This topic covers Sixt’s Q4 2025 earnings. A preview of the results will be posted here ahead of the earnings release. A full summary of the preview is available in the Notion:

Earnings date: March 4, 2026

Time of Earnings release: 7:30 CET

Time of Analysts Call: Unknown

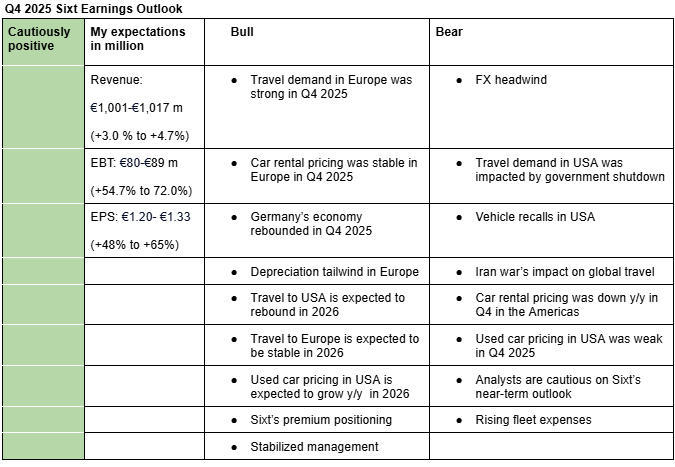

I am cautiously positive on Sixt’s Q4 2025 earnings. My estimates (Sixt’s Valuation Model – Google Sheets) incorporate resilient travel demand in Europe, the impact of the U.S. government shutdown on the car rental market, FX headwinds, pricing trends, Sixt’s premium positioning, e.t.c. However, given continued macro and demand headwinds in the U.S., I currently rate the shares as Hold. Overall, I think the current EPS growth rate (compared to P/E) is minimal to warrant a Buy rating. Here is a description of my bullish and bearish points.

Bullish arguments

Travel demand in Europe was strong in Q4 2025: According to air travel data from IATA, ACI and projections by the European Travel Commission, air travel in Europe remained strong during the quarter. For instance, according to ACI, passenger airport traffic in Europe rose 6.1% y/y in Q4 2025, a sequential improvement from the 3.9% growth witnessed in Q3 2025 (Insights on travel demand-Google Sheets). Similarly, Sunny Cars (a European Car rental company), saw the highest bookings in history during the November 2025-January 2026 quarter (Q4 2025 Sixt Earnings-Notion).

Car rental pricing was stable in Europe in Q4 2025: Sunny Cars said their average price for a rental car rose to €446 per booking in the first quarter (November 2025-January 2026) from €437 in the previous year (Q4 2025 Sixt Earnings-Notion). Similarly, Rental car prices were about 17.4% higher than a year ago during the December holidays in Germany, according to billiger-mietwagen.de (Q4 2025 Sixt Earnings-Notion). Avis and Hertz also witnessed international pricing growth of 11% and 1% y/y, respectively in Q4 2025 (Q4 2025 Sixt Earnings-Notion).

Germany’s economy rebounded in Q4 2025: Germany’s GDP rose 0.3% q/q in Q4 2025 compared to flat growth in Q3 2025 (Forum post). Sixt’s German revenue had started to witness a rebound in Q3 2025 and the positive development in Germany’s economy in Q4 2025 supports further improvement (Sixt’s Valuation Model-Google Sheets).

Depreciation tailwind in Europe: Sixt completed the sale of vehicles that were impacted by weak used car prices in Q1 2025 (forum), hence I expect depreciation of rental vehicles in the region to decline further.

Travel to USA is expected to rebound in 2026: European Travel Commission forecasts Americas inbound passenger travel will grow 4.6% y/y in 2026, up from around 1.9% in 2025 (Insights on travel demand-Google Sheets).

Travel to Europe is expected to be stable in 2026: European Travel Commission forecasts Europe inbound passenger travel will grow 6.2% y/y in 2026, up from around 5.2% in 2025 (Insights on travel demand-Google Sheets).

Used car pricing in USA is expected to grow in 2026: There was weakness in used car pices in USA in Q4 2025. Not seasonally adjusted (NSA) Manheim Used Vehicle Value Index fell 3.7%, 0.3% and 0.4% m/m in October, November and December respectively (Forum Post). However, Avis and Hertz are starting to see improvements and Manheim used vehicle value index is expected to end the year roughly 2% higher than in December 2025 (Q4 2025 Sixt Earnings-Notion).

Sixt’s premium positioning: Sixt’s 57% share of premium vehicles could help it withstand some macro pressures better than Avis and Hertz (forum). For instance, according to Advito Global Air Price Index, air prices for business class developed better than that of economy in North America in Q4 2025 (-1% versus -3% for intercontinental and +5% versus +4% for domestic and regional) (Q4 2025 Sixt Earnings-Notion).

Stabilized management: Sixt’s management has stabilized, with high executive turnover witnessed in 2024 and early 2025 no longer there. Also, employee reviews from German employees appear to be improving: Sixt’s management style and culture (Notion)

Bearish arguments

FX headwind: I expect FX to be the major headwind for Sixt in Q4 2025 and potentially throughout 2026 (unless Iran war continues for a while). I estimate FX headwind in the range of 7% to 9% in Q4 2025 and 9% to 11% in Q1 2026: FX Impact-Google Sheets.

Travel demand in USA was impacted by government shutdown: Avis and Hertz flagged reduced travel demand in Q4 2025 due to government shutdown. Government shutdown led to FAA flight reductions and air traffic control disruptions. Avis said commercial rental days went from mildly down in October to down 11% in November (Q4 2025 Sixt Earnings-Notion).

Vehicle recalls in USA in Q4 2025: In Q3 2025, Sixt flagged vehicle recalls in USA as one of the headwinds, citing that vehicle recalls saw a record of 8.5 million (Q3 2025 Sixt Earnings-Forum Post). Avis and Hertz recognized further recalls in Q4 2025, with Hertz booking $20 million in cost from additional fleet to compensate for the recalls (Q4 2025 Sixt Earnings-Notion).

Iran’s war impact on global travel: There have been more than 3,000 flight cancellations (forum post) affecting Middle East arline companies. Such flight cancelations and extra security checks are expected to create travel uncertainty, leading to reduced travel particularly from Asians traveling to Europe and North America. However, I expect some of the travel headwind from the war to be compensated by some improvement in USD against the Euro.

Car rental pricing was down y/y in the Americas: Avis’s Americas revenue per day (RPD) fell 4% y/y in Q4 2025 versus -3% y/y in Q3 2025 and Avis pointed out that this trend was industry-wide: Q4 2025 Sixt Earnings (Notion)

Rising fleet expenses: Sixt’s fleet expenses are growing faster than revenue, driven by repairs, maintenance and reconditioning costs (Sixt Valution Model-Google Sheets).

Analysts are catious on Sixt’s outlook: Analysts are cautious on Sixt’s outlook due to currency effects, macro slowdown in the U.S. and higher costs: Q4 2025 Sixt Earnings (Notion)

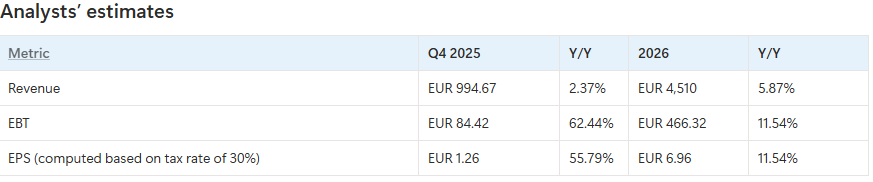

Here are analysts estimates for Q4 2025 and FY2026:

Aron’s estimates for 2026: Revenue of EUR 4,537 m (+6.3% y/y) and EBT of EUR 462 (+7.1%)

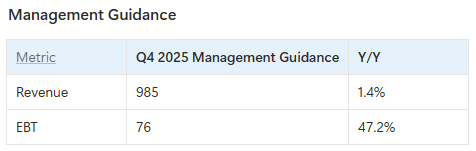

I=10 Sixt’s Q4 2025 revenue in line with estimates, EBT significantly misses estimate and 2026 guidance roughly in line with estimates

Sixt Q4 2025 (calcuated) revenue rose 4.7% y/y to €1,018 m versus management guidance of €985 m (my base estimate: €1,001 m), EBT was flat y/y at €52 m versus management guidance of €76 m (my base estimate: €80 m) while EPS was also flat y/y at €0.81 (my base estimate: €1.20).

Drivers of €28m EBT / €0.39 EPS miss versus my estimates were revenue beat (+€17m) offset by weaker other operating income (−€34m), higher personnel (−€15m) and fleet costs (−€7m), partly mitigated by lower tax (+€10m), lower depreciation (+€8m) and lower other operating expenses (+€4m).

Sixt expects 2026 revenue to grow by 4% to 7.5% to €4,450-4,600 m (midpoint: €4,525 m) and EBT margin of around 10% versus my base revenue estimate of €4,537 and EBT of €462.

Sixt revenue from Germany rose 7.4% y/y to €300 m (base estimate: €286 m), revenue from Europe rose 8.7% to €387 m ( base estimate: 395 m), revenue from North America fell 1.7% to €331 m (base estimate: €321 m)

In the Investor Presentation, Sixt pointed out that personnel costs growth rate benefited from digitalization and cost control but flagged very high car-related (repairs and maintenance inflation as a reason for growing fleet expenses.

Sixt shares rose as high as 5% following the release of the results and are now up 2.8%.

Assessment

I am starting to grow more bullish again on Sixt given the stronger than expected rebound in Germany revenue, commentaries on costs which make me think that costs might come down in future, management’s guidance which seems conservative to me given business trends in 2026 seem better than in 2025 and business performance in Q4 which was stable or even better (when you exclude other operating income which is highly volatile). See more of my assessment in Notion: Post-earnings assessment and recommendation (Notion)

I=5 Analysts mostly positive on Sixt after earnings

Hold, €83: Berenberg analyst Yasmin Steilen considers the strong reaction in Sixt shares excessive given the cautious tone of the conference call, adding that a stable pre-tax margin is likely the most realistic scenario in 2026.

Buy, €85: Deutsche Bank analyst Michael Kuhn said Sixt performed solidly, but offered few surprises.

Buy, €95->€90: DZ Bank analyst Dirk Schlamp said Sixt presented a robust picture despite a challenging environment, adding that the guidance for 2026 signals continuation of profitable growth.

Buy, €92: UBS analyst Zehua Jiang said Sixt shares are currently attractive given P/E of around 9 (below historical avarage of 15) and dividend yield of more than 5%.