This topic covers Bumble’s Q3 2025 earnings. A preview of the results will be posted here. For the full earnings preview and earnings call summary, see the Notion:

Earnings date: November 5, 2025

Time of Earnings release: 4:00 PM ET

Time of Analysts Call: 4:30 p.m. ET

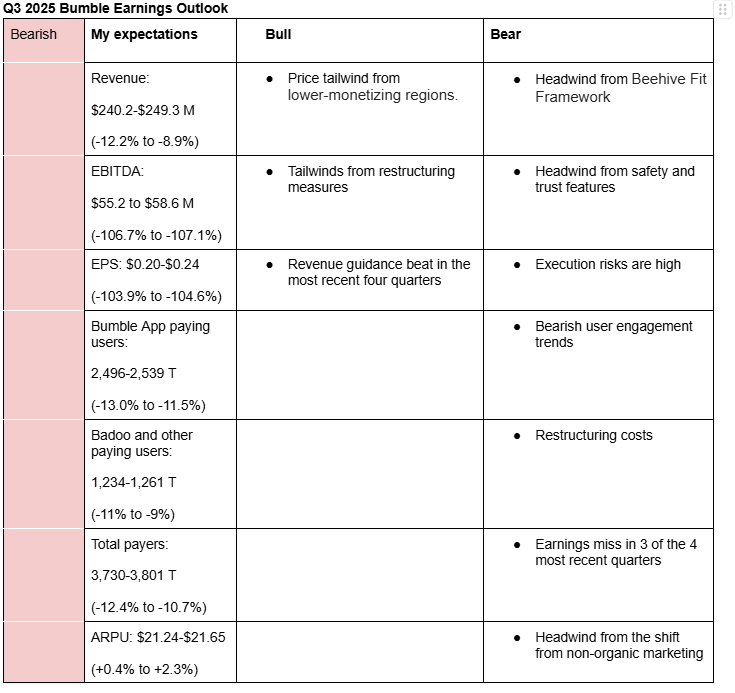

I am bearish on Bumble’s Q3 2025 earnings. My estimates (Valuation Model) are mainly based on user and pricing trends. Here is a description of my bullish and bearish sentiments:

Bullish arguments

Price tailwind form lower-monetizing regions: Bumble’s average revenue per user (ARPU) rose 1.5% in Q2 2025 due to optimization of pricing in lower-monetizing regions (Q2 Bumble Earnings). I expect this strategy to also play out in Q3 2025.

Tailwinds from restructuring measures: Bumble expects to generate annual savings of $40 million, beginning as early as the second half of 2025 from the 13% workforce reduction. It expects to save around $100 million from the whole restructuring process (Notion). The cost-savings will help offset the headwinds associated with the turnaround process.

Revenue guidance beat in the most recent four quarters: Bumble has beaten mid-point revenue guidance by an average of 1.9% in the most recent four quarters (Google Sheets).

Bearish arguments

Headwind from Beehive Fit Framework: Bumble is assessing payer quality through its Beehive Fit Framework, which classifies daters into three groups: approve (high-quality daters), improve (daters showing effort to enhance their profiles), and remove (low-quality users who make no effort to improve and should be removed). Remove payers make up less than 10% of the payers or less than 425,000 based on Q3 2024 total payers. If Bumble removed these payers in Q3 2025, then the decline in payers may be material.

Headwind from safety and trust features: Bumble launched a number of safety and trust features including phone and ID verification, and mandatory selfie checks in August. These features are expected to cause friction when signing in/up leading to user churn (Notion).

Execution risks are high: Almost every senior executive at Bumble is new. 8 out of 10 members of the executive management and around 40% of other senior executives have been with the company for less than 1 year (Notion). This could cause cultural shock, leading to slow rollout of new features.

Bearish user engagement trends: According to Apptopia data reported by Global Dating Insights, Tinder’s daily active users (DAUs) in the US dropped by 6.4% y/y (Q3 2024: +16%). The report also indicates that Gen Z usage of the platform dropped significantly (Notion). A report by Goldman Sachs also indicate adverse user trends for Bumble in Q3 (Notion).

Restructuring costs: Bumble expect to incur approximately $13 million to $18 million of non-recurring charges related to the 30% workforce reduction announced in June 2025. The charges will be incurred in Q3 and Q4 of 2025 (Notion).

Earnings miss in 3 or the 4 most recent quarters: Bumble has missed EPS estimates in 3 of the 4 most recent quarters (Google Sheets). I don’t expect this quarter to be an exception, especially with the ongoing volatility associated with the turnaround measures.

Headwind from the shift from non-organic marketing:The shift from non-organic marketing strategy i.e. the end of performance marketing may cause payer trends to decline in the near-term. This assessment is shared by a number of analysts (Notion)

Here are management and analysts estimates for Q3 and Q4 2025:

Q3 2025 management guidance for revenue: $240-$248 million (-12.3% to -9.4%).

Q3 2025 management guidance for adjusted EBITDA: $79-$84 million (-4.4% to 1.7%).

Q3 2025 consensus analysts estimate for revenue: $244.8 million (-10.5%).

Q3 2025 consensus analysts estimate for EPS: $0.34

Q4 2025 analysts estimate for revenue: $233.3 million (-10.8%)

Recommendation

Given the volatility around the turnaround measures, I don’t expect any significant improvement in revenue and earnings in the near-term. As I result, I recommend a Hold rating as we wait for more insights on the product rollout (and their benefits) as well management’s execution.

If you try to reconcile your EBITDA expectation of $55-58M and compare it with management guidance for adjusted EBITA of $79-$84M are the two numbers approximately in line? In other words by what does management adjust and how large are the adjustments? If there is a difference between your expectation and management expectation what causes it?

Do you have a theory why your EPS expectation of $0.20-0.24 cents is considerably smaller than the expectation of analysts? Like which items do you see differently?

What makes you expect that ARPU can again be adjust upwards? (I think i remember that the commentary in the Q2 2025 call was more that it was more like one off-adjustments but i could be wrong and it is a continuous thing)

Do you think that Bumble would cancel any paying users? From my understanding they want to get rid of the button 10% of users (often non paying) but not of the paying ones. If they would indeed cancel so many paying users wouldn’t the hit the Q3 2025 revenue be way larger?

How credible to you think Apptopia data is?

I also noted down a question directly in the valuation model.

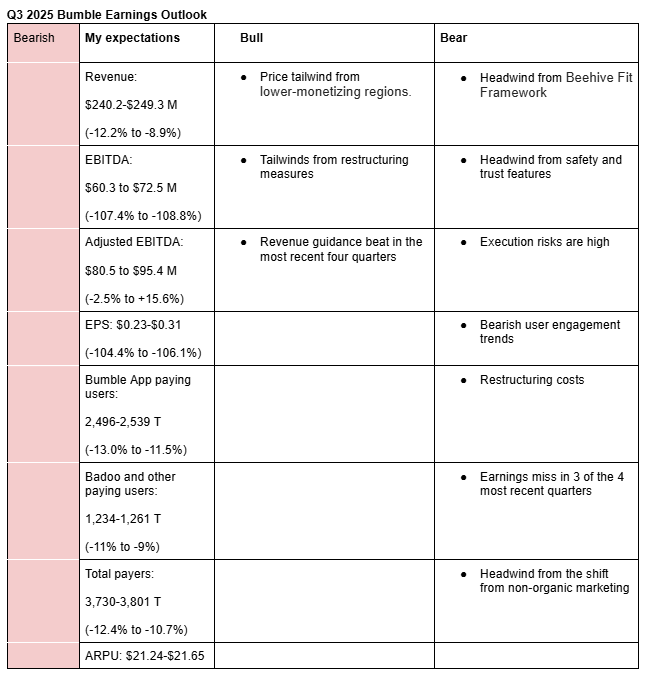

I have raised my estimates upwards after I realized management booked $13.9 million of the restructuring cost in Q2 2025, meaning balance is now around $4 million only (Adjusted EBITDA-Notion). However, my midpoint EPS estimate is still around 0.07 less than consensus. My guess is that analysts already expect larger restructuring cost-savings to flow through this quarter. My new estimates (Valuation Model) are shown in the screenshot below:

My adjusted EBITDA estimate is in the range of $80.5-95.4 million (management guidance: $79-$84 million). What could cause deviation from my estimate and that of management is the changes in interest rate swaps, which I didn’t spend much time studying (Adjusted EBITDA Estimate-Valuation Model)

Based on Herd’s commentary (Q2 2025 earnings call-Notion), the phase out of promotions in lower-monetizing regions seems not to be a one time thing, hence improving ARPU in the coming quarters. There was also some pricing optimization.

“The majority of this quarter’s payer decline came from the phase out of a legacy strategy related to promotions, which were skewed towards certain of our lower monetizing noncore markets. As of late April, we have been reemphasizing our core of sustainable full-price subscriptions,” she said in Q2 2025 earnings call.

“So on the our PPU our PPU growth, I mean, think it it was a result of some deliberate changes that we we had made in in the monetization and some pricing optimization,” Fior said.

Yes you are right, the 10% are likely to be the non-paying users. Wolfe Herd described them as bots, scammers and duplicates but she expects removing them to lead to a near-term headwind to the payers.

According to GPT, Apptopia is reliable as a directional source for user trends. However, its breadth is lower than that of Sensor Tower. Personally, I have come across analysts mentioning it when referring to user trends for Meta Platforms (Apptopia Research-Notion).

Bumble’s Q3 2025 (press release) revenue fell 10% y/y to $246.2 million, above analysts’ estimate of $244.8 million and in-line with management’s upper point guidance, adjusted EBITDA was $83.1 million (+0.6% y/y), slightly below management’s upper point guidance of $84 million while diluted EPS was $0.33, in line with analysts’ estimate.

Total payers fell 16% y/y to 3.58 million, significantly below my estimate of 3.77 million at the midpoint while total average revenue per paying user (ARPU) rose 6.6% y/y to $22.64, driven by ARPU at Bumble app which rose 10.5% to $28.27.

It guides Q4 2025 revenue in the range of $216-224 million (-17.5% to -14.5% y/y), significantly below our estimate of $237 million and adjusted EBITDA in the range of $61-65 million (-15.9% to -10.4% y/y).

The company announced amendment to its Tax Receivable Agreement (TRA) with Blackstone and Whitney Wolfe Herd, resulting in a $186 million settlement to terminate all payment obligations under the TRA- a process that is expected to improve Bumble’s cash flow, reduce long-term obligations, and provide strategic flexibility for future growth initiatives.

In the earnings call, management said trust and safety measures as well as reduction in marketing spend contributed 80% decline in payers (Real Time Earnings Call Notes-Notion).

Management also said in the earnings call that it expects sequential decline in paying users to improve in early 2026 as it largely complete their trust and authenticity work.

CEO Wolf Herd said they have started internal testing of the standalone AI product app that is powered by deep human connection but didn’t not provide the date of its launch.

Assessment

While Q3 2025 revenue and earnings met expectations, I don’t like that revenue was driven by growth in ARPU, especially at this time when industry sentiment is negative and the company is pursuing trust and safety measures. ARPU growth may not be sustainable in the near-term.

The fact that 80% of the decline in payers was due to trust and safety measures and decline and marketing spend makes me a bit optimistic that next year’s payer decline might improve. I also like that they continue to reduce costs, helping compensate for some or most of the revenue decline. For instance, 2025 revenue could decline by $100 million, but that will be largely compensated by cost savings.

However, execution risk remains high. Earlier reports indicated that they plan to launch the Stand-alone AI App at the end of 2025 but the fact that she didn’t indicate the timeline in Q3 call signals there may be delays.

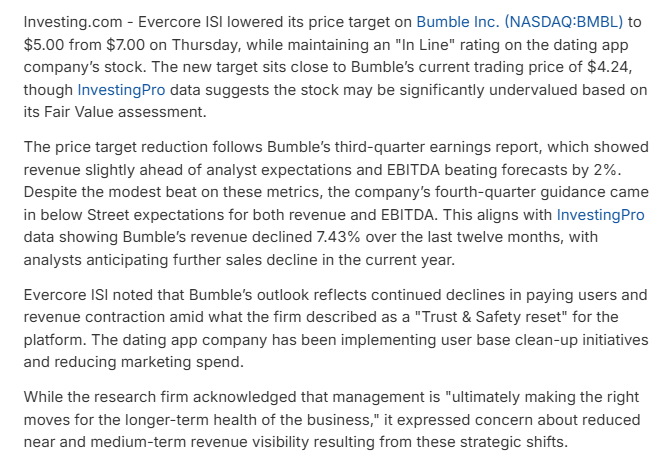

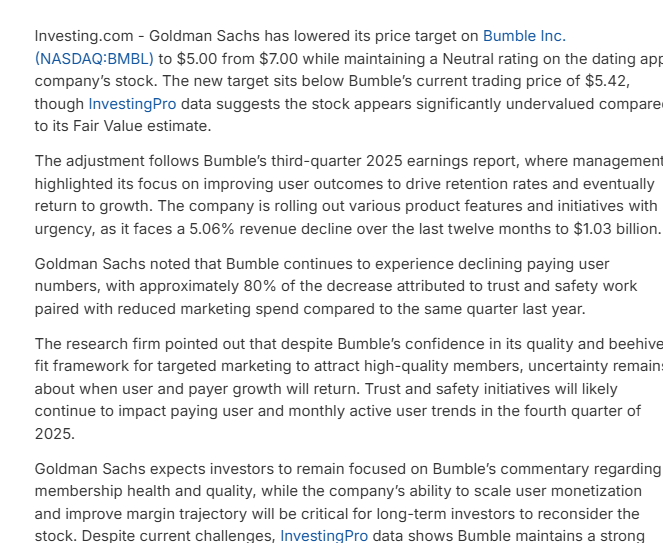

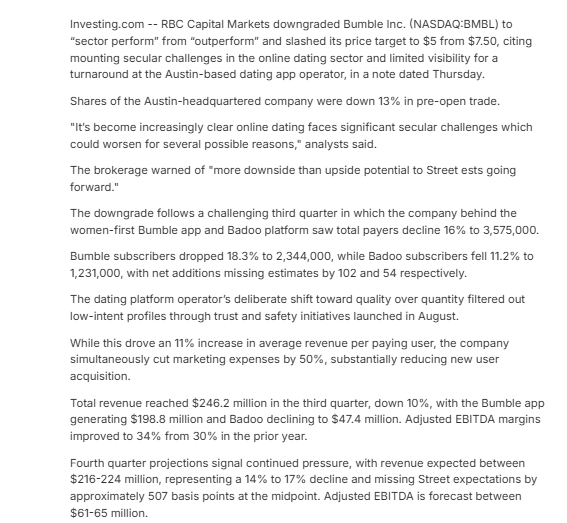

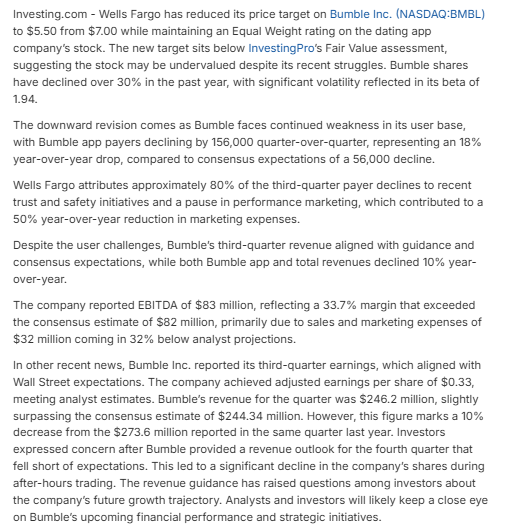

Analysts lowered rating on Bumble due to declining payers

In Line, $7->$5: Evercore expressed concerns that declining marketing spend and platform clean-up initiatives reduces near and medium-term revenue visibility.

Details

Outperform->Sector perform, $7.5->5: RBC said dating challenges could worsen for several possible reasons. It warned that street estimates could be lowered further.

Details