This topic covers Sixt’s Q1 2026 earnings. A preview of the results will be posted here ahead of the earnings release. A full summary of the preview is available in the Notion:

Earnings date: May 13, 2026

Time of Earnings release: 7:30 CET

Time of Analysts Call: Unknown

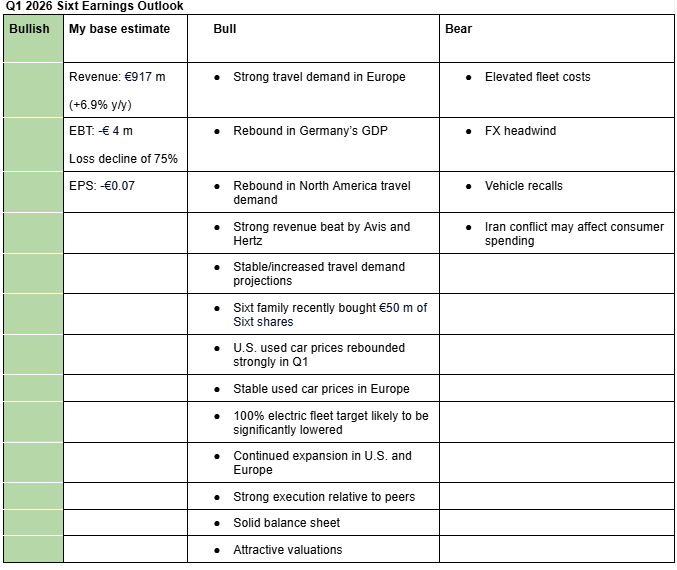

I am bullish on Sixt’s Q1 2026 earnings and on the company overall. My estimates (Sixt’s Valuation Model (Google Sheets)) incorporate strong travel demand in Europe, a rebound in Germany’s economy, recovering travel demand in North America, strong revenue beats from peers, supportive used-car prices during the quarter, a solid balance sheet, and stronger execution relative to competitors. Given expectations for strong quarterly results (or at least in-line performance) and improving sentiment, I am upgrading my rating from ‘Hold’ to ‘Buy’. That said, I aslo think Sixt might raised its guidance for the whole year. Below is a summary of my bullish and bearish arguments.

Bullish arguments

Strong travel demand in Europe: According to the International Air Transport Association (IATA), inbound travel demand in Europe was stable during the quarter compared to Q4 2025 (Travel demand insights (Google Sheets)). This supports another strong revenue growth for Sixt in the region, with Q4 2025 Europe revenue having risen by 10.6% y/y.

Rebound in Germany’s GDP: Sixt’s revenue from Germany rose by 6% y/y in Q4 2025, supported by a rebound in Germany’s GDP. Germany’s economic momentum remained resilient in Q1 2026, suggesting that the strong growth seen in Q4 could continue into the first quarter (forum post).

Rebound in North America travel demand: According to the International Air Transport Association (IATA), inbound travel demand in North America increased by an average of 2% y/y during the quarter, up from 0.8% growth in Q4 2025 (Travel demand insights (Google Sheets)). In addition, both Avis and Hertz reported revenue above analysts’ estimates, driven by strong performance in the U.S. market. Both companies also recorded their strongest pricing trends in several quarters (Q1 2026 Sixt Earnings (Notion)).

Stable/increase travel demand projections: The European Travel Commission (ETC) recently raised its growth forecast for Europe’s 2026 inbound travel demand to 7.8% from 6.2%. It also projects North America inbound travel growth of 4.2% (slightly lowered from 4.6%). For 2027, they project growth of 5% for both Europe and North America inbound travel (Travel demand insights (Google Sheets)).

Sixt family recently bought €50 m of Sixt shares: The Sixt family’s recent €50 million share purchase suggests rising confidence in the company’s operating outlook and may be interpreted by the market as a signal that the preference shares are trading below intrinsic value (forum post).

Positive used car prices: U.S. used-car prices rebounded strongly in Q1 2026, while prices in Europe remained stable. This should support Sixt’s continued decline in depreciation expenses (forum post).

100% electric fleet target likely to be significantly lowered: There are reports indicating the EU Commission plans to reduce their proposed 2030 zero-emission target for corporate fleet to 45% from 100%(forum post). This is largely positive for Sixt as it won’t have to invest in a lot of EVs whose demand has been low.

Continued expansion in Europe and USA: Sixt continues to expand in both Europe and the U.S., supporting continued high-single-digit and double-digit revenue growth in the two regions, respectively.

Strong execution relative to peers: While Avis and Hertz continue to make significant losses, Sixt is profitable (Q1 2026 Sixt Earnings (Notion)). Additionally, its recently launched Sixt ONE Loyalty program received strong reception and could help Sixt increase its retention metrics relative to competitors (forum post).

Solid balance sheet: Sixt’s financial position remains solid, supported by an equity ratio above 30%, leverage of 2.56x, and total liabilities amounting to approximately 82% of the book value of its rental vehicles (Google Sheets).

Attractive valuations: Despite Sixt’s preference shares having rallied around 14% year-to-date (YTD), its forward P/E of around 9x suggests that the valuation remains attractive.

Bearish arguments

Elavated fleet costs: This is currently one of the main headwinds facing Sixt. Fleet expenses are rising faster than revenue growth due to high maintenance, repair, and reconditioning costs. While Sixt is actively addressing the issue, a near-term resolution is unlikely (Q1 2026 Sixt Earnings (Notion)).

FX headwind: FX headwind (due to the strengthening of the Euro against USD) will also be another major headwind for Sixt in Q1 2026 and possibly throughout the remainder of the year. I estimate FX headwind of around 9% and 3% in Q1 2026 and Q2 2026, respectively (FX Impact (Google Sheets)).

Vehicle recalls: Sixt flagged U.S. vehicle recalls as one of the headwinds during the most recent earnings presentation (page 5). Vehicles recalled cannot be rented out or sold, hence impacting both revenue and depreciation. For instance, Hertz reported revenue headwind of $50 m in Q1 2026, representing 3% of its Americas revenue (Q1 2026 Sixt Earnings (Notion)).

Iran conflict may affect consumer spending: The ongoing Iran conflict poses a risk to consumer spending through higher oil prices, which increase transport and travel costs. This could weigh on discretionary travel demand.

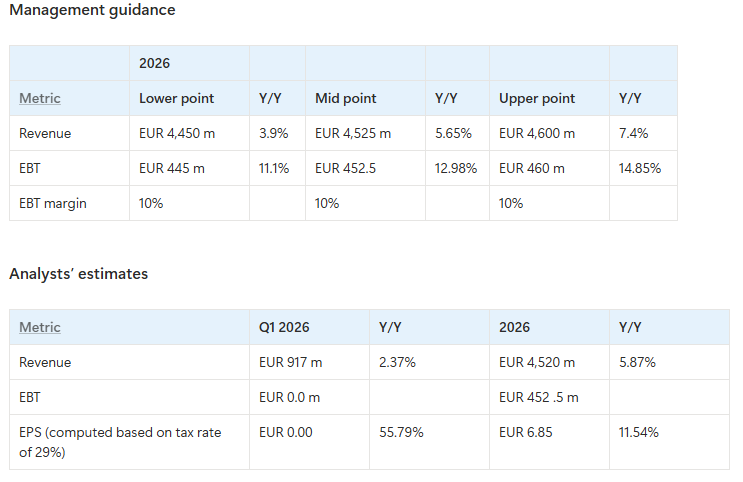

Here are analysts estimates for Q1 2026 and FY2026: Aron’s estimates for 2026 : Revenue of EUR 4,661 m (+8.8% y/y) and EBT of EUR 457(+14%)

I=10 Sixt beats revenue and earnings estimates, reaffirms 2026 guidance, but rising fleet expenses remain a major headwind to earnings upside

Sixt’s Q1 2026 revenue rose 8.3% y/y to €929 m, exceeding my estimate of €917 m, EBT came in at €2 m versus my estimate of -€4 m while EPS of €0.03 exceeded my estimate of -€0.07.

Sixt reaffirmed its 2026 guidance, expecting revenue to grow by 4% to 7.5% y/y to €4,450-4,600 m (midpoint: €4,525 m) and EBT margin of around 10% versus my base revenue estimate of €4,661 and EBT of €457.

Sixt revenue from Germany rose 11.8% y/y to €284 m (estimate: €264 m or +7.9%), revenue from Europe rose 16.2% to €345 m (estimate: 325 m or +9.4%), revenue from North America fell 1.9% to €310 m (estimate: €328 m or +3.8%).

Fleet expenses continue to dampen the earnings, rising 19.3% y/y to €266 m (my estimate: €252 m or +13% y/y).

Depreciation and amortization expense fell 8.3% y/y to €186 m, roughly in line with my estimate.

Sixt said they have launched its Sixt ONE Loyalty program in all the 13 corporate countries and around 1 m members have joined it, up from 300k as at March 2026.

Sixt’s preference shares are up 2.6% following the earnings results.

Assessment

While strong quarterly results were stable, with better-than-expected revenue growth in Europe (including Germany) offsetting less-than-expected revenue growth in North America, fleet expenses continue rising significantly faster than revenue growth. However, I like that repairs, maintenance and reconditioning costs only rose 5% y/y during the quarter, a deceleration from 17% last quarter. This may indicate that the measures put in place by management may be working. The major driver of the fleet expenses seem to be those associated with infleeting such as insurance and registration fees.

The strong acceleration in Europe (including Germany) revenue growth may have been driven by flight reroutings from Middle East to Europe and rebound in economic growth as noted by management in its analyst presentation (opportunities section, page 12).

North America FX-neutral revenue rose 9.2% y/y, below my estimate of around 13%. FX headwinds were 11.1%, versus my estimate of 9.1%. However, the reported y/y revenue decline was stable relative to Q4 2025. Since FX headwinds worsened by at least 1 percentage point versus Q4 2025, FX-neutral revenue growth likely improved by at least 1 percentage point as well.

Given that rental vehicle depreciation continues to improve, North America revenue is stabilizing (with FX headwinds likely temporary), and I continue to believe Sixt can rein in costs in the near term, I maintain a Buy rating on the preference shares, especially on further weakness.

Buy, €82: UBS analyst Zehua Jiang said Sixt’s operating business performed strongly despite currency headwinds.

Jefferies analyst Constantin Hesse said Sixt performed better than expected in all areas of its profit and loss statement despite a challenging economic environment. He added that fleet utilization and pricing supported revenues and profitability.