This topic discusses the upcoming United Internet Q4 2025 earnings, including our outlook and a summary of the results. You can find our full Notion article here:

Earnings date: March 19, 2026

Time of Earnings release: 7:30 CET

Time of 1&1 Analysts Call: 1.00 pm CET

Time of United Internet Analysts Call: 02.30 pm CET

Time of IONOS Analysts Call: 09:00 CET

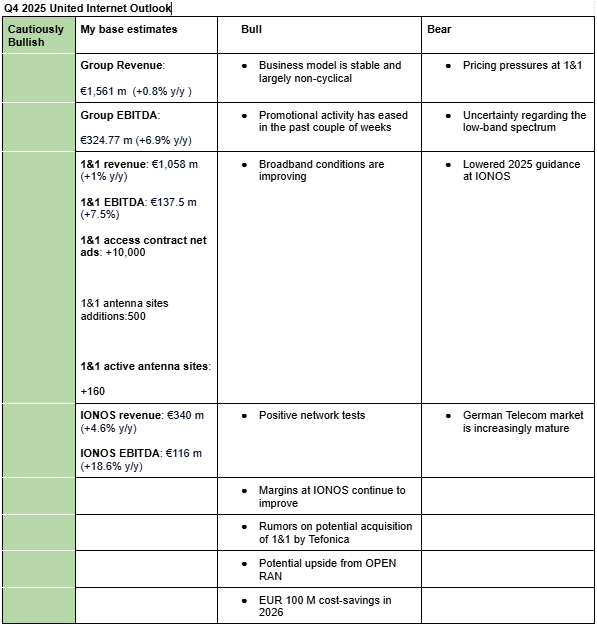

Cautiously bullish outlook on United Internet ahead of Q4 2025 earnings mainly due to current weakness at IONOS, pricing pressure at 1&1 and uncertainty on low-band frequencies

I am cautiously bullish on United Internet’s Q4 2025 earnings. My estimates (Valuation Model- Google Sheets) are based on comentaries from competitors, the fact that the industry is immune to macro pressures, guidance update by IONOS, positive network tests, end of customer migration and stable revenue from other business divisions. Here is a description of my bullish and bearish factors:

Bullish arguments

The industry is largely immune to macro pressures: United Internet has consistently maintained (page 24) that its business is non-cyclical and its performance during times of macro uncertainty confirms it. Additionally, business segments such as GMX and Web.De have stable revenue growth while 1&1 Versatile continues to expand.

Promotional activity has eased in the past couple of weeks: Deutsche Telecom and Telefonica Deutscheland pointed out in their most recent earnings call that promotional activity in Germany is starting to ease (Q4 2025 United Internet Earnings (Notion)). This positive trend should support 1&1’s pricing in 2026.

Broadband conditions are improving: Deutsche Telecom, Vodafone and Telefonica Deutschland also said broadband business conditions are improving but growth is likely to come from price increases rather than volume (Q4 2025 United Internet Earnings(Notion)). The improving trends in the broadband division are likely to boost 1&1’s revenue from 2026 as was guided by management in its Q3 2025 earnings (Notion).

Positive network tests: Third-party tests of 1&1’s network have been very positive (forum post). As such, I don’t expect any customer churn following the completion of customer migration from Telefonica Deutschland to its own network.

Margins at IONOS continue to improve: Margins at IONOS continue to improve, offeseting 1&1 network costs (Valuation Model (Google Sheets)).

Rumors on potential acquisition of 1&1 by Telefonica: United Internet and 1&1 shares have been highly volatile recently as reports indicating Telefonica is planning to acquire 1&1 keep changing (forum post). If 1&1 or United Internet confirm the potential acquisition or state that there are ongoing discussions, shares of both companies could rise sharply.

Potential upside from OPEN RAN: Even if 1&1 is not sold, we remain bullish on 1&1 OPEN RAN’s potential. OPEN RAN may materially lower costs and make 1&1’s network outperform that of rivals, leading to market share gain. In fact, it’s now emerging that one of the reasons Telefonica is interesting in acquiring 1&1 is its OPEN RAN technology (forum post). In my opinion, the fact that 1&1 now has 27% coverage (forum post) with only around 2,000 antenna sites (almost 5x comparable number from rivals) may be the first sign that its network quality is superior (to be researched further).

EUR 100 M cost-savings in 2026: 1&1 expects to save EUR 100 M in 2026 which was associated with customer migration from Telefonica Deutschland to own network in 2025 (page 7).

Bearish aerguments

Pricing pressure at 1&1: While promotional activity is starting to ease, the incumbents also noted that Q4 2025 was marked by continued pricing pressure (Q4 2025 United Internet Earnings (Notion)).

Uncertainty regarding the low-band spectrum: It’s now three months into 2026 and yet the incumbents haven’t given 1&1 access to the low-band spectrum (forum post). They were expected to avail the low-band frequencies by the end of 2025. The low-band spectrum is crucial for 1&1’s expansion since it enables it to penetrate walls. Without it, 1&1 will have to rely more on National Roaming, which is more expensive and thus limiting the upside from having own network.

Lowered 2025 guidance at IONOS: IONOS lowered its 2025 revenue guidance in December 17 by EUR 25 million due to delays in customer projects (forum post). IONOS had given new customers discount in Q3 2025 to encourage them to sign up and was expecting price improvements going forward, but this seems not to have materialized as expected (Q3 2025 United Internet Earnings (Notion)).

German telecom market is increasingly mature: Incumbents pointed out in their latest earnings that the German telecom market is increasingly mature (Q4 2025 United Internet Earnings (Notion)) as a result, strong growth at 1&1 through new contracts is unlikely in the near-term unless their is consolidation or OPEN RAN leads to material market share gain.

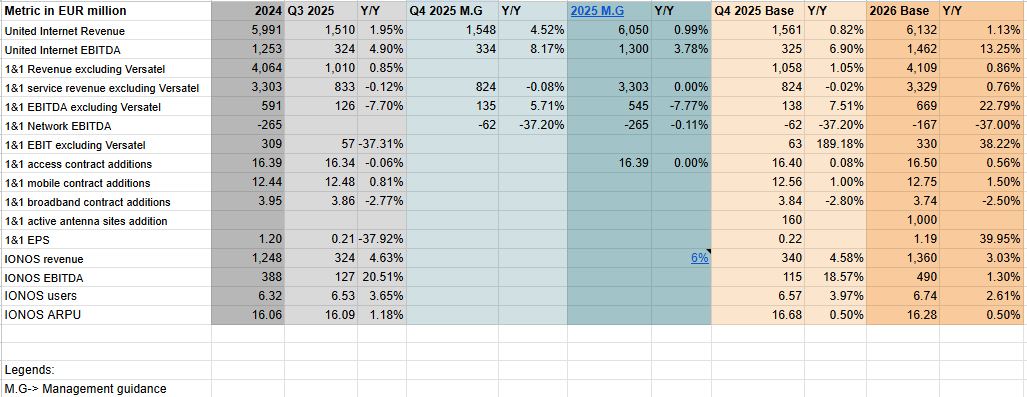

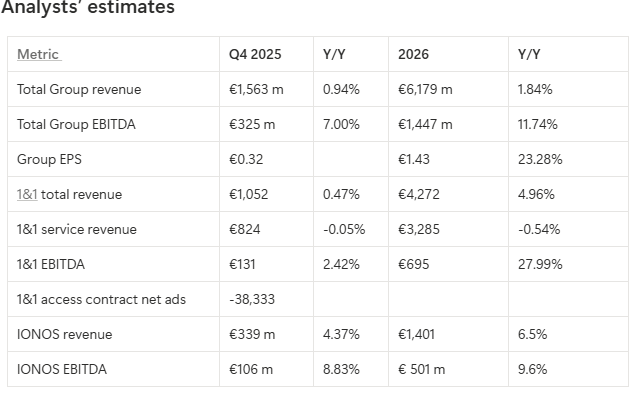

Here are analysts estimates, my estimates and management guidance for Q4 2025 and FY2026

I=10 United Internet shares rose as high as 8% on Q4 2025 revenue beat and positive commentary from IONOS

United Internet’s Q4 2025 revenue (excluding ad tech and discontinued “Energy”) rose 3.4% y/y to €1.6 billion, above management guidance of €1.55 billion (my estimate: €1.56 billion) while EBITDA rose 3.9% y/y to €316 million, below management guidance of €334 m (my estimate: €325 m).

United Internet expects 2026 revenue of €6.25 billion, above my estimate of €6.13 billion and EBITDA of €1.45 billion, roughly in line with my estimate of €1.46 billion.

1&1 (excluding Versatel) Q4 2025 revenue rose 0.4% y/y to €828 m versus management guidance of €824 m, EBITDA fell 13% y/y to €112 m (management guidance: €134 m), EPS of €0.31 was above my estimate of €0.22 due to strong tax benefit arising from acquisition of Versatel while access contracts came in at 16.32 (-70k y/y), below my estimate and management guidance of 16.40.

1&1 (including Versatel) guided 2026 service revenue of €3,662 m (flat y/y) and EBITDA of €800 m (my estimate: €851 m).

Ralph Dommermuth strongly pointed out in the earnings call that they are not planning to sell 1&1 and no discussions are going on.

United Internet, 1&1 and IONOS shares rose as high as 8%, 9% and 11%, respectively following the release of the results.

Assessment

Overall, the performance at United Internet was stable and management commentaries at IONOS was quite positive, probably explaining why their shares rose. It’s still hard to tell exactly why the shares at 1&1 rose that high. Maybe the market took the weaker than expected EBITDA at 1&1 as one of the factors that could push United Internet to sell 1&1?

Despite the stable performance at United Internet, some risks at 1&1 persist such as uncertainty on the low band spectrum and the risk that national roaming costs could remain high in the near-term since the contract with Vodafone looks a bit one-sided. Additionally, shares may be already pricing in the posibility of selling 1&1, creating some downside risk if management continues reiterating they are not planning to do so.

Given the risks above, I reiterate my hold rating on United Internet shares.

United Internet: Equal weight, €25: UBS analyst Ganesha Nagesha said EBITDA of 1&1 suffered due to roaming costs but slightly above expectations for United Internet. He expects takeover speculation for 1&1 to remain a focus.

United Internet, Buy, €34.60: Goldman Sachs said results and outlook from United Internet and 1&1 were largely reassuring.