This topic covers Bumble’s Q2 2025 earnings. A preview of the results will be posted here. For the full earnings preview and results summary, see the wiki:

Earnings date: August 6, 2025

Time of Earnings release: 4:00 PM ET

Time of Analysts Call: 4:30 p.m. ET

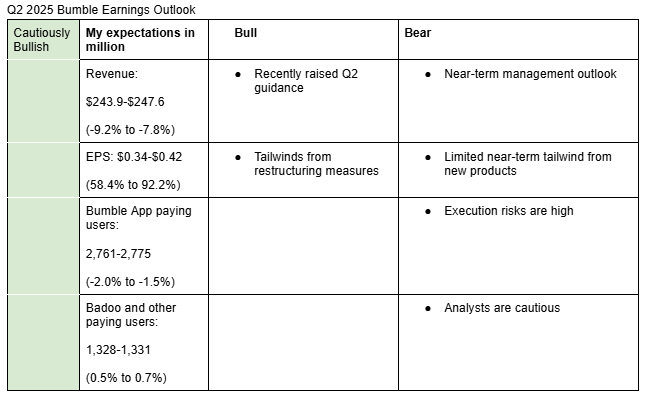

I am cautiously bullish on Bumble’s Q2 2025 earnings. My estimates are mainly based recent user and pricing trends and recent management guidance. Here is a description of my bullish and bearish sentiments:

Bullish

Recently raised Q2 guidance: On June 23, 2025, Bumble raised its Q2 2025 revenue guidance to a range of $244 million to $249 million, up from its prior range of $235 million to $243 million. Management also raised adjusted EBITDA guidance for Q2 to a range or $88 million to $93 million from the range of $79 million to $84 million. Given that the company likely had visibility into most of its Q2 operating metrics by that date, there is a strong likelihood that actual results will fall within the updated guidance range.

Tailwind from restructuring measures: Bumble expects cost savings from its restructuring measures to accrue in the near term. For example, during its Q1 2025 earnings call, the company stated that it had identified $20 million in marketing cost savings for Q2 2025. Additionally, the 13% workforce reduction is expected to generate annual savings of $40 million, beginning as early as the second half of 2025.

Bearish

Near-term management outlook: Bumble’s management expects their focus on the turnaround to lead to fewer users in the near-term.

Limited near-term tailwind from new products: A recent Bloomberg Intelligence survey found that AI features launched by Bumble and Match Group have yet to resonate with Gen Z. As such, it could take a while for Bumble’s AI products to improve the quality of the platform.

Execution risks are high: The restructuring measures being introduced by its new CEO Whitney Wolfe Herd could take a while to materialize, leading to volatility in key operating performance metrics.

Analysts are cautious: Morgan Stanley, Wells Fargo, and Citi analysts welcomed the restructuring measures but cautioned that it could take a while for the turnaround to materialize.

Bumble topped Q2 revenue and adjusted EBITDA estimates; Q3 guidance for both metrics (midpoint) is above consensus

Bumble Q2 2025 revenue fell 7.6% y/y to $248.2 million, above analysts estimate of $245.65 million and in line with management’s upper point guidance of $249 million while adjusted EBITDA was $94.6 million, above analysts estimate of $87.15 million.

Diluted EPS was -$2.45, significantly below estimate of $0.34 and Q2 2024 EPS of $0.22. However, excluding impairment loss of $404.8 million and restructuring costs of $12.2 million, diluted EPS was up 42% y/y to $0.33 (calculated).

Bumble guided Q3 2025 revenue in the range of $240 million to $248 million (analysts estimate: $241.72 million) and adjusted EBITDA in the range of $79 million to $84 million (analysts estimate: $76.16 million).

Total paying users fell 8.7% y/y to 3.78 million while total average revenue per paying user (ARPU) rose 1.5% y/y to $21.69 driven by ARPU at Bumble app which rose 4.1% y/y to $26.85.

Bumble recognized non-cash impairment charge of $398.1 million in Q2 associated with their strategic shift to improve the health of their membership base.

Bumble shares fell around 7% in the after-market trading, probably due to the sharp drop in the number of paying users.

Buy, $7->$7.5: RBC said they are not overly optimistic on the industry, adding that sentiment is already anemic.

Peerperform: Wolfe Research pointed out that Bumble’s continued clean-up of payers is inhibiting additional confidence on its near-to-mid-term growth trajectory. It acknowledged that the cleanup process could have positive long-term impacts on user engagement and monetization. Wolfe added that savings from in-app purchase saving fees could lead to earnings upside.

Market Perform: Raymond James noted that investors might remain on the sidelines until there is evidence that the strategic shifts at Bumble are resonating with users.

Here are my main takeaways from the earnings call;

The 8.7% y/y decline in payer users was mainly driven by the end of legacy promotions in lower-monetizing regions.

“The majority of this quarter’s payer decline came from the phase out of a legacy strategy related to promotions, which were skewed towards certain of our lower monetizing noncore markets. As of late April, we have been reemphasizing our core of sustainable full-price subscriptions,” CEO Whitney Wolfe said.

Bumble is assessing payer quality through its Beehive Fit Framework, which classifies daters into three groups: approve (high-quality daters), improve (daters showing effort to enhance their profiles), and remove (low-quality users who make no effort to improve and should be removed).

Improve users account for the largest number of payers while remove users make up less than 10% of total payers.

CFO Ronald Fior said trust and safety features they are rolling out will have a negative impact on revenue in Q3 and greater impact in Q4.

Assessment

The payer decline in Q2 was largely due to ending promotions in lower-monetizing regions, suggesting further pressure on payer counts ahead as Bumble prioritizes improving platform quality over short-term growth.

While Bumble will roll out several new features this month, Match Group has already launched multiple products with early performance data, underscoring that Bumble is trailing in execution speed (Q2 2025 Match Group Earnings Call Summary).

Overall, Bumble’s call felt less upbeat than Match Group’s. Match’s update was anchored in tangible product launches and measurable engagement gains, whereas Bumble’s was more focused on strategy and commitments.

Good catch that promotions did end and that caused lower subscriber numbers. I have to admit I missed that point in the call.

I think comparing Bumble and Match Group can obviously be done but it’s important to keep in mind that they are at very different stages. Bumble is more a turnaround play as the original founder is returning after a time that feels like chaos and mismanagement while Match Group is was more stable with some one the subsidiaries like Hinge already being run very well.