This topic discusses the upcoming Q2 2023 Meta Plattform Earnings.

It will include our final assessment and decision before the earnings release, report on the results, and discuss the results including any potential changes to my position.

The work which we are doing specifically in preparation to the earnings can be found in the Wiki.

Starting Situation

Meta Platforms is my largest position by a wide margin after it’s price recently skyrocketed through the $300 mark. (More information about my current capital allocation can be found here)

It is therefore also the most important company to understand correctly and get right before the earnings as it has the strongest effect on the portfolio.

Options include holding the position or reducing it. A reduction would most likely be in the 10-35% range.

My current neutral price target is in the $325-$375 range but might be adjusted slightly or clarified based on our last-minute findings before the earnings date.

Note: Numbers are rough guestimates. I lacked the time to calculate different scenarios based on the data points that we have.

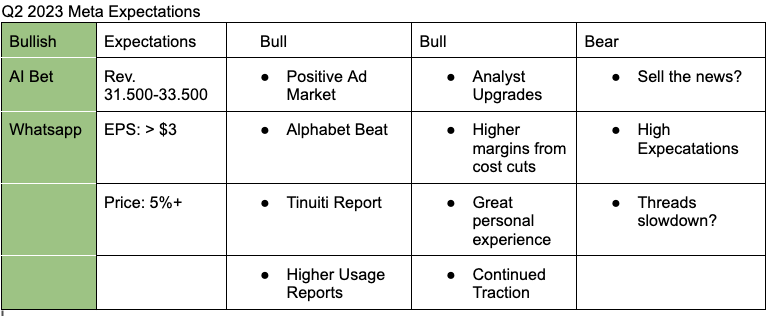

Our expectation for Q2 2023 Meta Platforms Earnings is positive.

All data points we are seeing are positive.

Social Media spending predictions have been revised up

Tinuiti reports which have been very insightful in the past, show a strong increase in Meta Platforms ad spent and strong impression gains

Alphabet had a revenue beat

Analysts cite increased reels usage and the personal reels and advertising experience stays very positive.

Additionally, there is a potential to see the first effects of cost cuts and the overall speed of iteration and improvement at the company feels strong.

On the downside, there is always a risk of a “Sell the news” event, which means people take profits even on good numbers, but I think the probability of this happening is low.

Additionally, expectations are high, but probably not high enough and there might be critical questions about Threads which slowed down significantly.

Given that Threads is not of critical importance I don’t expect this to be a risk either.

The largest risk at the moment is probably something that is not foreseen by us and we run a risk of getting complacent with so many good data points. A symptom of this is that I lacked the time to calculate different scenarios based on the numbers we have (e.g. Tinuiti report, usage, CPM, etc.) to reach higher convictions on guestimates.

Revenue grew by 11% y/y to $31.999 billion, above analysts estimate of $31.08 billion and in-line with management upper guidance of $32 billion.

EPS was $2.98, above analysts estimate of $2.91.

Operating margin was 29%, below analysts estimate of 30.4%.

Facebook daily active users(DAUs) was 2.06 billion versus 2.03 billion estimate.

Monthly active users(MAUs) was 3.03 billion versus 3 billion expected.

Average revenue per user(ARPU) was $10.63 versus $10.22 expected.

Reality labs operating losses was -$3.739 billion, above analysts estimate of $3.68 billion. Meta expects these losses to increase meaningfully y/y due to ongoing product developments in AR/VR.

Q3 revenue guidance: $32 billion-$34 billion versus $31.3 billion estimate.

FY2023 total expense guidance: Range raised to $88-91 billion from $86-90 billion due to legal-related expenses in Q2 and $4 billion restructuring costs.

FY2023 capital expenditures guidance: Range lowered to $27-30 billion from $30-33 billion due to cost savings, particularly on non-AI servers and shifts in investments to 2024.

My first impression is that I am a bit unsure if the stock can stay up after-hours given they announced plans for meaningfully increased operating losses on reality labs in 2024, as well as growing capex in 2024.

The details of the conference call are going to be interesting.

Reality Labs also comprises some of Metas AI developments and increased operating costs might be related to it.

Metas announcement of higher payroll expenses due to a higher composition toward higher-cost

technical roles might partially indicate an increased war for talents within the AI space.

I am also not sure if the rally will lose steam. Do you think that comes as a surprise? They said in Q1 earnings call that their focus is on AI and Metaverse. Also, a number of AR/VR launches are scheduled to be release by 2025. But yeah, I expect more details in the call.

Yes, I think it comes as a surprise esp. given that they declared a new focus on efficiency.

If I had to guess, I think that Mark got excited about how the rest of the business is performing and he knows that investors are less critical, so he decided to reaccelerate investments into the metaverse.

On the call, there was actually an analyst question about the ROI of the metaverse and Mark explained that he believes the metaverse can help to deepen connection so it is very aligned with the mission of Meta and it can be a profitable investment as he thinks engagement of the family of apps can increase in the metaverse as well and it is good to own the computing platform of the future.

From my perspective as a Meta Quest 2 owner I think, that it is an amazing product, but it is more complicated and exhausting to use compared to a phone which limits the usage significantly.

My main worry when it comes to the Metaverse is the technical challenge for one company to build a lot of core technology by itself, instead of having a larger industry that is evolving more naturally.

So Meta might be too ambitious and too much ahead of time in this endeavor.

Increases in cost will be partially contributed to the launch of Meta Quest 3 which will be likely heavily subsidized.

Overall the call has been interesting. Meta’s AI ambitions are very interesting and promising.

On the flipside, there will be a 3% fx tailwind from a 3% headwind in Q2. So Q3 numbers don’t look as impressive anymore considering there is 6% help which equals almost $2 billion.

I am not sure how aware investors are off this fact or will be tomorrow when the market opens.

I agree with Mark Mahaney that Meta’s Y/Y growth in Q3 will likely look very impressive.

Meta’s Q3 2022 has been particularly weak due to the impact of Apple’s privacy policy changes at $27,714 (-4% y/y)

For Q3 2023 Meta is now guiding a range of 32-34.5 billion. That’s 15.5% - 24.5% growth Y/Y. Adjusted for FX we get approx. 9.5%-18.5%.

Importantly Reels is still a headwind for Meta’s business and will turn into a tailwind towards the end of the year.

So it is probably fair to say that we are seeing Meta specific advertising strength as they successfully rebuilt their advertising technology stack and are overcoming Apple’s privacy policy challenge. (Similarly to Volkswagen we should develop an “Advertising Industry Players” article to increase our overview of how different advertising players are developing)

One could obviously argue that Metas has the easier Q3 comps. (e.g. 10% easier than Alphabet) but imo that kind of catch-up in the face of strong challenges is impressive.

Increased Reality Labs spent will be a drag for my EPS growth assumptions but will fundamentally not drastically change the investment case. (The underlying profitability of Family of Apps is important. Reality Labs spending could be reduced again in case there is no sufficient adoption of Meta Quest 3 and Apple Vision)

Overall I am continuing surfing the wave on AI adoption as I still feel comfortable with current Meta valuations and think that Meta has a chance similar to Microsoft, Nvidia, or Apple to reach new all-time highs towards the end of the year if we see no significant deterioration of the economy.

Here are additional insights from the earnings call;

34% increase in ad impressions was mostly in lower monetizing surfaces and regions leading to a 19% drop in price per ad.

Engagement and adoption of its products is strong; Reels Plays exceeded 200 billion per day and three-quarter of Meta Platforms advertisers now use Reels ads while AI recommended content drove a 7% increase in overall time spent on the platform.

Meta Platforms expects to generate some revenue by open sourcing its Llama 2 model in Microsoft Cloud and other companies.

Reels annual revenue run-rate crossed $10 billion, up from $3 billion last fall though they continue to expect monetization to develop more slowly than Feeds and Stories into the foreseable future because users scroll more slowly on Reels.

Online commerce vertical contributed the largest y/y growth to revenue due to strong spend by Chinese advertisers trying to reach new markets.