I=10 Vonovia wants to acquire Deutsche Wohnen shares held by minority shareholders

Vonovia and Deutsche Wohnen have initiated discussions to conclude a domination and profit and loss transfer agreement.

Vonovia is looking to acquire shares held by Deutsche Wohnen minority shareholders in return for newly issued Vonovia shares and an annual payment for the duration of the agreement.

Deutsche Wohnen shares up around 20% following the news.

A DPLTA can be concluded by a company once it achieves 75% voting rights (Vonovia has 87%).

The price offered is usually the greater of fair value, weighted price in the past three months preceding domination announcement or price offered to other shareholders in the last six months.

Shareholders who don’t want to participate in the DPLTA can retain their stake and will be paid a guaranteed annual dividend calculated based on the company’s historical earnings and future earnings prospects. The guaranteed dividend has generally been at least 5%.

If the some shareholders aren’t satisfied with the compensation, they can launch an appraisal proceeding in a court. The court can either dismiss the proceeding or raise the compensation-it can’t lower it.

Possible share exchange ratio

To establish the compensation that Deutsche Wohnen minority shareholders will receive, I looked at past DPLTA actions in Germany, one between Deutsche Wohnen AG and GSW Immobilien and another one between TLG IMMOBILIEN AG and WCM AG. In both cases, a discounted value and not the Net Asset Value (NAV) per share was used. The fair value arrived at was, however, not much different from the NAV. What is interesting is that the valuation expert for Deutsche Wohnen AG -GSW Immobilien had to compare the discounted value with the NAV to make sure that it was reasonable. Additionally, in the 2021 takeover of Deutsche wohnen shares by Vonovia, only the NAV was used as a valuation indicator. A joint statement by the two companies indicated that NAV was considered the main valuation indicator for the real estate industry. Therefore, I believe that the share exchange ratio in the Deutsche Wohnen DPLTA will probably be 1:1 given Deutsche Wohnen and Vonovia have a NAV of EUR 42.01 and EUR 44.08, respectively (confidence level: 70%). Below are my other arguments supporting this conclusion;

Turnaround in German real estate sector: According to insights, German real estate sector is beginning to stabilize. This will likely boost real estate shares in the near future. As such, Vonovia will likely offer an attractive offer in order to avoid squeezing out minority shareholders in future at a higher price.

One billion state tax: To achieve a squeeze-out, Vonovia will need to raise its stake to 90%. This will result in 1 billion euros state tax. I assume that Vonovia would want to avoid this until there is a complete pick up in the German real estate sector. Hence the best thing to do is offer attractive compensation.

Exchange of cash between Vonovia and Deutche Wohnen: If Vonovia doesn’t provide an attractive compensation, Elliot Investment (which has 3% stake) will probably hold on to its shares. This will be a constant headache for Vonovia whenever it wants to borrow funds from Deutsche Wohnen as seen in the past. I also assume that Vonovia wants to exert control over Deutsche Wohnen’s cash before a turnaround in German real estate sector fully materializes.

Good insights and interpretations. Especially, how the NAV was considered in the appraisal proceedings is interesting as well as the tax implications. I actually knew about them but completely forgot for a moment.

One of the next steps is getting a bit more insights into the current state of Vonovia.

Did they manage to sell some assets or raise some money and are now in a more financially stable position or need borrowings of Dt. Wohnen as much as before? What is their cash position? I assume that they would prefer that more shareholders exchange their shares for newly issued Vonovia shares instead of paying them in cash at a possible squeeze out later which could also hint at a 1:1 exchange ratio

Edit: Just in theory - could Vonovia sell Dt. Wohnen stock in the next months to keep the stock price down + raise money? (for the price of having to issue & exchange more new shares later)

Yes, they can trade Dt. Wohnen shares but only to an extent where such trading will not cause volatility or be construed as manipulating share prices.

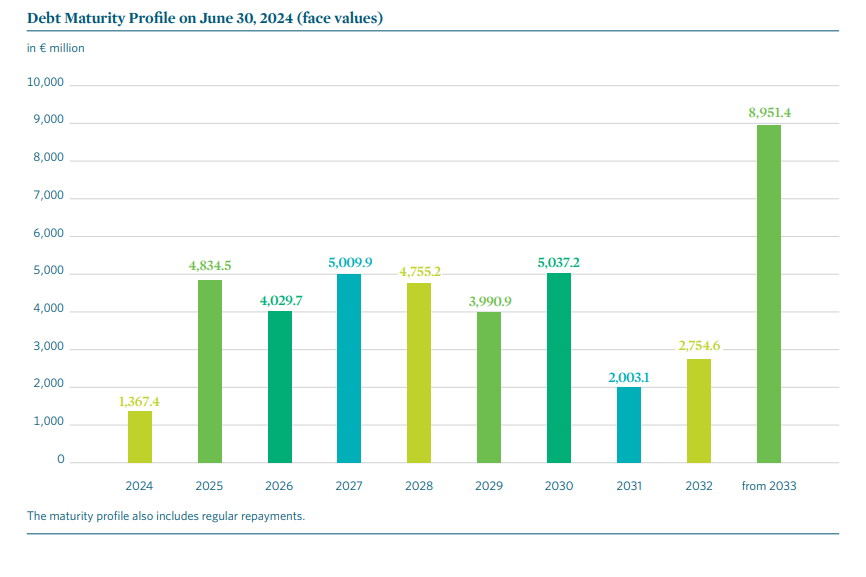

They have issued bonds worth €1.5 billion this year (H1 2024 report, page 7) and sold properties worth €1.5 billion. They are targeting to sell properties worth €3.0 billion in 2024. As at June 2024, it had €1.3 billion in cash and cash equivalents. That means its outstanding debt refinancing of €1.4 billion in 2024 is already covered. It is facing a debt maturity €4.8 billion in 2025. Therefore, though it seems to be managing its liquidity well, I think it will continue borrowing. Also, it’s expected to increase the pace of construction by around 1,500 units next year (from the current 2,500-3,000), which means it will need more cash.

Given that Dt. Wohnen is trading significantly below it’s NAV and has an up to 30% (?) short-term upside it might be worth considering to increase the position.

Do we know if Vonovia has been selling/buying any stocks in the last 3 years since the takeover? How often are their holdings reported? (In every quarterly or yearly report?)

Obviously, there is a risk that the buyout will not go through, but if it goes through, there should be a floor price for how low the stock price could go. If it does not go through there is a strong NAV.

What do you think which price is the worst price Vonovia can offer? How high are the changes that the buyout will go through?

What is your overall assessment of the situation?

Methodology

I think when quoting longer sources, it is always good to give a page number indication in brackets, e.g. (p.5), so that it is easy for the reader to know exactly which section we are referring to. What is your assessment of the sources you’ve linked how much Vonovia could sell without causing volatility or manipulating the market?

For the case of Vonovia, Deutsche Wohnen is only required to file holdings changes if it falls below 76%. However, it reports the current stake that Vonovia has in its half-yearly and yearly reports and here. Vonovia’s stake of 86.87% hasn’t changed since November 2021.

Those sources don’t indicate how much Vonovia could sell without causing volatility in share prices. In essence, Vonovia could use block trades to sell a large number of shares without causing volatility. However, suppressing the share price so as to buy at a lower price during takeover would still fall under market manipulation.

I think the worst case scenario is a premium of between 15% and 30% over the closing price in September 18. That will result in an offer price of between EUR 26.0 and EUR 29.0.

I think the DPLTA will easily sail through in the December AGM given that Vonovia controls majority of the voting rights. It can only fail if it’s either withdrawn by Vonovia or if it’s quashed by the anti-competitive regulator. I think the probabilities of these two are low. Firstly, Vonovia has been planning for it. In 2021, it said that it won’t initiate DPLTA until 3 years elapses. Secondly, current market conditions are favorable to buy out the minority shareholders. Thirdly, the combined portfolio market share of the companies hasn’t changed. For instance, they currently have 143,063 units in Berlin(March 2021: 151,000), hence like in 2021, the Bundeskartellamt will probably conclude that the DPLTA will not impede competition.

Hmm, it is pretty interesting that Vonovia is moving instantly after the 3 years expired.

Here are some additional elements that I think we should always analyze in a deal situation like the current one to give reference.

Impact of different conversion prices for Vonovia

As of H2 2024 there have been 400.30 million Dt. Wohnen shares (p. 4). In order to completely take over the company Vonovia needs to buy 12.29% of them or 49.20 million. This equates to a price of EUR 984m at EUR 20 a share, EUR 1,280m at EUR 26 and EUR 1,574m at EUR 32.

This cost is non-cash consuming as it will be paid by newly issued shares.

There are 822.85 million Vonovia shares. (H1 Report, p. 6)

It will dilute Vonovia shareholders by 6.0% if there is an exchange ratio of 1:1 and by 4.0% if the exchange ratio would be a low 3 dt. wohnen shares for 2 Vonovia shares.

Dt. Wohnen trading volume & price action

Trading volume at Xetra,Tradegate and a few other minor exchanges has been around 3 million shares since the announcement of the buyout. This is less than 1% of total outstanding shares. It tells us that there has been no significant buying interest and no significant exits of large shareholders. (Unless there are OTC block trades)

The current price action that we are seeing might therefore be meaningless as a signal of the conversion price and could be caused for example by some speculators which potentially heard market rumors about the announcement of the buyout beforehand and are taking some profits, some minor shareholders selling, or one larger shareholder reducing his position.

Conversion Price discussion

In addition I think we should always create a section in the associated Wikiarticle which highlights upsides and risks to have a good discussion base what outcome is most likely.

Especially a strong focus and arguments on risk is important as complacency is the largest source of mistakes and fallacies for investors and to be avoided at all costs.

Upside arguments are also important and should not be missed as well.

Below are some of my arguments and open questions. @Aron Can you create such a section in the Wiki and include my arguments and all arguments which are still missing + post your assessment here what you find will most likely happen and why and elaborate further on some arguments (either yours or mine) in more detail?

Upsides (to stock price)

LTV is risk factor for Vonovia and merger with Dt. Wohnen will reduce it

I still think Vonovias main reason to complete the takeover is bring down their LTV ratio, which is currently, as of H2 2024, standing at a very high 47.3% (presentation p. 10) while Dt. Wohnen has a LTV of 30% (p.2)

As a reminder Vonovias bond covenant is at 60%. At this threshold, creditors could size assets and force sell them.

Further rational for Vonovia to conclude deal quickly

Therefore I think Vonovia has a high incentive to conclude the matter swiftly and don’t have year long court procedures before they can complete the merger. In addition, having this deal completed frees Vonovia up strategically as it should improve their ability to borrow, which would lead to less pressure to sell property and allow them to seize buying/development opportunities if they arise.

Furthermore, a good/fast takeover will clear one major time-consuming issue for management and there will be less expenses for having duplicated functions in accounting, investor reporting etc. and all remaining synergies from the merger can be realized.

Risks (to stock price)

Vonovia has higher adjusted EBT per share

The stronger adjusted EBT per share is probably the strongest argument for a worse exchange ratio. Maybe the methodology changes in reporting from FFO to EBT has been a preparational step to strengthen the basis of Vonovia? (I did not look that up yet)

Do we know if both companies use the exact same methodology after the change? How much stronger is Vonovias adjusted EBT based only on rental? (EBT on rental is more related to underlying value compared to EBT from areas like development that can be more volatile.)

Average weighted stock price 3 months prior to buyout announcement has been relatively low

In the source that you’ve linked (p.9) it says that the average weighted stock price prior to the announcement of DPLTA agreement is important for the minimum consideration. Key are the 3 months prior to the announcement itself not the 3 month prior to the finalization of the terms and the offer. This average weighted stock price is relatively low.

Deal cannot completed quickly or negation offer is lower than final offer

Do we know for sure which threshold Vonovia needs to reach to initiate a squeeze-out? Are we 100% sure that the 90% threshold? Here it says to use the 90% threshold the process would need to be within initiated 3 months after the merger. Maybe it is 95% in this case instead? How quickly could a squeeze out be concluded if there are lawsuits against it? Potentially all considerations from above that it would be advantageous to have a faster buyout do not matter in case Vonovia knows it will take years in any case?

Risk Vonovia stock price falling

Regardless of how exactly the exchange ratio turns out a falling Vonovia stock price is certainly a possibility and risk. This risk could be high given the recent surge in stock price and if the german property sector would develop badly for example due to an economic downturn.

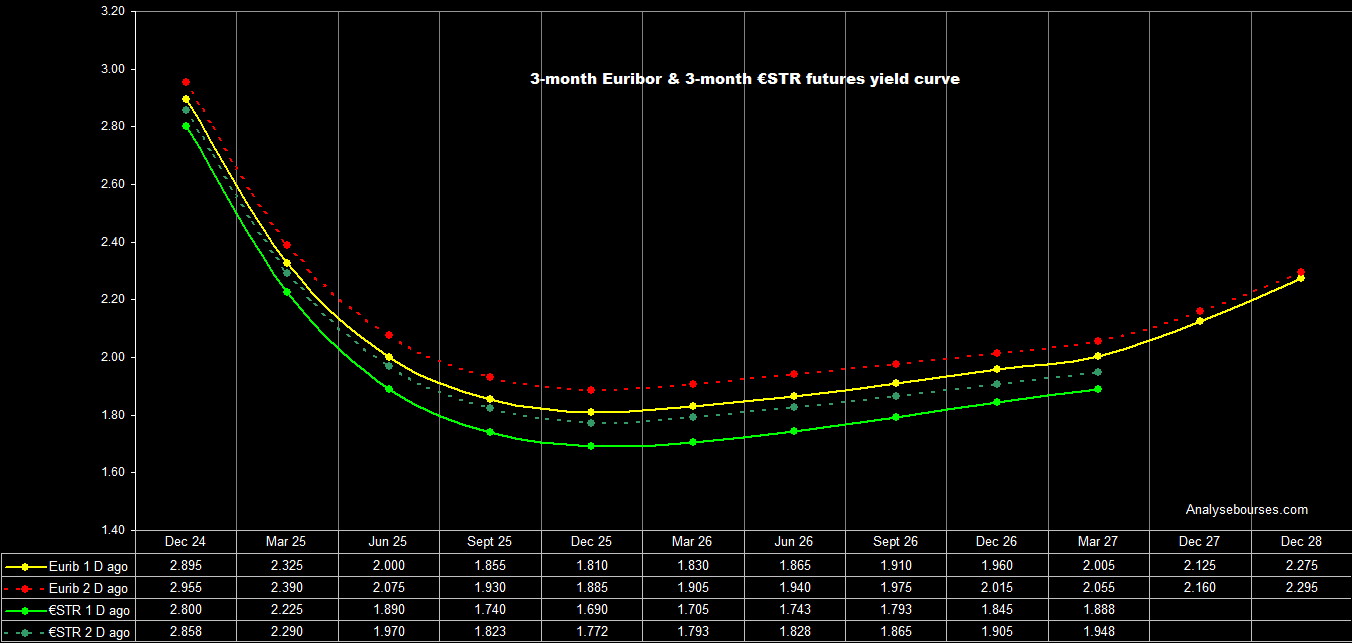

@Magaly, do we have a rough indication/project of how interest rates will develop in Europe? (Best if posted in correct topic and linked here)

Here you can find current market expectations and ECB projections.

Around 175 bps of easing priced in, which I don’t necessarily disagree with, because of a weaker economy.

Here are answers to some of your questions and further clarifications of my points above (based on further research);

I agree with you that Vonovia having higher adjusted EBT per share is the main argument for a worse exchange ratio. This is because earnings is usually one of the main factors considered when computing a company’s enterprise value. But why should we compare only adjusted EBT for the rental segments yet Vonovia would be valued as whole? The two companies shifted to adjusted EBT methodology at the end of last year. However Vonovia doesn’t breakdown its adjusted EBT into individual segments. At the end of first half 2024, Vonovia had an adjusted EBT of EUR 887.2 million, or EUR 1.09 per share (page 14, H1 2024 report) while Deutsche Wohnen had adjusted EBT of EUR 281.4 million, or EUR 0.71 per share (page 1, H1 2024 report). This will result in an exchange ratio of 1:1.42 or 7 shares of Deutsche Wohnen for 5 shares of Vonovia. Based on this and Vonovia’s closing price on September 18, the price that would be offered to minority shareholders would be EUR 22.99. This offer is higher than the Deutsche Wohnen’s share price of EUR 22.60 at the close of September 18.

Yes, the best entry-point for Vonovia squeeze-out of Deutsche Wohnen minority shareholders would be 95% of voting rights. At 90%, it can only initiate what’s called merger squeeze-out which will need merging with Deutsche Wohnen. Since merger agreement and profit and loss agreement (PLTA) won’t work hand-in-hand, general corporate squeeze-out which only requires 95% votings rights would be viable. To attain 95% voting rights, Vonovia would have to increase its shares at Deutsche Wohnen by 32 million, another reason it should offer an attractive exchange price.

German corporate act provides for fast tracking of cases related to squeeze-out release procedure. Such cases can take between three to six months to be resolved. However, appraisal proceedings take years to be concluded. Given that appraisal proceedings don’t prevent DPLTA or squeeze-out from being concluded, Vonovia could offer unattractive price now hoping that it would offset the future premium given by the court (and associated interest) with better earnings. Due to interest on the premium of up to 5% and legal costs, the probability that Vonovia will employ this strategy may be low.

Vonovia currently has 86.87% stake in Deutsche Wohnen, hence short of 3.13% to trigger the real estate tax. Since the DPLTA will push Vonovia shares upward, there is a high chance that this threshold will be hit. I estimate that Vonovia will pay around EUR 487 million real estate tax once it crosses this threshold. Given Vonovia’s current financial situation, it will probably borrow money to pay this tax. Therefore, the faster it completes the DPLTA, the sooner it can use Deutsche Wohnen’s cash to pay the debt.

Assessment

Since fair value (derived from adjusted EBT) was used in past real estate DPLTAs, I think adjusted EBT should outrank NAV in our assessment. If we are to use adjusted EBT per share, the mostly likely worst scenario is an exchange price of EUR 23.00. However, due to the expected benefits that Vonovia will obtain from the DPLTA, the exchange price could be higher than that. I would also expect the offer price to be higher than Deutsche Wohnen’s price on the day that DPLTA offer will be announced (to incentivize minority shareholders to exchange instead of selling at the open market). Therefore, I would still give it a premium of between 15% to 30% (22.5% at the mid-point). That will result in an offer price of EUR 28.20 (at the mid-point) or 6 shares of Deutsche Wohnen for 5 shares of Vonovia.

I think given the importance of the topic we should even dig deeper.

When comparing adjusted EBTs we should take the last couple of years into account to get an more longerterm view of the adjusted EBTs over time for both companies. We also need to make sure that they use the same methodology (adjust for same things and make sure that business specific temporary effects are reliably excluded in adjustments) and we also need to look at the core underlying strength of the businesses. Thats why I suggested to see if we could separate out the adj. EBT associated to rental incomes and therefore indirectly property values. This business is a very secure and stable conservative business while Vonovias development business is way more risky, should fluctuate more and in the worst case they can even loose money with it.

So if I understood you correct Vonovia would need 95% to initiate a squeeze out and 90% would not work? It is important to be absolutely certain on that point.

The fast tracking for a squeeze out is interesting. Does it work in both the 90 and 95% cases? (The laws are different for them as they have been designed for different situations and therefore details for squeeze out speeds might also vary)

I=8 Vonovia and Apollo forms a company that will hold 20% stake in Deutsche Wohnen

Vonovia said that it has agreed with Apollo to set up a business that will hold 20% stake in Deutsche Wohnen, in which Vonovia and other longterm investors will be invested.

The liquidity inflow for Vonovia from the Apollo partnership will be around 1 billion euros.

A company by the name WPG Legal Holdings Limited (probably the joint venture formed with Apollo) has acquired 19.83% stake in Deutsche Wohnen.

Assessment

@moritz I think Vonovia has sold some of its stake in Deutsche Wohnen to Apollo. Assuming today’s closing price of EUR 25.45 was used, then Vonovia may have transferred 9.82% of its stake and is now left with 77.05% (direct ownership: 67.04%, indirect ownership: 10.01%). Since having total control over Deutsche Wohnen will likely attract long-term investors to the joint-venture, this increases the probability that Deutsche Wohnen minority shareholders will get attractive offer price. What do you think?

Deutsche Wohnen shares are up 4% following the report.

Edit:

According to whispers, Vonovia will hold 51% stake in the special purpose vehicle while Apollo will hold 49%. That means Vonovia now holds around 77% stake in Deutsche Wohnen (directly: 67%, indirectly: 10%). This means that Vonovia transferred around 9.72% (or 33.8 million) of its stake to the special vehicle formed with Apollo. As a result, Vonovia might have been offered EUR 29.6 per share. The special vehicle will mainly help Vonovia avoid paying real estate tax since the 90% threshold will not be crossed after buying out all the Deutsche Wohnen minority shareholders.

I think that’s a good move by Vonovia to increase their liquidity and stay below the 90% threshold although it means they have been selling their Dt. Wohnen shares at a loss compared to their high takeover purchase price.

How do you arrive at a price of 29.6€?

Do we have other analyst opinions or commentary already?

In general other Forums or places where people comment in detail on the same topics we are working on could be great places to find great people for the community and attract them by engaging in discussions.

I divided the 1 billion euros received by Vonovia from the special fund vehicle by the 33.8 million shares transferred. However, the shares were acquired through conditional purchase agreement instruments maturing on September 30, 2025. Could that be the date when Vonovia will be paid?

We have 19.83% of the total shares transferred.

If the source is correct and 51% of those shares are sold to Apollo Investors that’s 10.1% of total outstanding shares or 40.48million shares.

Vonovia said they get a bit more than 1 billion in liquidity.

Considering fees for the transactions a sell price of around 1050million might be reasonable. This translates to a price of EUR 26 per share. (1050m/40.48m)

Vonovia might argue that this is the price third party investors are willing to pay and the price which is fair to offer in a share swap.

I think the purchasing agreement is likely conditional to make sure it works well in the context with the entire restructuring (DPLTA & offer to swap shares)

That’s correct (I made an error with the shares outstanding).

The conditional agreement could mean the transaction price could as well change if minority shareholders succeed in arguing a higher price or if market conditions change?

Yeah, the transaction price could have also been estimated using yesterday’s closing price of EUR 25.45.

According to Jefferies analyst, the plan came as a shock to him since Vonovia made it clear during the 2023 earnings call that it was not looking for another JV with Apollo. He thinks the plan will likely put a strain on Vonovia’s operating profit (FFO).

Overall I think the deal is positive because it shows that there is significant institutional investor demand for Dt. Wohnen shares at the current price point. That means that in order to convince investors to swap their shares they might need to offer them a premium over current prices.

Alternatively there is also the possibility that Vonovia made deals with some of the larger Dt. Wohnen shareholders. Someone like Elliot might participate in buying Dt. Wohnen shares through Apollo and then later swap their shares for Vonovia shares at the same price point. That way they can keep their interest in Dt. Wohnen and Vonovia does not need to deal with individual minority shareholders anymore.

Overall I think the downside risk for Dt. Wohnen esp. after this latest transaction is very limited and I will most likely simply hold and wait.

Yeah, those are possibilities. But I think the interests of Apollo and investors like Elliot may not necessarily align. For instance, I think Elliot will stand a better chance to conduct its activism roles by investing directly in Deutsche Wohnen instead of buying through Apollo since Apollo will be acting on their behalf.

I agree that the downside risk is now limited. Does that mean there is no need to answer this open questions?

Yes I agree that for Elliot it is better to be invested directly. Maybe they want to keep their position though and having it through Apollo is the only solution because otherwise they will be forced out by the DPLTA.

Yes the importance to get detailed answers to those questions is now reduced. Maybe you can go for a simple high-level comparison of adj. EBT of the last couple of years without trying to differentiate by businesses unit (rental, development etc.) so we get an impression without spending too much time.

We also don’t need insights into squeeze outs anymore because there will be no squeeze out (?)

Loosing the ability to squeeze out remaining shareholders could be positive for the offer Vonovia is going to make?

If I remember correctly, Elliot took a stake in Deutsche Wohnen hoping for a squeeze-out at a higher price. That’s what Elliot is known for. Unless its interests have change, it could still want to get out.

Why do you say there will likely be no more squeeze-out? I think Vonovia and Apollo could still want to have total control of Deutsche Wohnen, hence squeezing-out minority shareholders who refuse to take part in the DPLTA will be an option. Also, Vonovia now has enough liquidity to pay off these shareholders. But yeah, the journey to the 95% squeeze-out threshold is now further than before the formation of the special purpose vehicle-providing a reason to offer an attracting price at the DPLTA stage.

I already found insights on the squeeze-out questions anyway;

At 90% threshold, Vonovia can only launch merger-squeeze-out. Here, Deutsche Wohnen will be absorbed into Vonovia and it will cease to exist. I don’t see this as a possible scenario since the investors to the special fund vehicle are interested in Deutsche Wohnen. Also, if it uses this method, there will be no need for profit and loss sharing agreement. Vonovia won’t have initiated the DPLTA if it intended to merge with Deutsche Wohnen. In other words, a merger is an alternative to the DPLTA (page 49). That means Vonovia is mostly likely to prefer the 95% squeeze-out threshold.

It doesn’t matter whether the squeeze-out is at 90% or 95% threshold, fast-tracking of anti-resolution proceedings apply to all statutory mergers, DPLTAs and squeeze-outs. Since economic interests is usually given priority when deciding those cases, the interests of the company usually prevail over the interests of the minority shareholders.