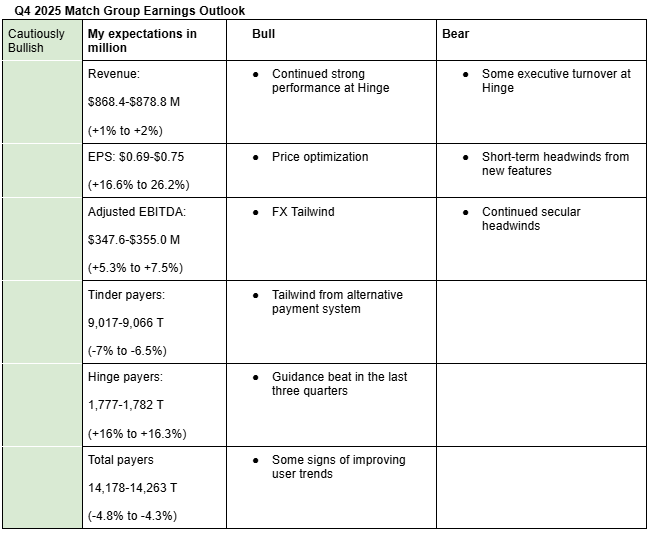

Cautiously Bullish Outlook Amid Hinge’s Strength, FX Tailwind, and Secular Headwinds

I am cautiously bullish on Match Group’s Q4 2025 earnings. My estimates (Google Sheets) take into account continued decline in Tinder paying users, strong performance at Hinge, FX tailwind, and revenue guidance beat in the last three quarters.

Here is a description of by bullish and bearish sentiments:

Bullish arguments

- Continued strong performance at Hinge: Hinge continues to deliver strong performance, with its revenue growth more than offsetting the decline in Tinder’s revenue. In Q3 2025, Hinge’s revenue rose by $39.3 million while Tinder’s revenue fell by $12.7 million. I expect Hinge to deliver another strong revenue growth this quarter.

- Price optimization: There was strong price optimization at Hinge, Tinder and E&E in Q3 2025 and Q2 2025. I expect this optimization to also play out in Q4 2025 as the company seek to compensate some growth headwinds (Q2 2025 Bumble Earnings (Notion)).

- FX Tailwind: The Euro continued to strengthen against the USD during the quarter. Given that Europe accounts for around 29% of Match Group’s revenue, I expect FX to be a tailwind to Match Group’s results. I project FX tailwind of around 2%-2.8% versus management’s guidance of 2.5% (Match Group FX Estimates (Google Sheets))

- Tailwind from alternative payment system: Management guided a tailwind of around $14 million from alternative payment system in Q4 (Q3 2025 Match Group Earnings Call (Notion)). However, the figure could be higher as management initially guided tailwind from alternative payment system of $60 million but upgraded it to $90 million in the next quarter.

- Guidance beat in the last three quarters: Match Group has exceeded management’s lower-point revenue guidance by an average of 1% in the most recent three quarters (Match Group Guidance Versus Actuals (Google Sheets)).

- Some signs of improving user trends: According to Apptopia, Tinder’s user engagement has started improving, with downloads declining 8% y/y in Q4 2025 versus a decline of 12% y/y in Q3 2025. The report also shows time spent per day by users aged 17-25 was up 20% y/y compared to +3% y/y for all users (Notion post). Search interest for Tinder also appears to have stabilized (Dating Apps User Trends (Google Sheets)).

Bearish arguments

- Some executive turnover at Hinge: Other than Hinge’s founder Justin Mcleod, Hinge’s Chief Risk Officer and Chief Operating Officer also left the company at the end of 2025 (Match Group Leadership & Other Executives). This may signal friction with the new Match Group CEO Spencer Rascoff. I didn’t find additional insights indicating the company’s culture or execution could be getting worse, but monitoring the situation remains crucial.

- Short-term headwinds from new features: While some analysts (such as RBC’s analysts) have indicated (citing management) that the headwind from the rollout of Face Check feature has stabilized (Notion Post), there are other upcoming features such as the new algorithm (being tested in Australia) which could cause further customer churn and lead to revenue loss. Also, the Face Check feature is yet to be rolled out in additional geographies.

- Continued secular headwinds: Dating apps such as Tinder and Bumble continue to lose users due to a combination of swipe fatigue, Gen Z’s need for authenticity, e.t.c. The trend could continue until better AI match-making features come into force, probably in the second half of 2026 (Dating Apps User Trends (Google Sheets)).

Here are management’s and analysts’ expectations for Q4 2025;

Management guidance for Q4 2025 revenue: $865-$875 million (+0.6% to 1.7%)

Management guidance for Q4 2025 adjusted operating income: $350-$355 million (+8.2% to +9.8%)

Analysts’ estimate for Q4 2025 revenue: $872.1 million (+1.5%).

Analysts’ estimate for Q4 2025 EPS: $0.70 (+17.5%).

Analysts’ estimate for Q1 2026 revenue: $853.3 million (+2.7%)

Analysts’ estimate for Q1 2026 EPS: $0.53 (+13.6%)

Confidence level and recommendation

My confidence level on the outlook is around 70% given the volatility surrounding the turnaround and the lack of enough insights on the quarter. As a result, I have a Hold rating on the stock. In the upcoming earnings call, I’ll be watching closely for updates on the product offensive, trends in Tinder’s user engagement, and other commentary on management’s execution.

Note: I may update my projections and recommendations if additional insights arrive before the earnings on Tuesday next week.