Majority of the weakness is expected to come from net exports, due to pull forward imports from consumers. However, consumer spending is also expected to be much more modest than Q4 2024.

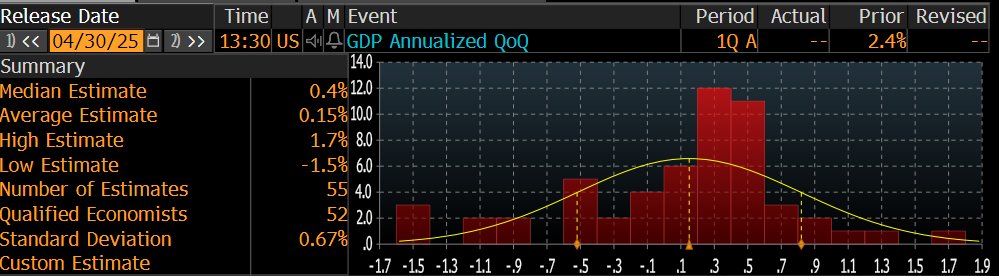

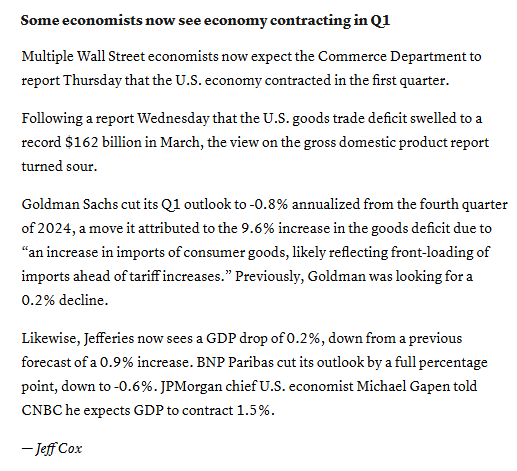

I think there is a high change (~50- 60%) that this could be a negative print of ~1% negative Q/Q SAAR, which could create a more a more negative market reaction, but not extremely negative since there are already some analyst expecting this to be the case also.

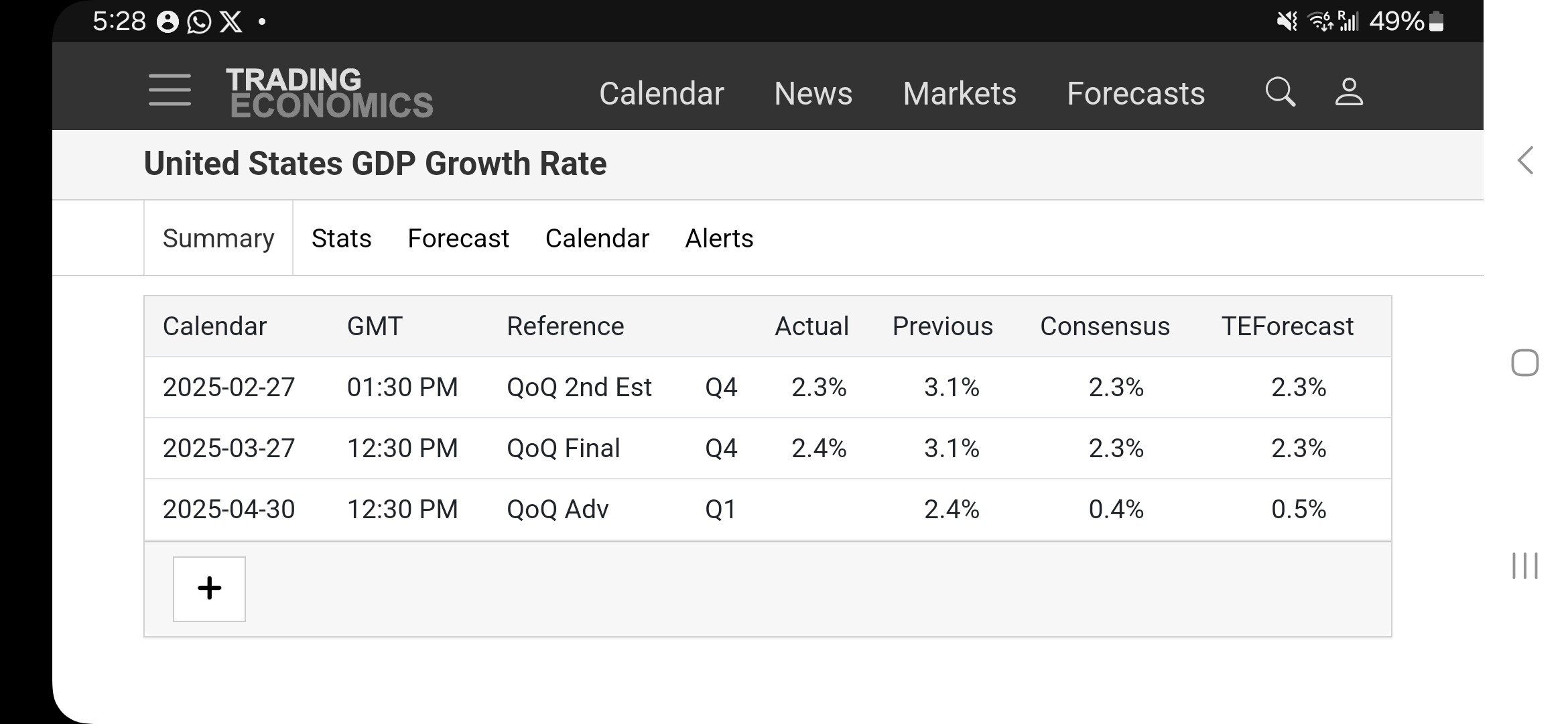

Some analyst expectations:

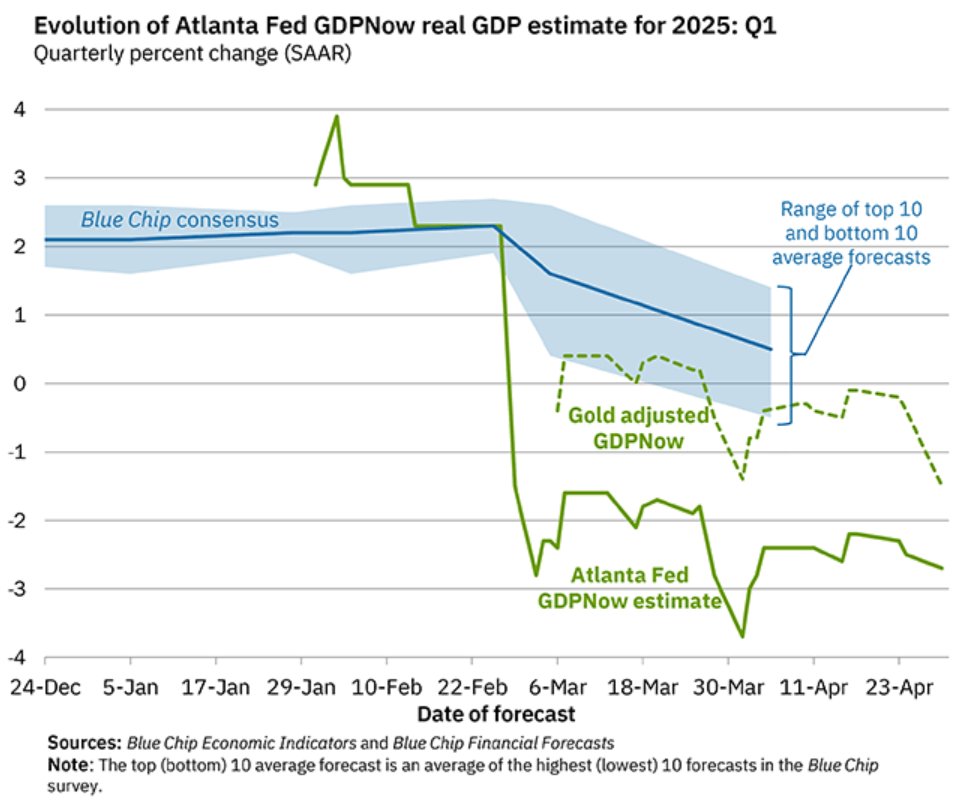

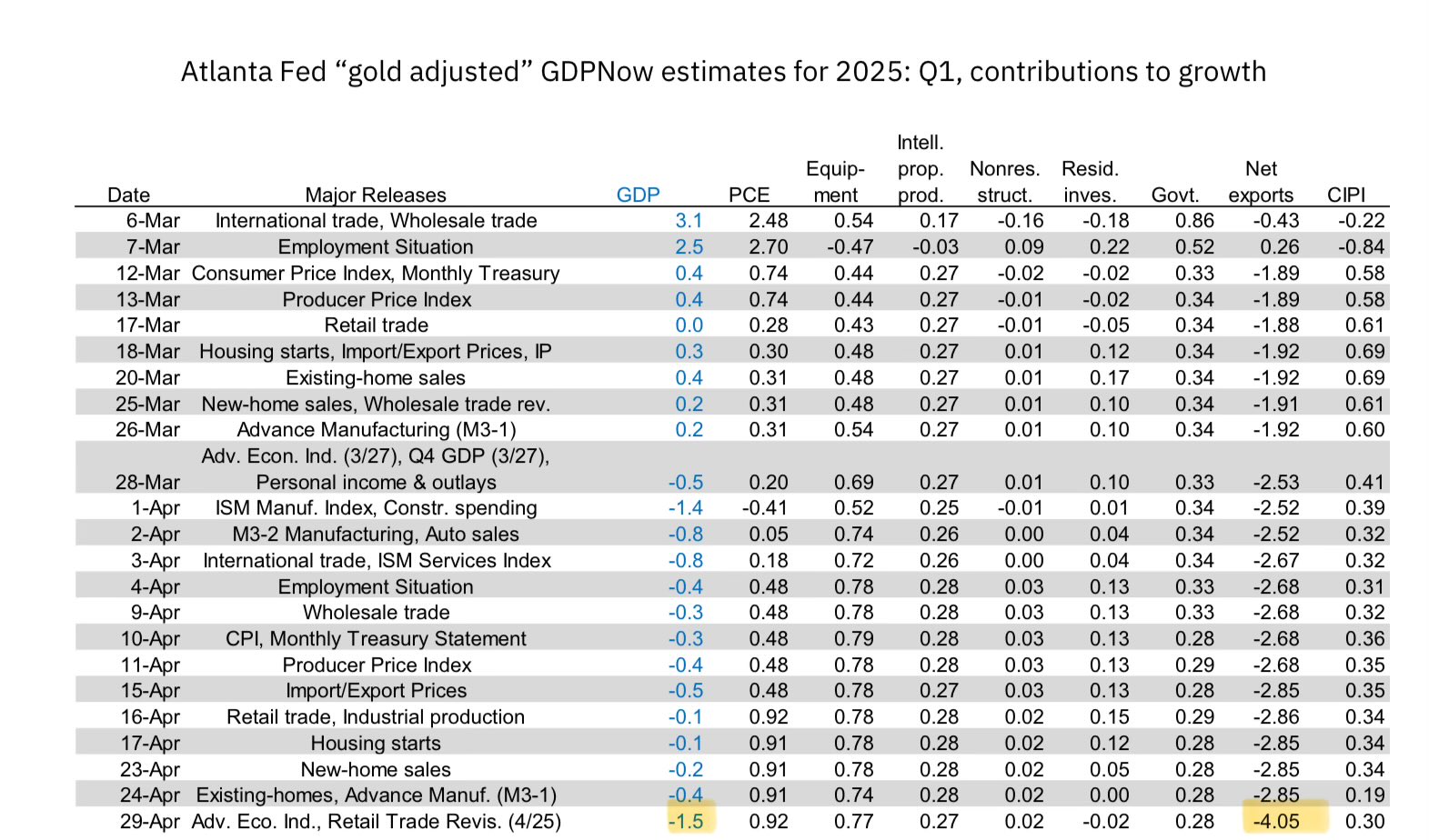

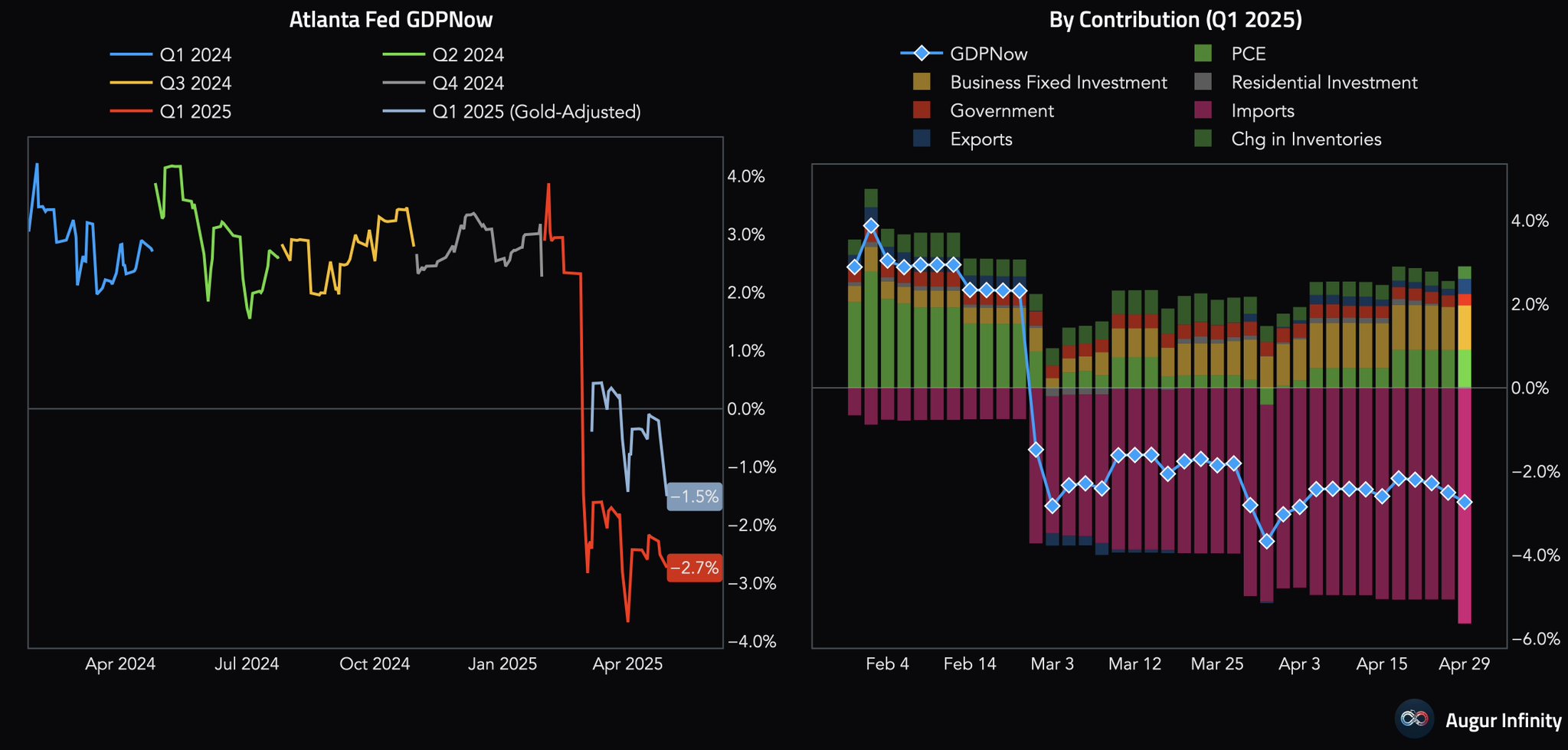

Atlanta FED is expecting a -1.5% Q/Q SAAR (adjusting for gold imports)

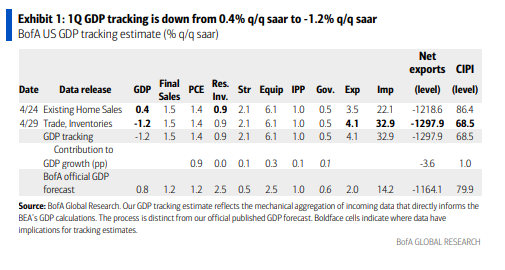

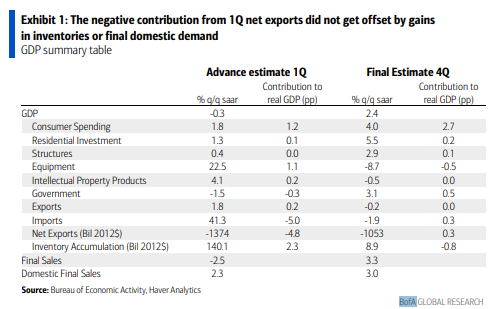

BoA is expecting a 1.2% Q/Q SAAR decline following the increased in trade deficits from yesterday, but says domestic sales stable at 1.5%.

More Details

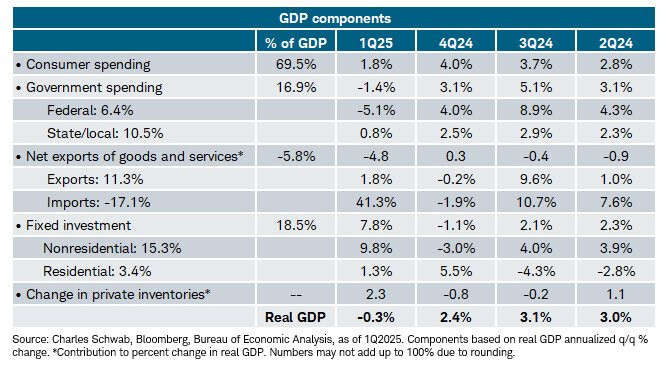

Also negative now is BoA whose 1Q GDP tracker falls a huge -1.6% to -1.2% Q/Q SAAR following the trade deficit. Unlike the Atlanta Fed, the model was also expecting a larger inventory build which also subtracted from the estimate (it was an addition for the Atlanta Fed).

That said, they reiterate, in line with the Week Ahead commentary this weekend, that increasing imports is not a sign of economic weakness. “[T]he trade deficit mechanically weighs on GDP tracking, imports are a net zero for GDP from an accounting perspective. They get subtracted out of net exports, but get added into one of the other components of GDP like inventories. But inventories are susceptible to measurement issues which is likely why we are tracking a low contribution from 1Q inventories. But this poses an upside risk to 2Q GDP (or 1Q GDP could get revised up) when inventories finally account for this import surge.”

“For now, despite the negative 1Q GDP print, we would recommend investors focus on indicators that reflect the underlying momentum in the economy, keeping aside the more volatile components like trade and inventories: Final domestic sales (GDP ex trade and inventories) is tracking at a stable 1.5%, in line with modest consumer spending in the quarter.”

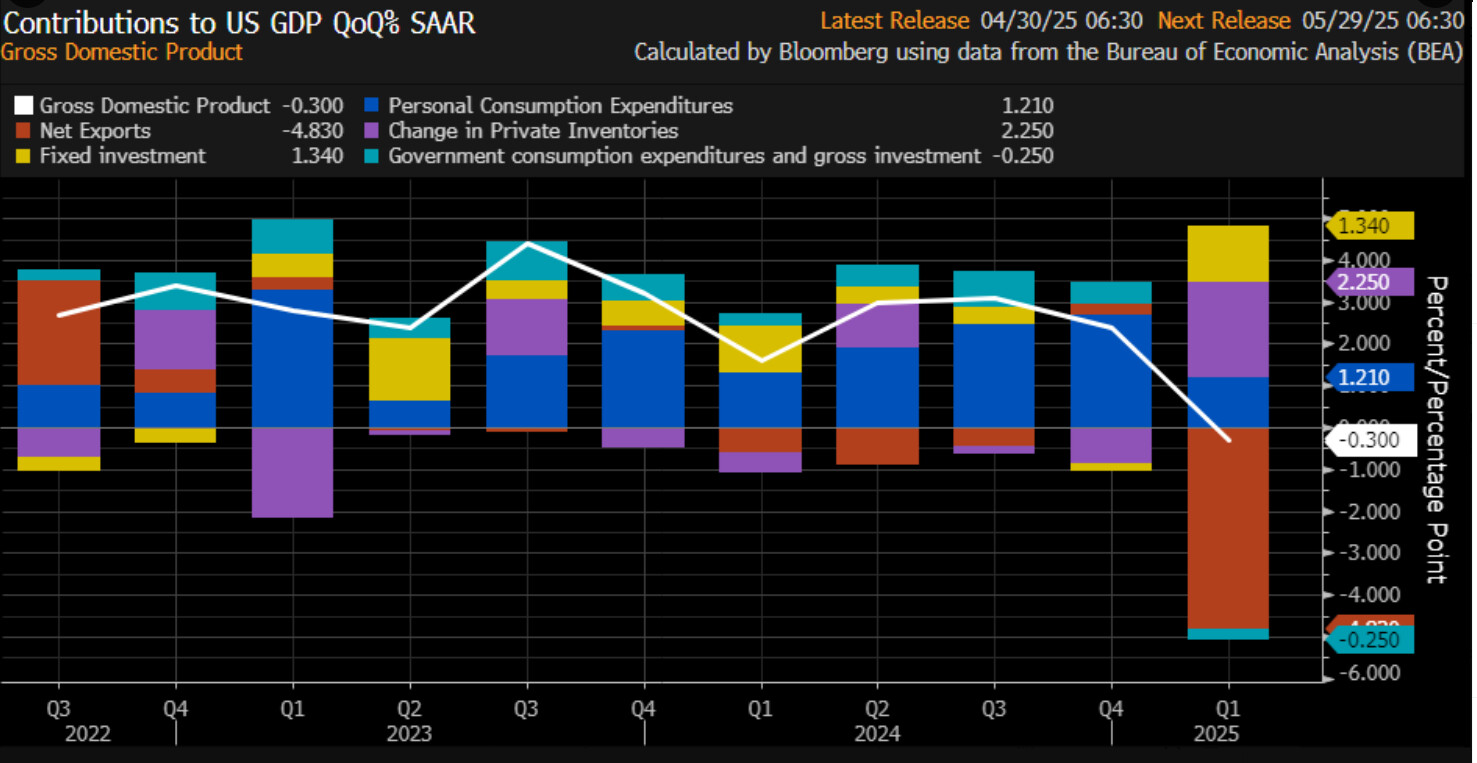

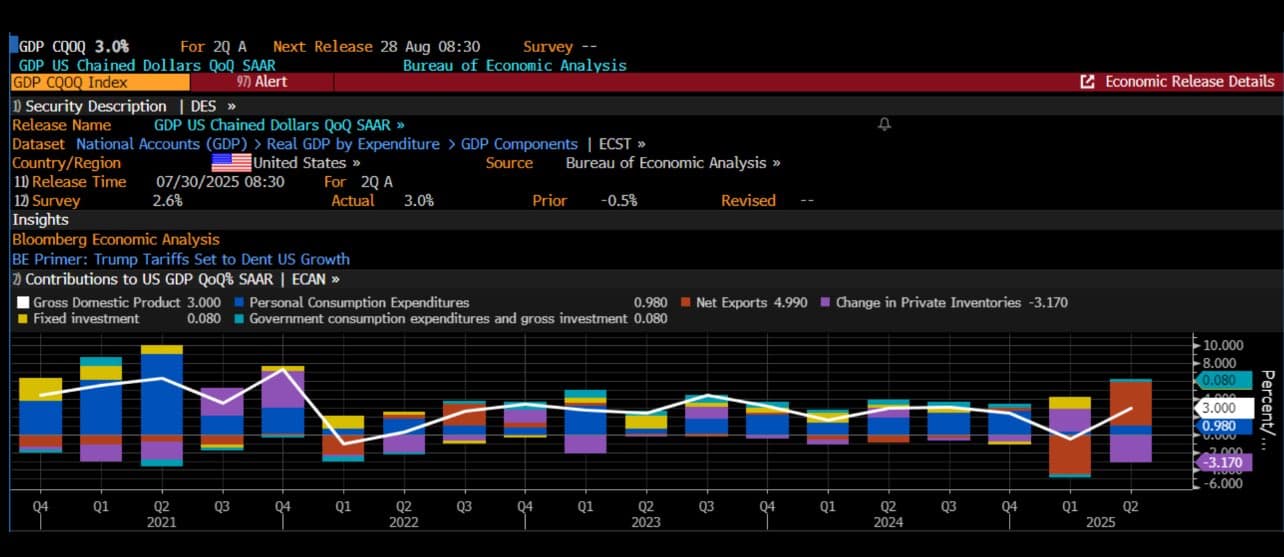

Despite the negative print, the economy continued to be solid in Q1 2025, with private domestic Final Purchases, or “Core GDP” (just consumption and business investment), rising by 3.0% Q/Q SAAR.

Underlying demand was resilient, but it was overwhelmed by one-off distortions from trade policy and fiscal retrenchment.

The decrease in government spending reflected a decrease in federal government spending -5.1% q/q SAAR (led by defense consumption expenditures -8% q/q SAAR)

The largest contributor to the increase in investment was private inventory investment, led by an increase in wholesale trade (notably, drugs and sundries)

Moderate consumer spending was mostly due to durable goods declining -3.4% SAAR (specifically motor vehicles and parts declining -3% q/q SAAR)

However, important to note this is for data up to March 31, 2025; the negative impact of tariffs, other than imports, will be reflected until later GDP reports, making this print not as important anymore.

Analyst Commentary about US economy as of May 5, 2025

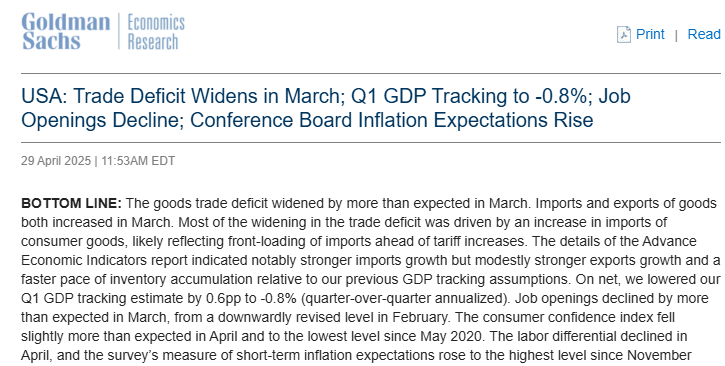

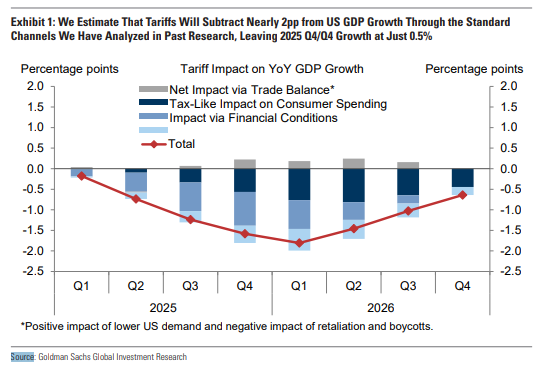

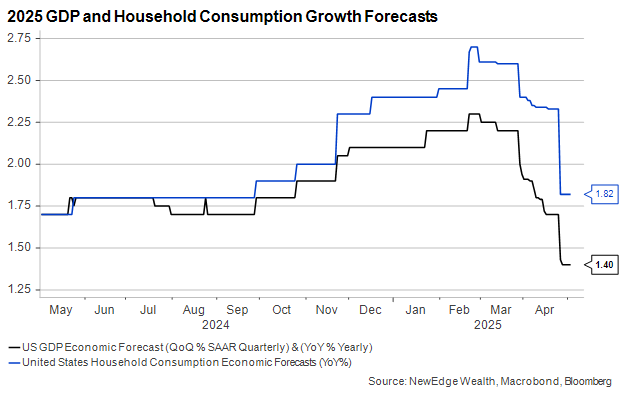

Goldman: soft GDP growth forecast of 0.5% for 2025 Q4/Q4 reflects a nearly 2pp hit from higher tariffs.

More Details

Our soft GDP growth forecast of 0.5% for 2025 Q4/Q4 reflects a nearly 2pp hit from higher tariffs. In past work, we have analyzed the effects of tariffs through standard channels—tariffs function like a tax hike, tighten financial conditions, and increase uncertainty for businesses, though they will likely also reduce the trade deficit somewhat.

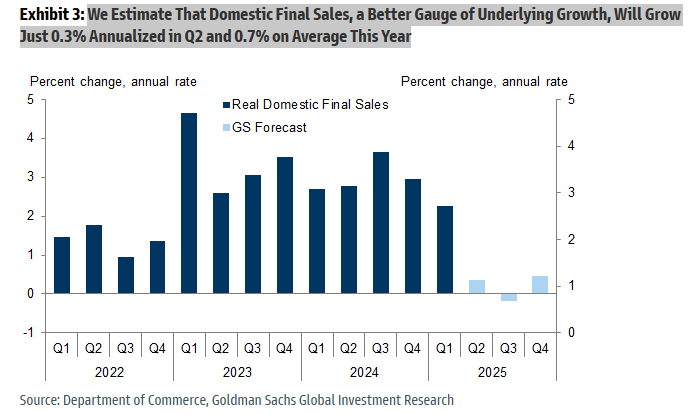

Goldman Sachs also estimates that Domestic Final Sales, a Better Gauge of Underlying Growth, Will Grow Just 0.3% Annualized in Q2 and 0.7% on Average This Year

BoA thinks Q1 is likely to see upward revisions since 1Q imports were most likely not properly accounted for in the other GDP components

More Details

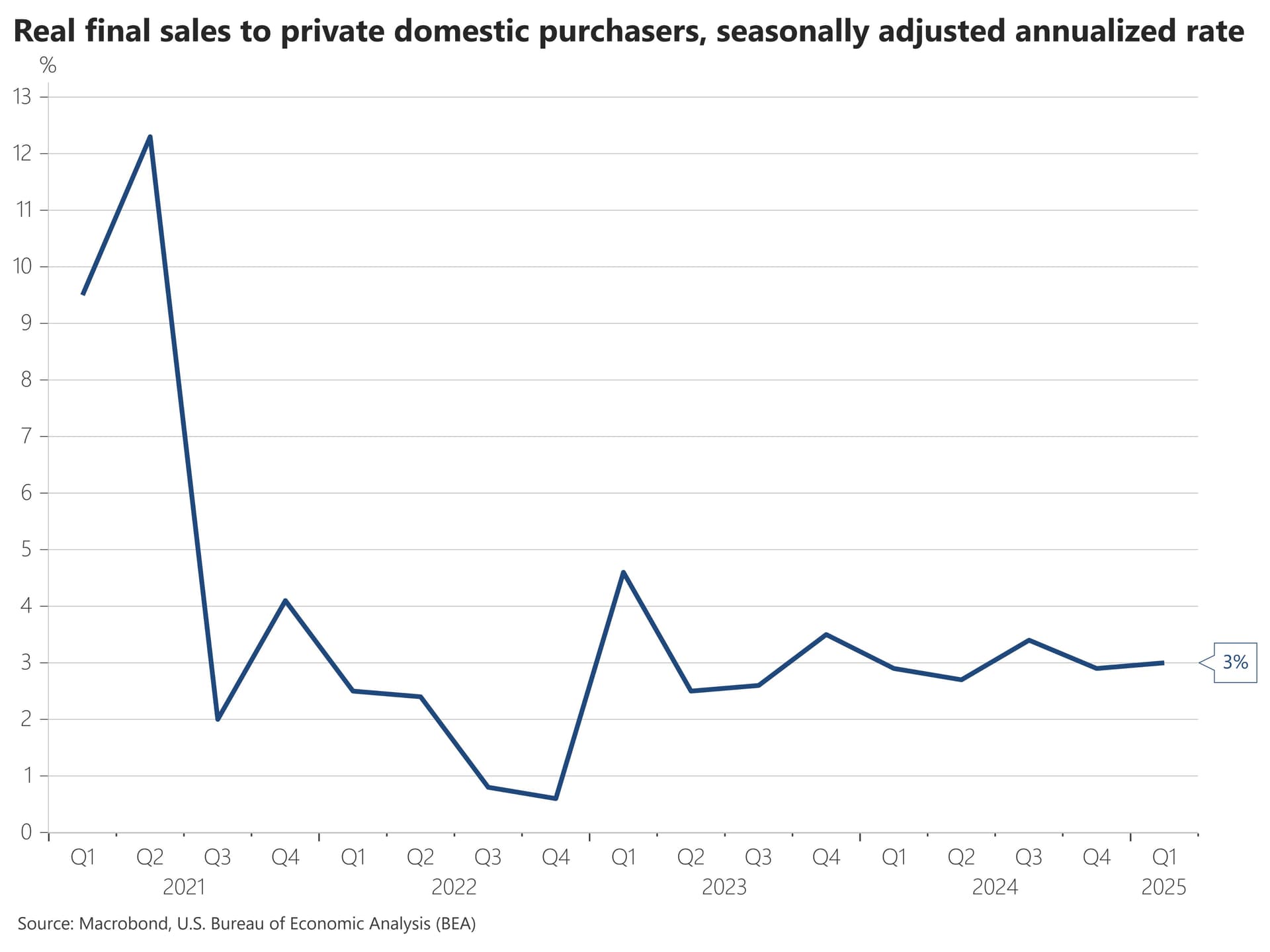

Our takeaway is that 1Q imports were most likely not properly accounted for in the other GDP components. This poses upside risks to 2Q GDP (or 1Q revisions). Investors should focus on final domestic demand (GDP ex trade and inventories), which landed at a decent 2.3% q/q saar, to gauge the underlying health of the economy. Unfortunately, as front-loading ends, final demand is likely to slow sharply in 2Q.