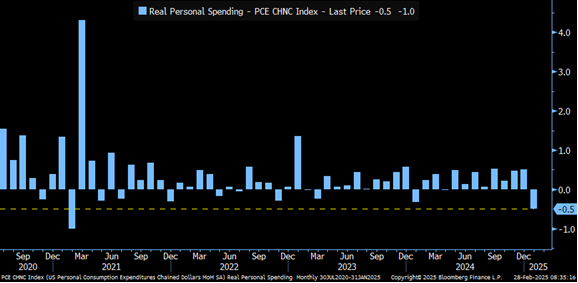

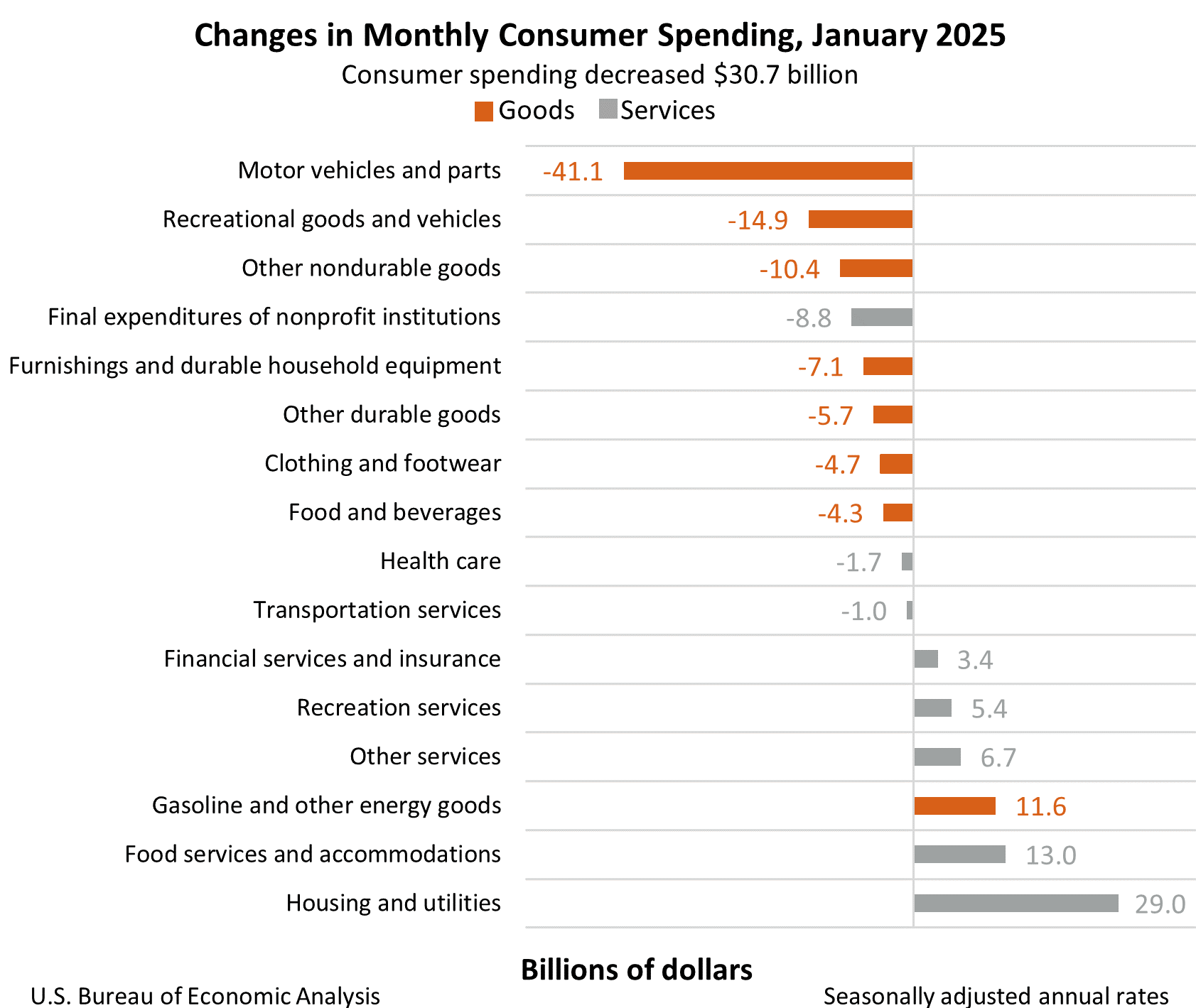

Consumer Spending for January comes negative and below expectations

Since retail sales were weak, this is not as unexpected, and it could have the exact same explanations like weather-related weakness and a strong holiday season, and also annual trends still looking solid. However, weak PCE will weigh on GDP more than only retail sales, and it adds to a series of economic data that have been coming weak and lower than expected since January, so it is something we should start to consider more now.

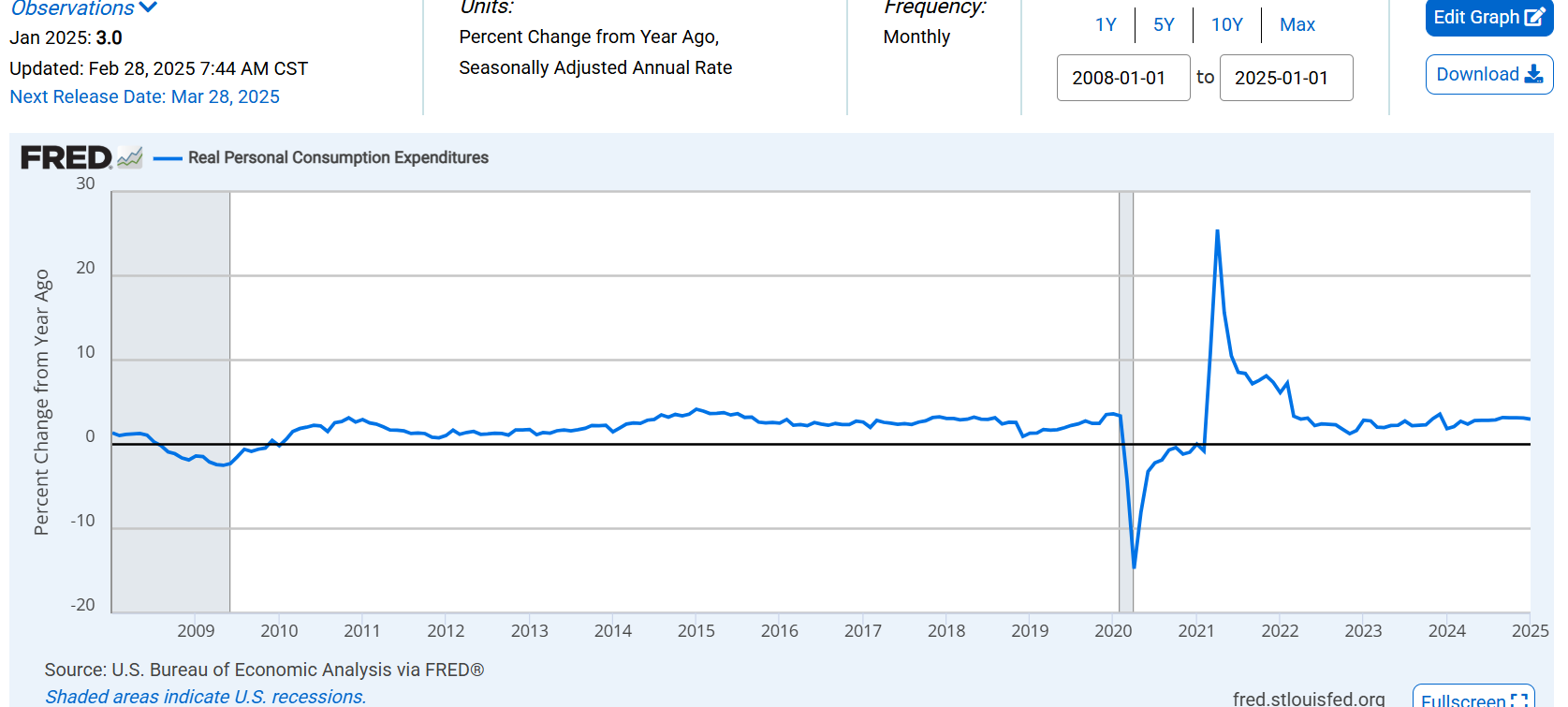

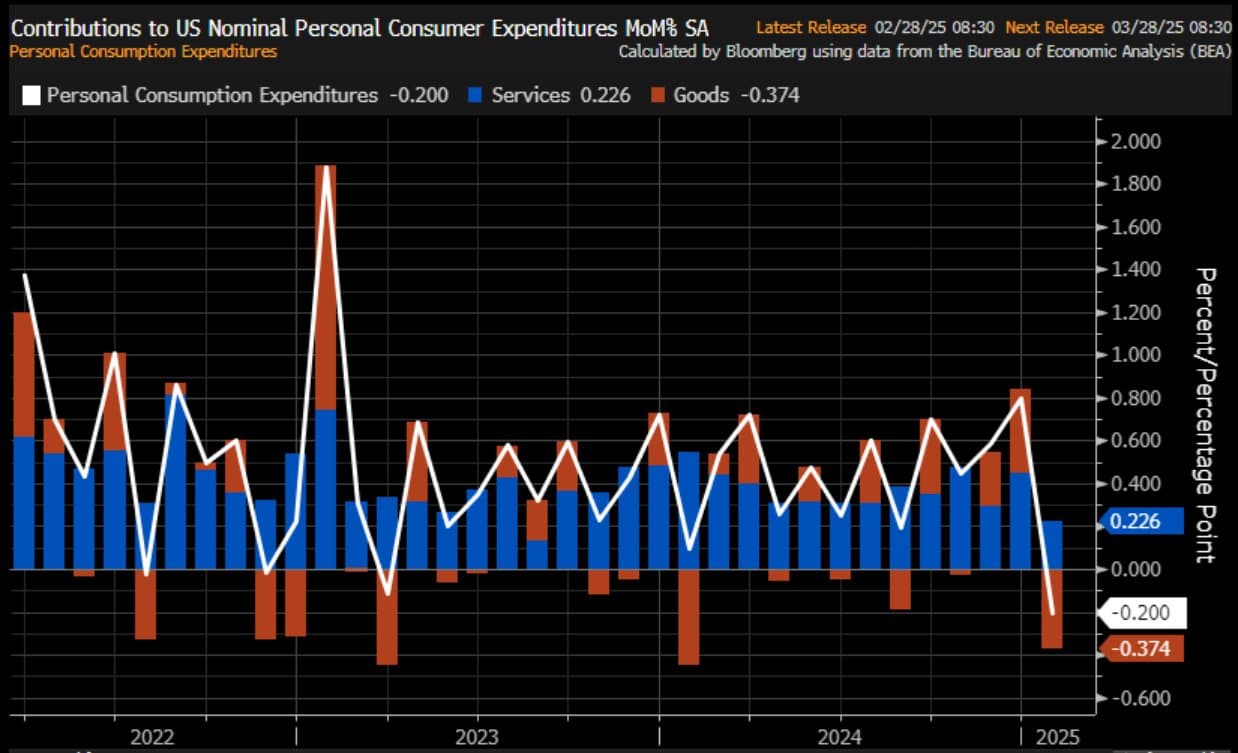

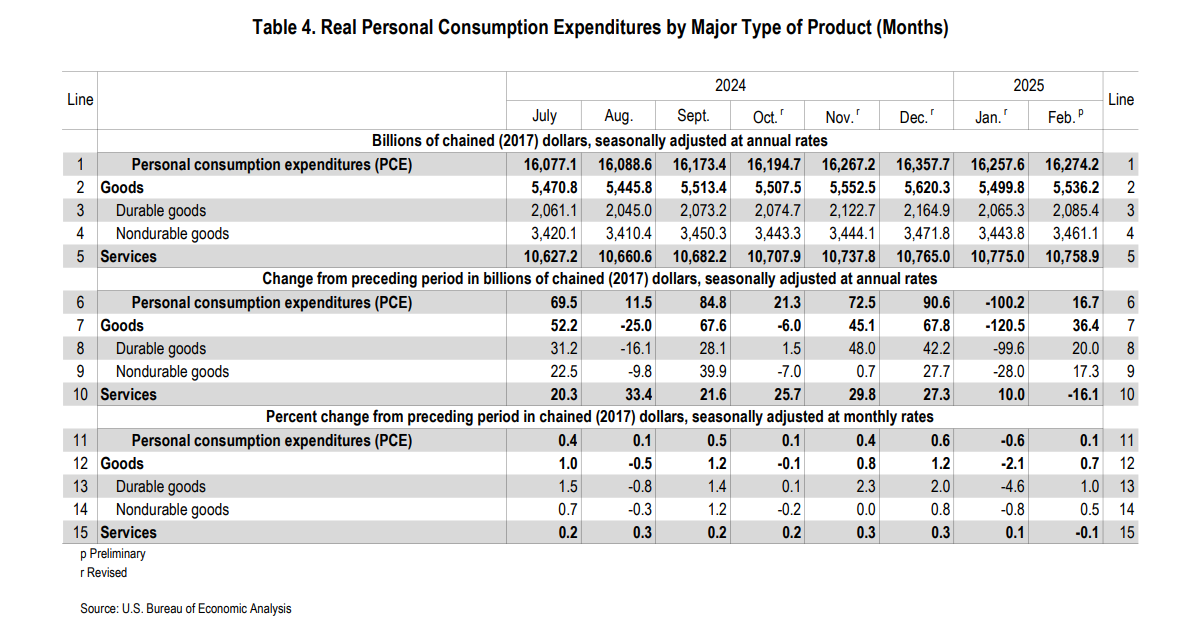

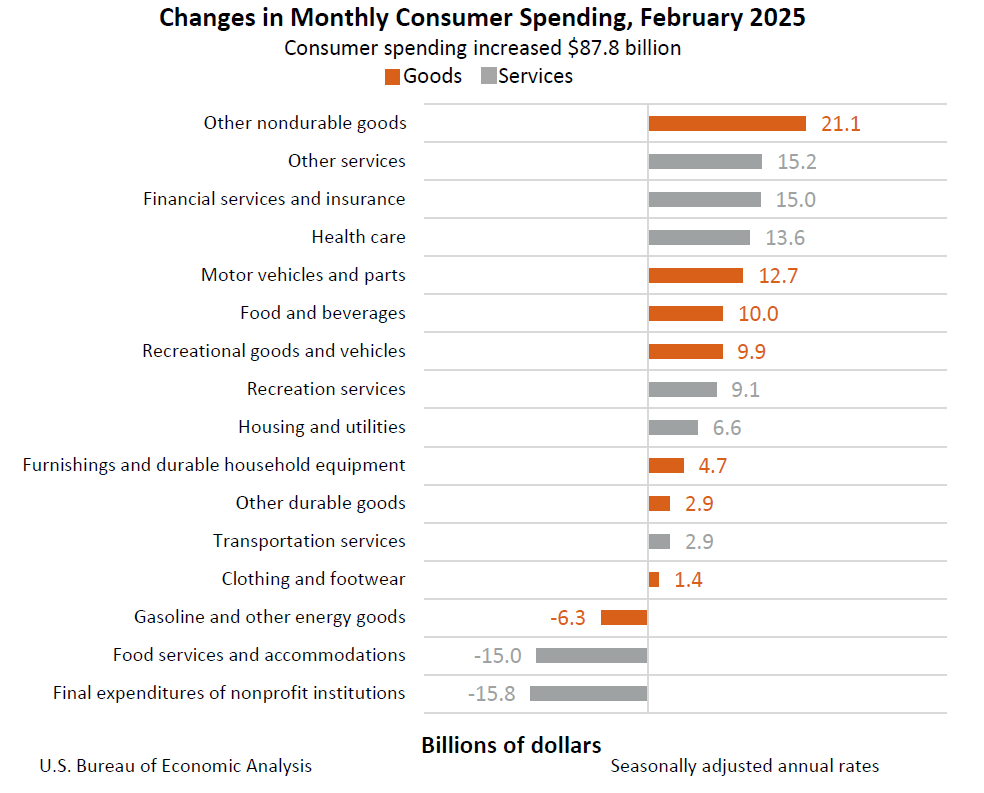

Consumer Spending Rebounded in February after the weak January, however, most of the increase is attributed to price increases and no volume.

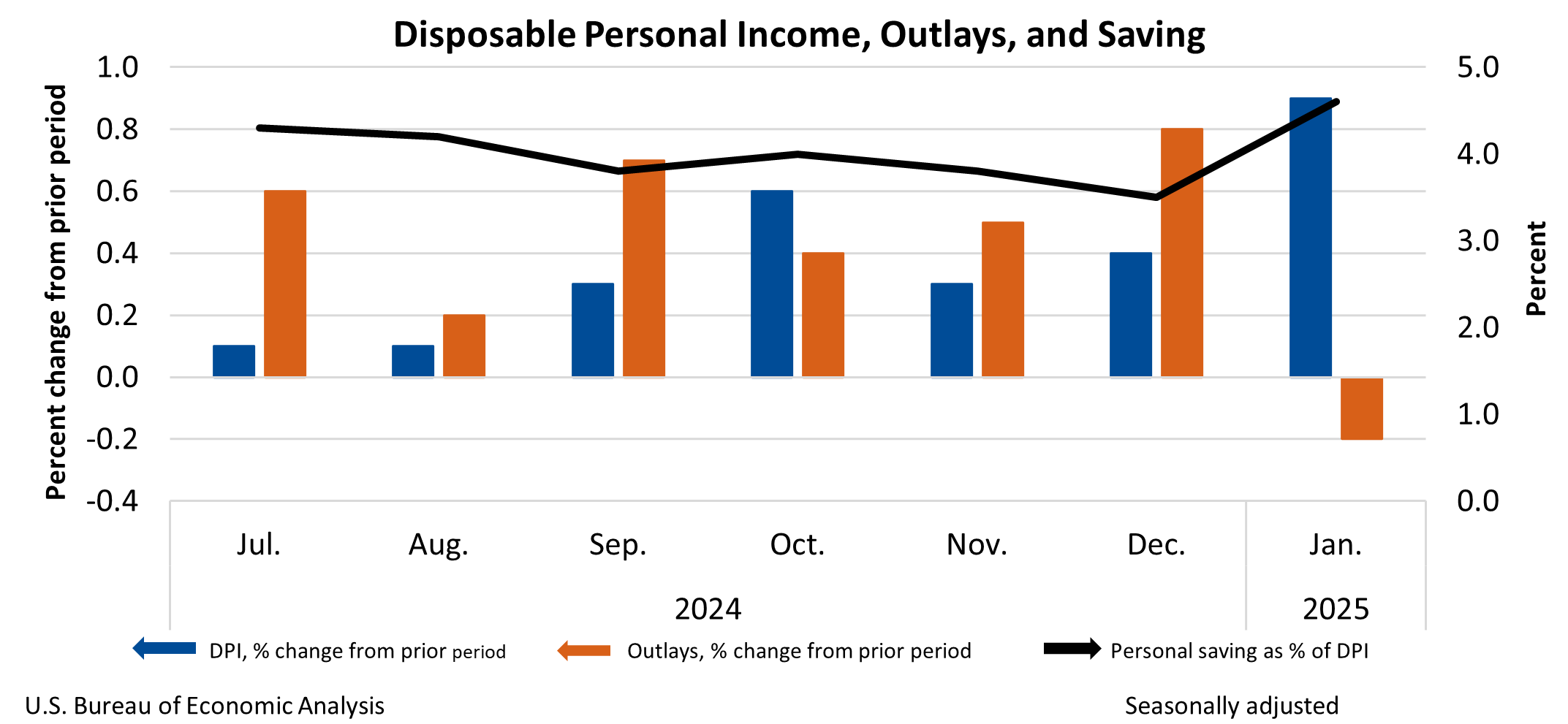

Personal Income 0.9%, vs. +0.4% est. & +0.7% prior. At 4.4% y/y

Personal Spending 0.4%, vs. +0.5% est. & -0.3% prior. Still 5.3% y/y vs 5.4% y/y prior

The savings rate surges from 4.3% to 4.6%. → Interesting trends, its common to see saving rates increasing in times of uncertainty, and if sustained could lead to lower spending

Inflation was primarily the force of the increase, without it, consumer spending was almost flat at 0.1% m/m vs 0.3% expected (vs -0.6 last month), and still 2.7% y/y.

For now, it seems will be a flat to negative quarter for consumer spending, which will flow to GDP.