I will use this topic to discuss and update once in a while the developments of the indicators that the NBER uses for its business cycle assessments.

This way we can assess the current status of the economy, and in which part of the business cycle we could most likely be located based on them.

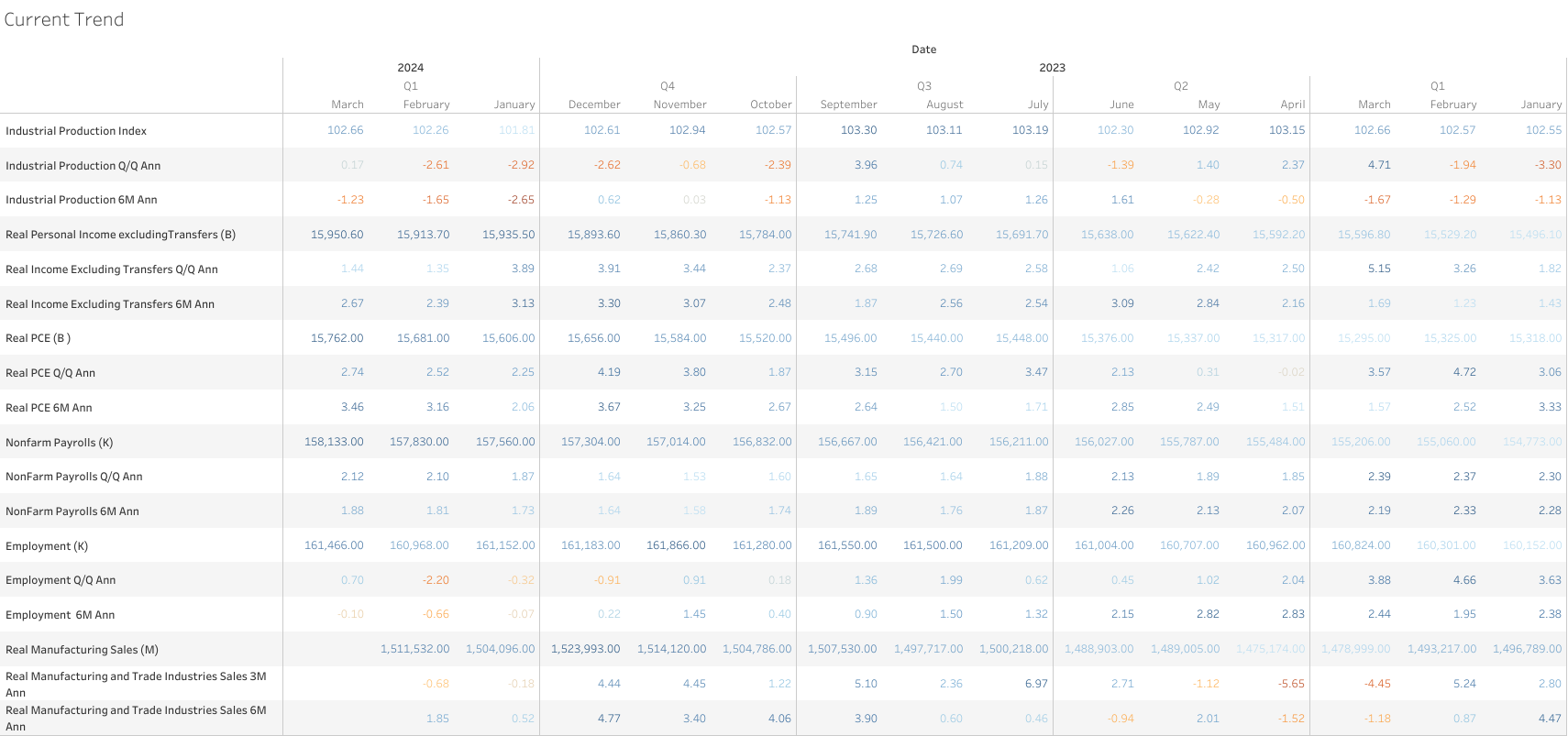

The determination of the months of peaks and troughs is based on a range of monthly measures of aggregate real economic activity published by the federal statistical agencies. These include real personal income less transfers, nonfarm payroll employment, employment as measured by the household survey, real personal consumption expenditures, wholesale-retail sales adjusted for price changes, and industrial production. There is no fixed rule about what measures contribute information to the process or how they are weighted in our decisions.

Two measures that are important in the determination of quarterly peaks and troughs, but that are not available monthly, are the expenditure-side and income-side estimates of real gross domestic product (GDP and GDI). The committee also considers quarterly averages of the monthly indicators described above, particularly payroll employment.

Q1 2024 update for business cycle indicators development

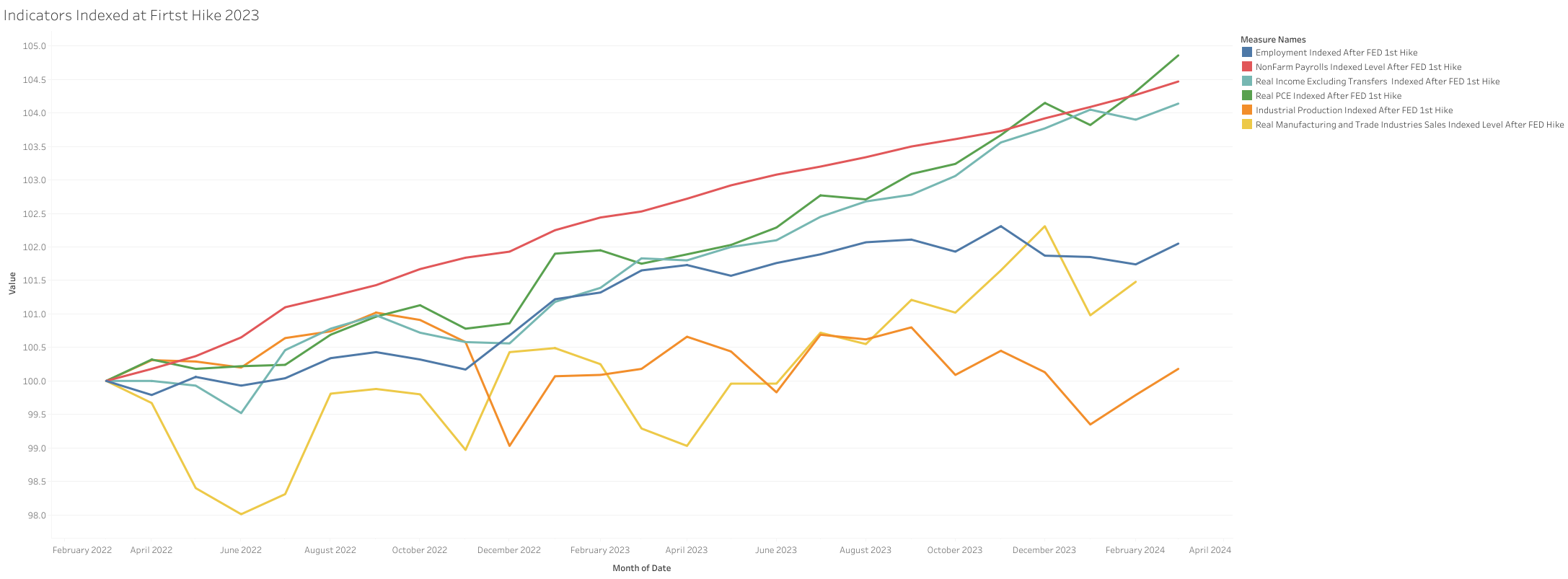

Comparable to the previous quarter, the current period remained relatively stable.

While there may be indications of decelerated growth in certain segments (income and spending, employment), at the same time they still exhibit steady performance, contributing to the overall stability.

Hence, no significant signs pointing to a significant deceleration at least for the next few months/quarter, or an imminent recession (keeping in mind this is past data already)

Spending, income, and payrolls continue to grow at a relatively good pace.

Employment and real manufacturing sales have been more flattish during Q1 2024. However, retail sales have been improving since the middle of last year, but growth has decelerated again.

While industrial production remains subdued, there are signs of a more stable trend for now.

Yes, I am planning to start doing it for the most important topics to have snapshots from time to time about the current trajectory.

I also want to create composite indexes that combine indicators into 1, but this is more medium/long term and will take multiple iterations until we get something that reflects reality more closely.

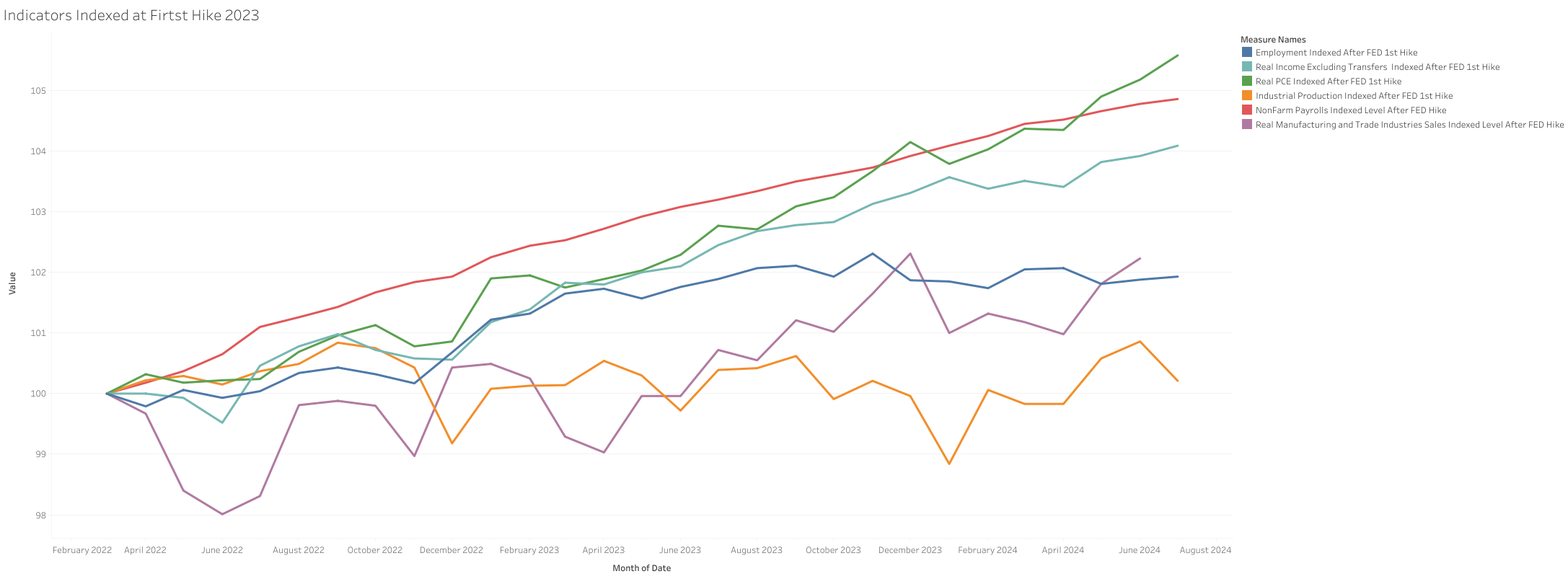

As of Q2 2024 Business Cycle indicators picture remains mostly unchanged

The indicators present a mixed yet stable outlook, imo does not suggest that the economy is not currently in a recession. However, it warrants caution for me as the growth rate is slowing, with the notable exception of spending indicators, which remain strong for now.

Pockets of concern for me comes from:

The underperformance of real income compared to real spending could not be able to support high levels of spending much longer

Employment has been flat for essentially 1 year already, and the other related labor market weakness in recent months.

Developments:

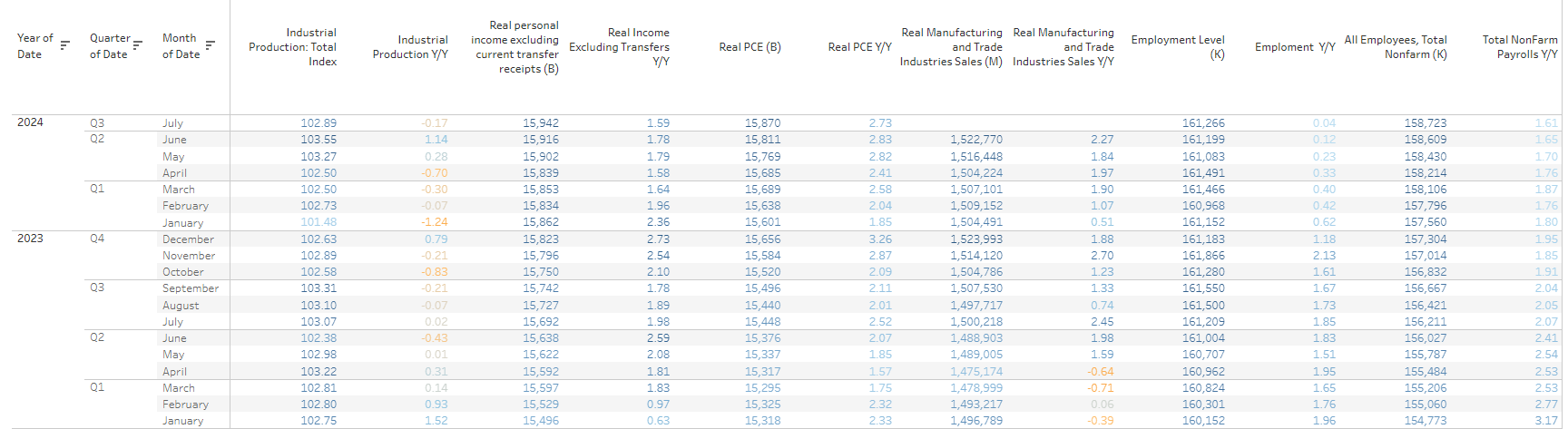

Most indicators reported increased activity growth in Q2 2024, except for income and employment.

Payroll added 503 thousand jobs in Q2 2024 (802 in Q1 2024), a 0.3% Q/Q and 1.7% Y/Y.

Employment decreased by -263 K persons in Q2 2024 (+283 in Q1 2024), a -0.16% Q/Q and 0.1% Y/Y. Basically flat in the last year.

Real Income excluding transfers increased by 36.5 Billion in Q2 2024 (60.2 B in Q1 2024), 0.22% Q/Q and 1.7% Y/Y

Real Spending increased by 112.1 Billion in Q2 2024 (56.4 B in Q1 2024), a 0.7% Q/Q and 2.7% Y/Y

Industrial Production Index increased on average 0.9% Q/Q (-0.44% Q/Q in Q1) and 0.2% Y/Y. Despite the recovery is still flat since mid-2022.

Real Manufacturing sales increased 22 Billion in Q2 2024 (-22 B in Q1 2024), a 0.5% Q/Q and 2% Y/Y.