Solid Meta Platforms earnings outlook tempered by rising Capex

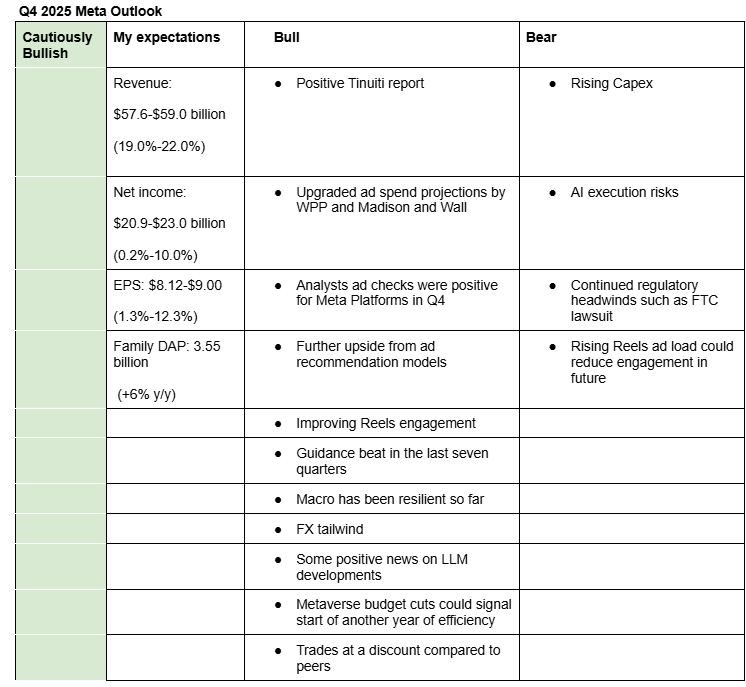

I am cautiously bullish on Meta’s Q4 2025 earnings. While I expect solid results, I believe commentary on AI investments will carry the day. My expectations (Meta Valuation Model (Google Sheets)) are based on positive Tinuiti report, upgraded ad spend forecasts, continued gains from Meta’s AI-driven ad models, and Meta’s consistent guidance beats over the past seven quarters.

Here is a description of by bullish and bearish arguments:

Bullish arguments

- Positive Tinuiti report: According to Tinuiti (forum post), which has been consistently reliable in predicting Meta’s revenue performance, ad spend on Meta Platforms by Tinuiti advertisers rose 9.7% y/y in Q4 2025. Based on this report, Meta’s Q4 revenue could grow by at least 19% y/y.

- Upgraded ad spend projections by WPP and Madison and Wall: WPP raised their global ad spend growth rate forecast for 2025 to 8.8% in December from 6% in June (forum post). It also forecasts global ad spend to grow 7.1% in 2026, up from 6.1% predicted in June. Similarly, Madison & Wall recently increased its 2025 U.S. ad spend forecast to 11% from 3.6% previously (forum post). Additionally, Guideline’s U.S. digital standard media index (SMI), which tracks actual ad spend shows U.S. digital ad spend rose 10.8% y/y in November and 12.3% y/y in October (forum post).

- Analysts ad checks were positive for Meta Platforms in Q4: RBC, Piper Sandler, UBS and Wedbush analysts have pointed out that their ad checks were positive for Meta Platforms in Q4 2025 (Q4 2025 Meta Platforms Earnings (Notion)).

- Further upside from ad recommendation models: Meta Platforms continue to make progress in making its ad recommendation models (Andromeda, GEM, Lattice) more efficient. For instance, in Q3 2025 they piloted a new ad rankings model that’s more efficient in selecting relevant ads. Meta CFO Susan Li also pointed out that even small improvements in these models result in a meaningful increase in ad revenue (Q3 2025 Meta Platforms Earnings (Notion)).

- Improving Reels Engagement: According to a recent Sensor Tower report, Instagram Reels and Facebook Reels are gaining share of time spent faster than TikTok or YouTube Shorts. Given that Reels are addictive, ads monetization should continue gaining from its usage (forum post).

- Guidance beat in the last seven quarters: Meta Platforms has beaten management’s mid-point revenue guidance by an average of 4% in the most recent seven quarters. Similarly, it has beaten management’s upper-point revenue guidance by an average of 2% in the most recent four quarters (Meta Platforms Google Sheets).

- Macro has been resilient so far: Based on expert commentaries, U.S. macro conditions have been resilient so far (forum post). This is positive to Meta given advertising spend is highly dependent on macro conditions.

- FX tailwind: I expect Meta Platforms to benefit from further strengthening of the Euro against the dollar. Chinese Yuan also strengthened during the quarter. Management expects FX tailwind of 1% but my expectations is that it could even by up to 1.9% (Meta Platforms Google Sheets).

- Some positive news on LLMs: There have been positive news recently on Meta’s LLMs. For instance, its CTO said the other day that Meta’s Superintelligence Lab has delivered the first models internally and they are “very good” (forum post). Small models released also received great reviews despite FAIR, the unit developing them seeing high executive turnover (Meta AI Releases (Notion)).

- Metaverse budget cuts could signal start of another year of efficiency: Meta Platforms recently laid off 10% of Reality Labs jobs (1500 employees) and announced that it was shifting investments to wearables and AI glasses (forum post). While this may not lead to material cost-savings, it may signal that management is now focusing on high return on investments (ROI) projects.

- Trades at a discount compared to peers: Meta shares currently trade at a P/E (next twelve months) of around 22, which is significantly lower than that of peers (e.g. Alphabet has Next twelve months P/E of 30.9 (Meta Platforms Google Sheets). This may signal that a number of risks mentioned below are now priced in.

Bearish arguments

- Rising Capex: Zuckerberg’s recent announcement that they plan to build hundreds of gigawatts of data centers over time goes against my earlier assumption that their AI investment levels could start to come down from 2028. Also, based on their past AI announcements (Meta Platforms Key Capex Announcements (Notion)), their Capex needs seem to be growing every quarter, signaling that they could raise their projections further next week. Based on my earlier assumption that Capex will come down from 2028, my base intrinsic value estimate for Meta is $654 (Meta Platforms (Notion)). If Capex continue to rise instead, then the base intrinsic value will come down to $500-$600. Therefore, I view capex spend as the greatest risk currently impacting Meta Platforms shares.

- AI execution risks: While we are starting to hear positive reports on the execution of MSL (as mentioned above), LLMs performance are rapidly evolving (i.e. Google and OpenAI continue to execute well) making it hard for Meta Platforms to catch up. Therefore, Meta’s upcoming LLMs should be really good for the company to convince the market.

- Continued regulatory headwinds such as FTC: In my opinion, Meta shares didn’t react much after the company won the FTC trial over its acquisition of Instagram and Facebook, probably because the market expected the FTC to appeal the case (forum post). Therefore, the FTC case is likely to continue being a drag on Meta Platforms shares. Meta is also facing other regulatory headwinds such as countries starting to ban social media usage by teenagers (forum post) and youth-related class action lawsuits (forum post).

- Rising reels ad loads could reduce engagement in future: I have noticed a rise in the number of ads in both Instagram and Facebook. Meta Platforms may be trying to extract as much revenue from Reels as possible to fund its AI investments (theory). If this trend continues, users may limit their usage of Instagram and Facebook as these ads can be boring.

Management guidance and analysts' estimates:

Management Guidance for Q4 (Revenue): $56.0-$59.0 billion (+15.7% to +21.9%)

Analysts’ Estimate for Q4 (Revenue): $58.4 billion (+20.6%)

Analysts’ Estimate for Q4 (EPS): $8.18 (+2.0%)

Analysts’ Estimate for Q1 2026 (Revenue): $51.3 billion (+21.3%)

Analysts’ Estimate for Q1 2026 (EPS): $6.36 (-1.0%)

Recommendation

Given that Meta Platforms is currently trading at $648, close to my base intrinsic value estimate of $654, and considering the risk that future cash flows could be further pressured by rising capex, I am recommending a Hold rating.

If the share price were to decline to around $500, I would upgrade the rating to Buy. Conversely, if management were to signal a significant increase in capex, I would consider recommending profit-taking.