Meta just reported one of the most impressive quarters I have ever seen in 8+ years.

Congrats to @Aron and @Magaly for pointing out the difference between search and social media and correctly predicting a strong quarter.

While Aron is going to report numbers and details of the conference call, here are two highlights I want to mention

Meta is actively working on general intelligence and models that can “reason, plan, code, remember and many other cognitive abilities”. The company appears to be running & performing extremely well on all fronts.

Here is what they imagine:

Everyone who uses our services will have a world-class AI assistant to help get things done, every creator will have an AI that their community can engage with, every business will have an AI that their customers can interact with to buy goods and get support, and every developer will have a state-of-the-art open-source model to build with.

Impressive growth in the quarter, but more importantly, a very strong outlook for Q1 makes EPS of $20 in 2024 achievable. Furthermore, Meta wants to maintain its financial discipline even if it continues to grow in the future, which could lead to margin expansions and EPS of $30+.

Assessment

I continue to believe that Meta is extremely well positioned for AI given the large number of people that are spending hours in their apps while liking, scrolling, messaging, saving content and giving other kinds of signals to their AI. In fact it is probably the company which is worldwide best positioned for training inputs.

Here are Meta’s comments about it

But even more important then the upfront training corpus is the ability to establish the right feedback loops with hundreds of millions of people interacting with AI services across our products. And this feedback is a big part of how we’ve improved our AI systems so quickly with Reels and Ads.

Therefore, I think the stock still holds significant fundamental upward potential. In addition, it could get ahead of its fundamental valuation at one point and reach “bubble territory,” given that the AI narrative is so compelling. In that regard, I found Meta’s comments that they want “additional flexibility” on how to distribute capital with dividends interesting, as it does not make sense to buy back shares if the stock is overvalued.

Revenue grew by 25% y/y to $40.11 billion, in line with management’s upper guidance of $40 billion (+24.3%) and above analysts’ estimate of $39.09 billion (+21.5%).

Earnings per share was $5.33 versus $4.99 analysts’ estimate while operating margin rose to 41% from 20% a year ago.

The average Family daily active people (DAP) rose 8% y/y to 3.19 billion (analysts’ estimate: 3.11 billion) while Family monthly active people (MAP) increased by 6% to 3.98 billion (estimate:3.93 billion).

The company increased its share repurchase authorization by $50 billion and initiated a quarterly dividend of $0.50 per share.

Meta is guiding Q1 2024 revenue of $34.5-37 billion (expectations: $33.61 billion), maintaining their earlier guidance of full-year 2024 total expenses ($94-99 billion) but increasing their 2024 capex guidance by $2 billion at the upper end to $30-37 billion on anticipated increase in investments on servers and data centers.

Here are additional insights from the earnings call;

Meta expects advertising strength to continue and its ad investments to pay off.

“On your second question, which is about the Q1 year-over-year – sorry, the Q1 revenue guide. This really just reflects a lot of the trends we saw in Q4, which is strong, broad-based advertising demand across verticals, particularly within online commerce and gaming. I’ll also note that we get the benefit from having February 29th in this quarter. And again, just the improvements that we continue to accrue to the business from all of our investments in improving ad performance over time,” CFO Susan Li said.

In 2023, China-based advertisers represented 10% of Meta’s overall revenue and contributed 5% to the total worldwide revenue growth.

Reels is now contributing to net revenue across Meta’s apps and the company is now focused on improving their recommendations.

In Q4, ad impressions grew by 21% driven by Asia-Pacific and Rest of World while the average price per ad increased by 2% " driven by advertiser demand and currency tailwinds, which were partially offset by strong impression growth, particularly from lower-monetizing surfaces and regions."

WhatsApp is succeeding more broadly in the United States; hence a huge opportunity given that the U.S. is an important contributor of revenue.

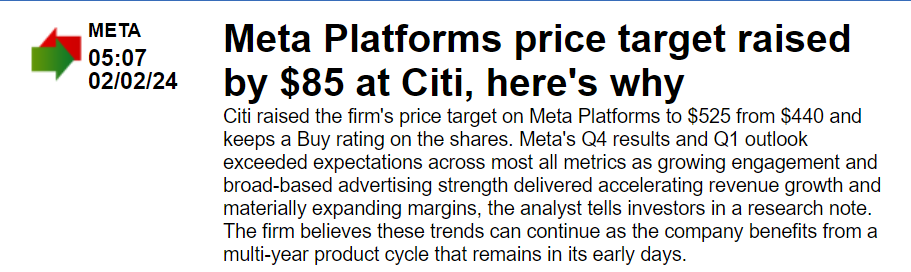

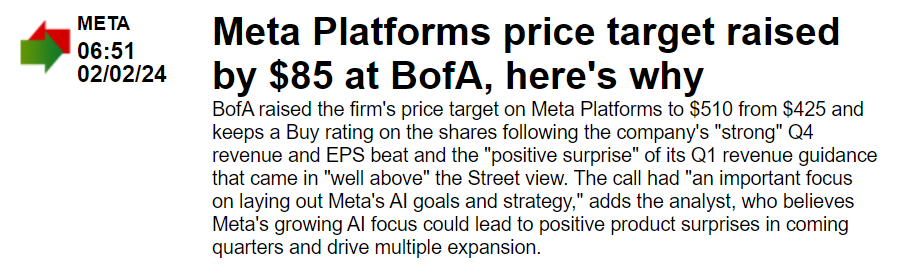

Buy, $425->$510: Bofa calls the Q1 guidance a positive surprise and believes Meta’s increasing AI focus could lead to new product releases in the coming quarters.