The topic focused on the developments of labor productivity in the US, and the implications this has on the economic path.

Main Article: Labor Productivity - InvestmentWiki

The topic focused on the developments of labor productivity in the US, and the implications this has on the economic path.

Main Article: Labor Productivity - InvestmentWiki

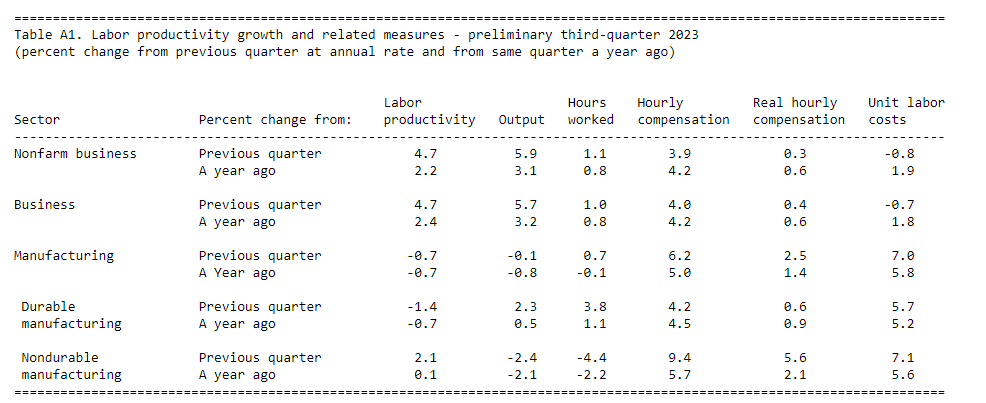

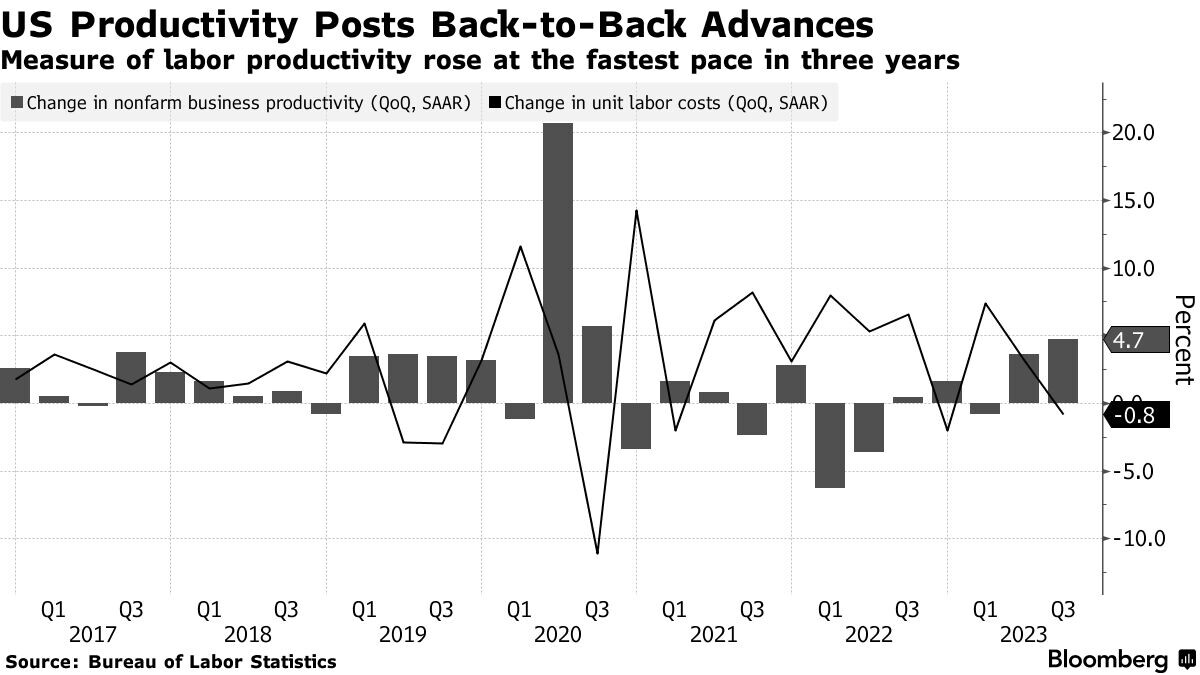

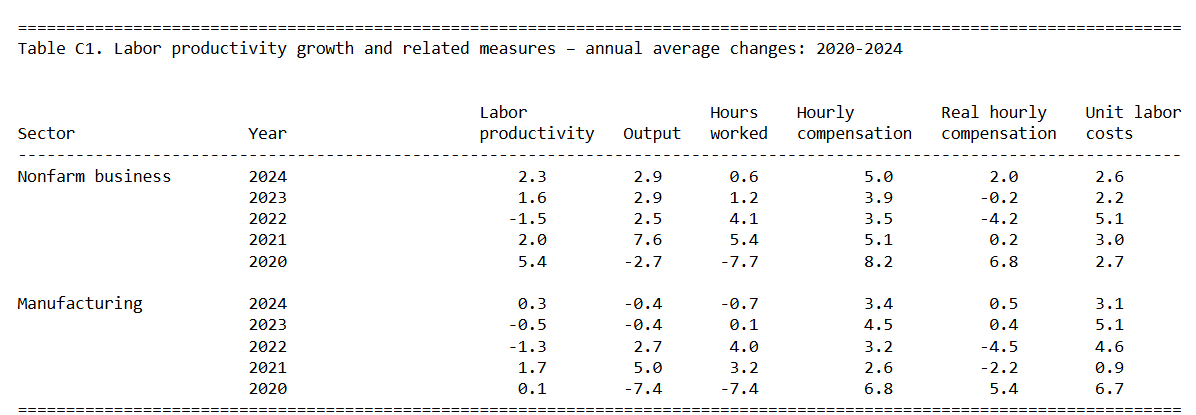

Impressive quarter in my opinion for labor productivity, nice to see, especially after a structural decline pre-pandemic. The annualized rate has been way above the average.

Manufacturing very different history to overall business too.

At this point I am not sure if this will be sustained, or just a boost after supply and all of these issues have been improving, and the cost restructuring during this year too. I will have to see more quarters coming this way to be more certain.

Very important topic. My current thesis is that advancements in productivity will help to offset problems in the labor market due to an aging population, changing supply chains etc., and therefore have an easing effect on wage growth and inflation + will help businesses to expand their margins.

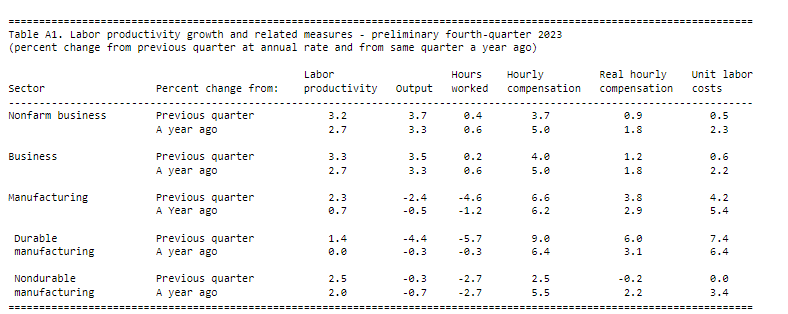

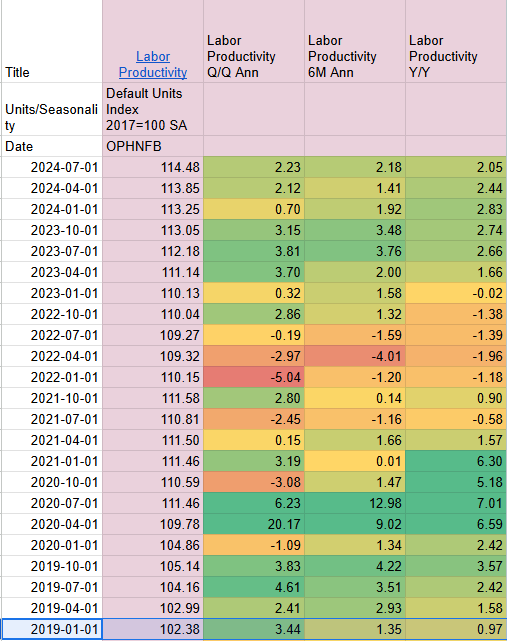

Productivity for Q4 2023 at 0.8 Q/Q ( 3.2% annu) , and 2.7% Y/Y

Declined from last quarter’s impressive numbers, is still above the average of the past years

For all of 2023, productivity was only at 1.3%.

Still think we probably need to wait until all the distortions of COVID+inflation completely pass to see where the numbers settle, since the index for now had been only recuperating the losses it had in 2022.

Same thought Powell had last conference.

https://www.bls.gov/news.release/prod2.nr0.htm

https://www.bls.gov/news.release/prod2.t01.htm

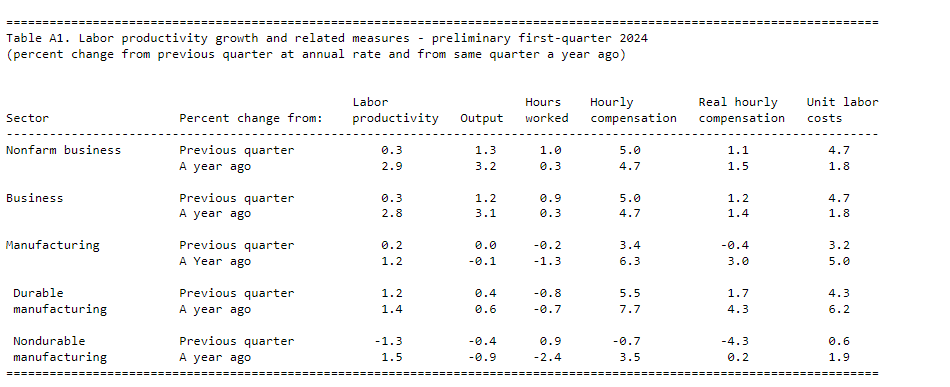

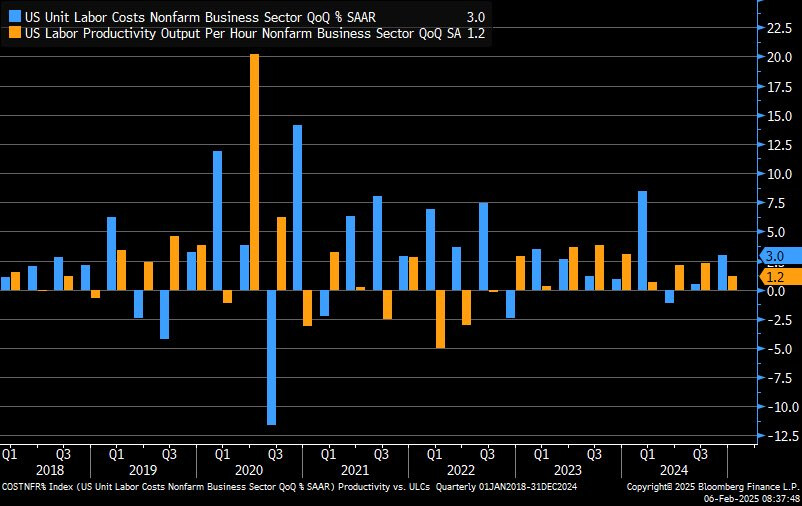

Very weak quarter for labor productivity, missing expectations that were already weak. It came only at 0.08% Q/Q (0.29 Ann vs 0.5%ann expected. It is at 2.9% Y/Y.

Unit labor cost came in high, beating expectations, 4.7% Q/Q Ann vs 4% expected and 0% in the prior quarter.

If productivity continues to ease and doesn’t pick up more from here, it will eventually impact our thesis that productivity will have a significant positive impact on growth and inflation.

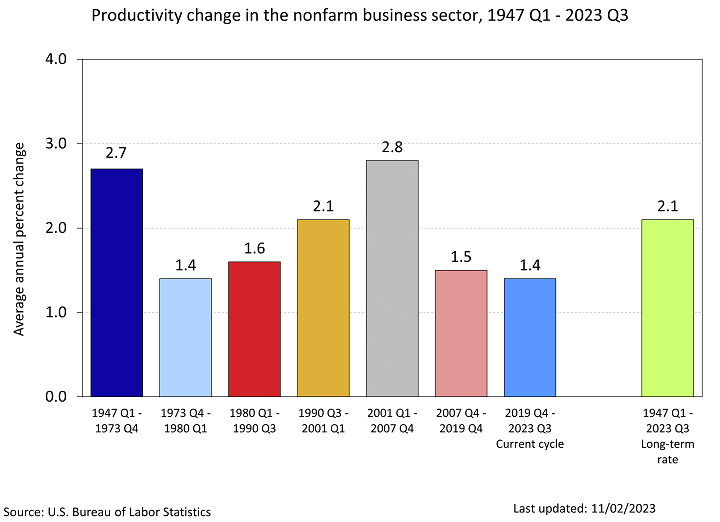

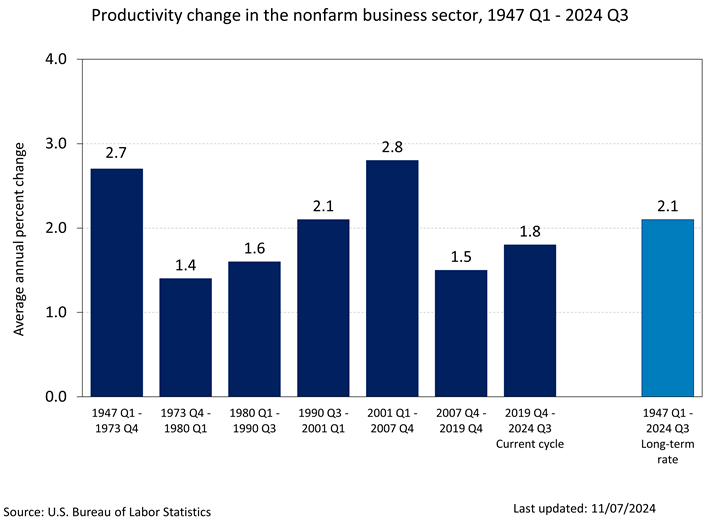

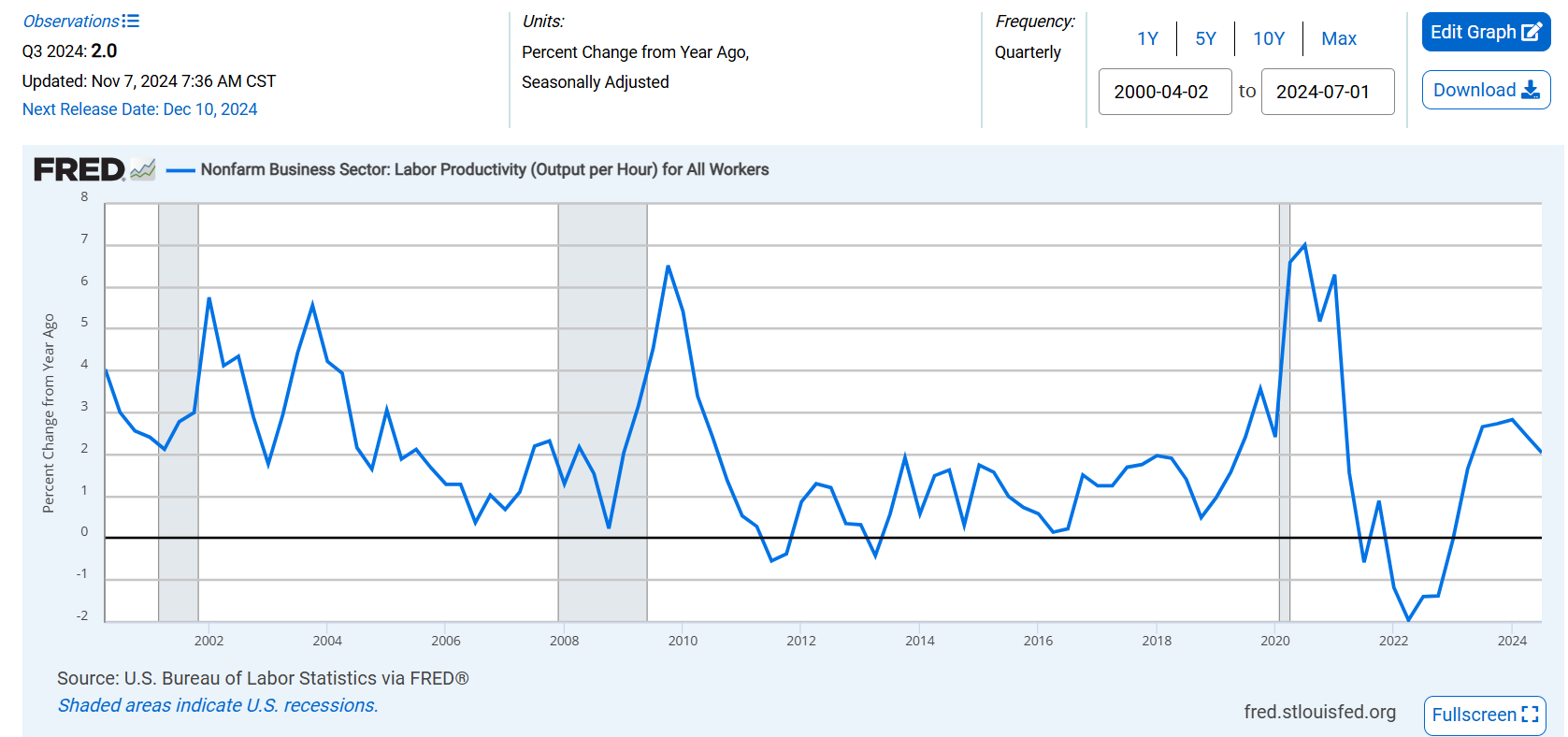

As it stands, it’s still too early to have full clarity, but I remain skeptical about the extent of near-term gains we can realistically expect. The current annual growth rate of around 2% seems insufficient for me, though it does exceed the average growth from 2007-2019. This suggests it could support a somewhat stronger trajectory than that period, yet may still fall short of delivering robust gains as everyone is expecting.

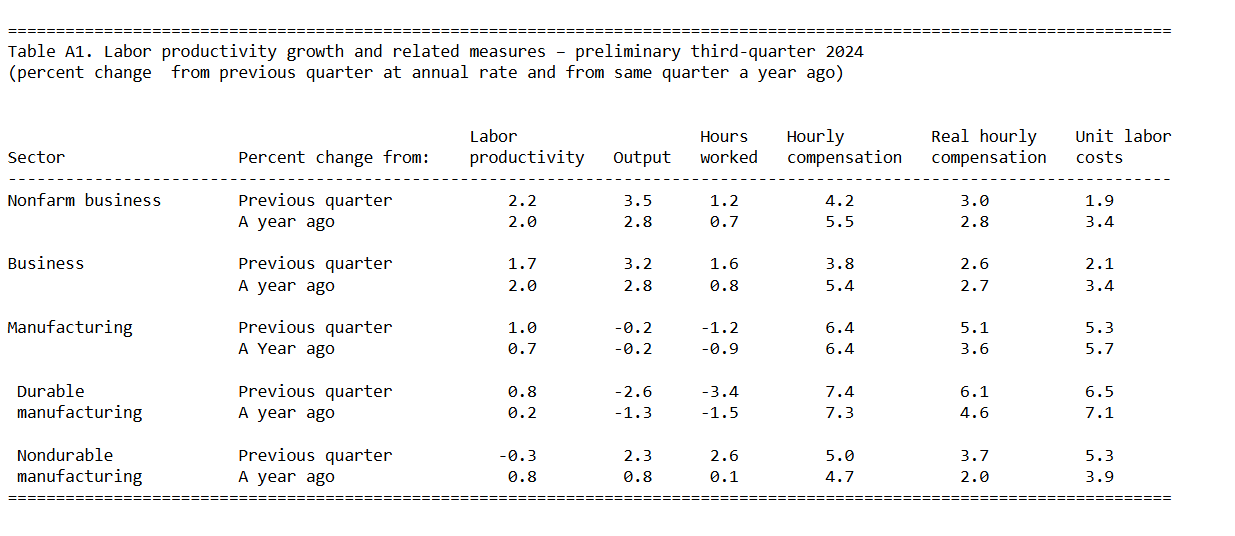

Still no clear signs of an AI productivity boom. Productivity has been above the previous cycle, but still below other historical periods of high productivity.