U.S. labor costs increased solidly in the third quarter amid strong wage growth latest signs that the Federal Reserve could keep interest rates high for some time.

The Employment Cost Index (ECI), the broadest measure of labor costs, rose 1.1% last quarter after increasing 1.0% in the April-June period. Economists polled by Reuters had forecast the ECI would rise 1.0%.

Wages increased 1.2% in the third quarter after climbing 1.0% in the prior three months. They were up 4.6% on a year-on-year basis after advancing by the same margin in the second quarter. Strong wage growth is being driven by worker shortages that still persist in some services industries.

There were notable increase in wages in the financial activities and education and health services sectors. But wage growth slowed in the leisure and hospitality industry, which had experienced worker shortages.

The employment Cost Index, (1 of the indicators the FED uses to asses wage growth) continued to decelerate in Q4 2023 but continues to be at a very small pace. Still above pre-pandemic levels.

The positive for consumers is the real wages are now positive.

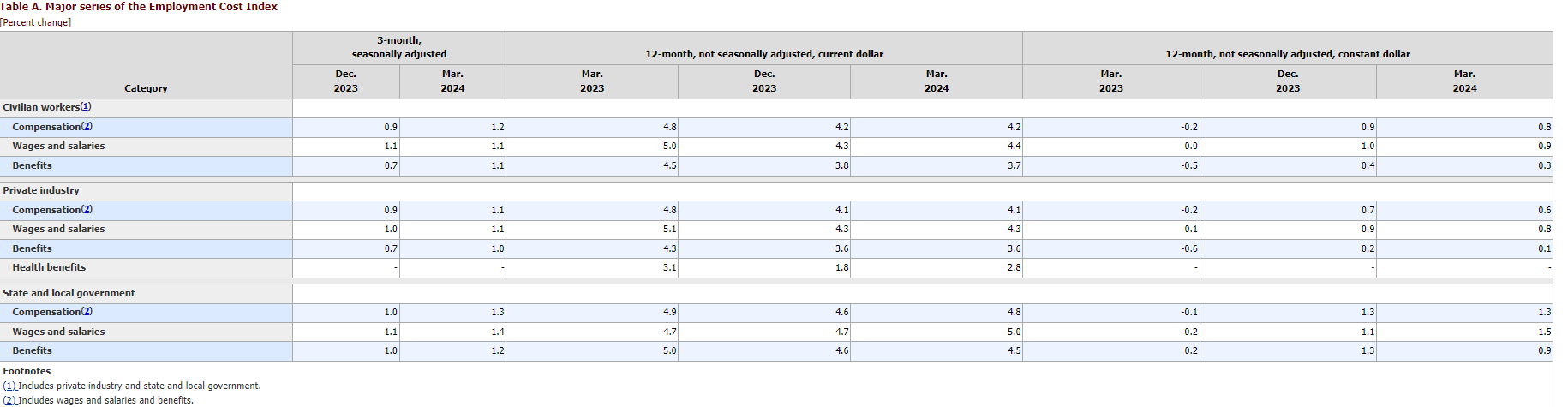

Another inflation-related metric showing a lack of improvement during Q1 2024 is the employment cost index.

The FED has mentioned they monitor this indicator closely, so is anticipated to contribute in their assessment to the already concerning inflationary trends observed this year in other areas.

The US Employment Cost Index rose by 1.2% in Q1 2024, accelerating from a 0.9% increase in the previous quarter, and beating the market consensus of a 0.9% increase.

Employment costs rose the most in one year, as wages and salaries advanced by 1.1% (vs 1.1% in Q4) and benefits increased by 1.1% (vs 0.7%)

Year over year the index came in at 4.19% vs 4.18 Y/Y in Q4 2023.