as high as the 20% universal tariff option, after pushback from option 1

The announcement will come tomorrow at 4pm ET (after hours)

I have read today’s analyst saying the market is not expecting a very adverse announcement and for uncertainty to come down after tomorrow, hence there could be a negative market reaction to more negative than expected news

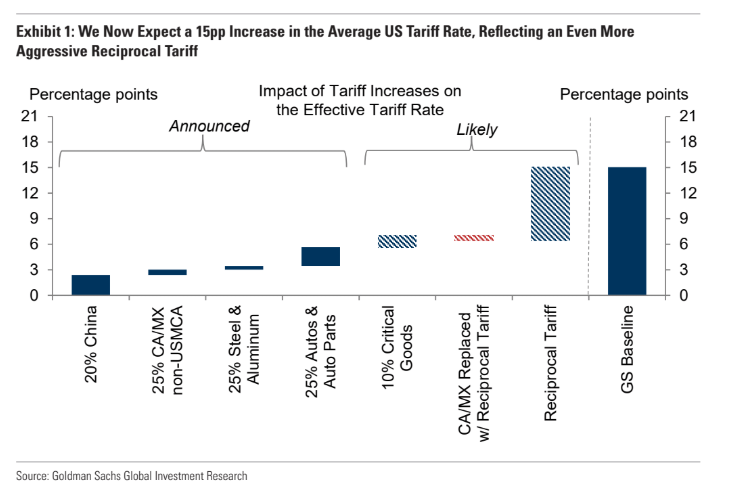

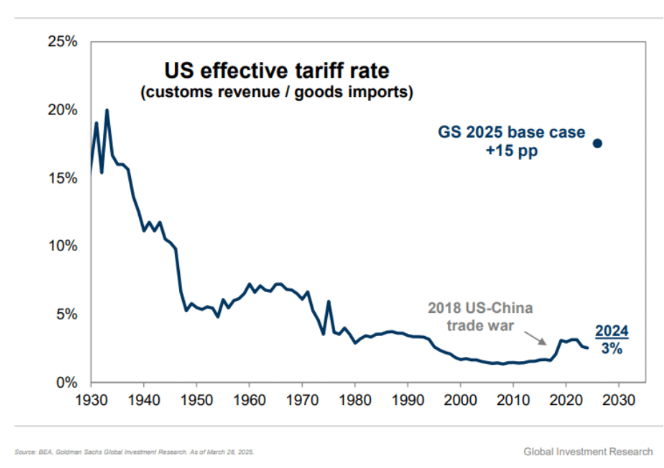

Goldman expects U.S. tariffs to initially rise by 15 percentage points—matching their previous “risk case”, but anticipates that product and country exclusions will trim the effective increase to 9 points.

More Details

“A realization of our new tariff baseline would likely come as a negative surprise to markets. Our recent survey of market participants indicated that the average investor expects the effective tariff rate to increase by roughly 9pp this year, while only a very small share (4%) expect an increase of 15pp or more.”

Mike Wilson (Morgan Stanley)baseline is for higher tariff on China goods, product specific tariffs on European and Asia ex-China goods, and de-escalation on Mexico and Canada. But market could sell of to lower end of firm forecast (5500) if tariffs news are more restrictive than expected.

More Details

He sees the announcement as “likely a stepping stone for further negotiations, as opposed to a clearing event,” with upside capped at 5,900 even in a better-than-expected announcement absent “clear reacceleration in earnings revisions breadth, something we are currently not seeing at the index level,” which could take it to 6,100 he says.

A worse than expected announcement likely takes the index back to the 5,500 level.

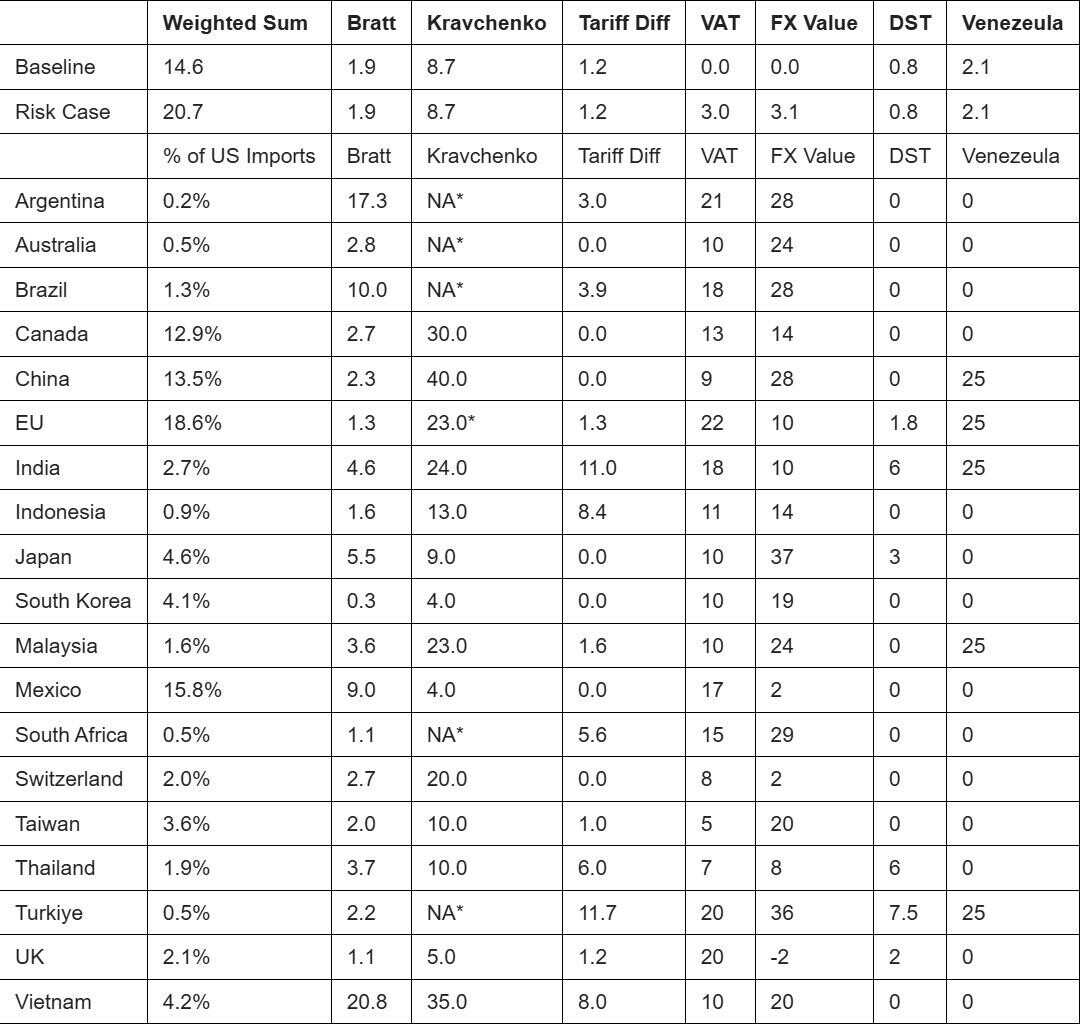

BBG columnist Simon Flint Agrees with Goldman that equity risks are tilted lower and believes the projected 6pp tariff hike now and 8pp in 2025 are likely underestimated.

More details

He says because of recent news reports investors believe “tariffs may be applied with a scalpel rather than a sledgehammer,” but he says there are many risks:

the opening numbers on April 2 may be larger than markets expect

the assumption that tariffs will be revised down significantly may be wishful thinking.

even if they are walked back, the constant flip-flopping is itself a drag.

while the rest of the world may be playing nice for now, don’t mistake politeness for weakness.

the damage to global cooperation, norms, and institutions could be long-lived and hard to reverse

He says current expectations for a “modest ~6 percentage point increase in tariffs due to reciprocal duties, and an 8 percentage point hike for 2025 as a whole” will likely prove to be too low. He builds off of Goldman’s work and comes up with his own table of expectations assuming all non-tariff barrier’s are taken into account.

If so, “we get an eye-watering 20.7 percentage point increase (as per the second row), drastically greater than the current expectations ‘priced in’.”

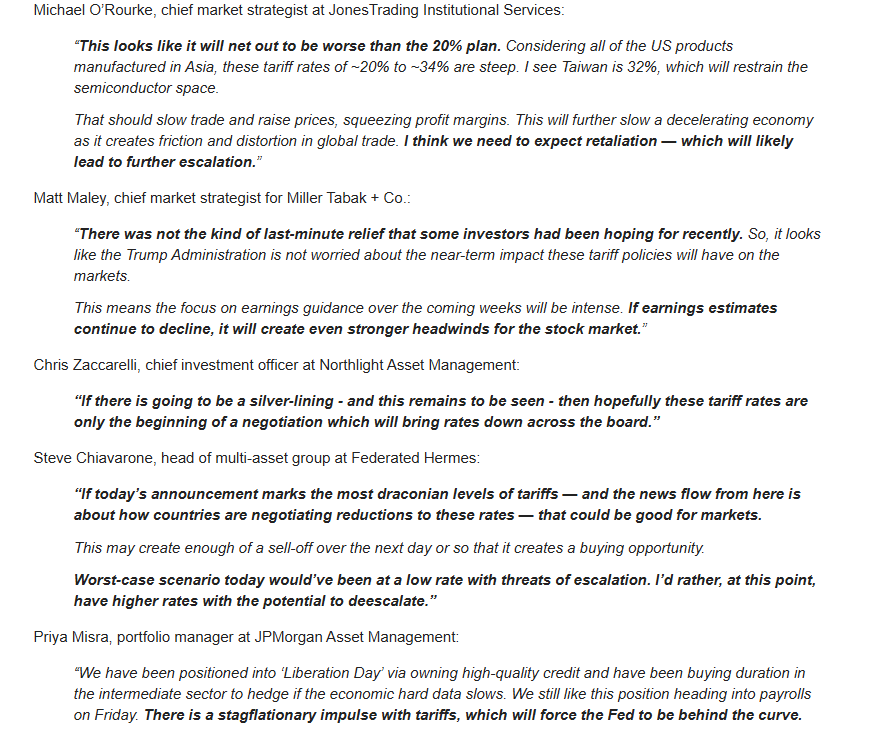

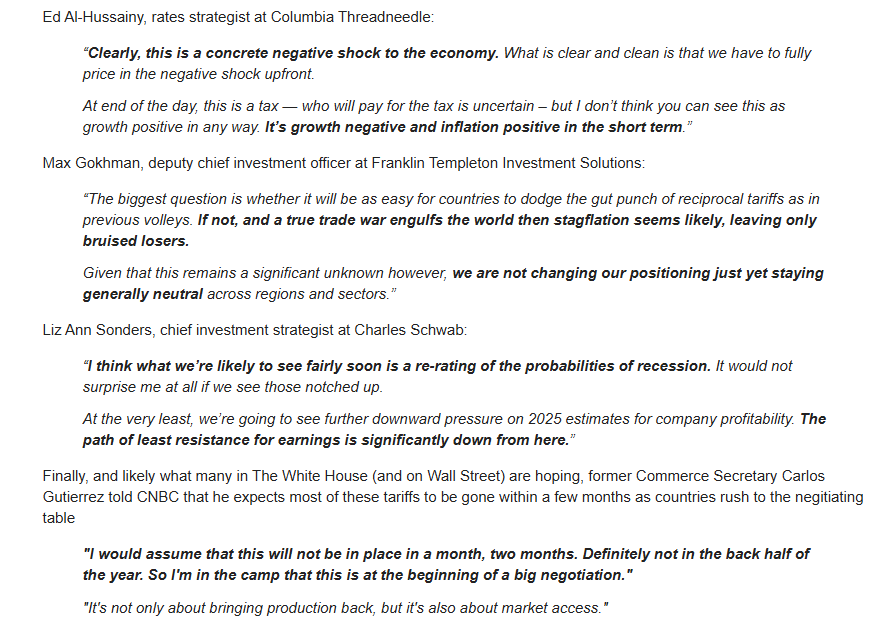

Some of Wall Street Reactions to the Tariffs Announced

The consensus across these quotes is broadly negative, with most viewing the tariffs as a growth negative, inflationary shock that increases recession risks, earnings pressure, and the chance of stagflation.

However, few also see this at the worst it can get, and potential for de-escalation or negotiation down the line.

Goldman which was already one of the few expecting a very adverse scenario today says this is worse than expected

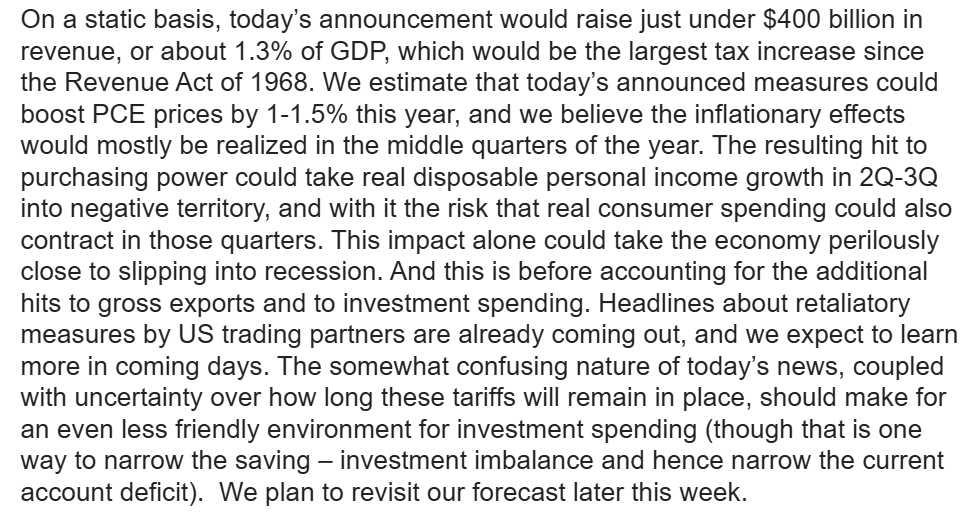

On our desk we are currently witnessing long selling of tech names and aggressive HF shorting in macro products… we think when you throw everything into a blender you get closer to a US effective tariff rate of 20%…vs our 15% baseline assumption … Not good… This will hit GDP growth, push inflation higher, and keep pressure on the US stock market. Uncertainty has not been tamed. With what we know right now we are clearly looking at a very challenging day for the US stock market tomorrow (feels like a S&P 500 down 4% ish type of session)…What we just got hit with appears to be significantly above our +15% base case.

JPM says today tariffs could increase PCE inflation by ~1-1.5%, and bring the economy very close to a recession

Tariffs to hit:

Real disposable income hence consumer spending in middle part of the year

Exports if retaliation happens

Investment spending if uncertainty continues

I currently think some of these tariffs will be negotiated and not final yet (Bessent kind of hinted it here), but the uncertainty how, when, and with whom is what will matter the most going forward because then worse case scenarios will need to be taken into account by everyone.

EU Commission said it’s working on further counter-measures to Trump tariffs

EU Commission President Ursula von der Leyen said they are preparing further countermeasures to Trump tariffs if negotiations fail.

“We are prepared to respond,” she said. “We are now preparing for further countermeasures, to protect our interests and our businesses if negotiations fail.”

The EU already announced that it will introduce counter-tariffs on $2.6 billion worth of U.S. goods in mid-April.

Dow Jones futures is currently down 2.5%, S&P 500 futures is down 3.1% while Nasdaq 100 is down 3.4%.

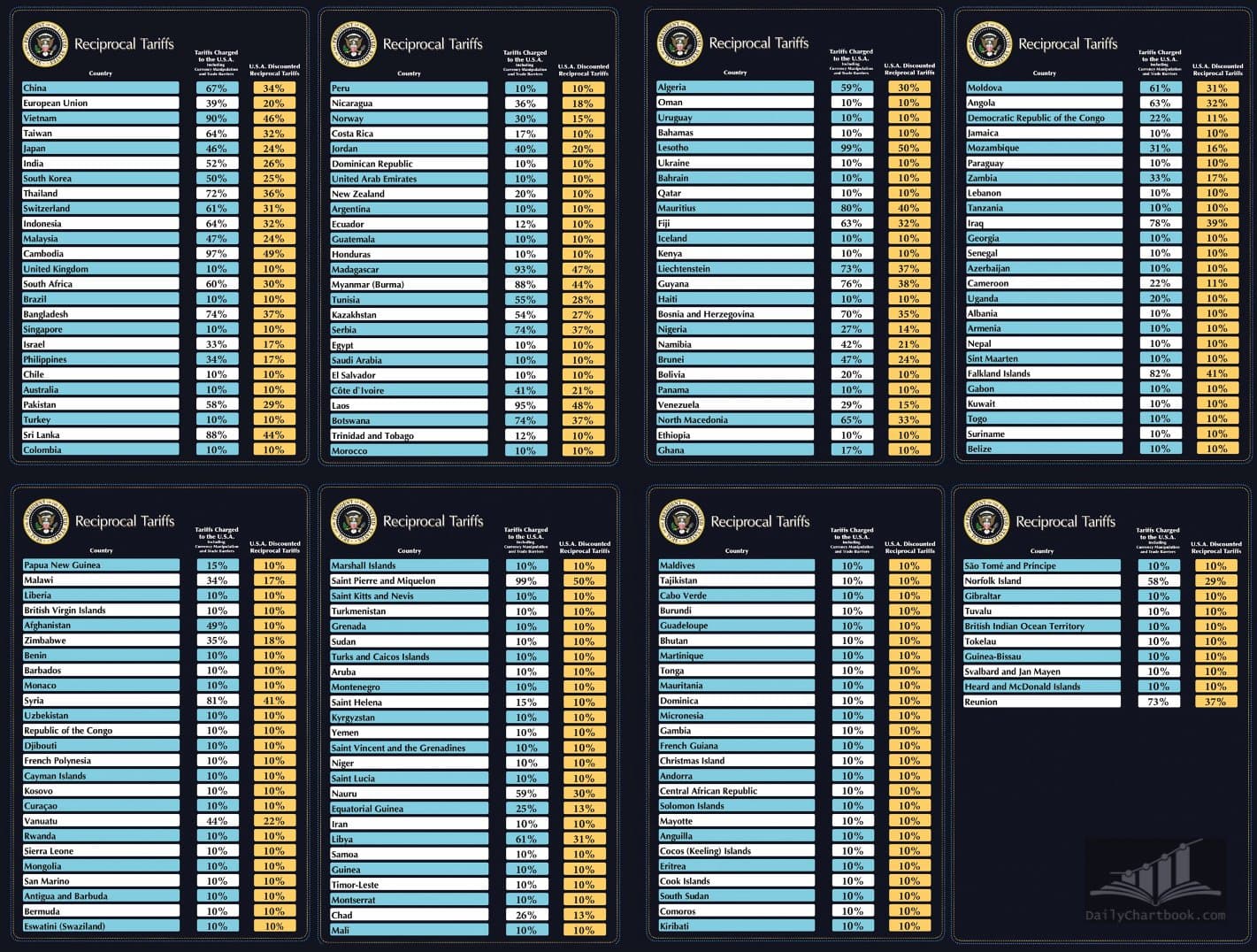

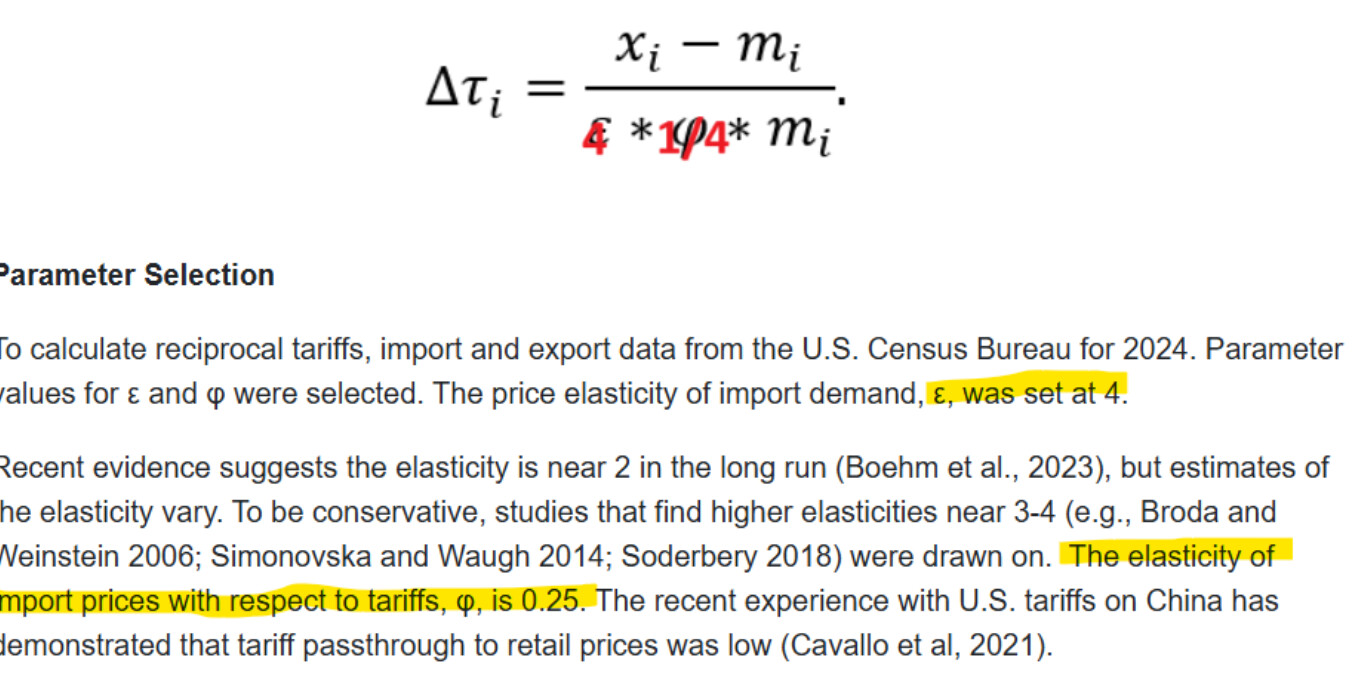

@Magaly I just read on X that in Trumps chart the “tariffs charged to the U.S” are in fact simply the U.S trade deficit divided by total imports from that country. (And if the U.S has a trade surplus it’s 10%)

Can you confirm this is the case? For the EU numbers make sense. The U.S has a trade deficit of 235.6billion while they imported 605.8billion → 235.6billion/605.8billion = 39%.

Same for Japan. Deficit of 68.5billion/148.2billion imports = 46%

I found also here a page in which they describe calculations but It looks like they made the explanation artificially difficult to understand.

I think to get a better take on what is going on we should look into more historic example of tariffs like Smoot/Hawley or other examples to reach an assessment. Maybe deep research can help as well.

Yes, it is. According to the parameters they choosed, the Greek letters cancel each other out, and in the end, it’s only: (exports—imports)/imports.

Apparently, they are only using 1/2 of this for their final numbers. eg 20% for the EU.

It will be difficult to find a precedent similar to this, according to Goldman charts we would have to go to the 1930s to find a similar rate of tariffs, as you also suggested. Which obviously was a completely different economy back then, and was intertwined with the great depression.

Will try to see what I am able to gather with deepresearch.

Good thanks. I see that you mentioned possible negotiations here and I wonder what a positive negotiated outcome that Trump is aiming for could be that some analysts mention. (If negotiation is the goal and not simply bringing manufacturing back via protectionism)

The EU claims that on average only around 1% tariffs are collected currently on trade of goods on each side (does not mention services)

This obvs. does not take into account areas in which trade would be possible but is not facilitated because of tariffs. So maybe e.g. the 10% on cars that the EU is applying does not make it feasible to export any U.S cars into the EU and therefore the EU does not collect tariffs on it simply because trade barriers are too large. (Making the EU numbers misleading as well)

I would be interested in some research (maybe using deep research or other studies) of trade barriers currently in place by major U.S trade partners that makes U.S exports in those areas impossible and an assessment if it would be likely Trumps goal to bring them down.

I also would be interested in any commentary/analysis why he is literally targeting the whole world at once and if the 10% minimum tariffs applies indeed on countries the U.S. has a trade surplus with.

If this is the case it makes it less likely that there is something to negotiate for but it looks more like a protectionist policy

US exports to China are only $143 B in 2024, even if exports to China are cut in half due to new tariffs, this would mean only a ~0.25% headwind to GDP from exports. This is only the direct effect, secondary effects as less employment and investment would also take place, but still only minor imo.

Trump warns no China deal without trade fix, signals market pain may be inevitable

Trump said in Saturday that he will not make a deal with China until they solve their trade surplus.

“We have to solve our trade deficit with China,” he said. “We have a trillion-dollar trade deficit with China, hundreds of billions of dollars a year we lose with China. And unless we solve that problem, I’m not going to make a deal.” “I’m willing to deal with China,” he added, “but they have to solve their surplus.”

He said he doesn’t want the stocks to go down but there’s nothing they can do.

“I don’t want anything to go down, but sometimes you have to take medicine to fix something,” he said.

EU offers the U.S. zero-for-zero tariffs on industrial goods

EU Commission President Ursula von der Leyen said the EU has offered the U.S. zero-for-zero tariffs on industrial goods.

“We have offered zero-for-zero tariffs for industrial goods as we have successfully done with many other trading partners. Because Europe is always ready for a good deal. So we keep it on the table. But we are also prepared to respond through countermeasures and defend our interests,” she said.

Peter Navarro, White House Senior Trade advisor said the willingness to negotiate is “a good, small start,” but non-tariff barriers, are “orders of magnitude” (min 5:30).

Industrial goods are products used to produce other goods or services. Examples are machinery and equipment.