This topic covers Sixt’s Q3 2025 earnings. A preview of the results will be posted here ahead of the earnings release. A full summary of the preview is available in the Notion:

Earnings date: November 13, 2025

Time of Earnings release: 7:30 CET

Time of Analysts Call: Unknown

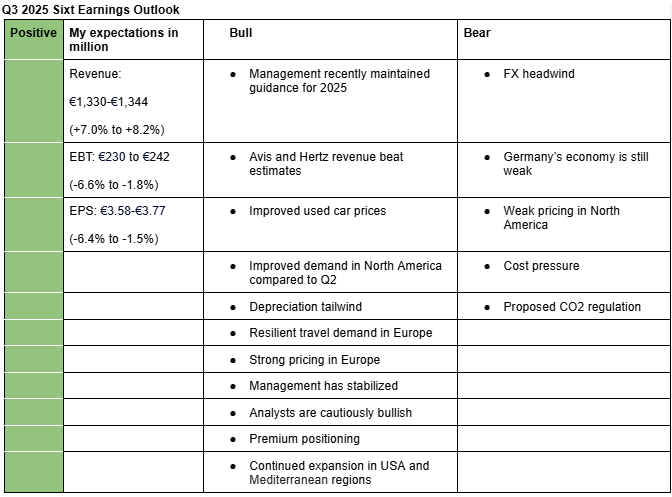

I am positive on Sixt’s Q3 2025 earnings. My estimates (Valuation Model) take into account resilient car rental demand in Europe, recent management guidance update, revenue beat by Avis and Hertz, continued expansion in USA and Mediterranean regions, premium positioning, FX headwind, etc. Given this positive outlook, I have a buy rating on Sixt shares. Here is a description of my bullish and bearish points.

Bullish arguments

Management recently maintained guidance for 2025: During Sixt’s investor presentation held on September 22, 2025, management reiterated that it expects 2025 revenue to grow in the range of 5%-10% y/y and EBT margin of around 10%. In the past, Sixt could update its guidance a few weeks to the earnings if it expected results to develop badly. As such, I expect that Sixt is on track to meet its annual targets (Sixt’s September 22 Investor Presentation (page 20)).

Avis and Hertz beat revenue estimates: Avis’s (Notion-Avis Q3 results) and Hertz’s (Notion-Avis Q3 results) Q3 revenue were $60 million and $50 million higher than estimates respectively, sending a positive signal for Sixt.

Improved used car prices: Used car prices continue to rise y/y in Europe (forum) and USA (forum). Europe used car prices rose by an average of 2.9% y/y in Q3, according to Auto1 Group. Similarly, U.S. used car prices rose by an average of 2.2% y/y, according to Manheim Used Vehicle Value Index. Improving used car prices help Sixt get better terms when selling vehicles, hence reducing depreciation rate.

Improved demand in North America compared to Q2: Hertz pointed out in the earnings call that travel demand improved in Q3 compared to Q2 (Notion-Avis Q3 earnings call). Similarly, Delta Airlines and United Airlines pointed out that demand picked up in Q3 and that premium segment were the main driver of revenue growth in Q3 (forum).

Depreciation tailwind: Sixt completed the sale of vehicles that were impacted by weak used car prices in Q1 2025 (forum). As such, Q3 2025 depreciation should also drop significantly. Avis (Notion-Avis Q3 results) and Hertz (Notion-Hertz Q3 results) also reported a 16% and 48% drop in depreciation per unit per month (DPU), respectively.

Resilient travel demand in Europe: According to ACI, Europe passenger traffic rose 3.9% in Q3 2025. However, this was a deceleration from the 4.5% and 4.6% registered in Q1 and Q2 respectively (forum). Travel demand in Mediterranean regions remains strong. According to Greece’s business magazine ekathimerini, searches for short-term rentals in countries, such as Spain, Italy and Greece, rose 35% y/y in the 9 months of 2025 (Notion-insights on travel demand in Mediterranean regions)

Strong pricing in Europe: Avis (Notion-Avis Q3 results) and Hertz (Notion-Hertz Q3 results) reported a 9% and 2% growth in international revenue per day (RPD), respectively. Given that majority of their international revenue comes from Europe, it signals that pricing in Europe was strong during the quarter. Additionally, Deutsche bank analyst Michael Kuhn pointed out that daily prices were strong in Europe in Q3 (Notion-Analysts opinions).

Management has stabilized: Overall, senior executive turnover has been low in 2025 following elevated churn in 2023–2024. While employee reviews remain largely negative, criticism now focuses mainly on high pressure and understaffing rather than widespread turnover. The persistent intensity appears consistent with Sixt’s high-performance culture rather than a new deterioration (forum).

Premium positioning: Sixt’s 57% share of premium vehicles should help it withstand macro pressures (forum)

Analysts are cautiously bullish: Analysts largely expect Sixt to meet its 2025 guidance but flag some issues such as cost pressure and subsdued economic situation in Germany(Notion-Analysts opinions)..

Continued expansion in USA and Mediterranean regions: Sixt is continuing its expansion in the U.S., particularly across major airport locations, while also adding new stations in key Mediterranean markets. For instance, in Q2 2025, the company opened five new locations in Italy (Sixt LinkedIn post). These additions are expected to be revenue-accretive in Q3 2025.

Bearish arguments

FX headwind: I expect FX to be the major headwind for Sixt in Q3. In Q2 2025, Sixt reported FX headwind of around 6.2% due to the strengthening of the Euro against USD (forum). I expect FX headwind of 7.6% in Q3 due to further strengthening of the Euro against USD (FX headwind estimate-Google Sheets).

Germany’s economy is still weak: Germany’s economy growth rate was flat in Q3 2025 (Q2 2025: -0.2%), signaling continued weakness in one of Sixt’s largest markets (forum).

Weak pricing in North America: Avis (Notion-Avis Q3 results) and Hertz (Notion-Hertz Q3 results) reported a 3% and 5% drop in America revenue per day (RPD) respectively, indicating that while demand improved, overall revenue growth rate may not improve much.

Cost pressure: Sixt personnel expenses rose 8% in Q2 2025 due to wage and salary increases and higher ancillary personnel costs (Valuation Model-Google Sheets). It seems like my expectations for improvement in personnel expenses due to ongoing digitalization may take a while to materialize. I have also come across analysts flagging cost pressure e.g. from additional vehicle features (Notion-Analysts opinions). Some press reports also flag gross margin pressure (Notion-ekathimerini article).

Proposed CO2 regulation: The EU Commission is drafting a regulation that would ban rental companies from purchasing internal combustion engine (ICE) vehicles starting in 2027 or 2030. Although the likelihood of it passing is low, the surrounding uncertainty could weigh on the share price in the short term.

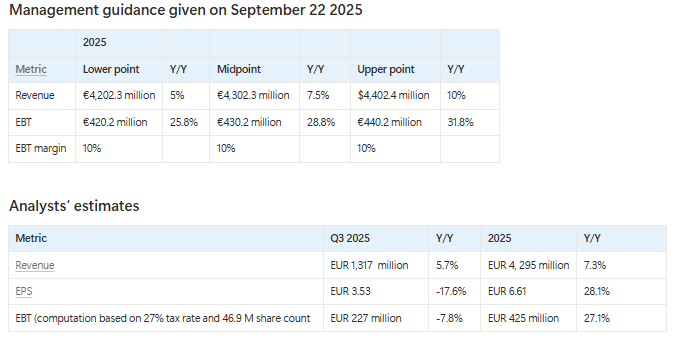

Here are analysts estimates for Q3 2025 and FY2025:

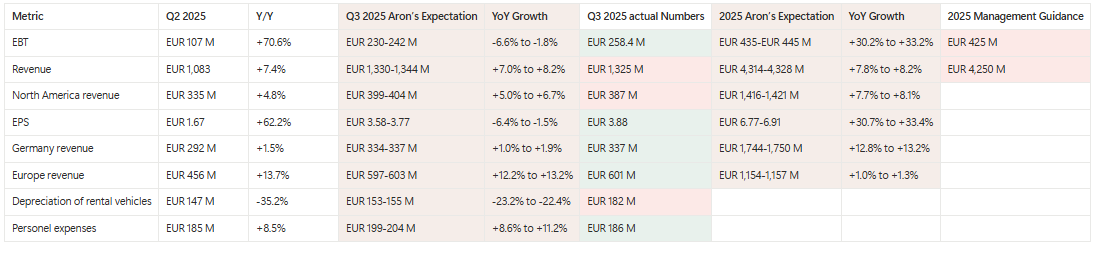

Sixt Q3 2025 revenue rose 6.6% y/y to EUR 1,325 million (analysts’ estimate: EUR 1,317 million), EBT rose 4.9% y/y to EUR 258.4 (analysts estimate: EUR 227 million) while EPS came in at EUR 3.88 (calculated in Valuation Model-Google Sheet) versus analysts estimate of EUR 3.53 (Notion-Q3 analysts estimate).

Sixt now expects 2025 revenue to grow 6% y/y to EUR 4,250 million (previous guidance: EUR 4,202-4,404 million (+5% to +10%) ) and EBT margin of 10%-unchanged from previous guidance.

Sixt revenue from Germany rose 1.8% y/y to EUR 337 million, revenue from Europe rose 12.9% to EUR 601 million, revenue from North America rose 2% (up 6.6% FX-neutral (page 1 Q3 2025 report) to EUR 387 million.

Sixt pointed to weak macro sentiment in USA as a reason for slow growth in North America revenue, citing that the government shutdown is expected to cost USD 4.1 billion in travel spending (page 5 of Q3 2025 presentation).

Sixt also flagged vehicle recalls in USA, citing that vehicle recalls saw a record of 8.5 million in Q3 205 (page 5 of Q3 2025 presentation).

Sixt said it launched a rewards program in USA in October 2025 and plan to expand it across its corporate countries in 2026 (page 8 of Q3 2025 presentation).

EBITDA was flat y/y at EUR 542 million, largely driven by higher short-term leasing costs (increase of EUR 15 M) and airport commissions (increase of EUR 14 M) (page 12 of Q3 2025 presentation).

CFO Weinberger said Sixt’s business remains robust and sees no reason why the company should deviate from its strong profitability.

When asked about its German competitor Starcar which recently filed for bankruptcy (and searching for an investor), CFO Weinberger pointed Sixt’s own financial strength, including the recent expanded debt facility.

Starcar has about 1,100 employees, generated a revenue of EUR 511 million in 2024 (+49% y/y) but had a syndicated loan facility of up to EUR 240 million, which was subject to very strict covenants and secured by transfer of vehicles ownership.

Assessment

Sixt shares shed around 3% yesterday and are down 2% today probably due to the reduced guidance for 2025.

While revenue growth rate for Europe and Germany were in line with my expectations, revenue growth rate for North America was significantly below my expectation (Notion-Q3 2025 earnings).

Sixt’s depreciation decline rate was also slower than I expected, probably due to the impact of the huge vehicle recalls in the USA as seen by a 7% rise in depreciation of rental vehicles in North America (Valuation Model-Google Sheets).

While performance in North America makes sense due to the reduced consumer sentiment as a result of government shutdown makes sense, rising other operating expenses is concerning as it may signal return on leased vehicles is low (I will look more into this). However, I like that its revenue per vehicle per month is growing, up 1.5% in 9M 2025 versus flat growth in 9M 2024-indicating that the company’s strategy to keep tight flight is working (Valuation Model-Google Sheet)

Overall, I think Sixt is doing well. However, a deep understanding of its Balance Sheet and Cash Flows, especially as 2025 is another heavy infleeting year following the strong defleeting in 2024 and rising debt-up 16% to EUR 3.2 billion at the end of September 2025 (Valuation Model-Google Sheet)