This topic summarizes and discusses analysts’ opinions on Match Group.

1 Like

I=5

Buy, $38: TD Cowen analyst John Blackledge said Match Group’s valuation (P/E: 13x) is attractive and Hinge’s outlook is solid (Revenue growth: 26% y/y). He pointed to the stabilization in Tinder’s revenue and workforce reduction that will lead to cost-savings of $100 million per year. He also acknowledged management’s commitment to maintaining 2025 outlook despite macro uncertainties.

1 Like

August 12, 2025

HSBC raised Match Group’s price target to $35 from $32 (reason behind paywall).

HSBC Raises Match Group’s Price Target $35 From $32 | MarketScreener

1 Like

I=4

Buy, $40: TD Cowen analyst John Blackledge said Tinder is showing promising signs of product innovation and user engagement. He expects the introduction of new features such as Double Date and the upcoming interactive matching feature to enhance user experience and engagement, especially among young users.

I=4, August 22, 2025

Hold, $35: Morgan Stanley analyst Nathan Feather said Tinder’s turnaround is showing early signs of progress, with the pace of product development increasing. However, the turnaround is expected to be non-linear, negatively impacting revenue in the short-term as Tinder prioritizes user experience over immediate monetization. He pointed out that while the alternative payment system is promising, there’s uncertainty over the full impact and how the company will utilize the cost savings.

1 Like

Goldman Sachs said Tinder has begun seeing improvement in international user trends

1 Like

I=5

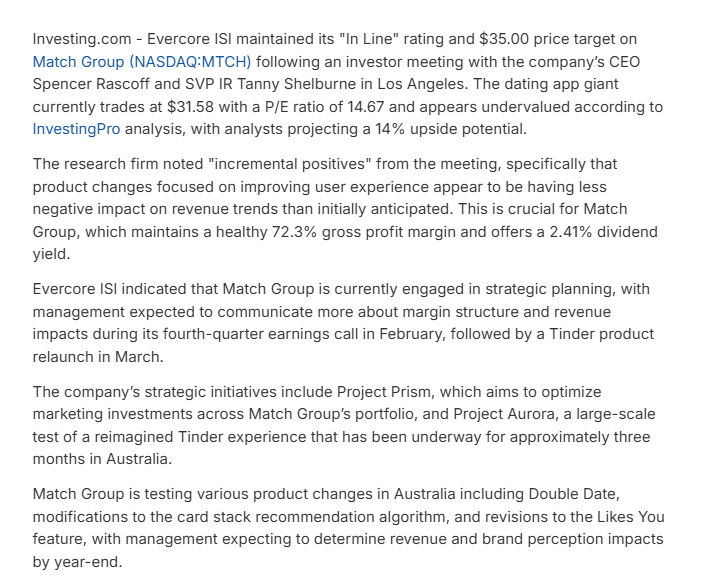

Evercore pointed to “incremental positives” after meeting management

In Line, $35: Evercore pointed to “incremental positives” after meeting CEO Spencer Rascoff and SVP IR Tanny Shelburne in Los Angeles. They product changes appear to be having less negative impact on revenue trends than initially anticipated. Evercore added that Match Group is currently engaged in strategic planning and the management is expected to communicate more about margin structure and revenue impacts in Q4 earnings.

1 Like

I=6

Tinder’s Face Check revenue headwind has stabilized to low single digits from 10%— RBC

Outperform, $37: RBC said Match Group is excited about its “double-date feature” driving interactions in 6 to 12 months, citing a meeting with the company’s leadership team. They added that Tinder’s new Face Check feature reduced revenue by 10%, but that has since stabilized to low single digits.

Assessment

Given that Face Check began rolling out in the U.S. in October, the 10% revenue headwind RBC cites likely reflects the impact during the initial rollout period, which overlaps with the current quarter. The effect likely applies only to the portion of U.S. revenue coming from users or transactions where Face Check is enforced, rather than all Tinder revenue globally.

1 Like

I=3

Outperform, $42->$43: Wolfe Research said 2026 could be another positive year for internet stocks, driven by AI developments and product catalysts, a relatively health macro backdrop, successful capital allocation, and pockets of re-rating potential.

1 Like

I=4

Buy, $40: TD Cowen analyst John Blackledge expects strong momentum at Hinge to drive double-digit growth and add meaningful incremental revenue in 2026. He added that Match Group’s mid-single-digit revenue growth looks achievable even with flat Tinder revenue, helped by higher revenue per payer and FX tailwinds. He pointed out that product and UX upgrades (verification, UI, optimization) could stabilize users and lift engagement, especially among younger users.

1 Like

I=6, May 14

Management signalled Tinder payer declines are still expected to run around 5% year over year in the coming quarters, UBS said

Neutral, $38: UBS pointed out that CFO Steven Bailey signalled that Tinder payer declines are still expected to run around 5% year over year in the coming quarters but revenue stabilization may occur before payer growth turns positive. UBS highlighted management’s view that Hinge remains under-monetized relative to its high-intent user base. UBS also indicated that management clearly framed M&A as secondary to buybacks.

1 Like

I=5

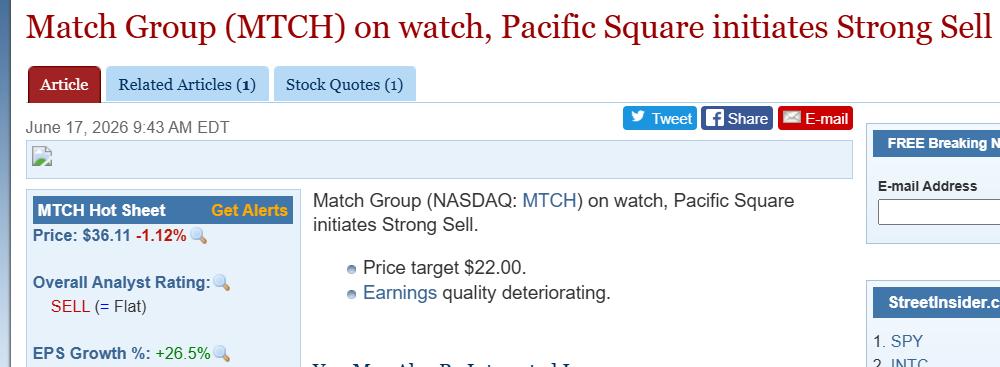

Pacific Square initiates Match Group’s strong sell, pointing out that earnings quality is deteriorating

@Aron whats your take on this? Are there indications that earnings quality is deteriorating? What could be meant by this?

In my opinion, earnings are stable. I will try to find out if they have a more detailed report. But they seem to be a small firm.

1 Like