Yes, I would just say his tone is still hawkish, since the only dovish position at the moment is not raising rates anymore, and pausing it at the current level for a significant amount of time.

Housing prices started to rebound since February.

He also mentions industrial production has slowed significantly, residential investment has declined in each of the past quarters, and loan growth has also declined very sharply already.

Federal Reserve Governor Christopher Waller said last week’s economic data was positive and that it can give them time to decide whether to raise interest rates further.

“That was a hell of a good week of data we got last week, and the key thing out if it is it’s going to allow us to proceed carefully,” Waller told CNBC’s Squawk Box. “We can just sit there, wait for the data, see if things continue.”

He emphasized that their rate decision will be determined by incoming data.

“So, I want to be very careful about saying we’ve kind of done the job on inflation until we see a couple of months continuing along this trajectory before I say we’re done doing anything,” he said.

He doesn’t think that one more rate hike will throw the economy into a recession.

“I don’t think one more hike would necessarily throw the economy into recession if we did feel that we needed to do one,” Waller said.

Christopher Waller is considered one of the most hawkish FOMC members.

Economists surveyed by Bloomberg expects the FOMC to keep interest rates steady at 5.25%-5.5% range at its September meeting and stay there until a first cut in May 2024, two months later than economists forecated in July.

The economists also think that the policymakers will likely suggest one more rate hike this year in their so-called dot plot, but won’t go ahead with the increase.

Markets are expecting a pause for the rest of the year. However, I have heard that if the FED wants to surprise at some point, this could be 1 of the opportunities since the data has not been particularly good for inflation.

While I don’t think they will hike in this meeting (my confidence is not as high as the markets), I think there is a likelihood that their new projections could show an increase in the terminal rate in 2024 with more growth, eliminating some of the rate cuts the market is pricing at the moment.

For now, I think they will continue to leave the door for more hikes in the future, and still data dependent.

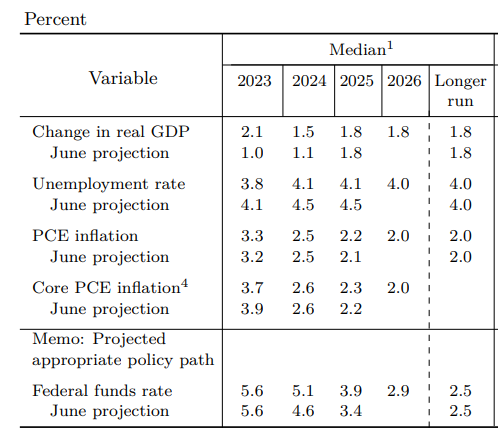

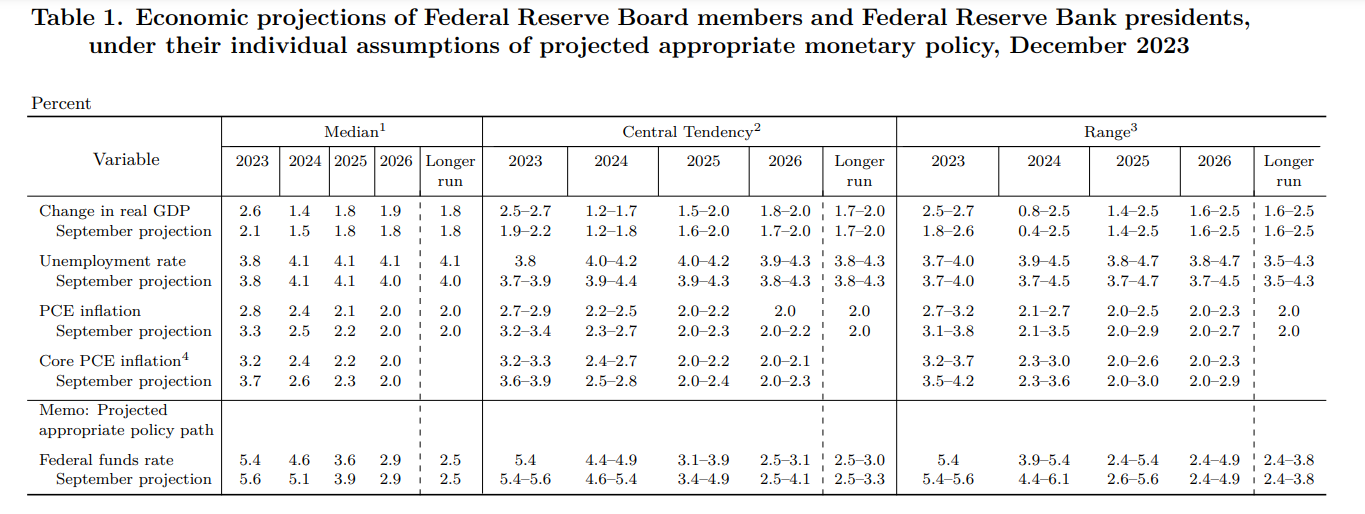

FOMC maintained the target range for the fed funds rate at 5.25%-5.50% as was expected by the market.

Fed’s dot-plot indicated there is a likelihood of one more rate hike in 2023, followed by two rate cuts in 2024, two fewer than forecasted in July.

The projections for 2025 funds rate also moved up from 3.4% to 3.9% while GDP projections for 2023 moved to 2.1%, more than double the projetion given in June.

The FOMC statement noted that future monetary decisions will be informed by incoming data and that they are committed to bringing inflation down to 2%.

The stament described the economic activity as expanding at a solid pace unlike in previous statements where they described it as moderate.

Also, unlike in the past where they described they labor market as robust, they said “job gains have slowed in recent months but remain strong.”

The majority is actually expecting another hike this year, 12-7. While now expecting higher rates for 2024 and 2025.

I stay with a phrase I heard in Bloomberg, “wishful thinking” from the FED

How inflation is supposed to come to 2% with the GDP and unemployment projections they are making?

So they increased growth for 2023 and 2024, and reduced unemployment to only a peak of 4.1, but inflation is not expected to be higher than the previous projections for 2024, and suppose to continue to come down the same.

And they increased the rate level for 2024 and 2025, and this is expected to only impact inflation, but generate higher GDP and lower unemployment than previous projections.

This is like what is was hearing the inflation transitory statement in 2021.

If they are able to achieve this, I will be Powell fan forever haha

Will make the notes tomorrow after the transcript is out, because at least Powell sounded more balanced, but confusing, not his best I think. (I am not the best at taking notes while listening)

The overall message is that a pause doesn’t mean that they have decided yet what will be the appropriate level for rates, and they will proceed carefully going forward assessing all the data available. (the inflation data, the labor market data, the growth data, the balance of risks and the other events that are happening out there)

My opinion at this moment is more balanced to think they are done hiking, but I dont have a great confidence in this. A somewhat hotter inflation readings or other data could change it.

Things that stood out for me:

Powell acknowledged that sustained higher energy prices is significant, could influence consumer inflation expectations, and could also impact spending negatively.

Powell said is possible that the neutral rate currently is higher than previously thought, and that’s why the economy has remained resilient longer than expected.

A strong economy would mean they would have to do more to get to 2%

Yesterday’s projections showed much more than a soft landing, but when asked about it, Powell did not agree to say that a soft landing is now his baseline scenario, said he always thought it was a plausible scenario, but the path is not in their control. So, it seems even he does not entirely agree with his staff forecasts, or at least is more balanced on this.

He also said forecasts are highly uncertain and is not a plan that is negotiated or discussed

I found it interesting that he said they are not so sure spending has held out because private balance sheets are strong, because at the same time consumer saving rate has come down a lot. He questions if this is sustainable, or if it just means that the effect will be felt later, or that the neutral rate is higher, or policy has not been restrictive long enough.

About the government shutdown, he said is a possibility they would have to deal with some lack of data, but is uncertain how that would affect next meeting.

Fed Chairman Jerome Powell said inflation is still too high and that recent positive inflation data is not enough to determine a trend.

“Inflation is still too high, and a few months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal,” said Powell in his prepared speech at the Economic Club of New York.

Powell pointed out that the fed is committed to bringing inflation to its 2% target.

“While the path is likely to be bumpy and take some time, my colleagues and I are united in our commitment to bringing inflation down sustainably to 2 percent,” he said.

He hinted that the labor market and economic growth may need to slow to achieve the inflation target.

“Still, the record suggests that a sustainable return to our 2 percent inflation goal is likely to require a period of below-trend growth and some further softening in labor market conditions,” he added.

Powell said that future decisions will take into account incoming data and policy risks.

"Given the uncertainties and risks, and how far we have come, the Committee is proceeding carefully. We will make decisions about the extent of additional policy firming and how long policy will remain restrictive based on the totality of the incoming data, the evolving outlook, and the balance of risks, " he said.

Tomorrow the FED is expected to pause, and the market is pricing a pause until June/July when they expect the first cut.

The overall feeling is that even though some numbers have not been the best, the move up in yields has already tightened the conditions more than enough.

FOMC maintained the target range for the fed funds rate at 5.25%-5.50% as was widely expected by the market.

The statement said that economic activity expanded at a strong pace in the third quarter and that “labour gains have moderated since earlier in the year but remain strong.”

The committee maintained that they will continue to rely on incoming data in their monetary decisions.

“In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments,” the statement said.

“In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals,” it added

Not much new from Powell, but some takeaways for me:

No decision made yet if another hike is needed, incoming data will determine it and the bias is to hike, but seems markets don’t buy this for the reaction during the conference.

Financial conditions tightening will only help if it is persistent, volatility does not help

FED Commission is not even thinking about rate cuts or stopping QT. Reserves are still not scarce.

Recession not back on the forecast.

The efficacy of the dot plot decays over the three months

Lags from the monetary policy are always uncertain, but he mentioned some effects can already be seen in some data, and some developments eg. debt coming due next year will increase them.

Supply issues alleviating has helped inflation to come down, but he does not believe this is enough to bring it to 2%, softening demand will also be needed.

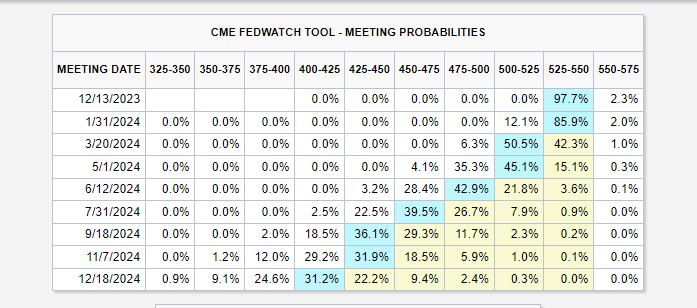

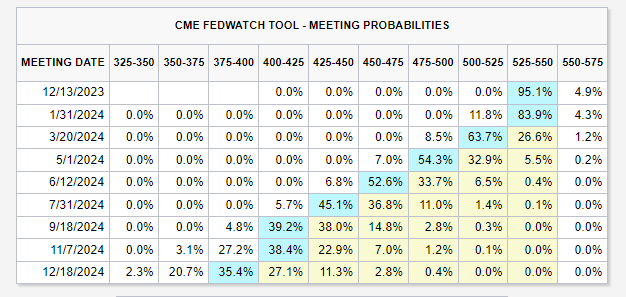

Market probability of pausing in December was 69% yesterday, after today’s meeting is 82%. Rate cuts are still expected after June 2024.

Fed Chairman Jerome Powell said that they are committed to bringing down inflation to their 2% target but he’s not confident they have achieved such a stance.

“The Federal Open Market Committee (FOMC) is committed to achieving a stance of monetary policy that is sufficiently restrictive to bring inflation down to 2 percent over time; we are not confident that we have achieved such a stance,” he said in IMF prepared remarks.

He said that though inflation has come down, they still have a long way to go in bringing it down to 2% target.

"U.S. inflation has come down over the past year but remains well above our 2 percent target. My colleagues and I are gratified by this progress but expect that the process of getting inflation sustainably down to 2 percent has a long way to go, " he said.

However, he said that they are cautious as the risk of doing too much and too little are now close.

“If it becomes appropriate to tighten policy further, we will not hesitate to do so. We will continue to move carefully, however, allowing us to address both the risk of being misled by a few good months of data, and the risk of overtightening,” he pointed out.

Powell pointed out that it is unclear how much more will be achieved through further supply-side improvements.

“While the broader supply recovery continues, it is not clear how much more will be achieved by additional supply-side improvements. Going forward, it may be that a greater share of the progress in reducing inflation will have to come from tight monetary policy restraining the growth of aggregate demand,” Powell noted.

Seems he wanted to sound more hawkish today, probably after last week’s reaction.

Not sure it will work, as the markets are not really changing their pricing.

Fed Governor Christopher Waller said yesterday that he is confident that the current policy is in a position to get inflation back to the 2% target.

“While I am encouraged by the early signs of moderating economic activity in the fourth quarter based on the data in hand, inflation is still too high, and it is too early to say whether the slowing we are seeing will be sustained,” he said. “But I am increasingly confident that policy is currently well positioned to slow the economy and get inflation back to 2 percent,” he said in a prepared remarks for a speech in Washington, D.C.

Fed chair Jerome Powell calls talks about interest rate cuts premature, adding that they are prepared to tighten policy further if needed.

“It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease. We are prepared to tighten policy further if it becomes appropriate to do so,” Powell said in prepared remarks for an audience at Spelman College.

Powell pointed out that inflation is moving in the right direction and that the policy is working.

“Inflation is still running well above target, but it’s moving in the right direction,” he said.

“The strong actions we have taken have moved our policy rate well into restrictive territory, meaning that tight monetary policy is putting downward pressure on economic activity and inflation,” Powell said. “Monetary policy is thought to affect economic conditions with a lag, and the full effects of our tightening have likely not yet been felt.”

The market is now pricing cuts as soon as March, and 5 cuts in 2024. Very aggressive imo, if there is not a significant economic slowdown as they also think.

FOMC voted unanimously to maintain the target range for the fed funds rate at 5.25%-5.50%, as was widely expected by the market.

The FOMC statement said inflation has eased over the past year but remains elevated, job gains have moderated, unemployment rate has remained low and economic activity has slowed from its strong pace in the third quarter.

The statement noted that the committee is committed to bringing inflation down to their 2% target and that they will continue to rely on incoming data in determining if “any” addittional policy firming will be needed.

FOMC’s “dot plot” models at least three rate cuts (of 25 basis points) in 2024, less than four rate cuts that was expected by the market but a sharper pace than projected in September.

For 2025 and 2026, the the dot plot" indicates four and three rate cuts respectively though individual expectations in these two years differed considerably.

A way more dovish conference, a pretty different feel to the last ones. I wonder if it’s that they really think inflation is coming to target soon, or if they are seeing some warnings for the economy, but there definitely was a change in the message. Unfortunately, Powell is not saying much either.

No additional hikes is likely, but they are not removing off the table completely the possibility if its becomes appropriate

Some fed member has said that If inflation continues to come down, rate cuts will be needed, if not the real rates could become more restrictive. So, cuts are a signal to keep real rates equal.

Rate cuts will be a topic in their meetings going forward. This is new, as last meeting they said rate cuts were not even discussed.

There is a real possibility that there will be a recession in 2024, but the soft landing is also still possible if the current trends continue. So, basically, no one knows.

Financial conditions will come into alignment with their goals, but in the meantime, there will be a lot of volatility.

He welcomes the progress in inflation, but he needs to see continued progress.

A surprise in growth in 2024 again, could mean inflation takes longer to get to target, and then rates higher for longer, or even more hikes.

No thinking about altering the pace of QT.

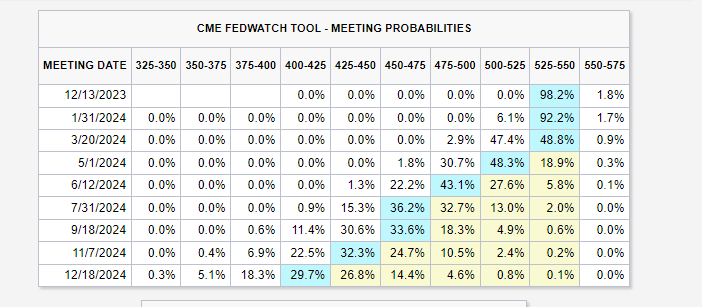

I again still think the markets getting ahead, after the conference they are again pricing cuts as soon as march, and 6 cuts in 2024. Whereas the fed projections only show 3.

This loosening of financial conditional is very well against their goal.

I do think significant rate cuts (4+) will happen if the economy gets very weak, but not if the economy is growing 1-2%.

But I have also seen that between the fed pause and the fed cuts is common to see a significant rally, even reaching ath right before a correction. So, this one could continue as the market’s price rate cuts, but not very low growth for 2024 or economic weakness.