This topic discusses the upcoming United Internet Q3 2025 earnings, including our outlook and a summary of the results. You can find our full Notion article here:

Earnings date: November 11, 2025

Time of Earnings release: 7:30 CET

Time of 1&1 Analysts Call: 10:30 am CET

Time of United Internet Analysts Call: 12:00 AM CET

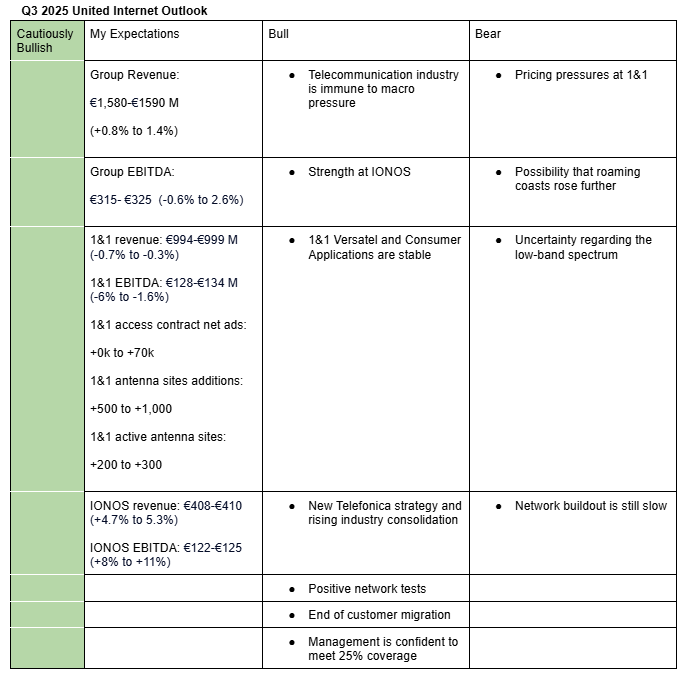

I am cautiously bullish on United Internet’s Q3 2025 earnings. My estimates (Valuation Model- Google Sheets) are based on recent performance trends, the fact that the industry is immune to macro pressures, strength at IONOS, positive network tests, end of customer migration and stable revenue from other business divisions. Here is a description of my bullish and bearish factors:

Bullish aerguments

Telecommunication industry is immune to macro pressure: The telecommunication industry is largely immune to macro pressure since people cannot do without calls or mobile data. Similarly, United Internet’s business is largely non-cyclical. Therefore, the slowdown in Germany’s economy is unlikely to have much impact on United Internet’s operating performance.

Strength at IONOS: I expect the almost revenue flat growth at 1&1 to be compensated by revenue growth at IONOS (Valuation Model- Google Sheet).

1&1 Versatel and Consumer Applications are stable: 1&1 Versatel and Consumer Applications (GMX and WEB.DE) are showing stable revenue and EBITDA growth trends. United Internet continues to make investments in Consumer Applications that should lead to margin expansion in the near-term (Valuation Model-Google Sheets).

New Telefonica strategy and rising industry consolidation: Reports (forum post) indicating that Telefonica plans to improve its relationship with 1&1 is positive for the Group. For instance, even if there won’t be any acquisitions, it raises the chance that Telefonica will be more willing to avail low-band spectrum to 1&1 at favorable conditions. Personally, I see the possibility of Telefonica acquiring 1&1 as low given that it’s Dommermuth’s legacy and the fact that financial conditions are unlikely to be favorable to Telefonica given continued earnings pressure from the loss of 1&1. I think the most likely scenario is Telefonica taking stake in 1&1 Versatel. My theory is based on Telefonica’s “Transform and Grow” strategy (Notion) where the CEO gave emphasis to growing their broadband business. Rising industry consolidation in Germany also gives United Internet the opportunity to dispose of some of its business units, leading to a more leaner structure and improved earnings multiples.

Positive network tests: Recent tests on 1&1 network by IMTEST and Chip found that 1&1 network is much better than many people think. While the network trailed that of incumbents, tests results were largely good (forum posts).

End of customer migration: With customer migration largely complete (forum post), customer churn is likely to be lower in Q3 compared to the first half. Management expects a little bit of growth in Q3 and Q4 as a result of the conclusion in customer migration.

Management is confident to meet 25% coverage: In a recent letter to BNetZa, 1&1 management reiterated that they are confident they will meet 25% coverage and said network expansion is progressing well (forum post). While 1&1 only added 200 new active sites in Q2 2025, taking the total number of actives to 1,200, it has a huge pipeline of antenna sites (5,800) (Notion). Based on these developments, I now believe 1&1 might actually meet the target. I also like that BNetzA was able to extend 1&1’s dateline to meet the minimum coverage in each federal district as it signals openness to do it further. 1&1 needs 6,000-6,500 active antenna sites by the end of 2025 to achieve 25% coverage and meet BNetZa obligations.

Bearish arguments

Pricing pressure at 1&1: I expect continued pricing pressure at 1&1 due to aggressive competition in the industry. Both O2 (Notion) and Freenet (Notion) flagged aggressive competition in Q3 2025. For instance, O2 reported that average revenue per user (ARPU) was down 1.5% y/y in Q3 (Q2 2025:-1.1%) (Notion).

Possibility that roaming costs rose further in Q3: There is a risk that roaming costs may have risen further in Q3 due to network expansion that is still slow. Also, according to Chip, roaming in Vodafone network is “normal” in most cases i.e. around 88% of internet browsing tests and 90% of phone calls were made in roaming mode. Similarly, Dommermuth warned in Q2 (Notion-Q2 2025 earnings) that if the network grows more slowly than expected, they will have to buy more capacity from Vodafone.

Uncertainty regarding low-band spectrum: Recent reports (forum post) indicate that 1&1 is concerned about the ongoing negotiations with the incumbents regarding the shared use of low-band spectrum, saying negotiations are progressing “very slowly”. If there is a delay in getting the low-band spectrum, 1&1 will incur more costs since it will have to rely more on national roaming.

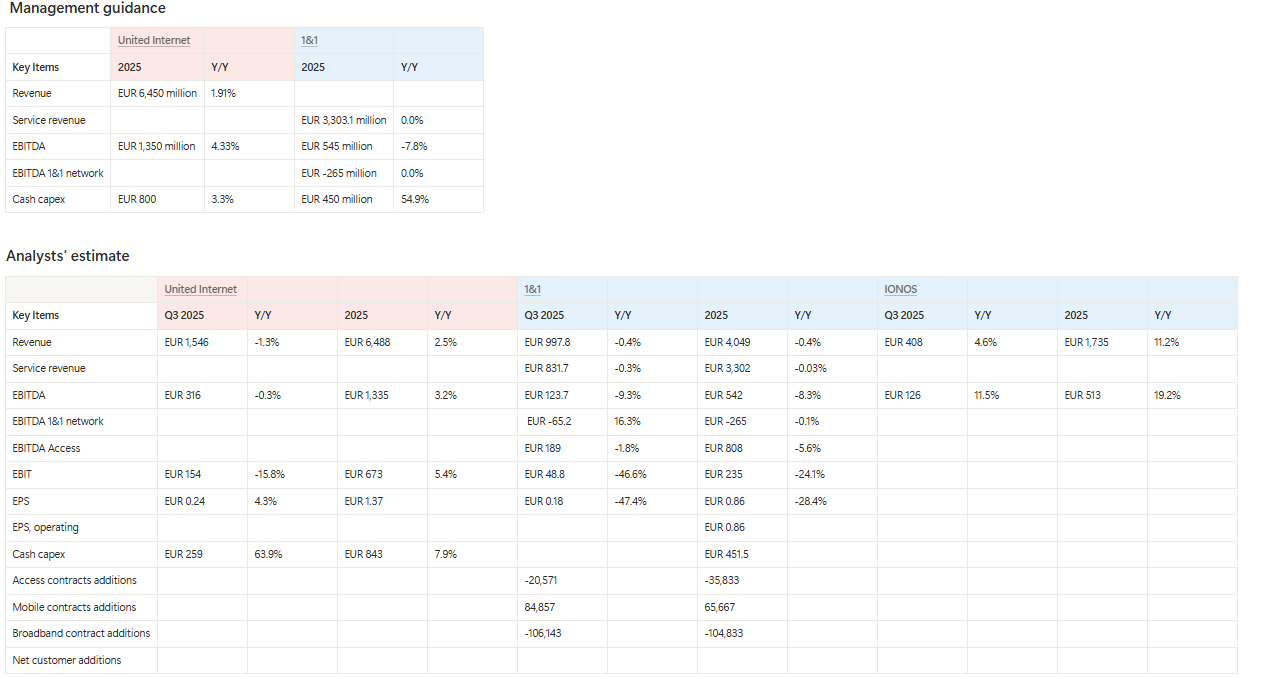

Here are analysts estimates and management guidance for Q3 2025 and FY2025 (Notion):

Recommendation

Given the low-band spectrum uncertainty and the lack of confirmed data on current network-buildout progress, I assign United Internet shares a “Hold” rating.

I=10 United Internet shares shed 7% as AdTech revenue falls 66% y/y and IONOS unexpectedly discontinues it

United Internet’s Q3 2025 (including discontinued AdTech division) revenue fell 2% y/y to EUR 1,537 million (calculated in Valuation Model)-driven by 66% y/y decline in AdTech revenue to EUR 28 million (IONOS key figures), below analysts estimate of EUR 1,546 million while EBITDA rose 1.6% to EUR 322 million, above analysts estimate of EUR 316 million.

United Internet said excluding the AdTech business (Sedo), they continue to expect 2025 revenue of EUR 6,050 million and EBITDA of EUR 1,300 million, but lowered 2025 cash capex guidance to EUR 750 million from 800 million due to phasing of some projects to Q1 2026.

1&1’s Q3 2025 revenue was up 0.9% y/y to EUR 1,009.8 million, above analysts estimate of EUR 997.8, EBITDA fell 7.7% y/y to EUR 125.9 million (analysts’ estimate: EUR 123.7 million), EBIT decline 37.3% y/y to EUR 57.3 million (analysts’ estimate: EUR 48.8), EPS was EUR 0.21 (analysts’ estimate: EUR 0.18) while access contracts fell 0.1% y/y to 16.34 million (analysts’ estimate: 16.33 million).

1&1 reiterated its 2025 guidance which includes service revenue of EUR 3,303.1 million (unchanged from 2024), EBITDA of approximately €545 million (2024: EUR 590.8 million), EBITDA in access segment of around €810 million (2024: €856.1 million), and 1&1 network EBITDA of approximately -€265 million (2024: -€265.3 million). It lowered cash capex to EUR 400 million from EUR 450 million due to phasing of some projects to Q1 2026.

1&1 said in the earnings call (Notion Q3 2025 real time earnings call) that it now has 1,500 active antenna sites (at the upper point of our estimate) and 4,500 sites under development (min 4:49).

United Internet CFO said in the earnings call (Notion Q3 2025 real time earnings call) that they are confident they will achieve 25% coverage at the end of 2025 and that they will need 2,000 active sites to achieve this coverage given their network is high-performance (min 30:16).

United Internet CFO also said in the earnings call that they are quite suite they will get the low-band spectrum in Q1 or Q2 2026 and not at the end of 2025 since negotiations are still ongoing (min 15:12).

United Internet CFO also said that no one has showed up (including Telefonica) regarding consolidation of 1&1 and that they are open to have a conversation as always (min 22:52).

1&1 CFO said competition remains intense in Germany (min 1:20).

Assessment

United Internet shares were down 7% while IONOS shares were down 10% at one point after the earnings probably due to the skepticism surrounding the collapse in AdTech revenue (-65% y/y) and the decision by IONOS to discontinue it unexpectedly. Management had guided flat revenue growth in the AdTech business in the second half of 2025, after very strong development in first half but is now saying the EUR 400 million guidance for 2025 may not be achieved. There is also uncertainty on whether and when IONOS will find its buy, given Q3 revenue and earnings development in the division. In my opinion (theory), the huge underperformance of the AdTech business may explain why IONOS CFO is leaving.

Overall, excluding the impact from the AdTech business, United internet’s revenue and earnings developed well.

The company’s announcement that it will only need 2,000 active sites to achieve 25% coverage largely diminishes the risk associated with coverage obligations. I think their estimate could be genuine (confidence level: 65%) given that 2025 and 2030 obligations do not specify (see except below) the exact requirements in terms of coverage and quality (Notion- antenna sites obligation). . More research on this area will improve my confidence level.

“It is not appropriate to impose on new entrants a more exacting requirement in terms

of household coverage, quality and transport routes – as was called for in the

responses – because, unlike existing network operators, they do not already have the

necessary infrastructure. In particular, there are at present no frequencies below

1 GHz available to new entrants that would enable them to roll out cost-effective

broadband nationwide,” BNetzA said.

I think the main risk at the moment is the issue of low-band spectrum since a delay in getting it will delay cost savings.