Given how large Metas reality lab losses are, i think we should put special emphasis on thinking about and modeling them. In 2023 Meta Platforms had losses of $6.13 per share in reality labs alone.

This hidden earnings power has always been an important part of the Meta thesis.

In their Q1 2024 quarterly report Meta projects increasing losses.

For Reality Labs, we continue to expect operating losses to increase meaningfully

year-over-year due to our ongoing product development efforts and our investments to further scale our ecosystem.

That said a recent report hints to significant cost cuts for reality labs hardware.

Assessment

If I had to guess I would think that Meta is indeed cutting back on VR costs as Apple’s Vision is failing to build significant traction and Apple is scale back it’s original goals.

That said I believe it is prudent for us to still model increasing reality labs losses as budgets likely shift to AI spent.

More detailed work on that front needs to be done by us in the future esp to understand which parts of AI costs are under reality labs and which under R&D.

In addition we should try to project capex which includes investments into AI infrastructure.

FX headwind during the quarter and potentially throughout 2025. Management is guiding for 3% in Q1 while I had projected around 6%.

Management guided for total expenses that’s around $5 billion higher than that expected by analysts. However, like in 2024, I don’t expect Meta to exceed the mid-point of its guidance ($114-$119 billion).

I expect growth in total expenses in 2026 to be lower than in 2025 due to continued efficiency gains and maturity of AI investments.

Cool, looks good.

I also believe expenses will grow slower in 2026 and beyond and think there might be even the possibility that they will shrink at one point. (As AI matures and gets cheaper)

If that happens that could lead to significantly higher EPS than currently projected.

At one point in this year we will also start to model free-cash flows given that capex and depreciations are becoming a larger factor and might deviate at one point strongly from each other.

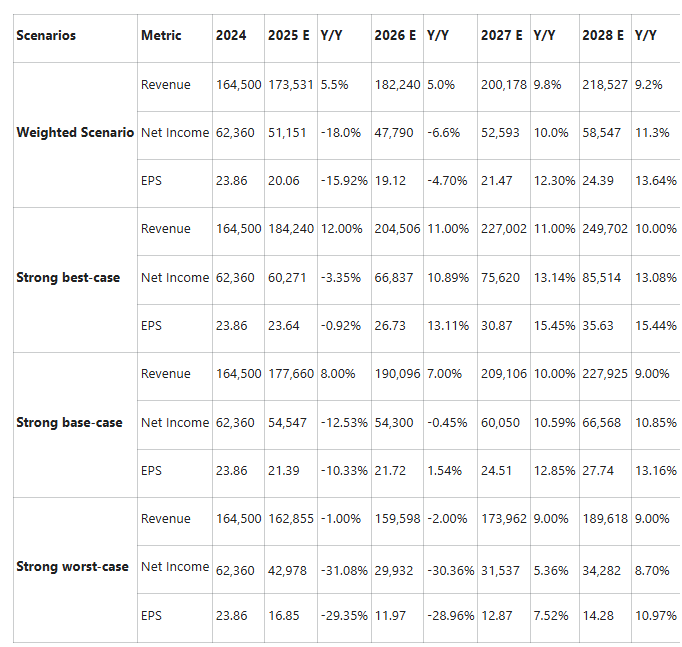

The above scenario model is based on the following assumptions:

Meta is somehow immune to economic slowdown, due to itsdominant position in performance-based advertising. Some analysts and advertising industry leaders have pointed out that during uncertain times, businesses tend to switch ad spend from brand marketing to digital advertising. This behavior was evident during the 2008–2009 recession, when US ad spending declined 18%, yet digital ad spend only fell 3.4%.

Mild revisions to the 2025 digital ad spending projection. Magna lowered their 2025 social media ad spend projections by only 0.8%. Similarly, MoffettNathanson reduced their 2025 estimate for online advertising spend by only 1.1%. These mild downgrades signal that Tariffs are not expected to be a major headwind to online advertising in 2025.

Only around 220,980 SMBs in U.S. are importers. This is only a tiny fraction of the over 8 million SMBs that advertise in Meta Platforms. However, even SMBs that don’t import are likely to be hit by the tariffs as well.

Consumers are unwilling to tolerate another wave of inflation, though their balance sheets remain healthy. As such, SMBs may be limited in how much of the tariff cost they can pass on to consumers.

The risk of a recession in 2025 is low. The tariffs will affect $1.4 trillion of imports, hence reducing GDP by 0.4-0.7%. However, my worst-case scenario gives recession a 35% probability.

The model assumes that Trump’s policies won’t affect the current corporate tax rate.

Recommendation

Based on the scenario-weighted analysis, Meta Platforms appears well-positioned to withstand potential turbulence from tariffs and broader macroeconomic uncertainty in 2025. I do not expect the share price to be significantly impacted by trade policy, as Meta’s performance-driven ad model provides meaningful downside protection. Instead, I believe investor sentiment will be more heavily influenced by the company’s execution in AI- particularly the commercial performance of Meta AI and its progress on agent-based solutions.

Recent developments raise concerns: early reports suggest that Meta’s business agents are underdelivering, and the resignation of Meta’s head of AI research this week adds uncertainty at a critical time. Unless Meta demonstrates meaningful progress on its AI roadmap in the coming quarters, particularly relative to peers, its valuation may face pressure independent of macro factors. Therefore, I wouldn’t recommend increasing the position until there is clarity on its AI performance.

Cool thank you. I think there are some good consideration made.

Your model assumes 12% y/y revenue growth in 2025 in the best case and -1% in the worst case. Why is this? Meta grew by almost 22% in 2024. Are there indications that growth will slow down significantly? If yes which are they?

I also spotted some minor things to improve:

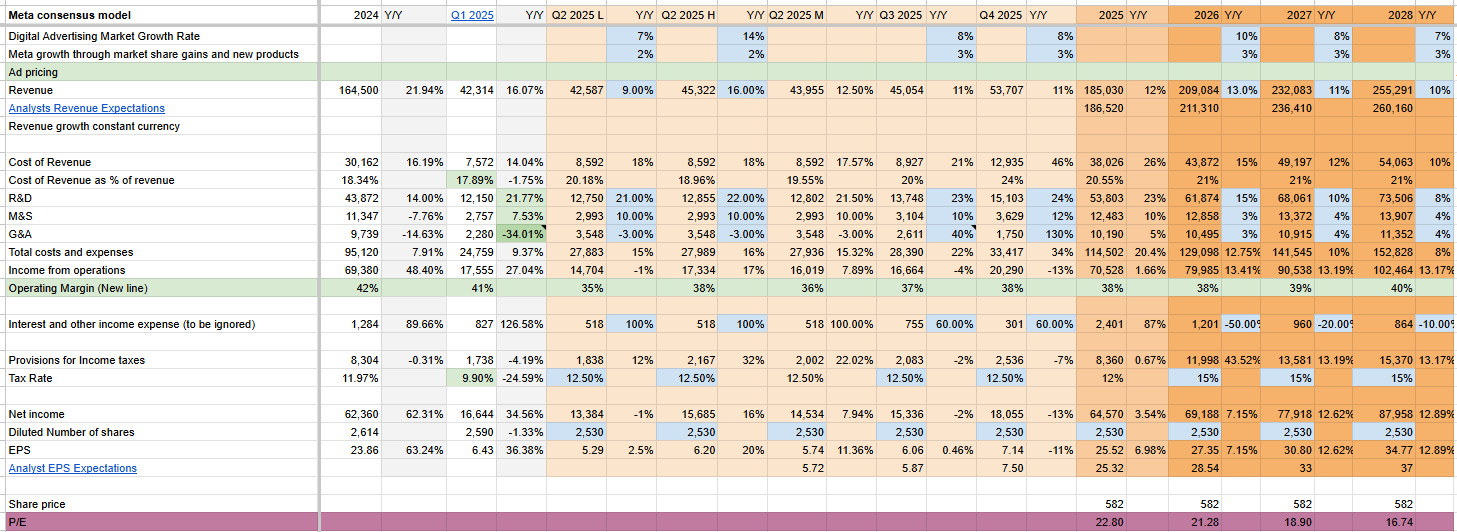

For example if I open the sheet on mobile I cannot instantly see which model is referring to which scenario (all are called “consensus model”) or I cannot see which model has which probability. (See picture below). I also noticed that the Notion page linked is not published (every Notion page we link to the forum has to be organized in the published format so everyone can follow along) and the net income of the bearish scenario of your picture above is not given.

I usually don’t like it to give feedback on smaller details like this and will try to avoid doing it in the future and think maybe you and Magaly can develop workflows to spot them yourselves to develop great final formats.

The strong deceleration in y/y revenue growth in 2025 is mainly due to lapping of a strong 2024. For instance, management is guiding Q1 2025 revenue to grow 8%-15%, a strong deceleration from the 27% growth in the same period last year. It cites lapping of strong period as a reason for this deceleration (page 2). Analysts are guiding 2025 revenue to grow 14.5% ( they haven’t incorporated the impact of tariffs in their estimates yet).

My worst case which projects -1% y/y growth in revenue assumes there will be a strong recession (15% probability). If there will be a mild recession (20% probability), I estimate that revenue will grow 2% y/y in 2025.

How do you determine those connections between recession and Metas revenue?

In the recent Magna release they reduce their social media growth rates as you highlighted only 0.8% from 11.5% to 10.7% and Magaly highlighted that many industries are resilient when it comes to ad spend. (Maybe Magna did not consider a recession though)

Did you do some research (e.g. using deep research etc.) that you could link why the impact on revenue could be so drastic?

I saw that you considered ad pricing which is good but I am also quite confident that Meta will also continue to gain marketshare at the same time.

When it comes to those models having the right assumptions, thoughts/ideas and research for them is key otherwise we run the risk of taking scenarios into account which might not be realistic at all.

Maybe in general it is also good if you list your confidence level on those scenarios, steps taken to develop them and further steps to do to increase transparency and give me or other readers more granular indications how much to rely on them. (We could also consider publishing & linking related tasks on Notion esp. if the steps there are clearly organized and categorized)

Magna did not consider a recession in its forecasts, they are only expecting a weak Q1 2025, but according to them most fundamentals remain healthy, so their outlook was overall still positive for the economy.

Ad spend has declined significantly in all recent recessions (much more than GDP fell), is a cyclical industry, and I would expect the same this time in a recession for the overall market. So, meta only slightly growing in a recession would still be better than the overall market due to market share gains.

I don’t think Meta will be immune completely to a recession though (because digital and meta are more mature now, and a bigger share of the overall market). But I also would still consider ~4-5% growth rate more appropriate for Meta in a mild recession.

I also think the strong recession probability is too high, because for me that would be a 2008 type of recession, which I don’t think is still very likely.

It’s good that Magaly has responded, given that she primarily worked on the impact of tariffs and other related topics. My role was mainly to review her research, draw conclusions, and incorporate them into the scenario model.

Yes, I asked GPT Deep Research about the possible impact and it pointed out that Meta could see a revenue decline if there will be a recession.

While I agree with you that Meta will continue taking market share from brand marketing platforms, I think you are not considering the fact that its current revenue is also under threat from the tariffs, since less than 16% of its revenue comes from the top 100 advertisers. Its ad pricing is also likely to come under pressure, given that Chinese advertisers have been cited as one of the primary drivers of pricing.

I agree with Magaly’s estimate on Meta’s growth during recession, but I thought it would be better to provide a margin of safety.

What do you mean by list my confidence level on those scenarios? I think the probabilities represent my confidence level.

I mean how exactly does the process of arriving at those revenue growth estimates work? Which kind of considerations go into it? How exactly do you arrive at final numbers?

With confidence I mean: Are you highly certain that revenue growth should be in the -1% til 12% range in 2025 based on all the research that you and Magaly did or do you regard your estimates as “wild guesses” at this point because you think it is plausible that it could be even higher or lower.

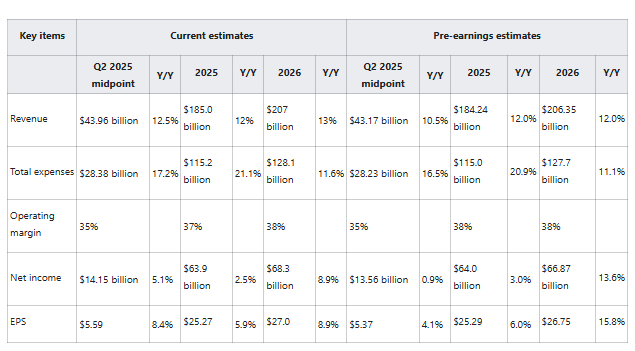

I have increased my Q2 2025 revenue estimate by approximately $1 billion, following Zuckerberg’s comments that Meta’s business is likely to remain resilient despite macro uncertainty. My new estimate now aligns with the midpoint of management’s revenue guidance. However, since Meta has historically exceeded the upper end of guidance, this still reflects a cautious stance on my part for Q2.

I have kept my full-year 2025 total expenses estimate largely unchanged at $115 billion, in line with the midpoint of Meta’s guidance range ($113–118 billion). Management’s decision to lower its Q2 OpEx guidance signals that spending may not reach the top end of the range. Notably, Meta’s OpEx came in $4 billion below the top end of its guidance in 2024, and $2 billion below in 2023, based on initial guidance from Q1 in both years.

I have also increased my 2026 revenue estimate by roughly $1 billion, primarily due to easier comps in 2025.

The projections are based on a scenario of macroeconomic softening without a recession, and they do not incorporate any potential effects from the DMA, which remains under evaluation.

I reflected about where to have valuation model discussions and think the valuation model topic is the right choice. (So people can follow along how those discussions evolve and learn from them) Therefore i moved your post here and posted it into the Q1 2025 topic for reference.

When it comes to valuation models I think overall i prefer to simply include a screenshot of our valuation model than creating those simplified overviews. This is easier for you and gives me more details faster on the individual line items.

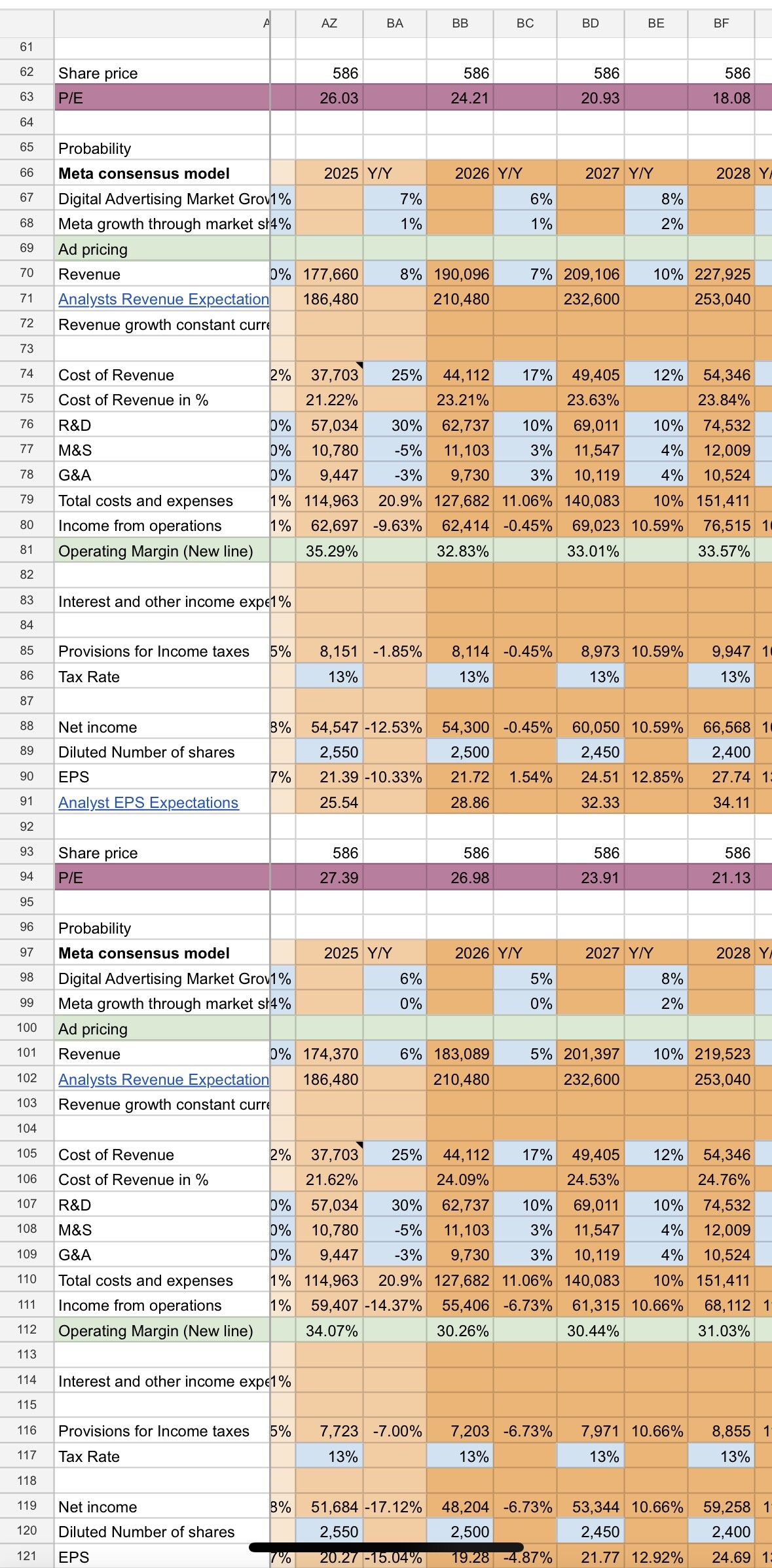

Reading your overview of numbers it struck me immediately as a bit strange seeing this huge drop in operating margin from 41% to 35% so i had a closer look into the individual quarters and think

G&A costs are more likely relatively evenly distributed through the year(?) There is no reason why they should be as low as >$1billion in Q4 2025 unless you predict strong special effects like in Q4 2024?

Growth in Cost of Revenue should rise a bit more gradually and not jump as drastically in Q4 2025 as depreciations from Capex/Ai Investments rise gradually? I think even in Q2 it might be already a bit higher than your projections. (We could have a closer look how they depreciate and try to make sense of it)

As a result of depreciations Cost of Revenue in general might be higher than projected by you in 2025 and in 2026 for sure. (It will likely be progressively more than 19% of revenue going forward) At the same time R&D cost might grow somewhat slower.

Do you agree with that? Overall it is absolutely crucial to model things correctly in our models so that i and others can rely on them when taking investment decisions.

If i had to guess i would assume to see an operating margin somewhat higher in Q2 2025 maybe at 38%.

I modeled Meta’s depreciation using the straight-line method. I also assessed how non-depreciation cost of revenue is developing. The model largely confirms my earlier estimates for Q2–Q4 2025 and full-year 2025 cost of revenue. For Q4 2025, I still expect depreciation to rise sharply, as CapEx in Q4 2024 increased significantly—by approximately $5 billion sequentially.

However, my cost of revenue estimates for 2026–2028 are now substantially higher, driven largely by depreciation costs. I should note that I do not have high confidence in my 2026–2028 CapEx assumptions, given management’s comment that compute needs remain dynamic. While I expect CapEx to decline after 2025, I still believe it will remain elevated, consistent with management’s tone and long-term infrastructure commitments.

On R&D, I agree with your assessment—I think it could grow in the mid-20% range in 2025, as observed in Q1 and decelerate sharply in 2026. As for G&A, I must admit I had not factored in the $1.55 billion special item in Q4 2024 (this supports your argument that valuation models should be updated immediately). Given the difficulty in forecasting G&A, I think it’s safer to assume there will be no similar special items in 2025.

Taking the above into account, I’ve updated my estimates as shown in the screenshot below. My operating margin estimate for Q2 2025 and 2025 are now 1% higher than my earlier estimate of 35% and 37%, respectively.

Modeling this like you are doing it certainly goes in the right direction.

That said there are still multiple mistakes like

Estimating depreciation as a % of the previous year capex does not make any sense as depreciation is based on the capex of the previous muliple years which is depreciated over the useful life of the assets. Therefore there will not be a super large depreciation jump as you model it in Q4.

Not considering any special effects i see no reason at all why G&A should be $3.5 billion in Q2 and $1.75 billion in Q4.

The assumptions of a continuous capex decrease are not realistic at all in my opinion given that we now live in a world of AI. 2025 might have been a local maximum but i think given managements comments and the importance of the technology i think 2026 could be at least at 2025 levels or even higher.

I did not look deeper into how you try to calculate the depreciation of different assets and unfortunately i do lack the time to give you feedback on those type of modelling and accounting questions.

Instead i would expect you to try building this capacity internally in our guidebook (soon to be published to the community) using AI and accounting courses to develop a strong knowledge system and then applying it in your analysis. (+ try to get feedback of ai or other sources if you do things correctly, what might be wrong, how to do certain things etc.)

Importantly i would expect you to use a lot of disclaimers in areas in which you are more uncertain to highlight to readers elements which you are less certain of to not create any false sort of security where there is none.

You could also try to interact with community members and get insights and feedback and see if there are knowledgeable people who could help.

The medium term goal would be that those models become so good that they are truly reliable. As long as they are not they offer unfortunately not a lot of value as they display a lot of misleading numbers, assumptions and accounting mistakes.