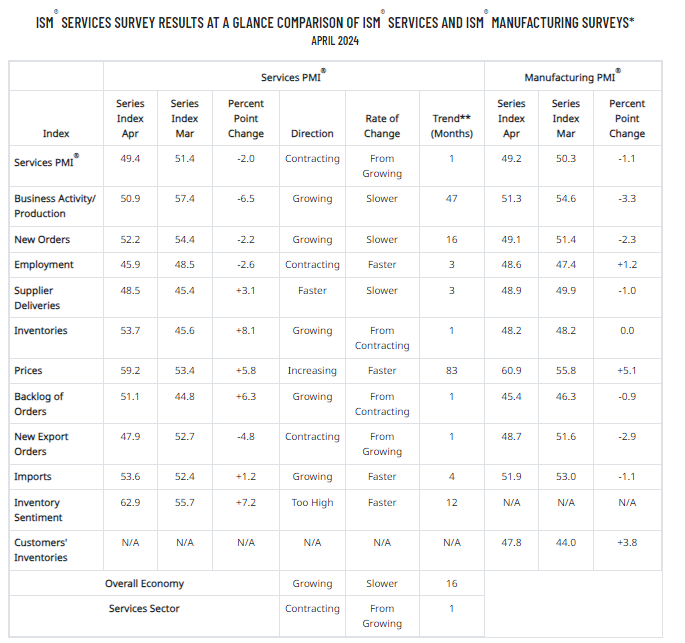

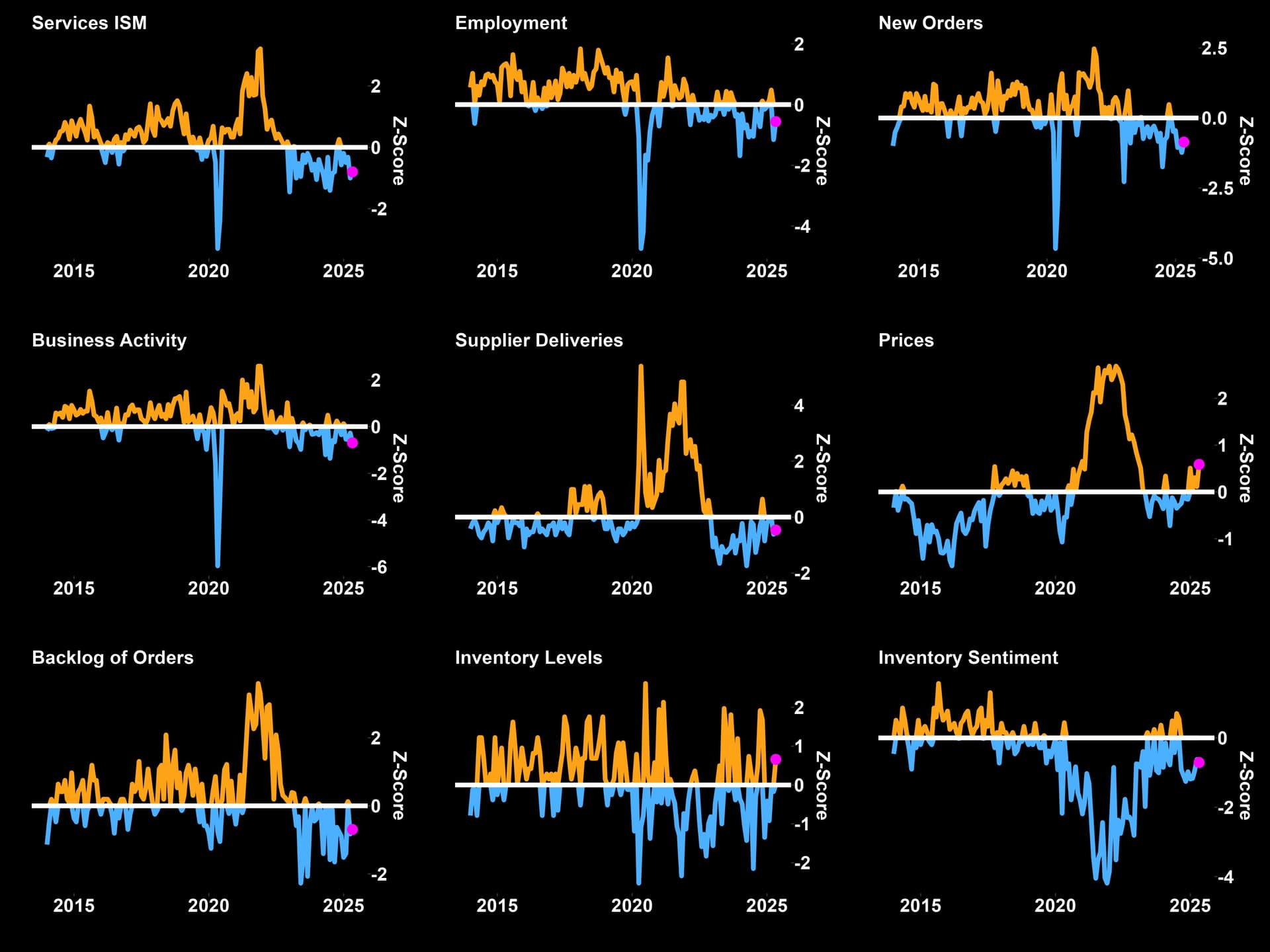

Both manufacturing and services came in April with mild “stagflationary” trends, both falling into contraction, with contracting employment too, but with increasing prices paid at the same time.

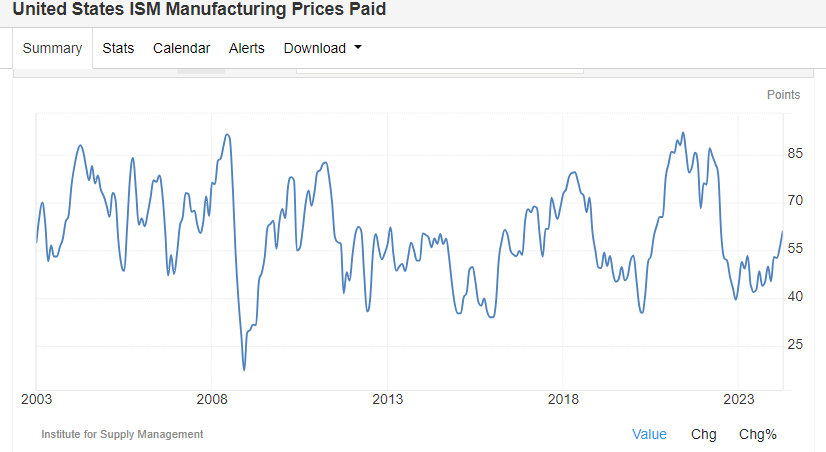

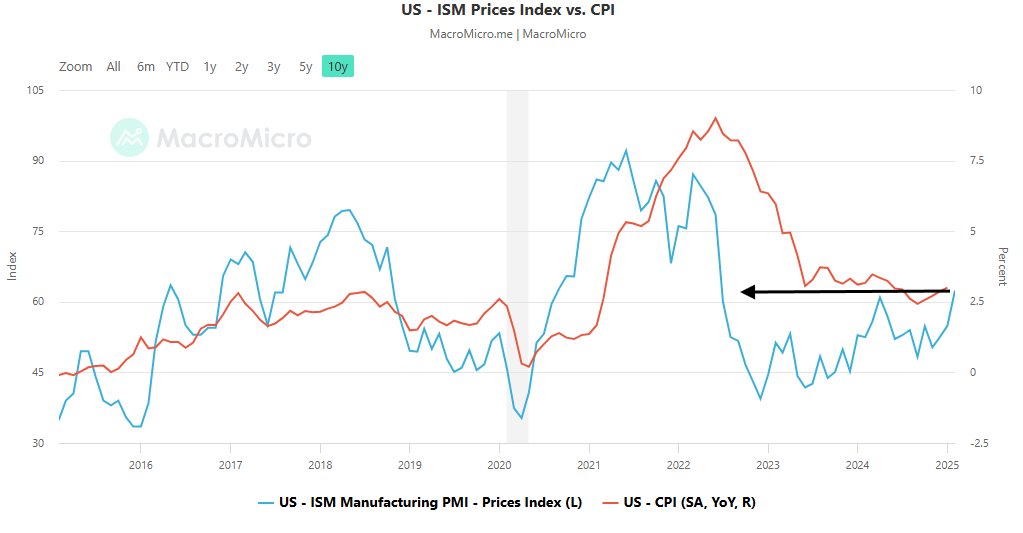

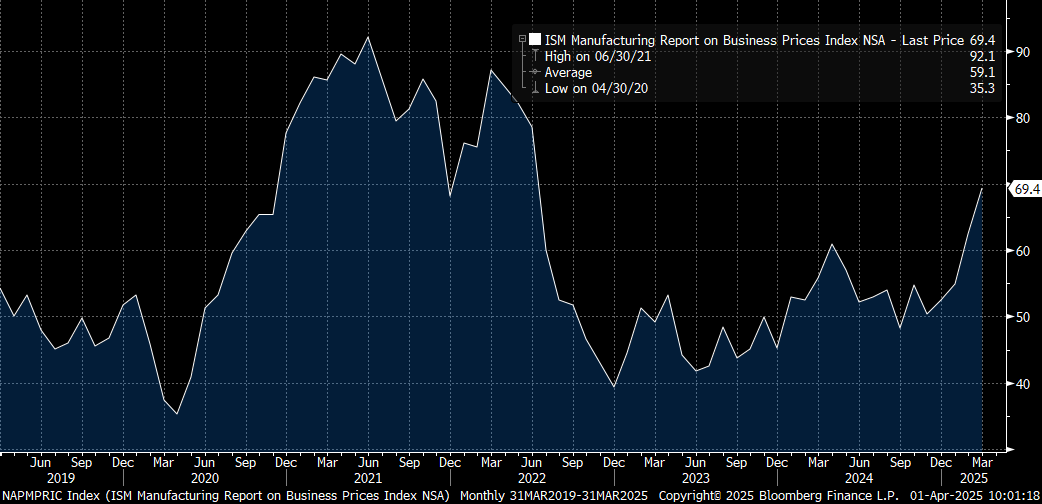

Prices paid for manufacturing are higher since June 2022. Still no near the highest levels, the series is also very volatile but the trend has been clearly up since the middle of last year.

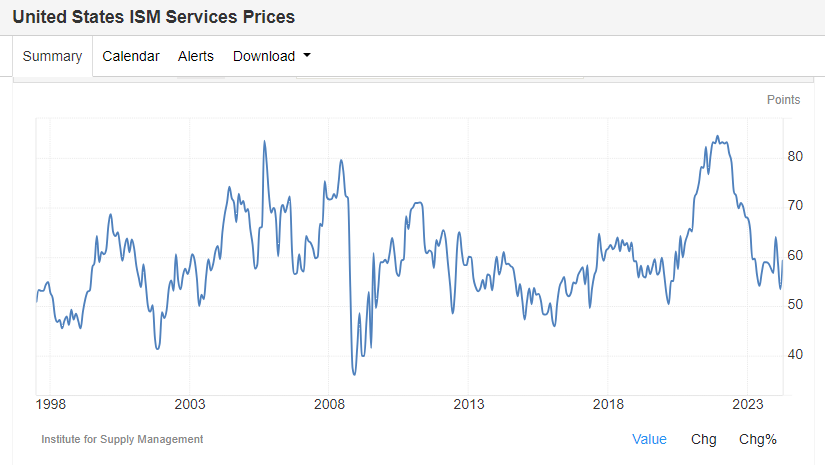

Prices for services look more stable still.

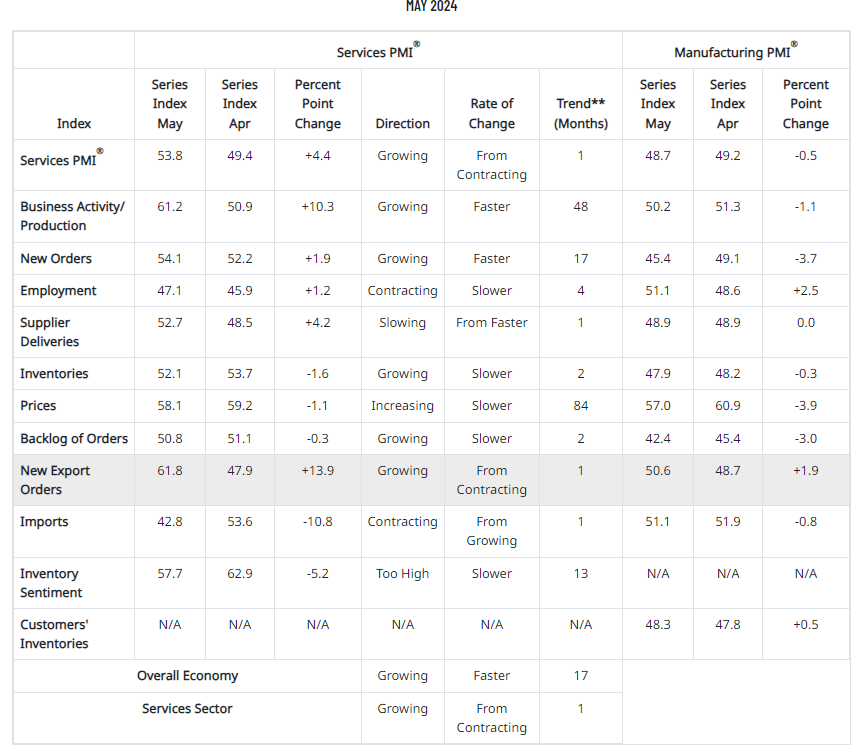

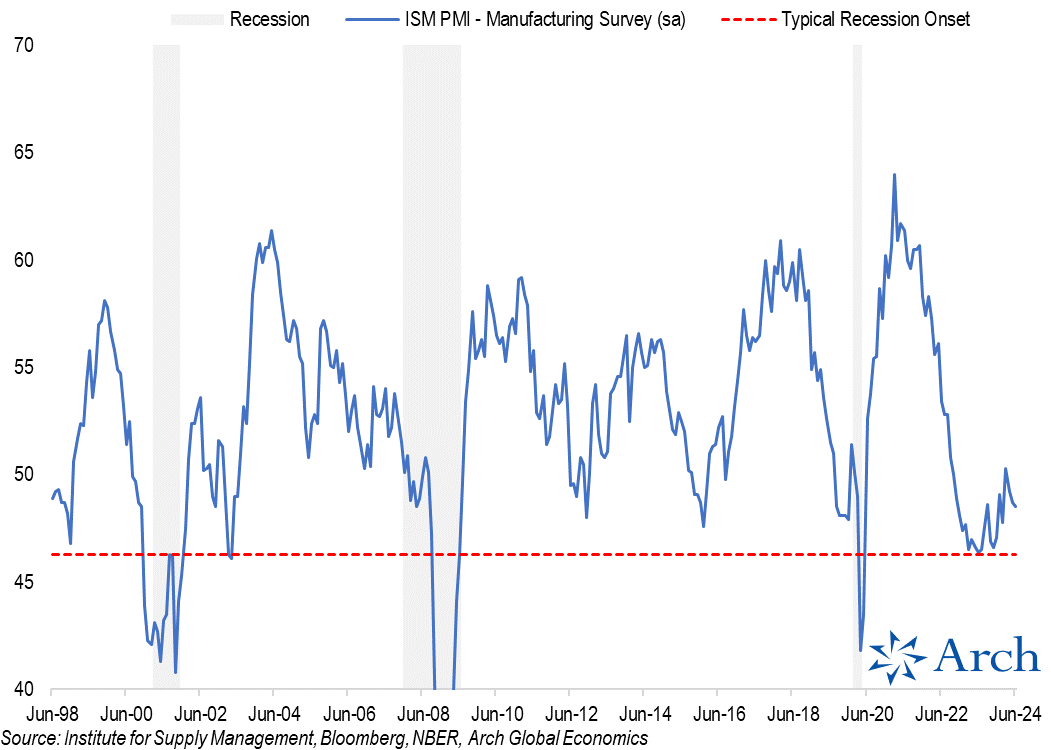

Manufacturing is weakening slightly again, while services continue to be very resilient.

It will be difficult to experience a singidcant improvement in manufacturing with rates this high.

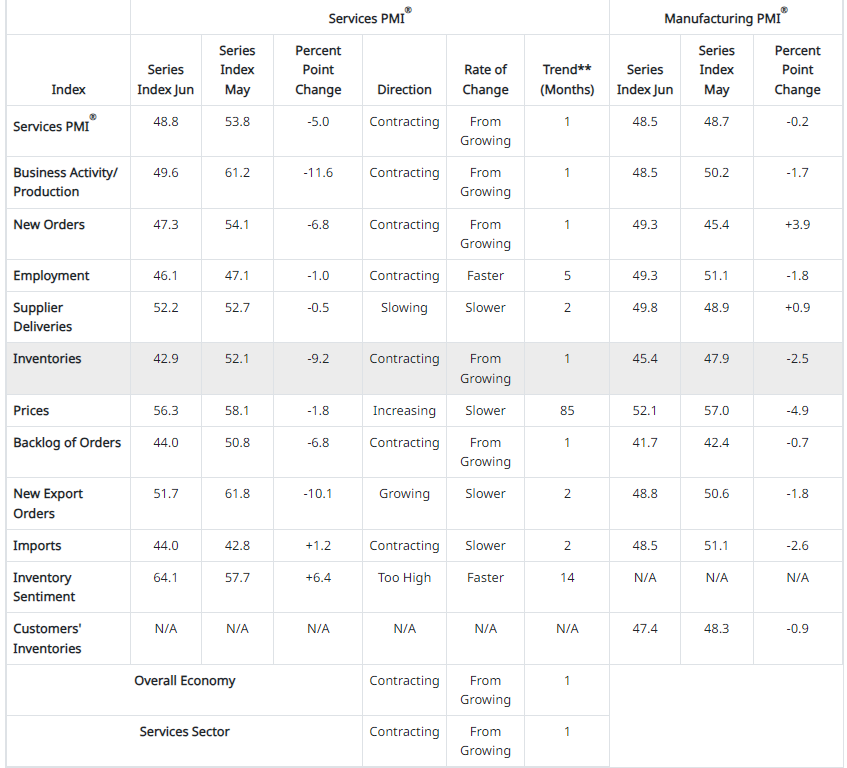

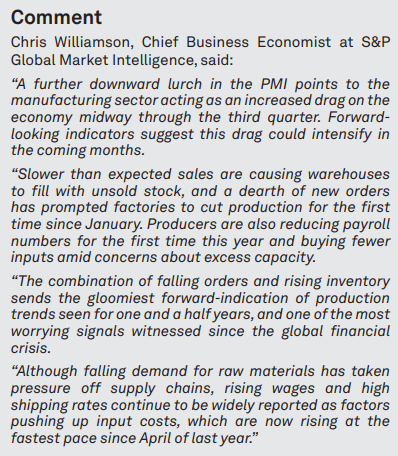

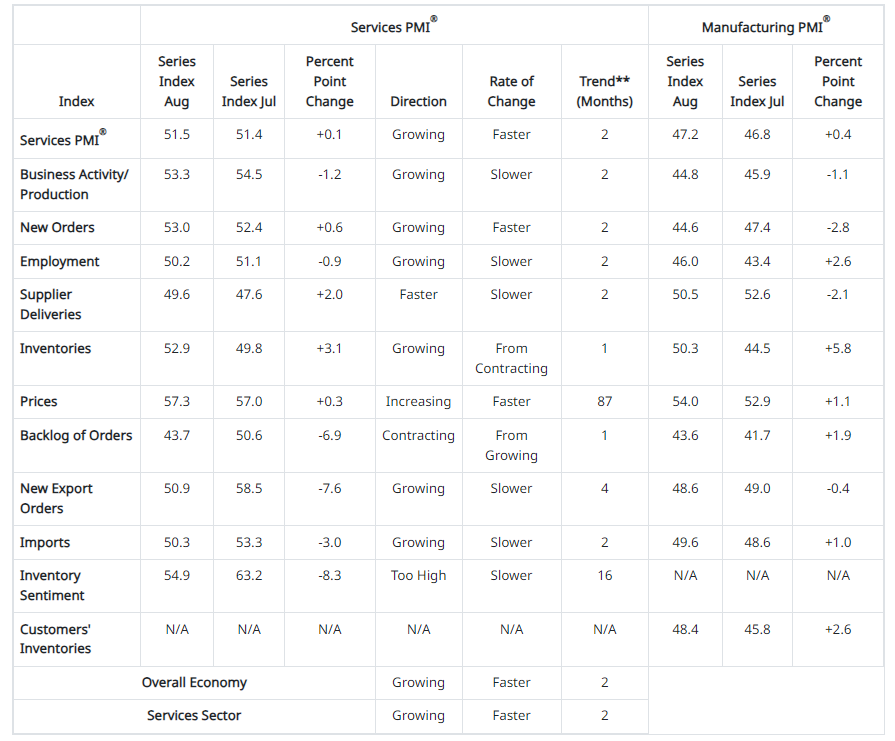

June 2024 PMIs reveal a noticeable decline in the Services Sector, while the Manufacturing Sector remains weak but stable

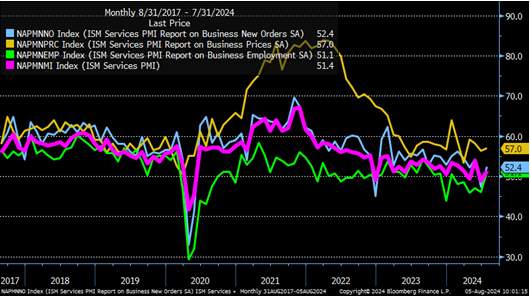

The ISM Services PMI in the US fell to 48.8 in June 2024, the sharpest contraction since April 2020. Markets were expecting 52.5 after 53.8 in May.

The decrease in the composite index in June is a result of notably lower business activity, a contraction in new orders for the second time since May 2020 and continued contraction in employment.

This is Mohamed A. El-Erian comment, which is noticeable to me because he has been very balanced always, even when everyone was on the recession camp.

Per the just-released ISM data, the US service sector fell by the most in four years.

At 48.8, down 5 points, the composite measure came well below the consensus forecast, driven by both the activity and order components.

This latest data release is consistent with growing evidence of what I have noted in recent weeks based on partial macro data and companies’ earnings calls—that is, the US economy is slowing faster than most expect, including the Federal Reserve.

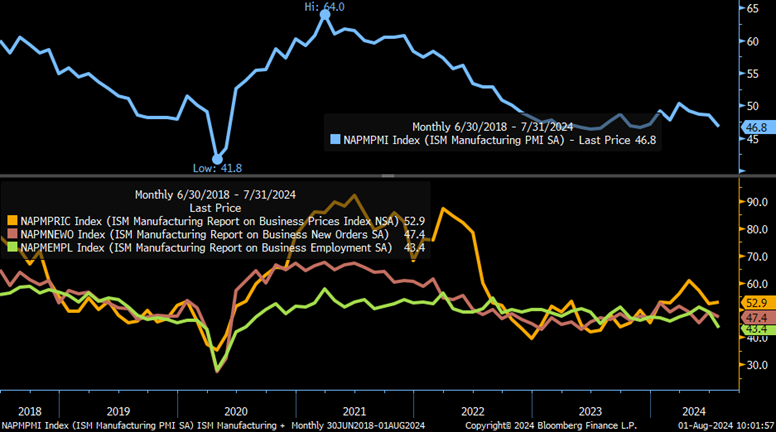

US manufacturing activity fell to 48.5 points in June, the third consecutive month of contraction. The latest reading of the ISM manufacturing PMI index missed expectations of 49.1 points.

Demand remains subdued, as companies demonstrate an unwillingness to invest in capital and inventory due to current monetary policy and other conditions. Production execution was down compared to the previous month, likely causing revenue declines, putting pressure on profitability

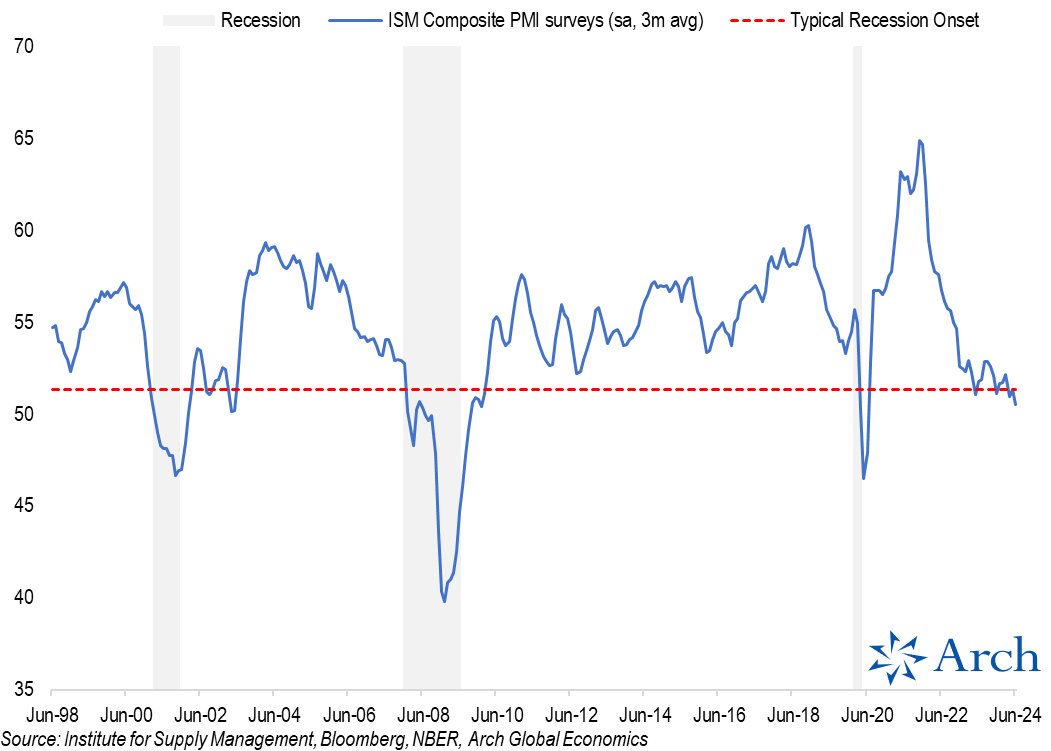

Combining the ISM Manufacturing and Services PMIs, weighted by their contribution to GDP, you get a proxy for implied economic activity. This metric has also dipped below the typical recession threshold

Manufacturing had a significantly weak month, with employment falling to the lowest level since 2021.

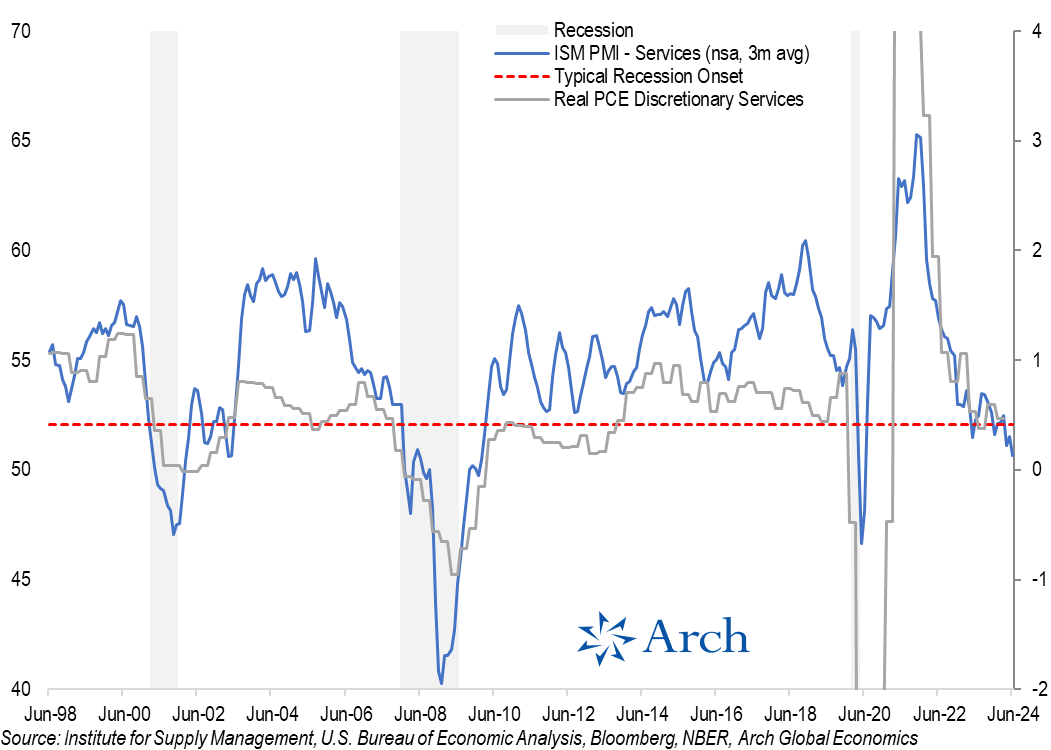

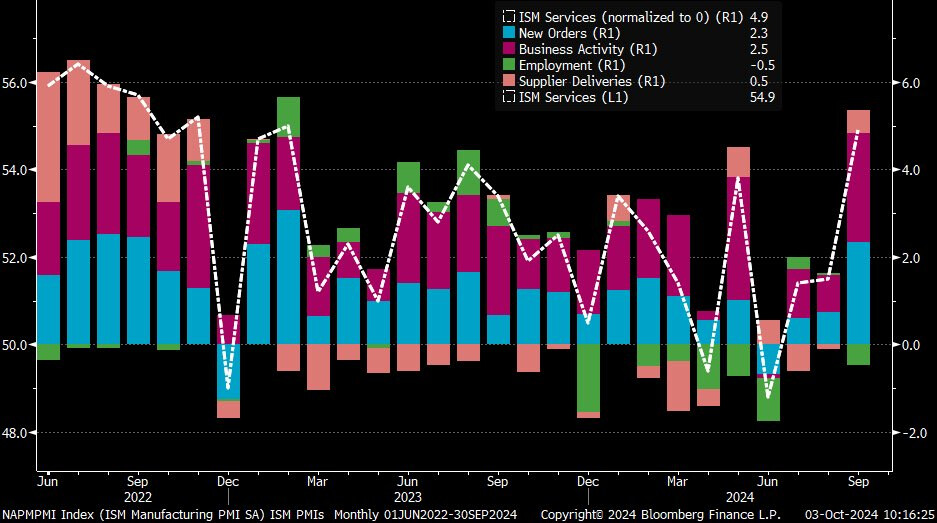

Services sector is still way more resilient, bouncing again for a weak June 2024 report.

Weak month for manufacturing activity once again.

It was expected that this year the sector would rebound but this has failed to materialize until now.

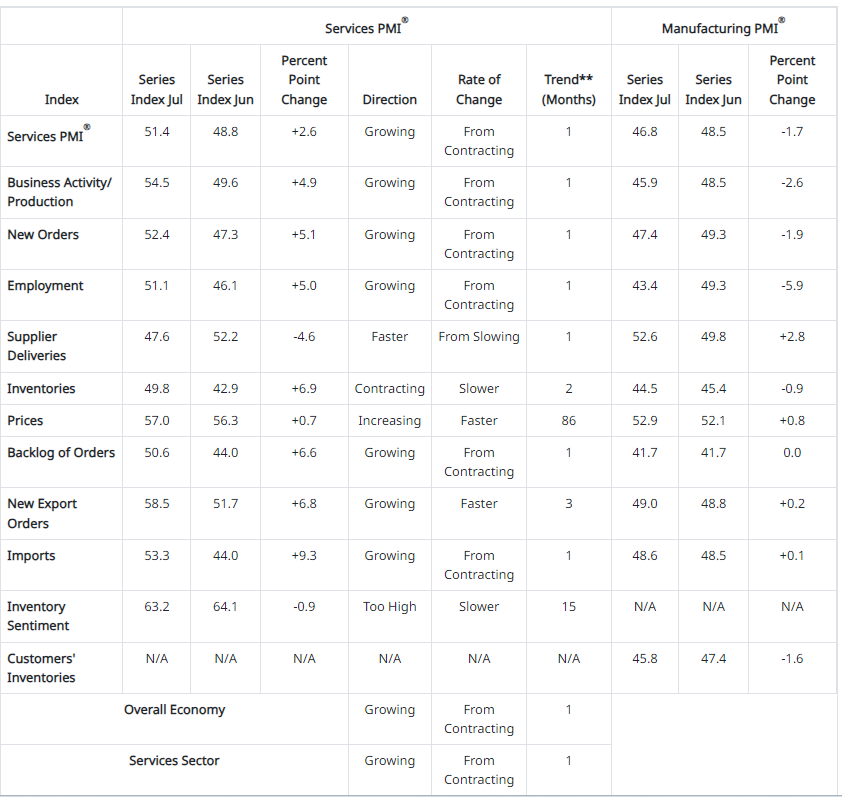

ISM PMI:

Demand remains subdued, as companies show an unwillingness to invest in capital and inventory due to current federal monetary policy and election uncertainty. Production execution was down compared to July, putting additional pressure on profitability.

The services sector on the other part remains resilient. However, employment reported a slight deterioration.

The economy is mostly services dependent, so a recession would probably need additional weakness from the services sector.

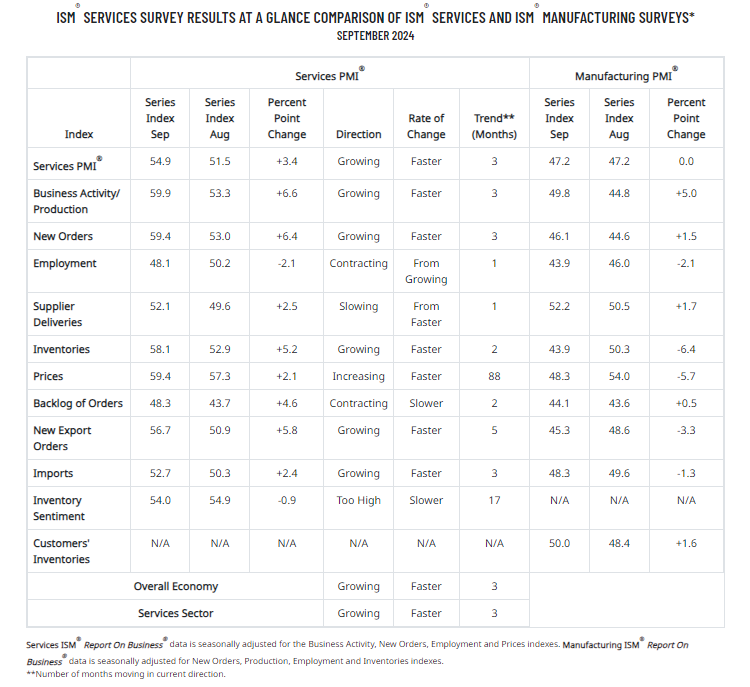

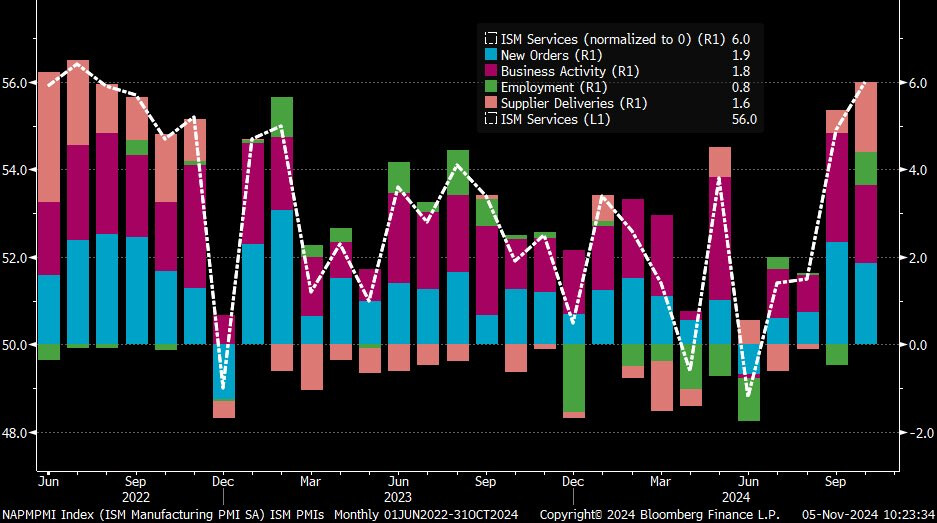

September 2024: Mixed report from both industries with employment weaker in both sectors

The September 2024 Services ISM reveals positive momentum in the U.S. services sector, with a Services PMI of 54.9%, indicating growth. The increase of 3.4 percentage points from August highlights expansion in business activity, new orders, and supplier deliveries.

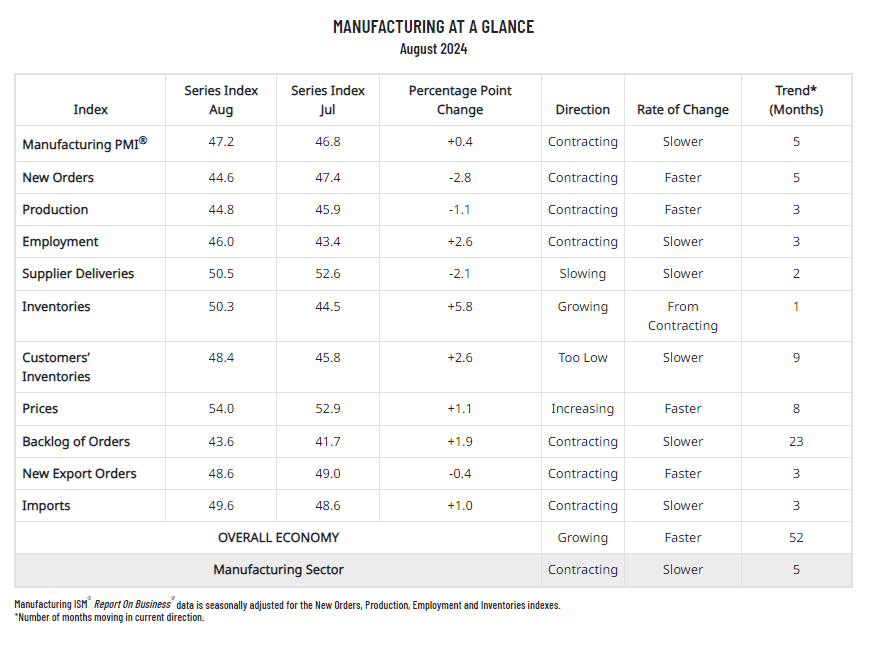

The September 2024 Manufacturing ISM indicates continued contraction in the U.S. manufacturing sector, with the Manufacturing PMI® at 47.2%, matching August’s figure.

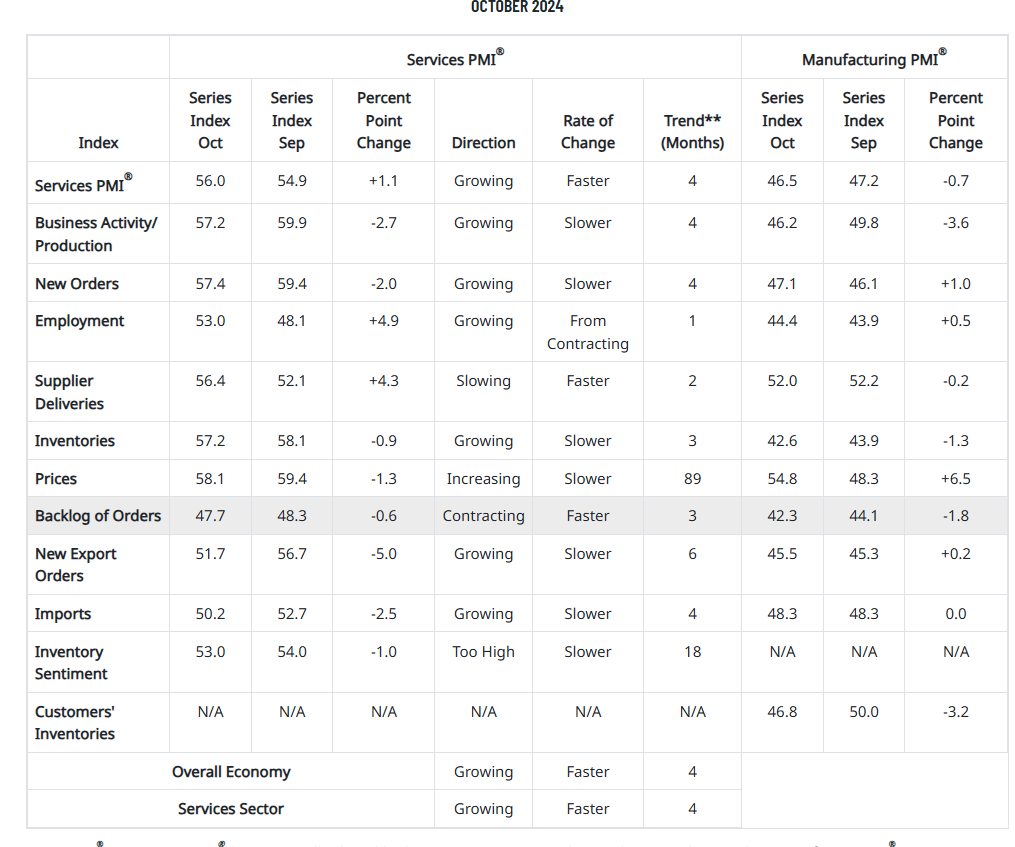

The ISM Manufacturing PMI index declined further in October, falling from 47.2 to 46.5, well below expectations of 47.6. U.S. manufacturing has now contracted for 22 out of the past 23 months, marking the second-longest contraction period on record.

Meanline, ISM Services PMI rose to 56.0 in Oct, above the estimate of 53.8. Notable the big increases in the Employment index, going from contraction in September to expansion again in october

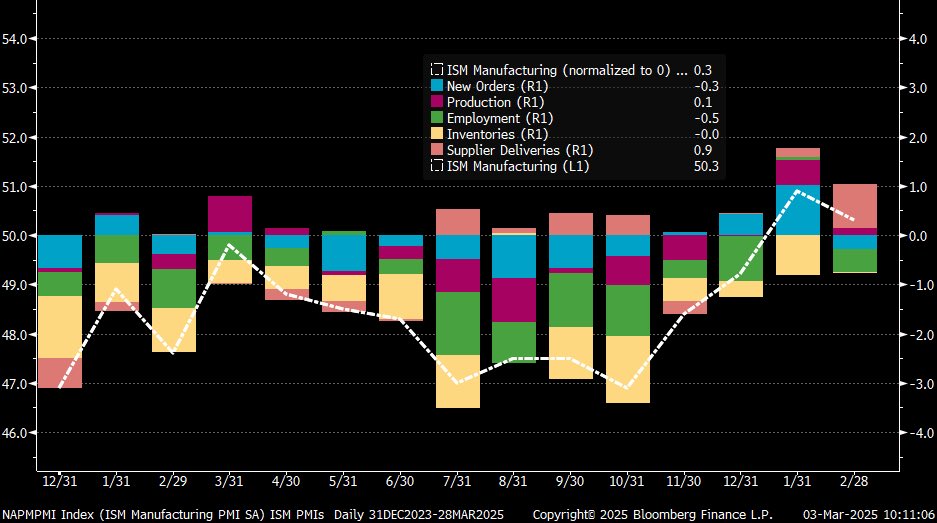

US ISM Manufacturing rebounded to expansion for the first time in 26 consecutive months of contraction rising to 50.9 (+1.7) signaling a pickup in economic activity.

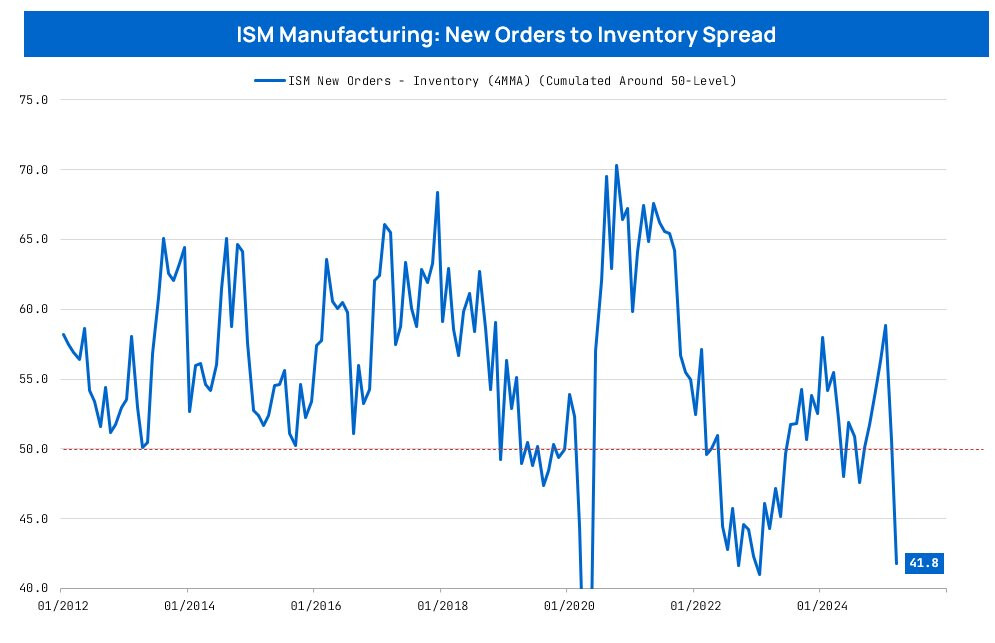

This reversal comes as new orders, production, and employment indices all turned positive, even as inventories remain low and supplier deliveries continue to slow marginally. Notably, prices have been increasing at a moderate pace - a trend that could pose challenges for managing inflation as demand strengthens.

Overall, the report paints a picture of a manufacturing sector at the cusp of recovery, with robust demand and output gains tempered by lingering supply chain constraints and careful price management.

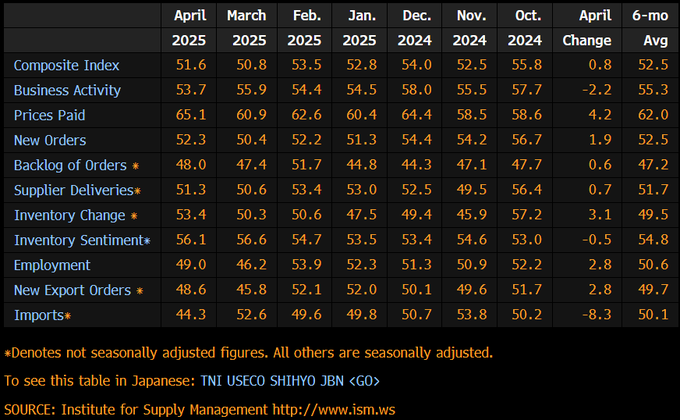

The February 2025 ISM Manufacturing PMI was stagflationary

Big drops in New Orders and Employment, Supplier Deliveries boosted the headline print by most since Aug 2022 (i.e. front-running tariffs?), and Prices Paid jumped to highest since June 2022.