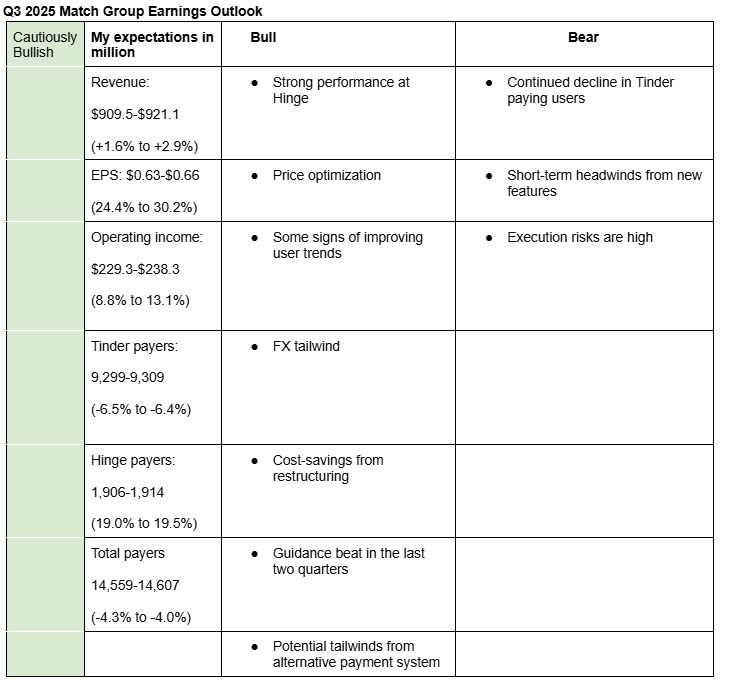

I am cautiously bullish on Match Group’s Q3 2025 earnings. My estimates (Google Sheets) take into account continued decline in Tinder paying users, strong performance at Hinge, FX tailwind, and revenue guidance beat in the last two quarters.

Here is a description of by bullish and bearish sentiments:

Bullish arguments:

- Strong performance at Hinge: Hinge continues to deliver strong performance, with its revenue growth more than offsetting the decline in Tinder’s revenue. In Q2 2025, Hinge’s revenue rose by $33.9 million while Tinder’s revenue fell by $18.7 million.

- Price optimization: Match Group optimized prices in Q2 2025 at Hinge, Tinder and Evergreen. Its CFO also said in the Q2 2025 earnings call (Notion) that they continue testing various merchandizing and monetization strategies. I expect these efforts to be the main driver of revenue growth in Q3 2025.

- Some signs of improving user trends: There are some signs that user engagement at Tinder is improving. According to Apptopia data which was reported by Global Dating Insights, Tinder’s daily active users (DAUs) in the US dropped by 5.4% y/y in Q3 2025, a deceleration from 8% in Q3 2024 (Notion). Similarly, according to Goldman Sachs, Tinder has begun seeing improvement in international user trends (Notion).

- FX tailwind: Match Group generates more than 55% of its revenue outside the U.S. As a result, the recent year over year strengthening of foreign currencies against the U.S. dollar should provide a tailwind in Q3. Management is guiding FX tailwind of 1% in Q3 2025. FX guidance for Q2 2025 had come in line with the guidance (Google Sheets), hence I also expect a 1% tailwind.

- Cost-savings from restructuring: New CEO Spencer Rascoff has centralized some functions and reduced the workforce by 13%. Management expects these changes to generate $45 million in cost savings in 2025 and $100 million annually starting in 2026.

- Guidance beat in the last two quarters: Match Group beat management’s upper point revenue guidance in Q2 2025 and Q1 2025 by an average of 0.3% (Google Sheets). Similarly, in the latest six quarters, it has missed management’s mid-point revenue guidance only twice, in Q4 2024 and Q3 2024.

- Potential tailwinds from alternative payment system: Match Group expect $65 million adjusted operating income tailwind from alternative payment system in 2026 (Notion). It also expect some tailwinds in 2025 (especially Q4). The alternative payment system’s tailwind will help compensate potential headwinds from the rollout of new features.

Bearish arguments:

- Continued decline in Tinder paying users: Despite some signs of improving user trends at Tinder, the app continues to lose users due to a combination of swipe fatigue, Gen Z’s need for authenticity, and competitive pressure (Google Sheets). Management does not expect this trend to reverse until new product initiatives begin gaining traction.

- Short-term headwinds from new features: Tinder recently announced that it will expand Facial Recognition Feature across the US in the coming months. Similarly, according to Morgan Stanley, Tinder is testing changes to its recommendation engine, potentially emphasizing relevance more than monetization (Notion). These changes are likely to cause customer churn in the short-term.

- Execution risks are high: The new CEO, Spencer Rascoff is championing for faster rollout of new features. According to internal reports, Tinder now ships code weekly compared to a twice-monthly schedule in the past. The swift rollout of new features may lead to buggy features. Similarly, he is making decisions quite fast, which may lead to poor decisions.

Here are management’s and analysts’ expectations for Q3 2025;

Management guidance for Q3 2025 revenue: $910-$920 million (+1.6% to 2.7%)

Management guidance for Q3 2025 adjusted operating income: $330-$335 million (-3.8% to -2.3%)

Analysts’ estimate for Q3 2025 revenue: $912.4 million (+1.9%).

Analysts’ estimate for Q3 2025 EPS: $0.64 (+25.5%).

Analysts’ estimate for Q4 2025 revenue: $882.1 million (+2.6%)

Analysts’ estimate for Q4 2025 EPS: $0.67 (+13.6%)

Confidence level and recommendation

My confidence level on the outlook is around 65% given the volatility surrounding the turnaround and the lack of enough insights on the quarter. As a result, I have a Hold rating on the stock. In the upcoming earnings call, I’ll be watching closely for updates on the product offensive, trends in Tinder’s user engagement, and other commentary on management’s execution.