This topic covers Bumble’s Q4 2025 earnings. A preview of the results will be posted here. For the full earnings preview and earnings call summary, see the Notion:

Earnings date: March 11, 2026

Time of Earnings release: 4:00 PM ET

Time of Analysts Call: 4:30 p.m. ET

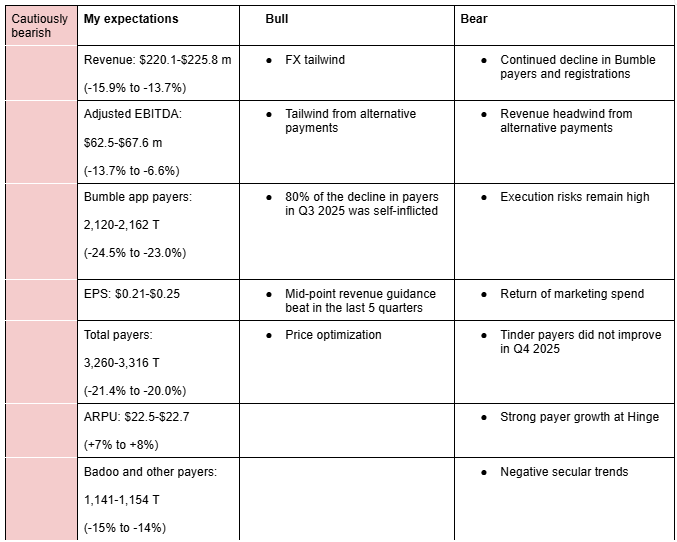

While I expect Bumble’s Q4 2025 earnings to come close to consensus estimates and management’s guidance, I remain cautious on the 2026 outlook. There is a material risk that management’s 2026 guidance could come in below my current estimates. My estimates (Valuation Model (Google Sheets)) above take into account FX tailwind, continued decline in payers, tailwinds and headwinds from alternative payment system, and the fact that revenue has exceeded management’s mid-point guidance in the last five quarters. Here is a description of my bullish and bearish sentiments:

Bullish

FX tailwind: The USD continues to weaken against major foreign currencies associated with Bumble such as Euro and the Pound. As a result, I expect FX tailwind of around 3.5% and 5% in Q4 2025 and Q1 2026, respectively. This is higher than the FX tailwind of 1.62% reported in Q3 2025: Bumble Fx Estimates (Google Sheets).

Tailwind from alternative payments: I expect cost of revenue in Q4 2025 and 2026 to benefit from alternative payments (web payments) launched in Q2 2025. I estimate web payments will reduce cost of revenue by around $7.5 million in Q4 2025 and Q1 2026 or around 3.5% of total revenue: Tailwind from alternative billing system (Notion).

80% of the decline in payers in Q3 2025 was self-inflicted: The fact that 80% of the 18.3% decline in payers in Q3 2025 was self-inflicted through trust and safety measures and reduction in marketing spend gives me some confidence that Bumble’s Q4 2025 revenue could come in line with management guidance as management has control over those factors: Q3 2025 Bumble Earnings (Notion).

Mid-point revenue guidance beat in the last 5 quarters: Bumble has exceeded the mid-point of management’s revenue guidance by an average of 1.7% in the most recent five quarters. Additionally, it has execeeded the mid-point of management’s adjusted EBITDA guidance by an average of 3.9% in the most recent six quarters: Bumble guidance versus actuals (Google Sheets).

Price optimization: Bumble’s average revenue per user (ARPU) rose 1.5% in Q2 2025 and 6.6% in Q3 2025 due to optimization of pricing in lower-monetizing regions (Bumble Valuation Model (Google Sheets)). I expect this strategy to also play out again in Q4 2025, a trend also observed in Match Group (Match Group Valuation Model (Google Sheets)).

Bearish

Continued decline in payers and new registrations: Bumble doesn’t expect sequential decline in payers to improve until early 2026. However, they don’t expect marketing spend to go back to historicals levels (Q3 2025 Bumble Earnings (Notion)). Third-parties such as Sensor Tower also indicate that Bumble app downloads in the U.S. was down 50% versus -29% for Tinder in Q4 2025. These factors signal that usage of Bumble in 2026 may not improve (Dating apps user trends (Google Sheets)).

Revenue headwind from alternative payments: Bumble is giving users discounts of around 10% to encourage them to use web payments, causing an headwind to revenue. I estimate a revenue headwind of around 2% in Q4 2025 and Q1 2026: Tailwind from alternative billing system (Notion).

Execution risks remain high: I am cautious on CEO Wolfe Herd’s ability to turn around the company given her past success was not entirely hers- Badoo founder had played a major role (Assessment of Wolfe Herd (Notion)). Similarly, recent departure of Bumble’s Chief Product Officer may signal execution was not going on well (forum post).

Tinder payers did not improve in Q4 2025: The decline in Tinder payers accelerated further in Q4 2025. Tinder payers fell 8% y/y in Q4 2025 versus a decline of 6.9% in Q3 2025. Tinder MAUs did not see any improvement as well, declining by 9% y/y in Q4 2025 versus a decline of 9%-10% in Q3 2025: Match Group Quarterly Results (Google Sheets)

Strong payer growth at Hinge: Hinge is Bumble’s fiercest competitor and its strong performance amidst weakness at Bumble may signal that it’s taking market share. Hinge’s payers rose 16.5% y/y in Q4 2025 versus growth of 16.9% in Q3 2025: Match Group Quarterly Results (Google Sheets)

Negative secular trends: Dating apps such as Bumble and Tinder continue to lose users due to a combination of swipe fatigue, Gen Z’s need for authenticity and privacy, e.t.c. The trend could continue until better AI match-making features come into force, probably after the second half of 2026: Bumble Market (Notion)

Here are management and analysts estimates for Q4 2025 and Q1 2026:

Q4 2025 management guidance for revenue: $216-$224 million (-17.4% to -14.4%).

Q4 2025 management guidance for adjusted EBITDA: $61-$65 million (-15.9% to 10.4%).

Q4 2025 consensus analysts estimate for revenue: $221.5 million (-15.6%).

Q4 2025 consensus analysts estimate for EPS: $0.23

Q1 2026 analysts estimate for revenue: $210.7 million (-14.7%)

Q1 2026 analysts estimate for EPS: $0.20

Q1 2026 Aron’s estimate for revenue: $212.8-$216.7 million (-13.8% to -12.3%)

Q1 2026 Aron’s estimate for EPS: $0.16-$0.21

Q1 2026 Aron’s estimate for Adjusted EBITDA: $49.4-$55.1 million (-23.3% to -14.4%)

Recommendation

Given the risks discussed above, I recommend staying on the sidelines until management demonstrates tangible execution progress and payer/active user trends show sustained stabilization or improvement.

Note: I may update my projections and rating before the earnings if I encounter new insights on user trends or management’s execution.

Analysts are divided following Bumble’s Q4 2025 earnings

In Line, $5:00: Evercore expects customer acquisition investment to rise significantly alongside product refresh, causing uncertainty on 2026 forecasts. It expects gross margin to continue to rise on direct billings. It’s monitoring for an inflection in user and payer growth as product innovation rolls out and evidence that profitability from gains from sales and marketing and direct billings is sustainable.

Underperform, $3.50→$3.30: BofA cited declining revenue growth, limited medium-term visibility, and soft dating industry trends.

Equal Weight, $5.50→ $5.00: Wells Fargo sees increased focus on new product launches and marketing spend as potential drivers for revenue growth in 2027. Wells Fargo expects improving Bumble app payer declines in the first quarter 2026 with a decline of 125,000 quarter-over-quarter versus a decline of 159,000 in the fourth quarter.

Underweight→ Neutral: JPMorgan said Bumble pointed out that the heavy lift from its member quality reset was behind the company. Bumble app registrations and active users are stable year-to-date and net add trends expected to improve going forward.

Equal Weight, $3.50→$4.00: Morgan Stanley analyst Nathan Feather said Bumble app registrations and active users have started to stabilize and financials “seem to be reaching a trough,”.

Neutral, $3.80→$3.90: Citi saidBumble’s Q4 results and Q1 outlook were better than expected. It cites Bumble’s improved paying user trends for the target bump.