I was only able to obtain numbers up to 2022. While it’s possible to calculate adjusted EBT for 2021 and beyond using the methodology they gave at the end of 2023, methodology inputs for such years are not given.

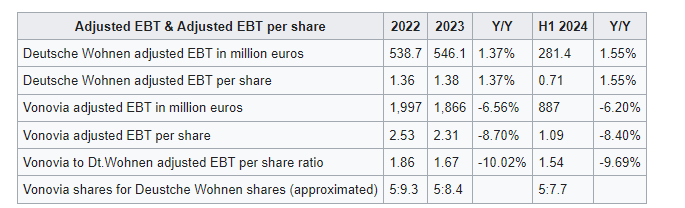

While Deutsche Wohnen’s adjusted EBT has been growing modestly, that of Vonovia has seen a notable decline. Also, unlike for Vonovia, there hasn’t been dilution of adjusted EBT for Deutsche Wohnen.

Can there even be a squeeze out if there is a Joint Venture that controls 20%? Can the JV and Vonovia both vote for a squeeze out of remaining shareholders if they control 95% together or can a squeeze out only happen if one single company controls 95%?

Can there be a squeeze out of shareholders in the 95% scenario and the company (Deutsche Wohnen) keeps existing so that the JV setup works?

Can you add a line in the table which shows the ratio of adjusted EBT per share between Dt. Wohnen and Vonovia so that possible exchange ratios become visible and give a very rough indication for some years before? What is your assessment? Do you think the substantially higher adjusted EBT of Vonovia in the last couple of yours is concerning?

Interesting questions. According to section 327a of the German Stock Corporation Act (AktG), only a single entity can initiate a squeeze-out. Additionally, section 327e of the act stipulates that all shares owned by minority shareholders will have to be transferred to the bidder. That means the only way Vonovia can squeeze-out the minority shareholders (other than the JV) is by transferring its stake in Dt. Wohnen to the JV (which is itself an entity) and asking it to act on its behalf.

I think the past adjusted EBTs for the two companies will be considered. However, the fact that Dt. Wohnen’s adjusted EBT has been stable while that of Vonovia has been declining will be an advantage to Dt. Wohnen. For instance, Dt. Wohnen’s minority shareholders may argue that there is a high possibility for future Vonovia earnings to decline. That means future exchange ratio (vonovia shares for Dt.Wohnen shares) will decline. Discounting that will result in a lower exchange ratio today.

I have edited the post above to include the ratio adjusted EBT per share between Dt. Wohnen and Vonovia.

Ok, this should mean a squeeze-out can be ruled out because I think its unlikely that Vonovia will sell more than half of its Dt. Wohnen stake to the investors in the JV.

A judge using trends to determine the fair value is an interesting thought but I think we would need to have a better understanding of Vonovias business to reach a qualified conclusion. As an example it is a possibility that part of Vonovias business had only some temporary weakness and could recover. For example I think the development business was affected by problems in the Germany real estate market in the last couple of years but its outlook might be positive and not negative right now.

If you had a Dt. Wohnen investment or Dt. Wohnen was under your responsibility, would you reduce the position or not? What are your key arguments?

I won’t rule out a squeeze-out yet since Vonovia can transfer its stake in Dt. Wohnen to the JV without necessarily selling it to Apollo as long as the JV by-laws allow it.

Vonovia’s adjusted EBT has been declining while that of Dt. Wohnen has been modestly growing because of the following:

Vonovia has a higher exposure to high interest rate environment compared to Dt. Wohnen due to its higher debt (Vonovia’s net debt in H1 2024 was seven times that of Dt. Wohnen). This leads to a higher financing expenses for Vonovia. For instance, in H1 2024, Dt. Wohnen’s net interest expense fell 6% to 76.4 million euros (page 35 of H1 2024 report) while that of Vonovia increased 10% to 424.5 million euros (page 28 of H1 2024 report).

Vonovia’s portfolio is more diversified while that of Dt. Wohnen is more focused on rentals. In 2023, Vonovia’s rental income accounted for 63% of total revenue while that of Deutsche Wohnen accounted for 80% of total revenue. Rental income has been more stable than other businesses, hence Vonovia’s earnings has been more volatile.

Vonovia has been incurring expenses associated with the integration of Dt. Wohnen.

My estimate is an offer price of between 25 and 28 euros (26.5 euros at the midpoint). Given that Deutsche Wohnen is currently trading at around 25 euros, I think I would reduce the position. My main reason for reducing is the lack of sufficient visibility on Dt.Wohnen’s fair value. Even at current conditions, it will take some years before Vonovia to Dt.Wohnen adjusted EBT per share ratio is equal to one (currently: 1.54). Given that some of the above conditions such as interest expenses and integration costs are likely to come down in the next one or two years, the possibility of arriving at an exchange ratio of 1:1 in the short-term based on this metric is low. Additionally, the 26.5€ is a premium of 17% over the closing price of 22.60€ on September 18 when the DPLTA was initiated.

Hmm. Can you describe in more detail how this would work? In the JV Vonovia owns only 51%. How could it transfer its Dt. Wohnen stake to it without selling to JV investors and keep full ownership of the part that it is transferring?

Are there any examples or precedents of something similar to what you describe happening esp. in combination with a squeeze out?

Based on which calculations do you believe that the adjusted EBT of both companies could reach 1:1?

What about earlier arguments like that JV investors likely paid EUR 25.5/26 a share and Vonovia might need to offer at least the same?

What are the different scenarios that you think could happen (including their price per share), how do you estimate their probabilities and what is the average probability weighted price per share based on those scenarios?

By how much would you reduce the position?

I meant that if the JV by-laws could be changed allowing Vonovia to be the majority shareholder, then it’s possible for Vonovia to transfer its remaining 66.84% direct stake in Dt.Wohnen to JV without selling to Apollo. Vonovia will then own 76.56% stake in Dt.Wohnen indirectly (via the JV) while Apollo will have 10.11%. Additionally, Vonovia will have 88% stake in the JV while Apollo will have 12%. The JV will only need to acquire 9% of the shares held by Dt. Wohnen minority shareholders to initiate the squeeze-out of the remaining shareholders. An example of a JV that initiated squeeze-out in the past is Daimler-Rolls-Royce JV. In 2011, Daimler and Rolls-Royce announced that they will form a JV that will acquire 100% of the share capital of Tognum AG. Daimler had 28% stake in Tognum by then. In 2012, the JV squeezed-out the minority shareholders of Tognum.

I have considered various scenarios such as the price paid by Apollo, trajectory of adjusted EBT per share, possibility of using NAV as a valuation method, and synergies that comes with full control of Dt. Wohnen. I arrived at a weighted exchange ratio of 1.24 or an offer price of 25.67€.

Given the offer price estimate, I think I would reduce the position by around 50%.

Thank you for the insights. If you are correct with your scenarios I would not sell shares because the worst of the scenarios that you painted is an offer price of €21.45 which limits the downside risk significantly.

Are you confident that there will not be any worse scenarios? Like for example a worse exchange ratio based on EBT? Could we rule out for example that Vonovia wants to take the average EBT of the last 3 or 5 years? Going back into 2023 and 2022 Vonovias adj. EBT was considerably higher than it is now and therefore the exchange ratio based on EBT would be worse than in any of your current scenarios.

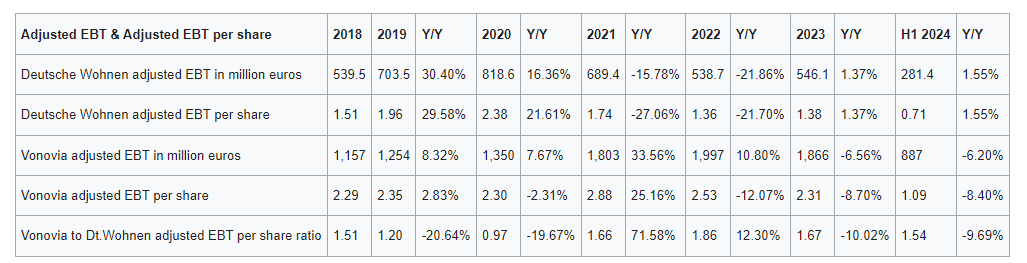

As said before, I think I would also need an indication of adj. EBT for 2021, 2020, 2019 just to get an impression if the situation back then was even more in favor of Vonovia but it doesn’t need to be super precise.

What about the scenario that the DPLTA and offer to exchange shares will be canceled? Do you think there remains a slim chance or can it be ruled out completely?

I also read this post and the Wiki article again. Where does it say that the TLG transaction was based on income? (Just reading through the Wiki it appears it orientates heavily on share price) Interestingly enough WCM shareholders got a better offer than expected based on their NAV.

I have estimated Vonovia’s adjusted EBT from 2021 to 2018. Dt. Wohnen’s adjusted EBT for 2021 to 2018 is given by the company. As you can see from the table below, adjusted EBT ratio was declining rapidly prior to the takeover by Vonovia. After the takeover, there was an uptick in the ratio partly due to integration of Dt. Wohnen’s earnings. For instance, in 2021, Vonovia’s adjusted EBITDA total rose 18% to 2.3 billion euros. Excluding adjusted EBITDA contribution by Dt. Wohnen, its adjusted EBITDA total could have grown by 9.9%. That said, I think basing the exchange ratio on past EBT performance will not be realistic since integration with Vonovia is one of the reasons behind the lower Dt. Wohnen’s adjusted EBT. Nevertheless, the discounted valuation model mainly looks at the future. The past is only used as a base for projecting future earnings. Given that Dt. Wohnen will probably have lower beta (risk) due to its lower debt and less-volatile portfolio, I am confident that a worst case scenario due to lower EBT in the past is low.

I think I will rule out the possibility that the DPLTA will be canceled since it’s a requirement if Vonovia wants to have total control of Vonovia. Also, Vonovia’s debt is still large and having total control over Dt. Wohnen’s assets will be very advantageous.

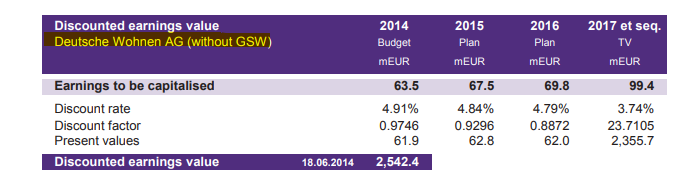

In the TLG DPLTA, an exchange ratio of 1:5.75 was used. The share price exchange ratio was 1:5:55. Alternatively, SdK, one of the minority shareholders claimed that a beta of 0.375 was used to compute the offer price. These proves that fair value of the two companies were used and not the weighted average share price in the past three months.

Thank you for the calculations. How confident are you that those calculations are correct or come close to reality?

I saw that you used the same calculations with more recent numbers. Have you been able to verify that your methodology is correct doing so? (calculated & actual numbers after 2021 matching)

(Note: I could have checked those things myself in the numbers but it will always be easier for me if you provide an indication about your confidence or some additional insights so I don’t have to verify/check things)

Why do you think the Dt. Wohnen contribution was only 8% y/y growth in 2021? Did they state this somewhere in the report?

I think Dt. Wohnens EBT dropped after 2021 because they have been selling property. This shows that using fair value based on income or discounted cash flows is a bad methodology as it is completely disregarding the debt situation. A company could simply buy more property and leverage themselves to reach a higher EBT.

Given how close average weighted share price and offer price have been in the TLG case I think the average weighted share price heavily influenced the offer price?

Overall my current take is that we only have a very small sample size of DPLTA/merger cases to draw definite conclusions from. NAV was considered in the Dt. Wohnen/GSW case and was the only factor in the Dt. Wohnen + Vonovia merger and to heavily lean on EBT would not make sense because it disregards debt as described above.

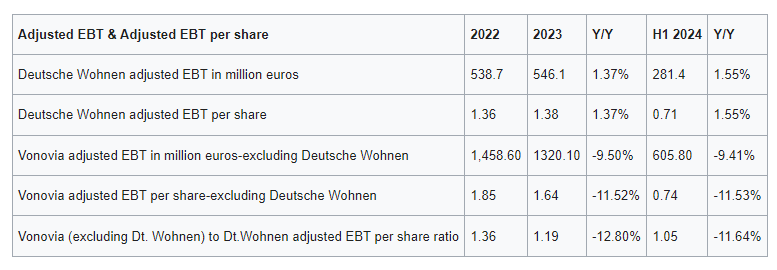

In addition even a comparison based on EBT might look good for Dt. Wohnen if we deconsolidate Dt. Wohnen from Vonovias numbers? (This is something we would need to calculate)

I am looking for more arguments from your side but I think based on our findings we could even consider to increase the position because I see a clear upside scenario but no clear downside scenario?

My confidence level on the calculations for adjusted EBT from 2021 to 2018 is around 80%. The methodology used has been provided by the company. The inputs for 2022 to H1 2024 are also given in the financial reports. I only estimated the inputs for 2021 to 2018. Therefore, adjusted EBT for 2022 to H1 2024 are actuals while that of 2021 to 2018 are estimates.

Yes Vonovia said in its 2021 report that Dt. Wohnen adjusted EBITDA total contribution was 170.8 million euros. The contribution was small because integration occurred in Q4 2021.

When I exclude Dt. Wohnen from Vonovia’s adjusted EBT per share, I arrive at an exchange ratio of close to 1:1 at the end of June 2024.

I think the DCF model doesn’t ignore debt completely. The fact that Vonovia has high debt presents a risk which is captured by beta.

I looked at two other Vonovia takeovers and in both cases, the offer price carried a premium over the target’s previous close.

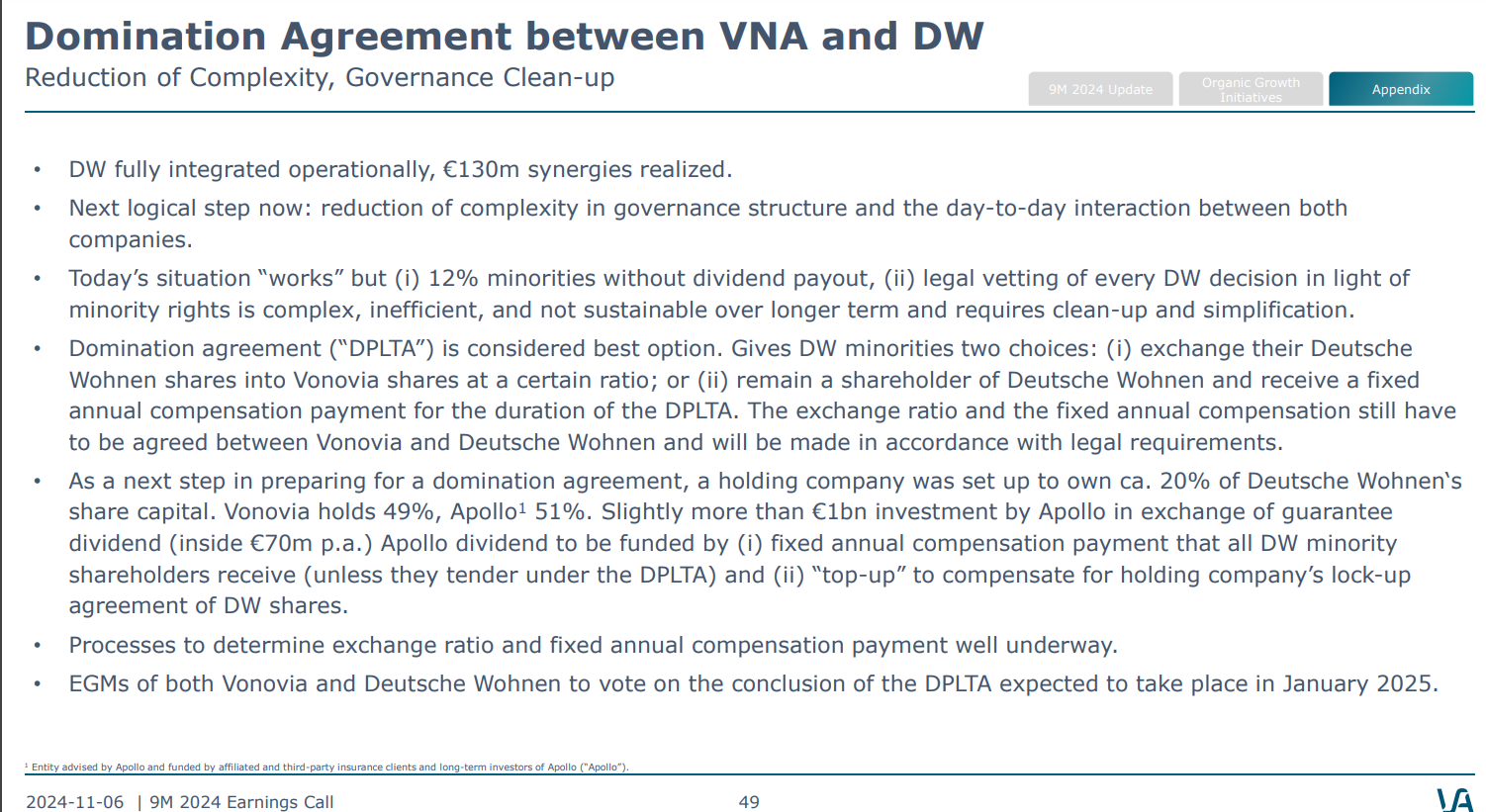

Another reason why I think Vonovia is unlikely to cancel the DPLTA is because they term the formation of the JV as a “next step towards domination agreement.” They said that the shares held by the JV will be subject to a lock-up agreement and be entitled to an annual compensation (like any other minority shareholders). Vonovia pointed out that the annual compensation impact on its operating cash flow will be around 70 million euros.

I think buying more brings some risk while holding it presents less risk.

Yes I fully understood the differentiation. I did not get the part that you already had the methodology but I thought you derived the methodology and then tested if it was correct by applying it to the years after 2022 to see if calculated results with the derived methodology would match actual numbers.

How certain are you that we can completely deconsolidate Dt. Wohnens numbers to arrive at Vonovia adj. EBT ex Dt. Wohnen and our methodology overall is correct? Has this be done also in other DPLTA cases in which one company already consolidated the numbers of the other company when DCF was used?

I assume that if we adjust our scenarios based on our new findings, the average weighted price and your recommendations would be significantly better?

The document that you found regarding the JV is very interesting. In the future we always have to search directly on the investor relation websites of both companies when significant news are announced to see if they publish any more details.

It basically confirms the whispers and therefore a share price of EUR 25/26.0 in the transaction and tells us that the investors are insurance companies and other Appolo Investors (not only current investors who swapped their stake) and most importantly it gives us an indication how high the annual fixed compensation offer will be.

I found the exact statement regarding it a bit tricky to interpret and also attached it below. My take is that “minorities” does only refer to external shareholders and not the 49% of the JV that is owned by Vonovia and ChatGPT seems to confirm this.

This means the up to 70m will go to the 10.2% Apollo investors and any investors that refuse to exchange their shares for Vonovia shares. Let’s say if 5% do not tender their shares, 70m will go to 10.2%+5%=15.2% of the share capital. Considering a valuation of the Apollo shares of “a bit more than 1billion” we can assume that the value of the total shares of external shareholders is around 1.5billion. This would mean that the compensation yield for the shareholders would be 70m/1500m=4.66%.

Broadly speaking I think we can say that the yield offered to shareholders will be between 4% and 5% given that neither we nor Vonovia current knows how many shareholders will not tender their shares and we don’t know with which scenario Vonovia is calculating in their press release.

What is your take? Can you maybe write a short mail to Vonovia investor relations to get a definitive answer if the 49% in the JV held by Vonovia would be included in the minority line item or if this line item is only considering external shareholders?

Which risks do you see from here? I am still heavily considering to increase the position esp. if it will be clear that the compensation offer will be at least 4% based on current prices and Vonovia could not opt for a very low compensation offer + our confidence is increasing that the share exchange offer will be good. On the other side if you believe that after concluding our analysis of the share exchange price and potential clarification from Vonovia that there are risks that I might underestimate or you strongly feel I should be more careful I would be very interested in any arguments (actually for both sides also the bull case) that could help me to take a better decision.

I was able to establish with certainty that the €70m annual compensation will only go to Apollo and is based on its stake in the JV. That is an annual yield of around 6.67% assuming the “a bit more than 1 billion” valuation of Apollo stake.

Since the yield is related to the stake in the JV and not the DPLTA, we cannot confidently tell if Deutsche Wohnen minority shareholders will receive a similar compensation.

I found some interesting comments regarding the offer price:

Sdk, a shareholder advocate wants NAV to be used in calculating the offer price.

“In our view, the compensation offer should be based on the NAV, as this value should be realizable relatively quickly,” said Bauer.

Vonovia CEO Rolf Buch wants the weighted average share price to be used.

“We are aiming to base our valuation primarily on the weighted average price of Deutsche Wohnen shares in relation to Vonovia shares,” he told Handelsblatt. “The last time a similar decision was made was at the beginning of 2024 in a similar case between Vodafone and Kabel Deutschland, which has once again expressly confirmed such an approach,” he added.

According to Sdk boss Bauer, activist investor Elliot is unlikely to drive up the offer price any more.

“He is unlikely to drive up the compensation price any further, as this will be determined by Vonovia based on the valuation reports to be prepared by the auditors,” said Bauer.

Yes, I am 100% confident that Dt. Wohnen’s earnings will be deconsolidated from that of Vonovia during valuation. This was the case in the Dt. Wohnen-GSW DPLTA (page 67-88).

Assessment

The fact that GSW earnings were deconsolidated from Dt. Wohnen’s earnings during the DPLTA is a game-changer in my estimates. Though Buch wants the weighted average share to be used, that won’t matter since the German corporate act stipulates that the highest between weighted average share price and fair value should be used to calculate the offer price. Taking these new information into account, my new offer price estimate stands at €27.67. The annual compensation is also likely to be attractive (maybe 4% to 5%) considering the around 6.7% that was offered to Apollo. As such, it might actually makes sense to buy more.

I increased my position by 20% today at a price of EUR 24.70, given that I believe that the odds for a favorable offer - higher than the current price - are high. (80%+)

In addition, I believe that the upside is significantly higher (up to +30%) than the downside (likely not less than -15%)

I also agree with Aron that it is basically certain that there will be an agreement, given that Vonovia already set up the JV and sold 10% of its stake in preparation. I also believe that it is unlikely that the offer is too low because it is in Vonovias interest to resolve the matter in order to improve it’s financing situation. (I think Rolf Buchs recent comments could have been made to increase Vonovias negotiation position)

Considering that the conclusion of the agreement will already be voted on in December an announcement of the conditions could be imminent or could happen within the next month.

This would lead to a very good annualized return of investment if the share exchange price is indeed favorable compared to the current price.

My main arguments why I believe that the price should be higher are

Dt. Wohnens NAV per share is slightly higher than that of Vonovias

Dt. Wohnens adj. EBT per share is almost on par with Vonovias

Terms of the Apollo JV sale are favorable both on a shareprice and compensation level. (The share price is at least a bit higher than current prices, and I think that investors in the JV might have gotten a discounted share price compared to what Vonovia will offer minority shareholders.)

Especially the first two arguments should weigh heavily as they are undeniable truths and need to be considered and prioritized by law.

Why didn’t I increase the position more?

After the price increase in Dt. Wohnen stock and todays increase of 20%, my holding is already almost on par with my second largest investment, Volkswagen and therefore larger than 10% of my portfolio.

Additionally, I don’t have extensive experience with those kinds of situations, as can be seen by our research. While I believe a positive offer is likely, I could be wrong. There is also always the possibility that we did not consider important aspects or made mistakes in our calculations. (therefore it is always great if everyone checks and challenges our research to help improve it) Some of our assumptions might also be wrong. For example, Vonovia could make a low first “negotiation offer” even if it knows that this will likely be challenged in court.

Lastly the stock exchange offer is only as good as Vonovias stock price. While the period until the terms of an agreement will be announced should not be large there is a risk that Vonovias stock could fall in this period and this risk will be persistent in case Vonovias offer will not be good and need to be challenged in court.

As always, I will keep evaluating the position and might change it in the future.

@Aron I am wondering if parts of my prior argumentation has been wrong.

Here I am discussing that the completion of the takeover could bring down Vonovias LTV ratio. This is probably wrong because Dt. Wohnen is already fully consolidated in Vonovias numbers?

If this is the case Vonovia might not have an incentive to conclude the agreement quickly?

My main remaining worry are the recent comments of Rolf Buch about the weighted share price approach. According to ChatGPT this approach was indeed used more commonly recently.

What is your take of that? Do you find any additional sources or indications that the conversion price offer could be unfavorable even though this might not hold up in court or do you have more arguments why the initial conversion price offer will likely be good?

You are right, the LTV ratio will likely remain unchanged since the Dt. Wohnen is already fully consolidated. But there are other benefits that will accrue to Vonovia through the DPLTA, hence it remains important that the process is completed quickly.

“This reduces complexity, increases the speed of decisions and strengthens legal certainty,” a Vonovia spokesperson recently said in reference to the DPLTA.

Rolf Buch said in this article that the extraordinary general meetings may not take place until January since the determination of the offer price may not have been completed by December. If only the weighted share price approach were to be used, then determination of the offer price would be quicker. Additionally, according to Bafin, the offer price can be based on the weighted share price approach only if the process relates to voluntary takeover bids, mandatory offers and delisting offers. According to GPT, a DPLTA is not related to these processes. Based on recent company control offers, it appears to me that only the weighted average price approach is used in cases of squeeze-outs and delisting offers. Here are examples;

The Vodafone-Kabel control agreement (which Rolf Buch is referring to) was a squeeze-out offer.

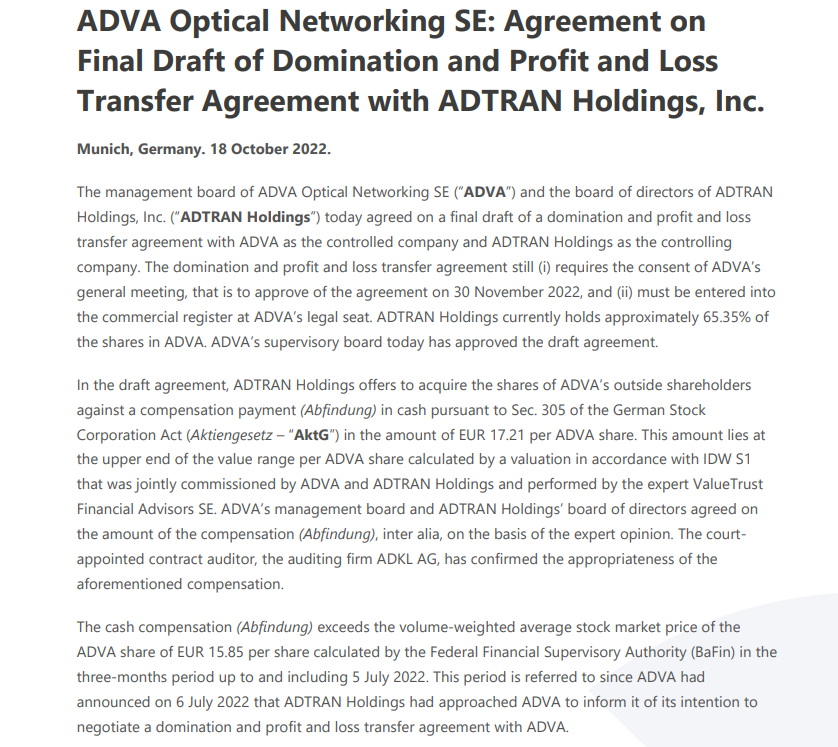

The October 2022 DPLTA between ADVA and ADTRAN based the offer price on fair value and weighted average share price.

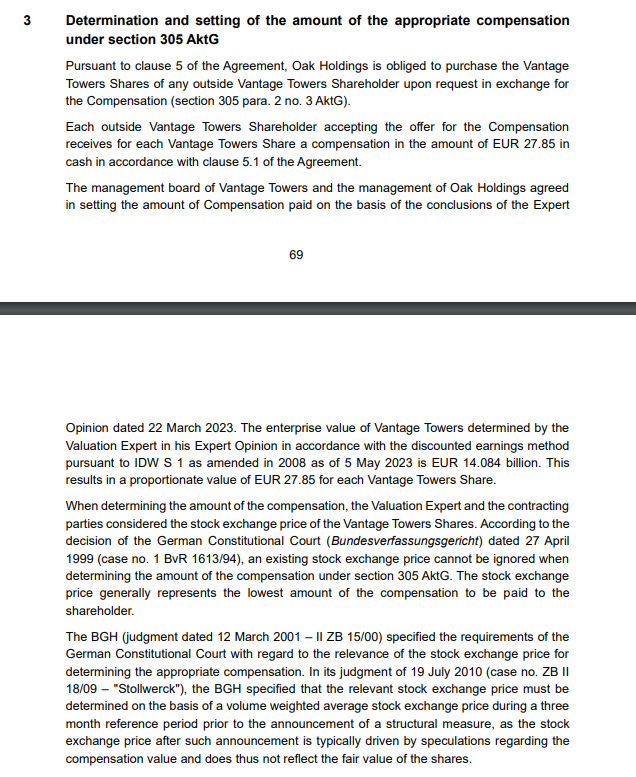

The March 2023 DPLTA between OAK Holdings and Vantage Towers determined the offer price based on the fair value and the weighted average share price (around page 78).

The 2020 DPLTA between AMS and OSRAM based the offer price on the fair value and the weighted average share price. One year later, OSRAM was delisted and minority shareholders received an offer price based only on the weighted average share price approach (page 29)

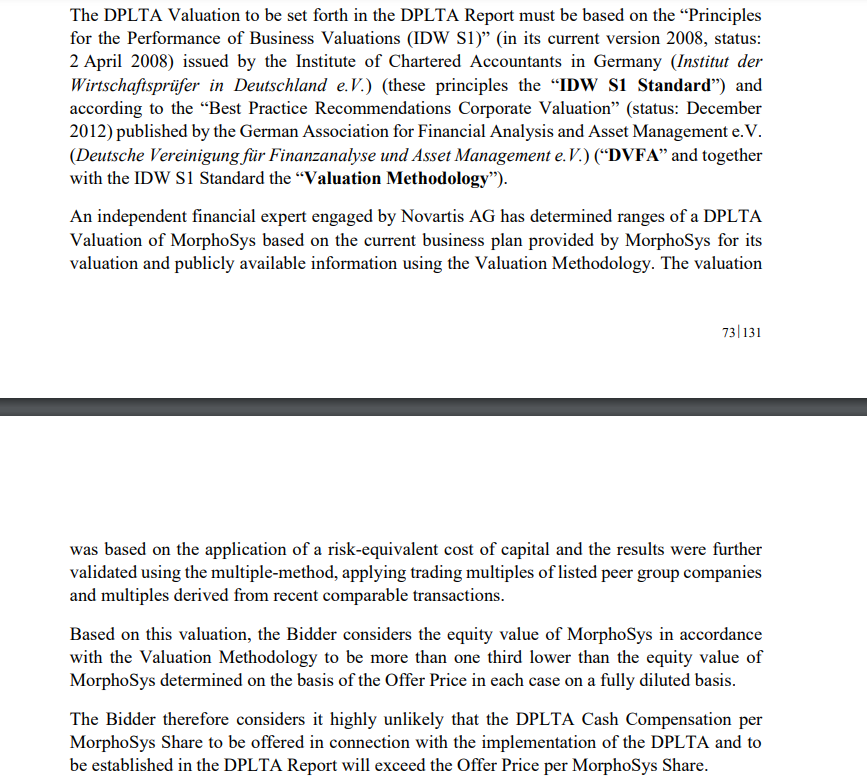

In the 2024 voluntary takeover of Morphosys by Novartis, only the weighted share price was used to determine the offer price. However, Novartis said then that it intended to pursue a DPLTA and that they had determined the DPLTA offer price based on the enterprise value of morphosys (page 79)

In summary, all the DPLTAs that I have looked into (around five) have computed the offer price based on the fair value and the weighted average share approach. That’s, they based their offer price on German Federal Court of Justice ruling of 2001. The ruling states that under DPLTA, the offer price should be the higher of the fair value of the company and the weighted average share price in the last three months.

As such, I don’t see the possibility of Vonovia deviating from these precedences.

Insights on the DPLTA from Vonovia’s earnings call

In their Q3 2024 earnings presentation, Vonovia highlighted the importance of the DPLTA such as reduced complexities and stated that the exchange ratio will be made according to legal requirements.

When asked whether they will consider a voluntary price instead of the legally required minimum price so as to drive up higher acceptance price, they said that they will wait for the valuation report and that their desire is not to increase the acceptance rate but to achieve a lean structure.

“The valuation work is currently on its way including a court-appointed appraiser, and we will await the results. We will then discuss it and decide with the invitation to the EGMs, which will take place in January you will see all the details. So that’s going to be pre-Christmas. So let’s wait for that,” CFO Philip Grosse said.

“But to be very clear and I think this is sometimes on understood, especially in the society, not so much in Europe. We are not doing this to get more shares from Deutsche Wohnen necessarily. We are doing it to get a determination agreement to clean up the structure,” CEO Rolf Buch added.

Rolf Buch pointed out that Deutsche Wohnen minority shareholders will not receive the same compensation as Apollo. He also concurred with an analyst who asked whether the minority shareholders are at risk of getting a lower compensation than Apollo.

“This is different. So this will, of course, not be the case because there’s a big difference because Apollo structure does not allow to liquidate their shares, while the others have a liquid stock, very simple,” he said.

Assessment

The fact that Apollo structure doesn’t allow Apollo to liquidate their shares, effectively rules out the possibility of a squeeze-out in future. Also, the fact that Vonovia is not interested in a higher acceptance rate lowers the incentive for a higher exchange rate. However, the fact that they have stated that legal framework will be used to calculate the exchange rate means that the fair value will likely be used.

Good overview. I largely agree with your assessment. Overall, those are not good news esp. that Apollo investors will get a higher compensation compared to regular DW investors. (But we could have expected it in hindsight)

According to your explanation here, couldn’t the JV squeeze out remaining shareholders even if Apollo investors which are longterm strategic allies cannot sell?

If I had to speculate I would think that Vonovia will probably want to wait for the results of the appraisal process and then discuss numbers with key shareholders like Elliot to see if there is common ground so they don’t have to face those large and sophisticated shareholders in court.

A squeeze-out affects all the minority shareholders. That means either Apollo will have to liquidate their shares or Vonovia will have to sell their outstanding shares to the JV. The JV will then carry out the squeeze-out of Dt.Wohnen minority shareholders. Since the Apollo structure doesn’t provide for liquidation and Vonovia is after a lean structure and not a high acceptance rate, I no longer see the possibility of a squeeze-out.

There is a difference between something being technically impossible or us seeing it is unlikely.

In theory Vonovia could sell its shares to the JV and the JV could squeeze out remaining shareholders correct? (Let’s say in order to get rid of remaining independent shareholders who sue against the DPLTA)