Worst retail sales drop in nearly two years. Since Dec was had a very strong holiday spending and the weather events in January, the dropoff to January could just be noise, and be a one-off.

However weakness in the control group that directly flows into GDP (spending is 70% GDP) is not to be dismissed entirely.

The growth concerns highlighted by the weak Jan retail sales print reverse some of the upside pressure on rates as the Fed has to weigh implications for both sides of its mandate.

Based on market pricing, there is actually a higher probability of a rate cut in June now than there was before the CPI report, with 10y yields down even more on growth concerns.

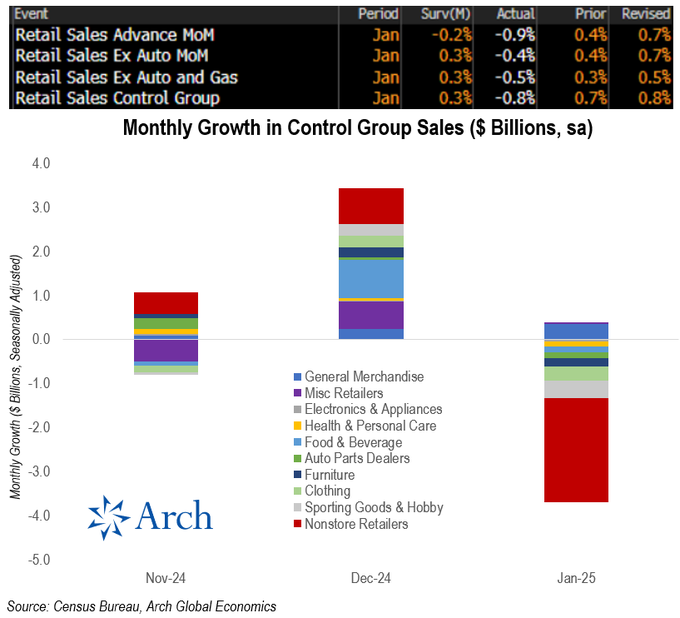

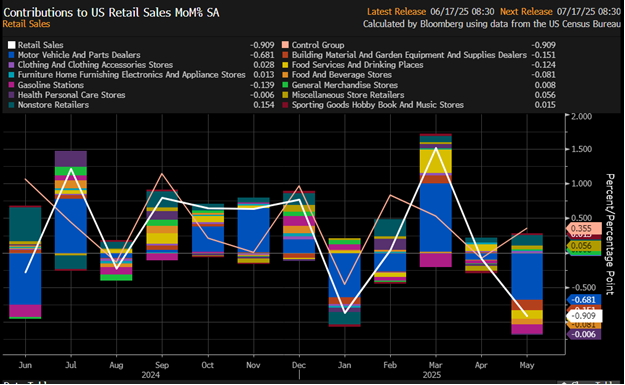

Retail Sales -0.9%, Exp. -0.2%. At 4.2%, year-over-year growth is still above most of last year.

Retail Sales ex-auto -0.4%, Exp. 0.3%

Control Group -0.8%, Exp. 0.3% (direct input for GDP)

Retail sales is very volatile, but the miss was outside normal levels. It was nearly a 5 sigma event for control group retail sales based on the economists surveyed by Bloomberg.

Auto Dealers had a bad month and were the main drag on headline retail sales.

Nonstore retailers (i.e. online sales) were the big drag on control in Jan '25, recording the worst monthly decline since the immediate aftermath of the pandemic in July '21.

If we look at Retail Sales Ex Auto MoM, there is a 0.7% difference between the survey expectation (0.3%) and the actual (-0.4%).

The miss on headline retail sales was 0.7% as well.

This indicates to me that there is no surprise coming at all from auto but from other categories? Is this surprise solely coming from online sales or other sources? (Interesting case you can find those insights with reasonable effort) (The chart is a bit hard to read. It looks like online sales are down 0.4% m/m? If we know what was expected for online sales before the release we know how large the surprise was)

If yes, that could be a headwind to Meta?

There arent expectations reported for individual categories.

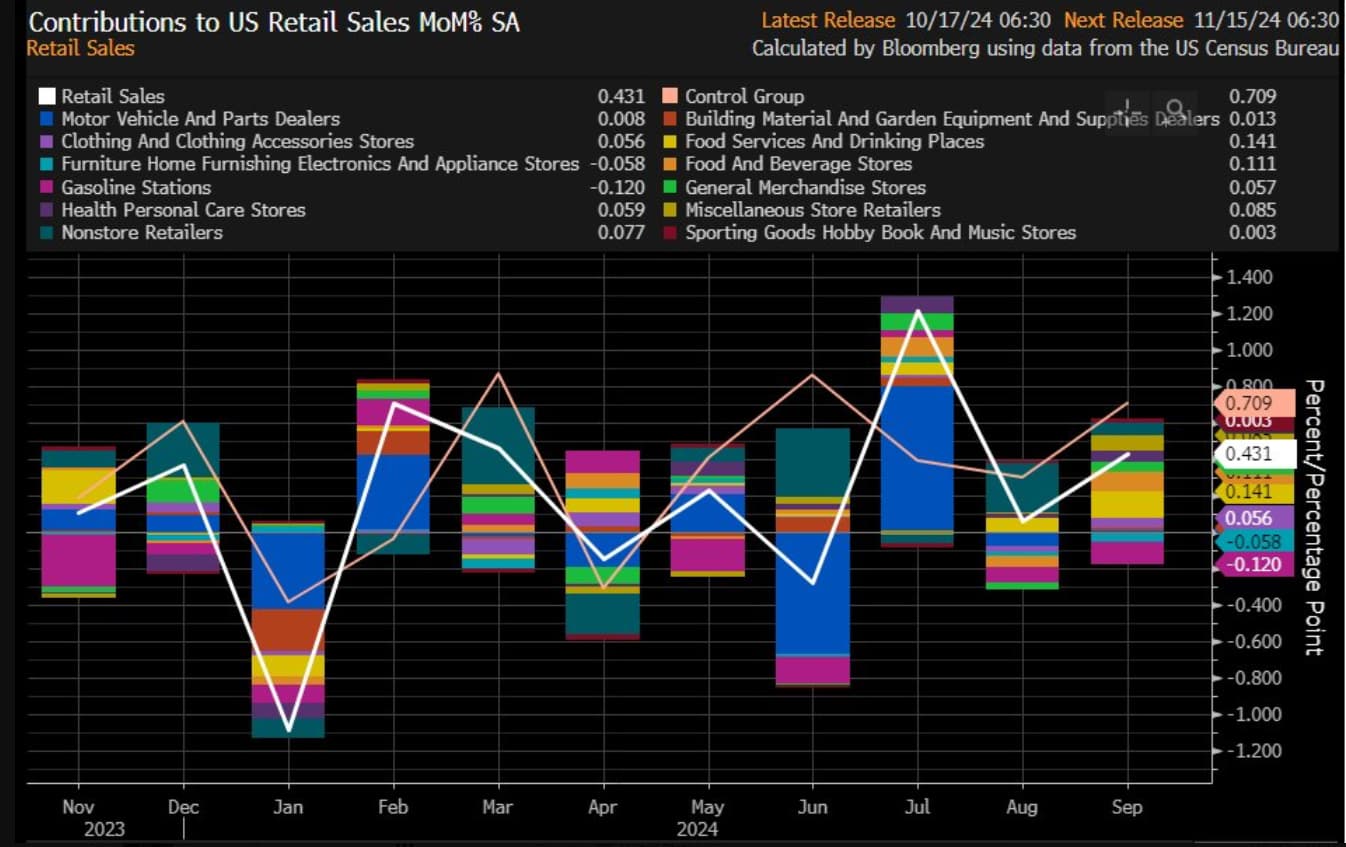

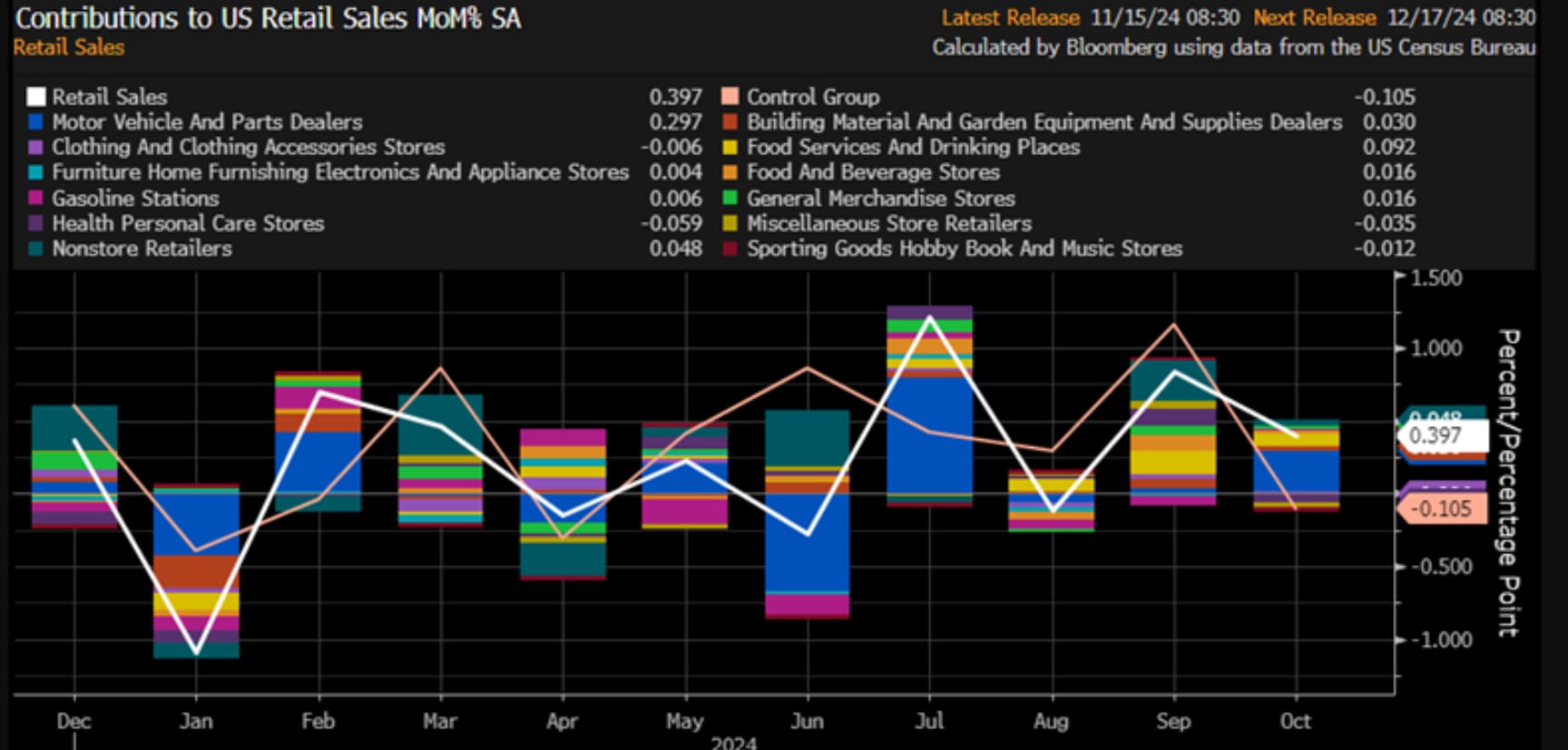

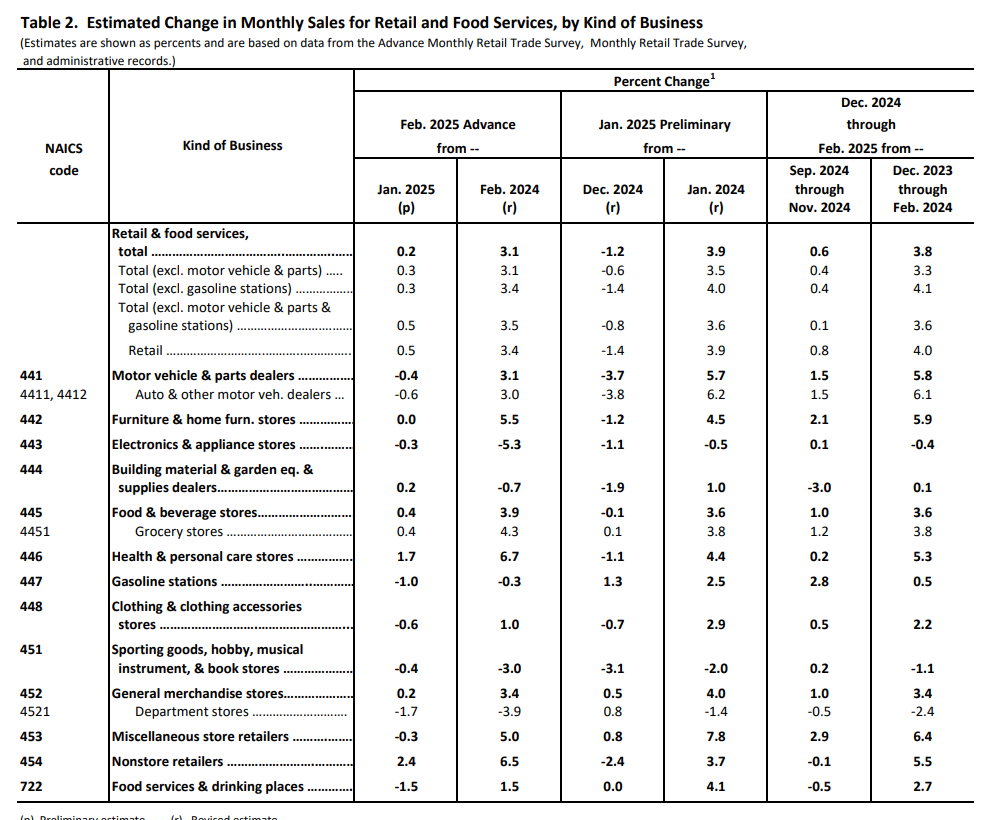

This is the more granular data from the report:

Auto sales are very volatile (that’s why they are excluded from the control group), and despite dropping -2.8% m/m. Is one of the categories expected to have been most affected by weather, and the pull forward of demand at the end of 2024 due to tariff expectations.

Online sales (-1.9 m/m) from what I got reading analyst posts were the more surprising, since weather is not expected to impact this category, contrary online sales should go up due to weather.

The fact restaurants and some retailers actually increased, it tells me weather did not have much impact, and weakness is beyond that at least in january. Could be just a bit of a pullback in spending after the spending was very high at the end of 2024.

I think would be premature to just made a conclusion based on this month only, but february data should be able to clear more. Maybe I could make a summary of retailers earnings, especially related to online, and see what they are saying currently.

Hmm you mean if those online retailers have a cautious Q1 outlook? I think if you can find something e.g. using GPT in 10-20 minutes it could be interesting but otherwise I would not invest too much time into it for the following reasons

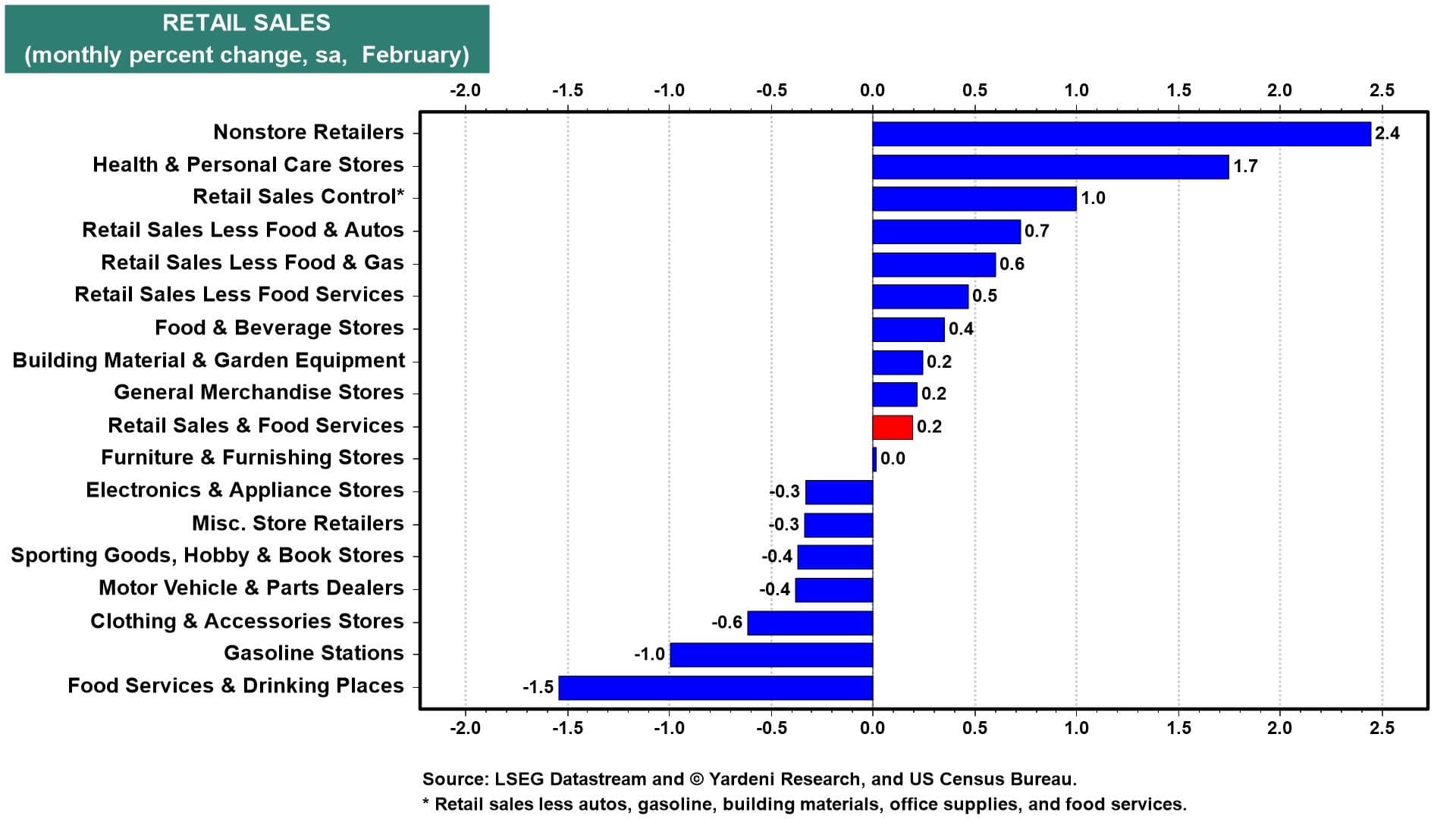

Nonstore retailers are still up 4.7% y/y which looks quite healthy too me. (Maybe December was even exceptionally strong) (Main argument)

Most advertisers on Meta are small businesses. Finding something on them is probably even harder and the correlation between performance of large listed online retailers and smaller online retailers is unsure.

As you say the data can be quite volatile so probably no reason yet to worry (esp. given strong growth y/y) and I would need to see stronger signs than one weaker month of online sales to consider reducing the Meta position.

Do you think maybe Bloomberg or one of those other sources has expectations by individual category? (If yes maybe some people you follow on the topic post pictures on X about it - Just something to keep in mind. Not worth investing too much time searching but great sources/people like those are always valuable for our sources database)

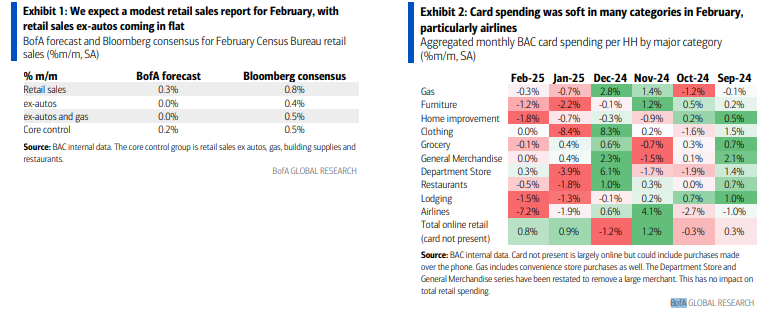

Bank of America expect a modest retail sales report based on its card data, below current consensus but better than January

“BAC card spending per HH was up 0.3% m/m in February on a SA basis. We expect the Census Bureau’s February retail sales ex-autos figure to come in flat, and the core control group (retail sales ex autos, gas, building materials and restaurants) to rise 0.2%”

Overall, a mixed report (downward Revisions to last month and barely a recovery this month), with some nice underlying strength in many areas (online sales continue to be very strong despite last month decline), but as expected it looks like there’s going to be some tariff front-running overhang, and some concern around the bars/restaurants since discretionary spending could be slowing, in line with trave demand slowing according to airlines guidance.

Year over year growth seems resilience still, though slowing in recent months (and below historical averages), and accounting for inflation is almost flat growth.

Despite the monthly improvement, this report caused the Atlanta Fed’s GDPNow model to lower Q1’s real GDP growth from -1.6% to -2.1%, led by a decline in the growth of consumer spending from 1.1% to 0.4%. (Model is not reflecting the gold imports adjustment, which they will do on March 26)

So, low or even flat spending is still expected for Q1 2025.

This is mostly goods-related spending (only about 35% of PCE), for services spending, will have to wait for the PCE report, and see Atlanta GDP adjustment for additional data.

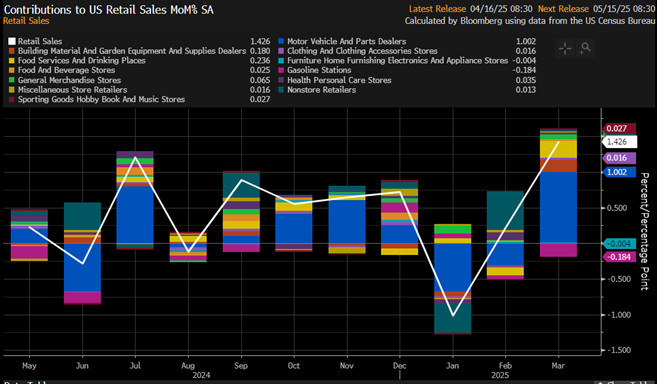

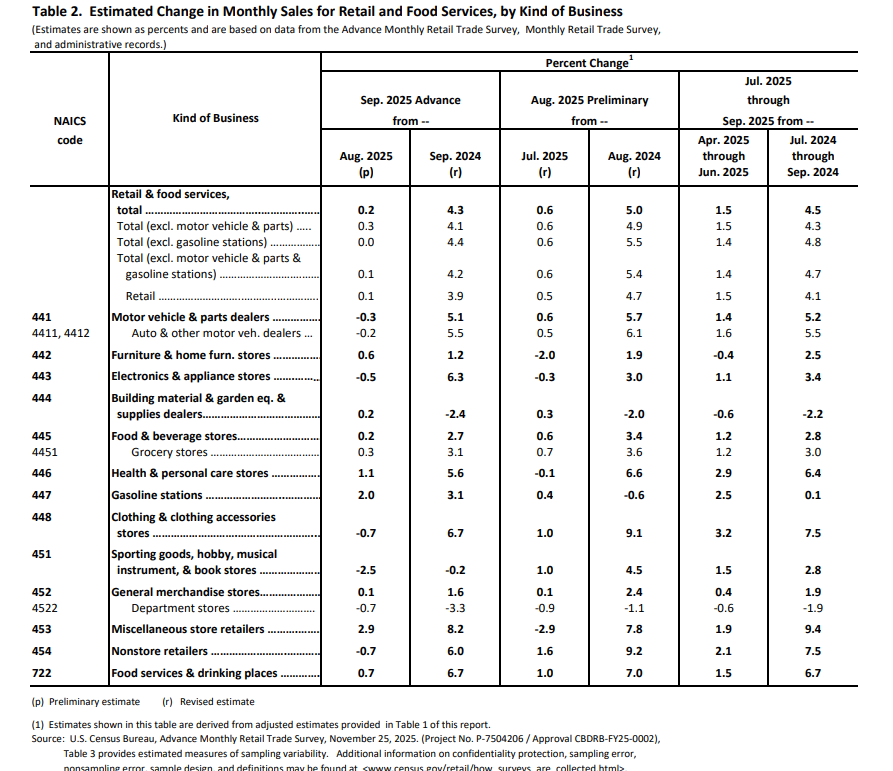

The gain in retail sales was driven by a jump in motor vehicles and auto parts dealers sales. Consumers likely brought forward car purchases before the tariffs kick in.

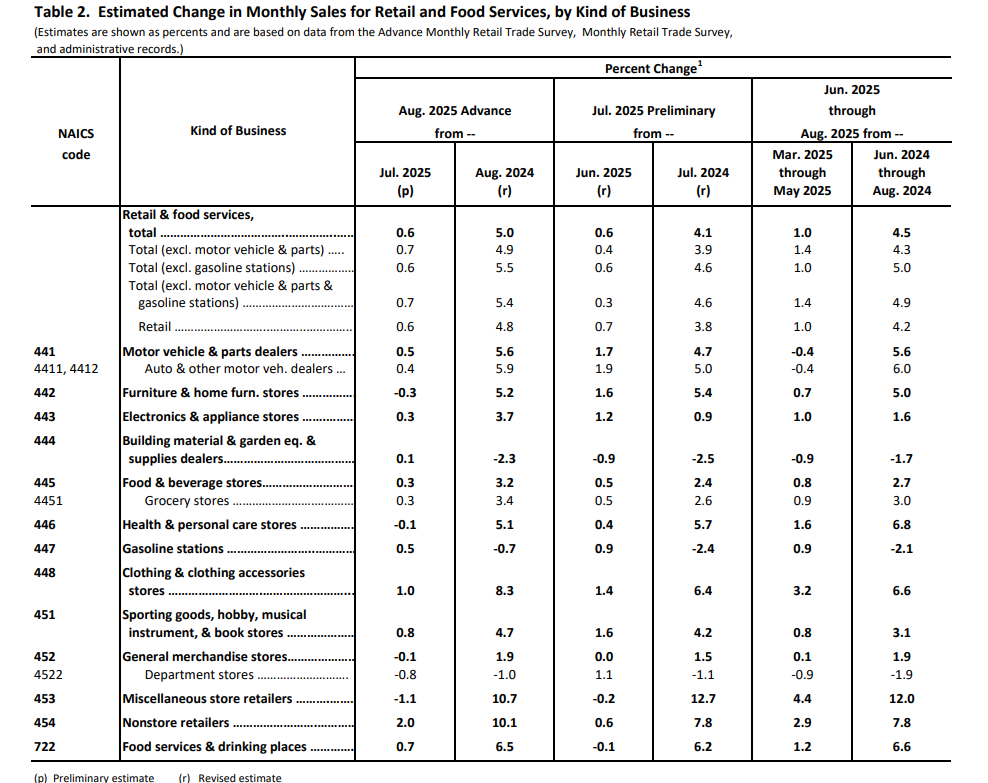

I=6 Retail sales rose 0.5% in July, missing the 0.6% estimate, June’s figure was revised up by 0.3%

Retail sales rose 0.5% in July, below 0.6% estimate and 0.9% in June (revised upwards from 0.6%).

Excluding autos, retail sales rose 0.3%, in line with expectations.

‘Control group’ sales, which feeds into GDP, rose 0.5%, above 0.4% estimate.

Nine of the 13 categories posted an increase led by motor vehicles and parts (1.6%), furniture and home furnishings receipts (+1.4%) and sales at online retailers (+0.8%) .

The strength in retail sales data eased concerns over consumer spending after uncertainty on Trump’s tariffs kept consumers on the sidelines.