Sixt’s Q3 2025 revenue and earnings topped analysts’ expectations, management revised 2025 guidance downwards

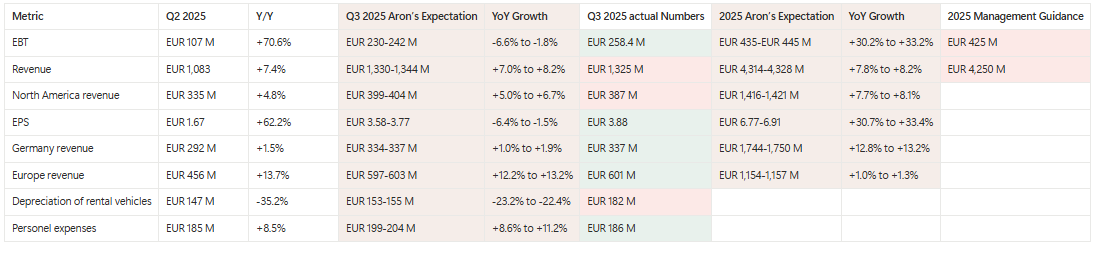

- Sixt Q3 2025 revenue rose 6.6% y/y to EUR 1,325 million (analysts’ estimate: EUR 1,317 million), EBT rose 4.9% y/y to EUR 258.4 (analysts estimate: EUR 227 million) while EPS came in at EUR 3.88 (calculated in Valuation Model-Google Sheet) versus analysts estimate of EUR 3.53 (Notion-Q3 analysts estimate).

- Sixt now expects 2025 revenue to grow 6% y/y to EUR 4,250 million (previous guidance: EUR 4,202-4,404 million (+5% to +10%) ) and EBT margin of 10%-unchanged from previous guidance.

- Sixt revenue from Germany rose 1.8% y/y to EUR 337 million, revenue from Europe rose 12.9% to EUR 601 million, revenue from North America rose 2% (up 6.6% FX-neutral (page 1 Q3 2025 report) to EUR 387 million.

- Sixt pointed to weak macro sentiment in USA as a reason for slow growth in North America revenue, citing that the government shutdown is expected to cost USD 4.1 billion in travel spending (page 5 of Q3 2025 presentation).

- Sixt also flagged vehicle recalls in USA, citing that vehicle recalls saw a record of 8.5 million in Q3 205 (page 5 of Q3 2025 presentation).

- Sixt said it launched a rewards program in USA in October 2025 and plan to expand it across its corporate countries in 2026 (page 8 of Q3 2025 presentation).

- EBITDA was flat y/y at EUR 542 million, largely driven by higher short-term leasing costs (increase of EUR 15 M) and airport commissions (increase of EUR 14 M) (page 12 of Q3 2025 presentation).

- CFO Weinberger said Sixt’s business remains robust and sees no reason why the company should deviate from its strong profitability.

- When asked about its German competitor Starcar which recently filed for bankruptcy (and searching for an investor), CFO Weinberger pointed Sixt’s own financial strength, including the recent expanded debt facility.

- Starcar has about 1,100 employees, generated a revenue of EUR 511 million in 2024 (+49% y/y) but had a syndicated loan facility of up to EUR 240 million, which was subject to very strict covenants and secured by transfer of vehicles ownership.

Assessment

Sixt shares shed around 3% yesterday and are down 2% today probably due to the reduced guidance for 2025.

While revenue growth rate for Europe and Germany were in line with my expectations, revenue growth rate for North America was significantly below my expectation (Notion-Q3 2025 earnings).

Sixt’s depreciation decline rate was also slower than I expected, probably due to the impact of the huge vehicle recalls in the USA as seen by a 7% rise in depreciation of rental vehicles in North America (Valuation Model-Google Sheets).

While performance in North America makes sense due to the reduced consumer sentiment as a result of government shutdown makes sense, rising other operating expenses is concerning as it may signal return on leased vehicles is low (I will look more into this). However, I like that its revenue per vehicle per month is growing, up 1.5% in 9M 2025 versus flat growth in 9M 2024-indicating that the company’s strategy to keep tight flight is working (Valuation Model-Google Sheet)

Overall, I think Sixt is doing well. However, a deep understanding of its Balance Sheet and Cash Flows, especially as 2025 is another heavy infleeting year following the strong defleeting in 2024 and rising debt-up 16% to EUR 3.2 billion at the end of September 2025 (Valuation Model-Google Sheet)