This topic discusses the upcoming Q3 2025 Meta Platforms earnings. It will include our final assessment and decision before the earnings release. We will also summarize the results here. You can find our earnings preparation and full summary of the results in the Notion:

Earnings date: October 29, 2025

Time of Earnings release: 4:00 PM ET

Time of Analysts Call: 4:30 p.m. ET

Tinuti Digital Ads Benchmark report signals Meta’s Q3 2025 revenue could grow at 23%-24%

Ad spent growth on Meta Platforms by Tinuiti advertisers accelerated to 14% in Q3 2025 from 12% in Q2, impression grew 16% y/y- the strongest growth since Q4 2023 while CPM fell 2% y/y (Q2 2025: -0.5%).

Ad spend on Facebook rose 9% y/y (Q2 2025: +12% y/y), impression grew 15% y/y (Q2 2025: +18% y/y) while CPM fell 6% (Q2 2025: -0.5% y/y) due to rising Reels inventory (Reels carry lower CPM than Feed and Stories ads).

Spend on Instagram ads rose 21% y/y (Q2 2025: +11%)- largely due to weak comps, impression jumped 9% y/y- the strongest growth since Q1 2024 while CPM growth decelerated to 11% from 12%- also due to rising share of Reels inventory.

The share of Advantage+ shopping campaigns’ (ASCs) slipped again to 27% from 35% in Q2 2025.

Ad spend growth on TikTok fell 4% y/y (Q2 2025:-20%), impressions rose 23% y/y (Q2 2025:+3%) while CPM fell 22% (Q2 2025:-22%).

Ad spend on Google search rose 10% y/y (Q2 2025:+11%), click through rate (CTR) accelerated to 11% (Q2 2025: +7%) while cost per click (CPC) fell 1% (Q2 2025: +3%).

Assessment

Over the most recent seven quarters, Meta’s reported revenue growth has outperformed Tinuiti’s Meta ad spend growth by an average of 9.35%. Based on the Tinuiti report, which has historically been a reliable indicator of Meta’s revenue growth, Meta’s Q2 2025 revenue could grow at 23%-24% .

Over the most recent seven quarters, Meta’s reported ad price per ad has outperformed Tinuiti’s Meta CPM by an average of 8.25%. As such, Meta’s ad price per ad could grow by around 6% in Q3 2025, a deceleration from 9% in Q2 2025. Given Meta’s focus on reels, I expect ad price per ad to continue decelerating in the near-term. Hence, Meta’s ad revenue growth in the near-term will likely be driven by market share gain (due to rising impression) and not CPM growth.

I like that Instagram impressions rebounded during the quarter, reinforcing third-party reports of solid engagement growth on the platform (Notion).

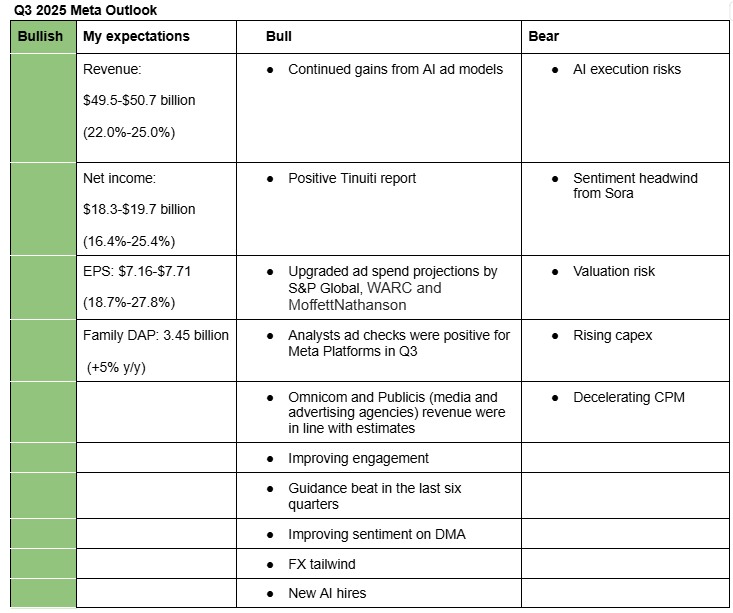

I am bullish on Meta’s Q3 2025 earnings. My estimates (see Google Sheet) are based on continued gains from Meta’s AI-driven ad models, insights from the recent Tinuiti report, upgraded ad spend forecasts, positive Q3 results from major media and advertising agencies, and Meta’s consistent guidance beats over the past six quarters.

Here is a description of by bullish and bearish sentiments:

Bullish sentiments

Continued gains from AI ad models: Meta’s AI ad models such as Andromeda and GEM continue to get better in retrieving and ranking ads and targeting users with relevant ads. CEO Mark Zuckerberg said (Notion) Q2 2025 revenue outperformance was largely due to these AI models “unlocking greater efficiency and gains”. Meta is still launching these models across its platforms (Notion), hence further tailwind is expected. Also, Meta expects Gen AI to boost its recommendation landscape further.

Positive Tinuiti report: Tinuiti’s Q3 2025 Digital Advertising Benchmark report report shows that ad spend on Meta Platforms grew 14% y/y. Historically, Tinuiti has been a reliable indicator of Meta’s ad revenue. Based on the report, Meta’s Q3 revenue could grow by at least 23%.

Upgraded ad spend projections by S&P Global, WARC and MoffettNathanson: Recently, S&P Global, WARC and MoffettNathanson raised their ad spend projections for 2025, signaling that sentiment has improved after a shaky start to the year. S&P Global raised 2025 growth estimates for US digital advertising spend to 9.5% from 6.7%. WARC raised 2025 global ad spend forecast by 1.2% to 7.4% while MoffettNathanson raised 2025 growth estimates for US advertising spend by 0.3% to 6.3%.

Analysts ad checks were positive for Meta in Q3: Several research firms such TD Cowen, Piper Sandler, Guggenheim, and Deutsche Bank said (Notion) their Q3 2025 ad checks were positive for Meta Platforms.

Omnicom and Publicis (media and advertising agencies) revenue were in line with estimates: Omnicom Group and Publicis reported (Notion) Q3 2025 revenue growth rates that were in line with estimates. The two firms said they have not seen budget cuts and Publicis even raised its 2025 revenue guidance. Advertising spend typically flows first through media and advertising agencies. In a macroeconomic slowdown, advertisers often bypass agencies. Therefore, continued strength in agency spend suggests positive momentum for Meta Platforms.

Improving engagement: Third-party estimates (Notion) indicate that engagement in Meta Platforms, particularly in Instagram continues to improve. Citizens Financials said Instagram’s global time spent rose 18.5% y/y in September, the fastest growth rate since March 2024 and representing a 20 basis points increase from August. Similarly, Facebook saw a 5.6% increase in time spent by U.S. users, increasing 380 basis points month-over-month.

Guidance beat in the last six quarters: Meta Platforms has beaten management’s mid-point revenue guidance by an average of 4% in the most recent six quarters. It has also beaten management’s upper-point revenue guidance by an average of 2% in the most recent three quarters.

Improving sentiment on DMA: Recent reports indicate that Meta and the EU Commission are close to reaching a workable solution regarding the “pay or consent” model. I had estimated that the DMA could lead to a $3.8 billion revenue headwind in 2025 and Meta’s management also expected significant headwind as early as Q3 2025. Based on commentaries, it’s unlikely that Meta made any drastic changes to its ad targeting model in the EU in Q3.

FX tailwind: Meta’s Q3 2025 revenue will likely benefit from the weaker U.S. dollar against major global currencies. Management guides FX tailwind of 1% in Q3, in line with my rough estimate.

New AI hires: Meta continues to recruit top AI engineers and researchers from OpenAI, Google, and Apple. I expect these new AI hires to address Meta’s underperformance in large language models (LLMs) in the medium-term.

Bearish sentiments

AI execution risks: Managing newly recruited top AI talent could prove challenging, as many were former team leaders in their previous roles. Their high compensation packages and Meta’s heavy reliance on them may also dampen morale among long-tenured employees. Meta’s recent decision to cut 600 out of 3,400 AI roles—its fourth AI team restructuring—underscores ongoing organizational volatility and raises execution risk.

Sentiment headwind from Sora: Sentiment on Meta Platforms shares has been under pressure recently following the launch of OpenAI’s TikTok-like Sora. Some investors are concerned that Sora may steal user engagement from Social Media platforms such as Meta Platforms. I don’t expect Sora to be a major risk given Meta’s strong network effects. However, Instagram’s user engagement may come under pressure in the coming months as users test Sora (Notion).

Valuation risk: Trading at a trailing twelve-month (TTM) P/E of around 26.6, Meta’s share price could face a significant pullback if the company slightly misses expectations or if management delivers negative commentary on AI.

Rising capex: Based on recent management commentary, it’s likely that Meta will increase capex guidance for 2025 further. Growing capex and ongoing underperformance of its Gen AI models may limit further upside for Meta shares. I expect Meta to increase its capex guidance for 2025 to a range of $68-$72 billion, up from $66-72 billion (Depreciation Model-Google Sheet).

Decelerating CPM: Meta’s focus on reels is creating pressure on CPM since video carries lower monetization compared to Stories and Feed. Hence, Meta’s ad revenue growth in the near-term will likely be driven by market share gain (due to rising impression) and not CPM growth. However, I expect CPM to stabilize after a while and to benefit from growing efficiency gains from AI ad models.

Here are management’s and analysts’ expectations for Q3 2025;

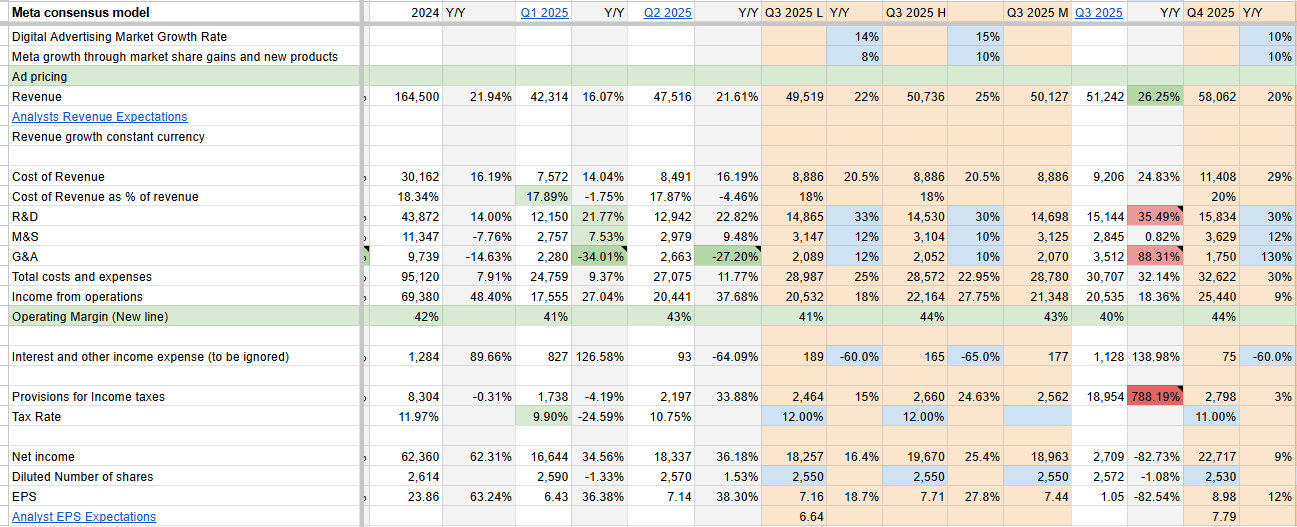

Management Guidance for Q3 (Revenue): $47.5-$50.5 billion (+17.0% to +24.4%)

Analysts’ Estimate for Q3 (Revenue): $49.57 billion (+22.1%) Analysts’ Estimate for Q3 (EPS): $6.72 (+11.4%)

Analysts’ Estimate for Q4 (Revenue): $57.2 billion (+18.2%) Analysts’ Estimate for Q4 (EPS): $8.11 (+1.2%)

Recommendation

Overall, given the resilience of the advertising market, Meta’s continued market share gains, ongoing improvements in its AI-driven ad models, improving regulatory sentiment in the EU, and rising user engagement, I reiterate a Hold rating on Meta shares. However, should there be any pullback driven by negative sentiment surrounding Sora or AI developments, I would view it as a buying opportunity.

Meta beat revenue estimates in Q3, provided a conservative guide for Q4, and said its CapEx expectations have risen

Meta’s Q3 2025 revenue rose 26% y/y to $51.24 billion, above management’s upper guidance of $50.5 billion and analysts estimate of $49.57 billion while operating margin of 40%, was roughly in line with analysts estimate of 39.3%.

EPS came in at $1.05, impacted by a one-time, non-cash income tax charge of $15.93 billion. Excluding the charge, EPS could have been $7.25, above analysts estimate of $6.72.

Family daily active people (DAP) rose 8% y/y to 3.54 billion, versus analysts estimate of 3.48 billion, ad impressions grew 14% y/y (Q2 2025: +11%), above analysts estimate of +10.8% while average price per ad increased 10% y/y (Q2 2025: +9%), in line with analysts estimate.

Meta is guiding Q4 2025 revenue in the range of $56-$59 billion, (analysts estimate: $57.2 billion), 2025 total expenses in the range of $116-118 billion (increased from $114-118 billion) and CapEx in the range of $70-72 billion (increased from $66-72 billion).

Meta expects 2026 y/y expense growth rate to be significantly higher than the 2025 expense growth rate driven by infrastructure costs and employee compensation.

It also expects 2026 capex growth rate to be notably larger than in 2025, pointing that their compute needs have continued to expand meaningfully, including versus their expectations in the last quarter.

Meta said their discussions with the EU Commission regarding the Less Personalized Ads offering is constructive but they cannot rule out further changes to their model that could lead to significant revenue headwind as early as this quarter.

Meta also flagged a number of youth-related trials in the US in 2026 that it say may result in material loss.

Assessment

Despite the higher than expected total costs and expenses, Meta Platforms delivered another strong quarter. However, shares fell 7% following the report, likely due to Q4 2025 guidance coming in below the overall analyst consensus. Given the highly bullish sentiment surrounding Meta ahead of earnings, such conservative guidance may have been perceived negatively by investors. The decline may also reflect concerns about rising capital expenditures coupled with negative sentiment related to U.S. youth-related legal cases.

Analysts downgrade Meta shares on rising capex and expenses

Outperform, $930->$875: Evercore said Meta is leveraging a strong position in the online ad market and AI advancements, making it a compelling investment. However, the increased spending for 2026 warrants close attention.

Details

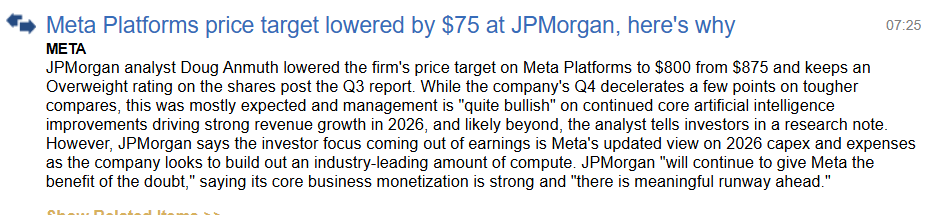

Overweight, $875->$800: JPMorgan said it will continue to give Meta the benefit of the doubt regarding capex and opex, saying core business monetization is strong and there is meaningful runway ahead.

Details

Outperform, $840->$810: RBC said the AI product narrative is largely unproven for many investors. However, AI’s impact on core growth is more durable and underappreciated, and that the incremental surface opportunities will start to monetize sooner than later.

Details

Buy, $900->$875: Truist said Meta continues to earn the right to invest as long as it delivers faster top line growth and free cash flow in the near term.

Details

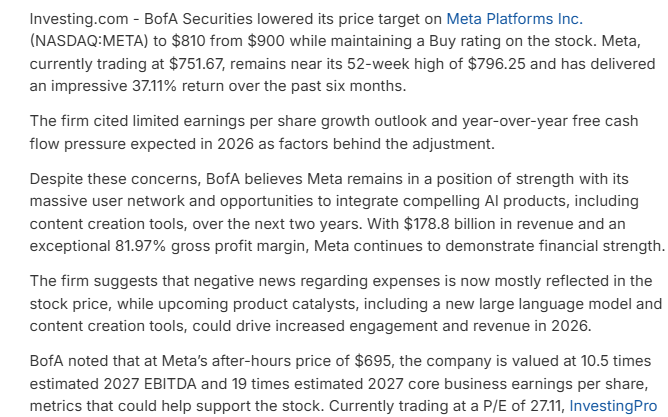

Buy, $900->$810: Bofa cited limited EPS growth outlook and free cash flow pressure in 2026. It pointed out that the negative news regarding expenses is now mostly reflected in the stock price.

Details

Outperform->Perform: Oppenheimer highlighted Meta’s substantial spending on “Superintelligence” saying the revenue opportunity is unknown, drawing parallels to Metaverse investment in 2021/2022. Oppenheimer also questioned the lack of rationale in Q4 guidance, pointing out that it’s a 600 basis point deceleration.

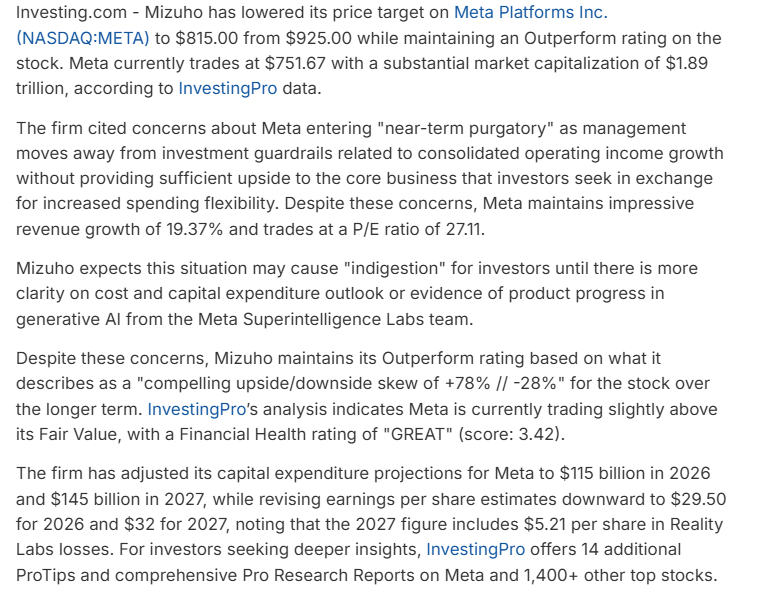

Outperform, $925->$815: Mizuho cited concerns about Meta entering “near-term purgatory” as management invest more heavily without guaranteeing that profits will keep rising. It raised Meta’s capex estimates to $115 billion in 2026 and $145 billion in 2027 but revised down EPS estimates to $29.50 for 2026 and $32 for 2027.

Details

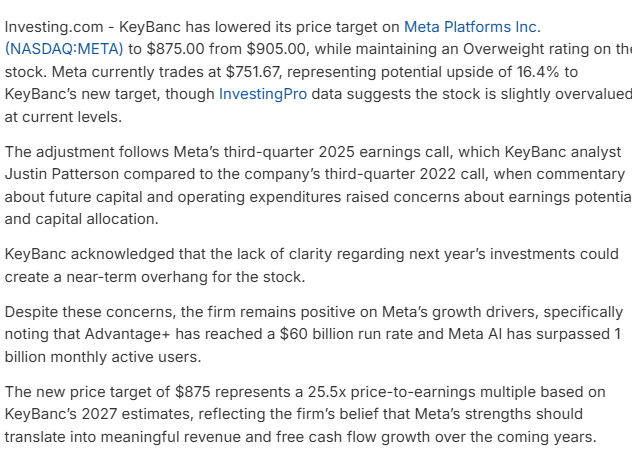

Overweight, $905->$875: KeyBanc analyst Justin Patterson compared yesterday’s Meta earnings call to Q3 2022 earnings call, when commentary about future capital and operating expenditures raised concerns about earnings potential and capital allocation. However, he remains positive on Meta’s growth drivers.

Details

Outperform, $820: Baird said the expense outlook might challenge investor confidence in the near term.

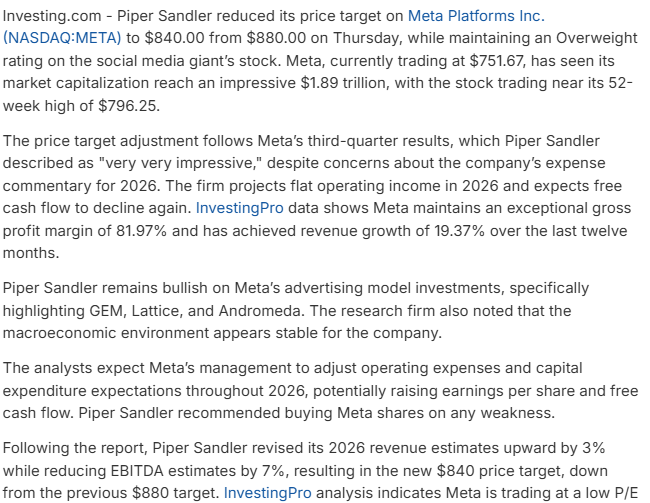

Overweight, $880->$840: Piper Sandler described third-quarter results as “very very impressive,” but flagged concerns on rising expense. Piper Sandler remains bullish on Meta’s advertising model investments.

Details