This topic discusses Spotify’s Q4 2023 earnings. A summary of our expectations as well as the earnings results will also be posted here. You can find our earnings preparations and full summary of the results in the Wiki:

1 Like

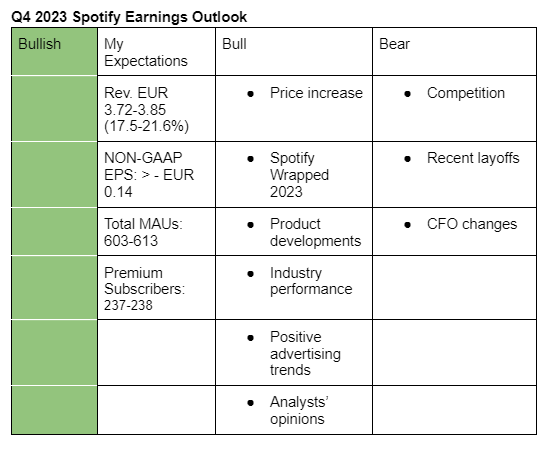

I am positive on Spotify’s Q4 2023 earnings. My guestimates are based on its past performance and business trends.

Here is why I am bullish on the quarter;

-

Price increases announced in July will likely be a tailwind to its Q4 2023 revenue growth. The management expects the price increase to be a positive mid-single-digit ARPU benefit to Q4, FX neutral.

-

Spotify Wrapped 2023 likely contributed to more engagement and user growth. According to Sensor Tower, Spotify’s global DAUs spiked by 14% DoD (2022: +13%) when Spotify 2023 Wrapped went live while global downloads rose by 35% DoD (2022:+23%). Spotify acknowledged in Q4 2022 earnings that Spotify Wrapped 2022 contributed to their Q4 success.

“A notable call out in the quarter was our eighth annual Wrapped campaign, which was a big contributor to our Q4 success, and we broke all sorts of records and reached several all-time highs with an increase of over 30% in user engagements,” CEO Daniel EK said.

-

I expect product developments such as Daylist, AI DJ and the addition of audiobooks to the premium subcription to have contributed to more engagement and user growth during the quarter.

-

Global revenue forecast for 2023 was revised upward while 22% growth in on-demand audio song streams for 2023 (reported in Q3 2023) was unchanged at the end of the year.

-

Spotify’s ad business probably benefitted from the ongoing improvement in advertising trends. Meta Platforms and Alphabet recently posted positive ad growth results.

-

Analysts seem to have moved beyond Q4 2023 and are now forecasting solid performance in 2024.

Some of concerning areas include;

- The recent layoff may indicate impending slowdown in revenue growth; hence (though low), the company’s outlook for 2024 could come below estimates. This could cause a drop in the stock price.

- Growing competition, particularly from YouTube Music. Recently, YouTube announced that its YouTube Music and Premium subscribers had crossed 100 million. That’s up from 80 million announced in November 2022 and 50 million given in September 2021.

- The company hasn’t found a new CFO. Hence the perfomance of the department may not be optimal.

N/B:

Management Guidance: Revenue (3.7 billion or +16.9%), MAUs (601 million), Premium subscribers (235 million)

Analysts estimate (revenue): 3.72 billion (+17.5%)

2 Likes

Good overview.

What is your base case for the strength of the Q1 outlook? Do you think Netflix strong performance is a positive indication for Spotify or not?

I think so. Both are in the same sector, hence follow similar consumer trends.

I think they will give a strong outlook for Q1 given continued tailwind from price increase and further growth in the number of users due to its AI products which received a boost from the Spotify Wrapped 2023. Q1 2024 will also benefit from weak comparisons in the prior period.

- Revenue grew 16% y/y to 3.67 billion euros while GAAP EPS was -0.36 euros, both missing analysts’ estimates of 3.72 billion euros and -0.31 euros, respectively.

- Premium subcribers increased by 15% y/y to 236 million while monthly active users (MAUs) was up 23% y/y to 602 million, both beating management guidance of 235 million and 601 million, respectively.

- Operating loss was -75 million euros, below mid-point management guidance of -100.5 million euros while gross margin came in 26.7%, above management guidance of 26.6%.

- Excluding €143 million associated with efficiency efforts announced at the end of Q4, operating income could have been 68 million euros.

- Management is guiding Q1 2024 revenue of 3.6 billion euros (analysts’ estimate: 3.637 billion), premium subcribers to reach 239 million (analysts’ estimate: 238.3 million), MAUs of 618 million (analysts’ estimate: 618.8 million) and operating income of 180 million euros (analysts’ estimate: 82 million).

1 Like

Why the positive reaction today? Seeing only the numbers they don’t see that impressive against expectations.

Is it only for the operating income?

Yes, it’s a profitability story, but I also did not like the weak premium sub-guidance.

The other question is always the degree to which the increased profitability was already factored into the stock, given that changes that lead to more profitability were announced a while ago.

I sold my Spotify position after earnings for the following key reasons

2 Likes