This topic discusses Match Group’s Q2 2025 earnings. A preview of the earnings results will be published here. You can find a full summary of the earnings preview and results in the wiki:

Earnings date: August 5, 2025

Time of Earnings release: 4:00 PM ET

Time of Analysts Call: 5:00 p.m. ET

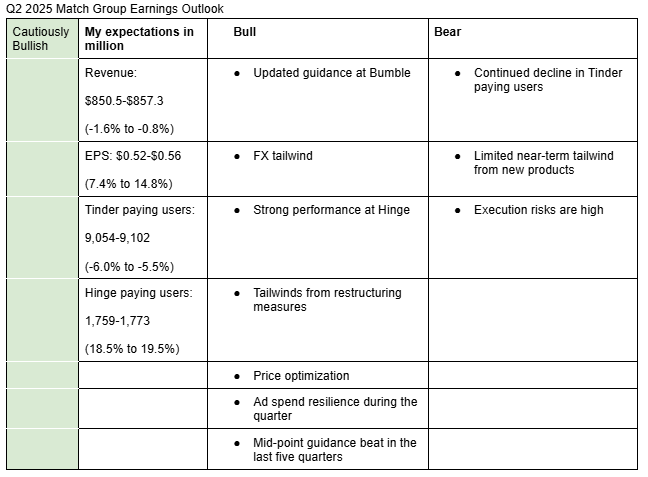

I am cautiously bullish on Match Group’s Q2 2025 earnings. My estimates take into account continued decline in Tinder paying users, strong performance at Hinge, FX tailwind, raised guidance at Bumble, resilient ad market during the quarter, and revenue guidance beat in the last five quarters.

Here is a description of by bullish and bearish sentiments:

Bullish arguments:

Updated guidance at Bumble: On June 23, 2025, Bumble raised its Q2 2025 revenue guidance to a range of $244 million to $249 million, up from its prior range of $235 million to $243 million, signaling improved business prospects during the quarter.

FX tailwind: Match Group generates more than 55% of its revenue outside the U.S. As a result, the recent strengthening of foreign currencies against the U.S. dollar should provide a tailwind in Q2. Management has guided for a 1% FX tailwind this quarter. However, it has a history of misestimating FX impact; in Q1 2025, it overestimated the FX headwind by 20%. Given this pattern, I expect the actual FX tailwind in Q2 to come in slightly above the 1% estimate.

Tailwinds from restructuring measures: New CEO Spencer Rascoff has centralized some functions and reduced the workforce by 13%. Management expects these changes to generate $45 million in cost savings in 2025 and $100 million annually starting in 2026.

Strong performance at Hinge: Hinge continues to deliver strong performance, with its revenue growth largely offsetting the decline in Tinder’s revenue.

Price optimization: During the Q1 2025 earnings, Match Group management stated that they would raise prices if certain factors negatively impact operating performance. This suggests they still see room to increase prices without triggering significant user churn.

Ad spend resilience during the quarter: Q1 2025 indirect revenue rose 30% due to strong spend by Match Group’s advertisers. While management noted that they don’t expect this trend to continue in the coming quarters, insights suggest that ad spend remained resilient during Q2.

Mid-point guidance beat in the last five quarters: Match Group has beaten its midpoint and lower-point guidance by an average of 0.13% and 0.72% respectively in the most recent five quarters.

Bearish arguments:

Continued decline in Tinder users: Tinder continues to lose paying users due to a combination of product fatigue, shifting user preferences, and competitive pressure. Management does not expect this trend to reverse until new product initiatives begin gaining traction.

Limited near-term tailwind from new products: In my view, the benefits of Match Group’s AI-driven product strategy are unlikely to materialize meaningfully before 2026. This view is supported by a recent Bloomberg Intelligence survey, which found that the company’s AI features have yet to resonate with Gen Z.

Execution risks are high: Rascoff is new in the role. The organizational changes he has implemented may take time to pay off and could cause internal friction.

Here are management’s and analysts’ expectations for Q2 2025;

Management Guidance for Q2 (Revenue): $850 million to $860 million (-1.6% to -0.5%) Management Guidance for Q2 (adjusted operating income): $295 million to $300 million (-3.7% to -2.1%) Analysts’ Estimate for Q2 (Revenue): $854.5 millionn (-1.1%) Analysts’ Estimate for Q2 (EPS): $0.58 (+20.8%)

Recommendation

Given the execution risks surrounding Match Group’s turnaround and the continued decline in Tinder’s paying users, I have a Hold rating on the stock. In the upcoming earnings call, I’ll be watching closely for updates on the product offensive, trends in Tinder’s payer base, and early signals from Rascoff’s restructuring efforts.

Can you remind me what the significance of advertising is for the match group and link to the relevant section in which you investigate that topic in Notion?

Advertising plays a relatively small role in Match Group’s overall business model. In 2024, it accounted for approximately 2% ($61 million) of total revenue.

Match Group Beats Q2 Revenue Expectations; Guides Q3 and 2025 Revenue Above Consensus, AOI Below Estimates

Match Group’s Q2 2025 revenue was flat year-over-year at $864 million, exceeding the upper end of management’s guidance of $860 million and beating analysts’ estimate of $854.48 million.

Adjusted operating income (AOI) declined 5% y/y to $290 million, below management’s guidance of between $295 million and $300 million. Excluding legal settlement charge of $14 million, AOI exceeded the guidance.

Match Group is guiding Q3 2025 revenue in the range of $910 to $920 million, up 2% to 3% (analysts’ estimate: $889.91 million) and AOI in the range of $330 to $335 million, down 3% y/y (analysts estimate: $336 million).

It plans to reinvest cost savings of approximately $50 million in the second half of 2025 towards marketing and product testing at Tinder, Hinge and other early-stage bets like Archer and Her.

Match Group now expects full year total revenue to be near the high end of the earlier guidance range ($3,375 million-$3,500 million) due to positive FX impacts and AOI margin of 35.4% lowered from at least 36.5% due to restructuring costs and the $14 million legal settlement charge.

Here are my main takeaways from the earnings call;

The product offensive has strengthened compared to Q1, particularly at Tinder. Rascoff noted that the new “Double Date” feature is showing strong product–market fit. He also highlighted upcoming college-specific features, as well as positive momentum and outcomes from recent trust and safety initiatives. He added that they now ship new code every week instead of every two weeks.

Rascoff said all tracked user metrics have improved compared to a few months ago, but acknowledged that year-over-year declines persist, though the rate of decline has moderated.

Rascoff praised Hinge’s team, saying they are using Hinge’s formula to turn around Tinder.

“Hinge is firing on all cylinders. I mean it’s got a really impressive and distinctive company culture, very highly engaged employees, shipping innovative products. They’ve got a terrific brand and a clear product strategy and they understand their users incredibly well and what users want from them. And the last compliment I’ll pay is that more than any of our other brands, they’ve infused AI into the product at an even greater rate than others, and it really shows.”

CFO Bailey said they are testing alternative payment systems across the brands, which could lead to $65 million AOI savings opportunity in 2026. The 2025 savings (mainly in second half) from this alternative payment system are not included in the guidance.

Bailey said they are feeling a lot better about macro in general compared to last quarter.

“But I think at the highest level, we feel much better about the macro environment and impacts on our business than we did a quarter ago. We’re not really seeing it aside from some small pressure at Tinder that we mentioned last call,” he said.

Rascoff said they are not planning to increase price as a result of early product success at Tinder since they are prioritizing the recommendation algorithm more towards user outcome and less towards revenue.

Assessment

Overall, Rascoff’s tone sounded more confident regarding the product momentum and outcome than in the previous call. Analysts acknowledged the early success when asking questions.

Analysts cite early signs of progress at Match Group, but caution recovery Will take time

Outperform, $39->$42: Wolfe Research said it’s not seeing a complete turnaround in top-of-the-funnel metrics yet but cited “green shoots” in the company’s operating performance, especially improving MAU trends, accelerating product changes and improved marketing strategy. They believe current valuation remains attractive.

Outperform, $35->$39: RPC pointed out that while full recovery signals might be several quarters away, management’s current approach represents an improvement. They highlighted three positive factors which include marginally promising new products, product roadmap compared to last quarter, and Hinge’s outperformance.

Neutral, $28->$35: JPMorgan believes Tinder is moving in the right direction after the company reported Q2 2025 results.

Buy, $39->$42: Goldman Sachs cited positive signs around registrations and user outcomes. It added that Match Group maintains strong financial health, with current ratio of 1.62.

In Line, $32->$38: Evercore highlighted encouraging progress on Tinder’s top-of-funnel metrics, improved product development velocity, and comments on alternative payment solutions. It added that Match Group’s financial health appears solid, with liquid assets above short-term obligations. The neutral rating reflects lack of evidence for sustained improvement in user acquisition trends despite improved execution speed since management transition in February.

M Science analyst Chandler Willison said they are starting to see early benefits from Match Group’s AI initiatives.

“We’re starting to see some of the early benefits from Match Group’s AI initiatives. And improvements in recommendations and other aspects of user interaction,” said M Science analyst Chandler Willison.