@Aron I tried to gather information about it here, but unfortunately quality information about this industry is very scarce. I will continue to look for credible sources or data, and post it in that channel.

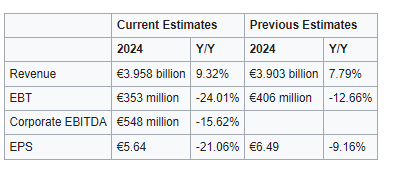

Following new insights during the Q2 earnings such as percentage of risk vehicles in different regions, cost-efficiency measures, demand and pricing trends, I have updated the 2024 estimates as follows;

Headwinds considered in the update include;

60 million euros increase in depreciation and amortization expense.

55 million euros increase in other operating expenses.

Travel demand is non-discretionary: Consumers are already cutting back on travel due to macro uncertainty. However, expected increases in new car prices may drive some consumers to use rental cars while delaying purchases.

Tariffs will increase the residual value of Sixt’s U.S. vehicles: At the end of 2024, 87% of Sixt’s North America fleet consisted of risk vehicles. U.S. used car prices fell 2.3% in 2024, and Sixt’s U.S. depreciation expenses more than doubled to €284 million. This makes North America the main driver of Sixt’s depreciation costs. Cox Automotive estimates that tariffs could increase used car prices by 2.8%, likely reducing depreciation expenses.

Sixt will be impacted by a recession, but not severely: In the 2009 recession, Sixt’s revenue declined 10%, compared to 17% at Hertz and 14% at Avis. Current estimates suggest any potential recession will be milder than 2009.

Car rental companies tend to reduce expenses during downturns: Sixt and peers historically cut fleet and personnel costs during macro slowdowns to preserve margins.

Tariffs will weaken international inbound travel: Inbound demand supported Sixt’s Germany and Europe revenue in 2023–2024, when there was macro slowdown. However, tariffs are expected to negatively affect travel volumes, especially from the U.S.

Premium positioning offers pricing resilience: Sixt’s average revenue per unit (ARPU) is estimated to be 30–40% higher than that of Hertz or Avis. This premium mix gives Sixt better protection against pricing pressure in a demand slowdown.

Based on these estimates, Sixt is somehow positioned to withstand a macro slowdown. While a macro slowdown would weigh on travel demand, the impact on earnings would be partly offset by the increase in residual values. Given the low probability of a severe recession and the company’s structural advantages- including premium positioning and fleet flexibility- the downside to earnings appears limited. Therefore, I would recommend a buy considering the attractive valuation.

Hmm interesting. Are you buying yourself and if not which open questions hold you back? How could they be resolved?

I think you are raising a couple of good points but i would be interested in commentary on details how you translated each of them into the valuation model.

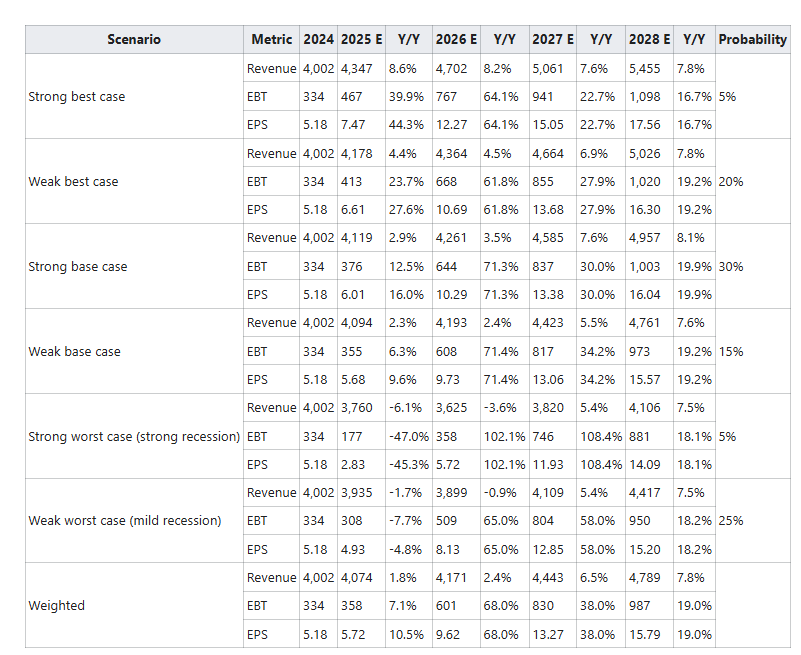

For example I see that in the worst case scenario you model an approx. 10% revenue decline by 2026 but think EPS will recover then again already to 2024 levels due to cost cutting. Why do you think they can achieve the same results with a 10% smaller revenue base by then?

I know that quantifying things can be hard and is often based on best guesses (based on current knowledge), but ideally I like to understand which kind of impact (ranges) all the points you mentioned have to understand what is most important and how we should think about them.

I also see that you have extremely bullish midterm projections (2028E) as you expect sixt will earn around 15€ EPS in all scenarios. Is this a mistake or are those outlooks outdated?

If no what is your bull case why you think Sixt will be able to drive such exceptional margin expansions and reach this very high profitability?

No, I’m not buying yet. I don’t like that it’s cyclical, which makes future forecasts uncertain. I’m also waiting for more clarity on the trajectory of tariffs, since used car prices are a key driver of my estimates. That said, if the stock were to fall further to the €40-45 range, I might consider buying.

Here is how I translated each assumption into the valuation model:

Sixt’s strategy during economic uncertainties involves cutting down on variable costs. At the end of 2023, 77% of Sixt’s operating expenses were variable (page 42). I have used variable costs as percentage of revenue to model them. This means that if revenue falls, these expenses will reduce as well.

The large share of variable costs makes it possible to have a lower revenue and better EPS. For instance in 2022, Sixt’s revenue was €3.0 billion yet EPS was €8.23. Similarly, 2023’s revenue was €3.6 billion yet EPS was €7.15. Therefore, to answer your question, with a revenue of €3.6 billion, it’s possible to attain an EPS of €5.72 in 2026. The drop in 2024 EPS by around €2.0 was driven by an increase in depreciation expense.

As noted above, Cox expects price of used cars in the U.S. to rise by 2.8% in 2025 due to tariffs on imported new cars. This is slightly larger than the 2.3% drop in 2024. As a result, the uptick in used car prices coupled with almost 100% share of non-risk vehicles in Europe should reduce Sixt’s depreciation expense in 2025 and 2026.

I modeled revenue estimates based on expected GDP growth rates. According to GPT Deep Research, there is a strong correlation between Sixt’s Europe revenue growth and Euro area GDP growth- approximately 0.9% revenue growth for every 0.1% increase in GDP. I applied a slightly lower sensitivity (0.7%) to allow for a margin of safety.

Sixt’s revenue and Germany GDP growth rate are highly uncorrelated. However, based on past performance, Germany revenue growth rate has been slightly higher than that of Europe.

According to GPT Deep Research, Sixt’s U.S./North America segment shows the highest sensitivity to GDP, with revenue growth changing by approximately 16% for every 1% change in U.S. GDP. For my estimate, I assumed a 7% revenue increase per 1% GDP growth to include a margin of safety. This projection was guided primarily by Sixt’s 2024 revenue performance.

I assumed that, if there will be a strong recession, Sixt’s U.S. revenue is likely to decline by around 10%, slightly lower than that observed by Avis (-14%) and Hertz (-17%) in 2009 given that Sixt has a larger share of premium vehicles.

Yes, you are right. The 2027 and 2028 estimates were outdated and used highly bullish depreciation expenses. However, my 2028 weighted EPS estimate of €10.4 is still bullish, driven mainly by revenue and continued cost efficiency.