This refers to loans denominated in U.S. dollars provided by financial institutions (especially global banks) to borrowers in other countries. These borrowers can include:

Corporations

Sovereign entities (governments or central banks)

Banks

Lenders are typically:

U.S. banks with foreign operations

Non-U.S. banks that borrow dollars in offshore markets (e.g. Eurodollar system)

Based on the most recent data, estimated put US dollar liabilities outside the US close to 100 trillion

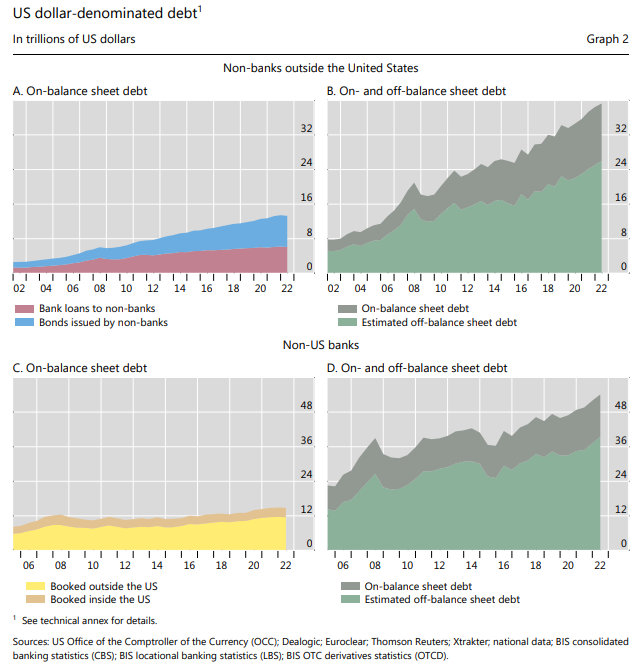

On-Balance Sheet Obligations

About 60% of international and foreign currency liabilities (primarily deposits) and claims (primarily loans) are denominated in U.S. dollars. This share has remained relatively stable since 2000 and is well above that for the euro (about 20 percent).

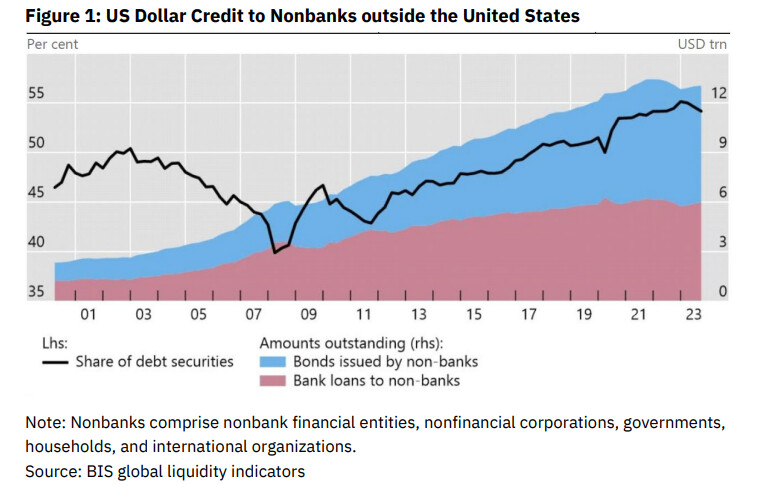

Nonbanks outside the U.S.** (e.g., corporates, governments, households):

~$13 trillion in outstanding dollar bank loans and bonds

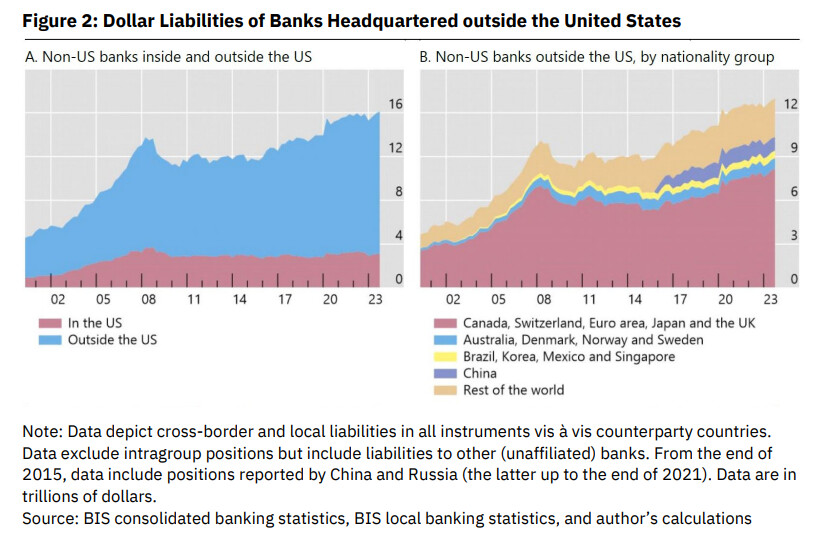

Banks headquartered outside the U.S.:

~$16 trillion in dollar liabilities (deposits and bonds)

~$13 trillion of this is booked outside the U.S., thus not directly backstopped by the Fed

~$3 trillion is booked inside the U.S. and has potential access to Fed liquidity

Off-Balance Sheet Obligations (Mostly FX Swaps)

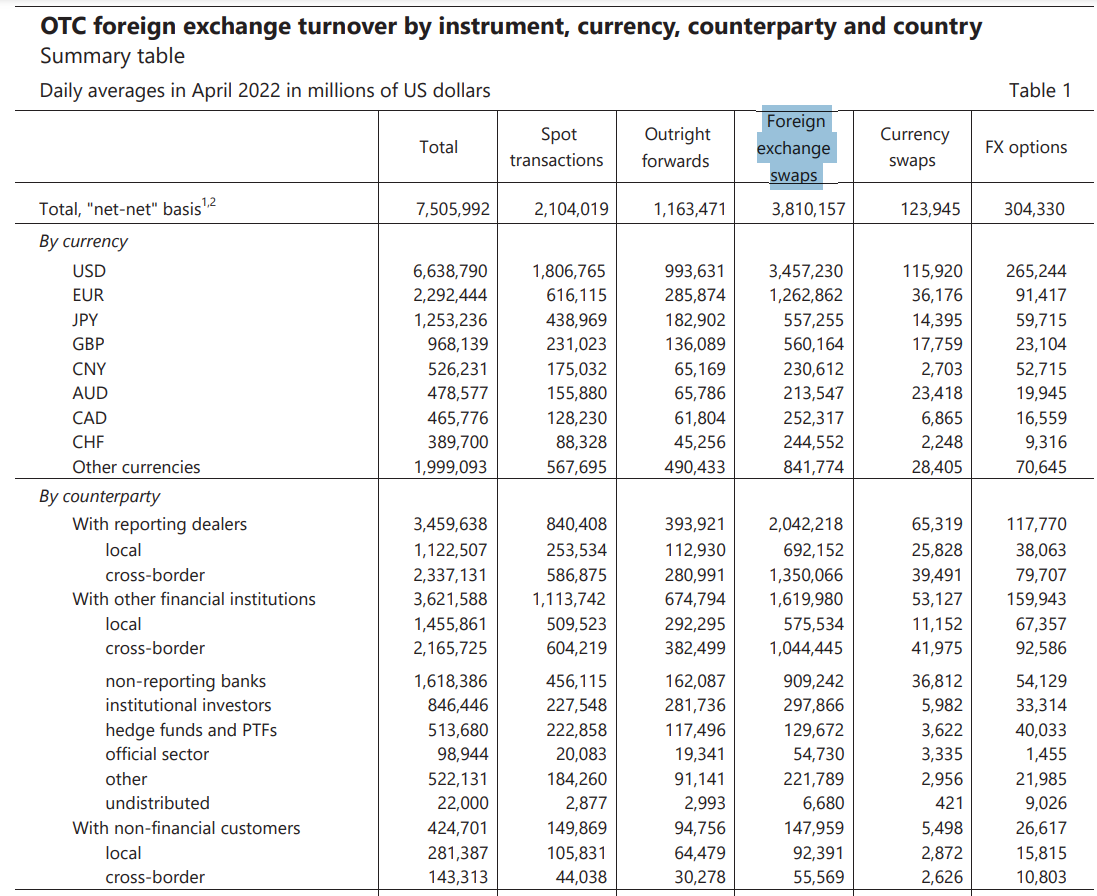

FX swap market is the largest dollar credit market, turning over $3.5 trillion per day (as of April 2022). USD is on one side of ~90% of all FX swap transactions

Nonbanks owe an estimated $26 trillion in off-balance sheet forward dollar obligations

Banks outside the U.S. owe an estimated $39 trillion in similar off-balance sheet contracts

Can you explain those FX swaps a bit better and make some practical examples? Is there data who are the counterparties in most cases and most common use cases? (Hedging, plannability of business etc)

$55 trillion between banks and non-banks and esp. $3.5 trillion per day are enormous numbers.

Can you establish how much of international business is hedged with those kind of swaps and how much is unhedged? (This might help to establish by how much business needs/settlements are driving fx ratios)

Example: Let’s assume a deal settles in e.g. dollar or any other currency that one counterparty does not want to hold longterm, which % of volume have fx swaps established to swap those dollar to their own currencies vs. which volumes need to swap dollar on the spot market and therefore driving exchange ratios?

I had asked GPT before to explain FX swaps, It is basically a contract between two parties to exchange currencies today and reverse the exchange at a specified future date at a pre-agreed rate. It is more about borrowing USD (using EUR as collateral for example), so allows institutions to borrow or lend dollars without moving on-balance-sheet debt.

And since this is mostly related to getting funding and getting dollar liquidity, this market has been central to major USD global shortage financial crisis (deepresearch from GPT). In times of stress, this is the USD global market the primarily breaks due to its short term maturity nature (2008, 2012, 2020), and the one that needs monitoring because it can cause fire sales of assets.

Use cases, there is no data how much is used for each, but since the primary counterparty are banks and financial institutions, it seems it is mostly used for funding needs to get us assets and hedging exposure.

Now, there is no data available to establish how much hedge or unhedged there is necessarily, but BIS surveys have data on the size of each FX market and the counterparties.

According to the 2022 BIS Triennial Survey, the average daily turnover in the global foreign exchange market was approximately $7.5 trillion. The breakdown is as follows:

FX Swaps: $3.8 trillion (51%)

Spot Transactions: $2.1 trillion (28%)

Outright Forwards: $1.1 trillion (15%)

FX Options and Currency Swaps: $0.4 trillion (5%)

About counterparty, it seems banks dominate the FX swap markets and FX market overall, and the corporations are only a small proportion of the total. It seems to me that most use cases go beyond business activity, and the majority of FX market flows are related to other acivites.

And for this kind of deal settlements you put as example, probably outright forwards are mostly used.